Breast Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

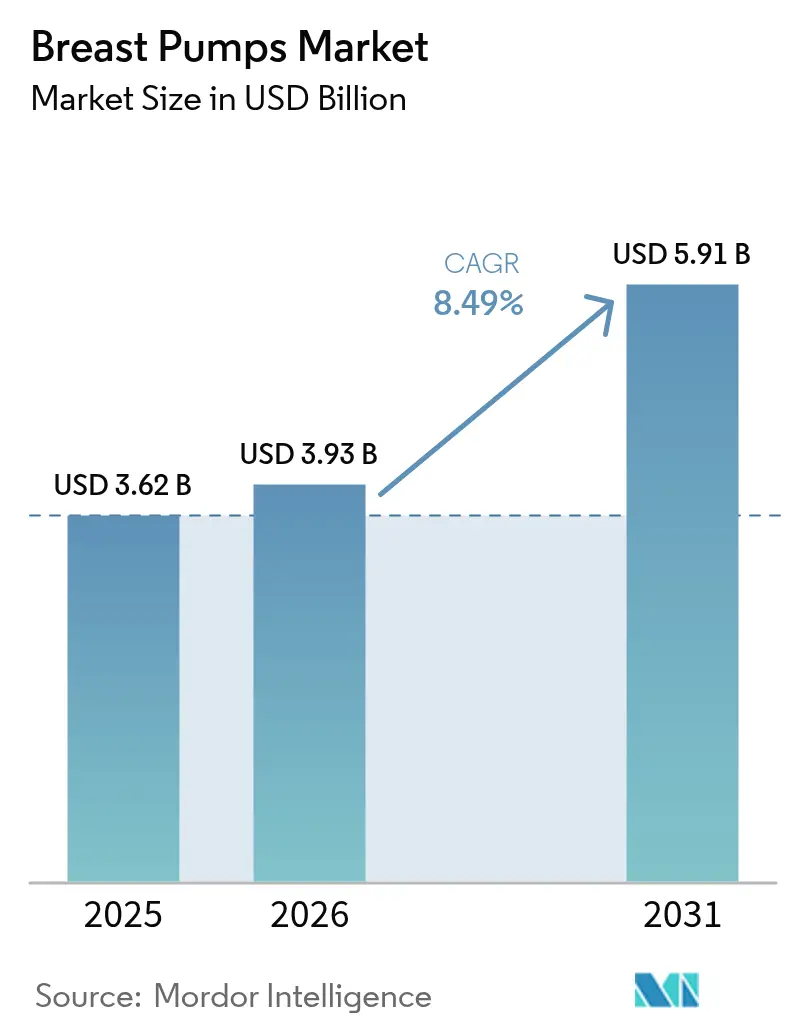

| Market Size (2026) | USD 3.93 Billion |

| Market Size (2031) | USD 5.91 Billion |

| Growth Rate (2026 - 2031) | 8.49% CAGR |

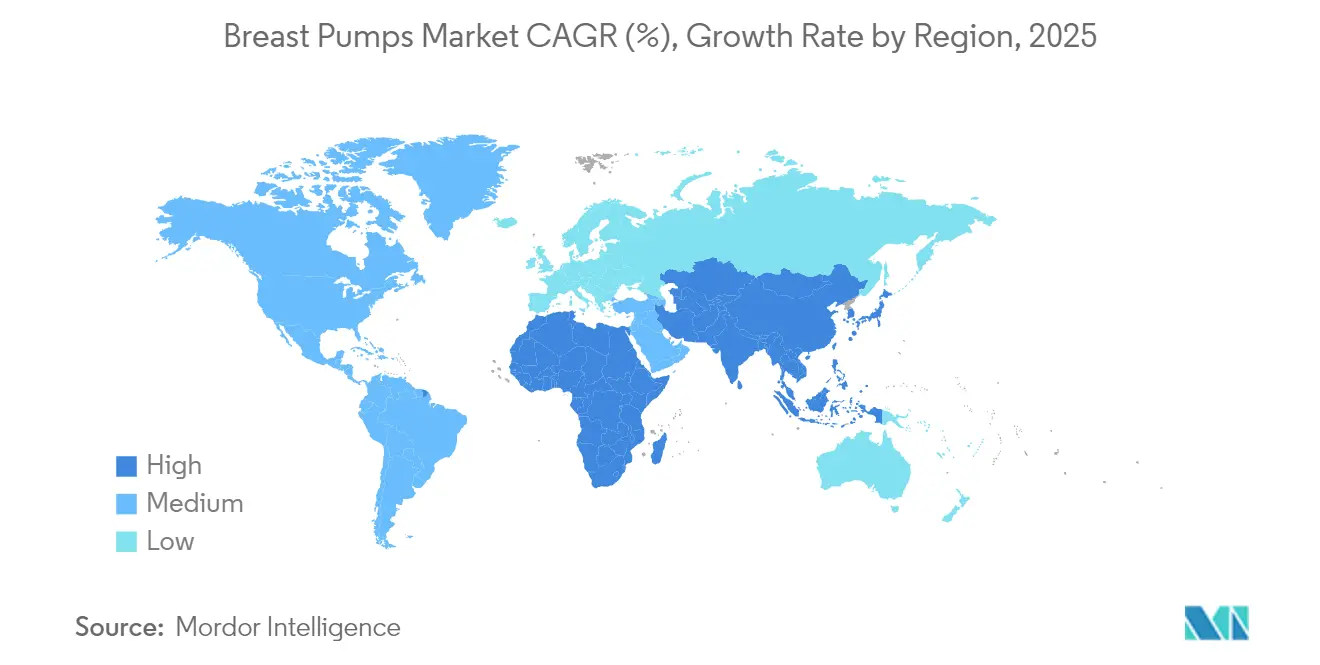

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

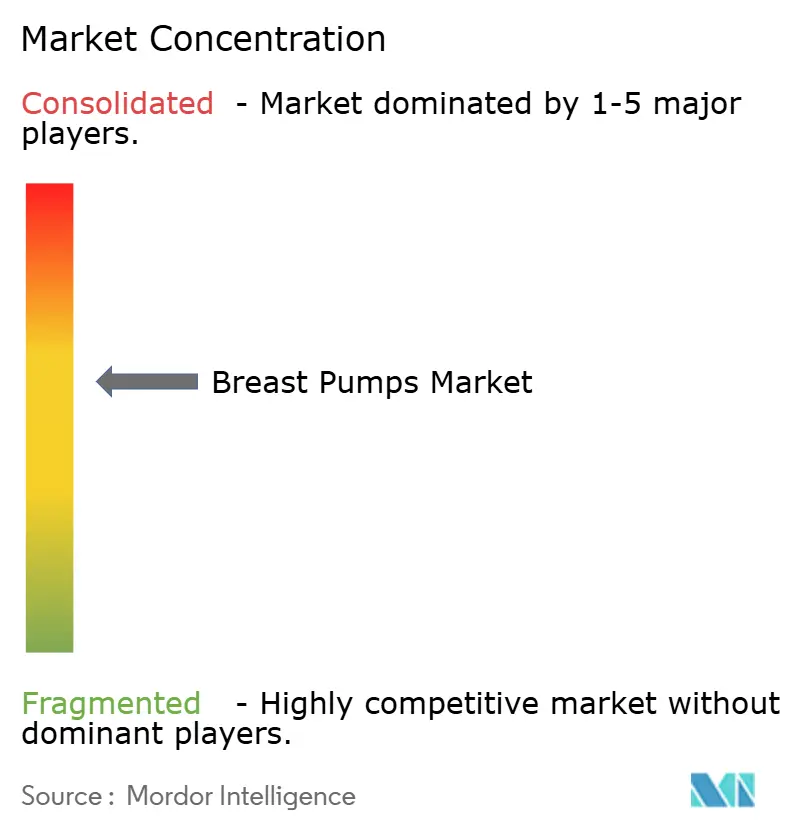

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Pumps Market Analysis by Mordor Intelligence

The breast pumps market size was valued at USD 3.62 billion in 2025 and estimated to grow from USD 3.93 billion in 2026 to reach USD 5.91 billion by 2031, at a CAGR of 8.49% during the forecast period (2026-2031). Across every major region, three structural forces—workplace lactation mandates, hands-free wearable innovation, and direct-to-consumer e-commerce—are expanding access to modern pumping solutions. Employers covered by the Pregnant Workers Fairness Act must now provide reasonable lactation accommodations, so corporate demand for closed-system electric models keeps building. Meanwhile, AI-enabled, app-linked pumps transform home routines and encourage premium upgrades. On-line sales channels simplify insurance reimbursement, lower mark-ups, and shorten delivery times, all of which enlarge the overall addressable base. At the same time, governments from Washington to Seoul continue earmarking maternal-health funds, which fosters R&D activity and accelerates regulatory clearances.

Key Report Takeaways

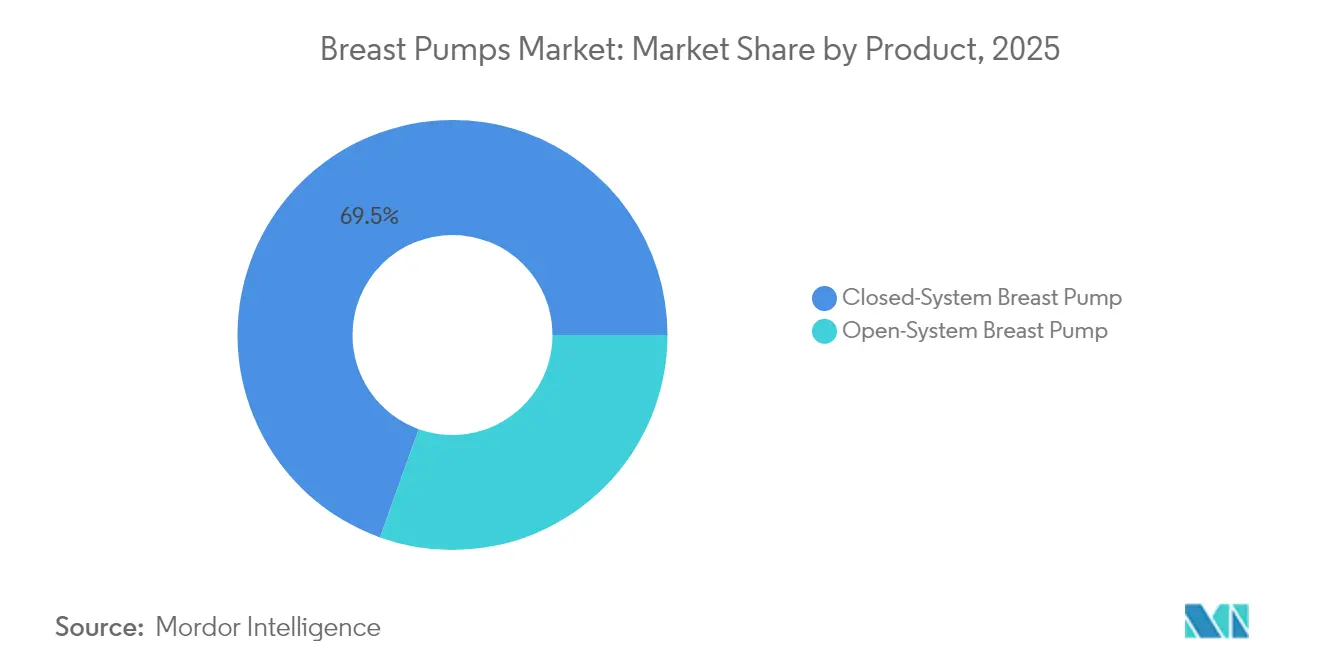

- By product type, closed-system pumps led with 69.52% revenue share in 2025; open-system units are growing more slowly but still serve select single-user niches.

- By technology, electric pumps held 60.74% of the breast pumps market share in 2025, while battery-powered variants are forecast to post the fastest 9.41% CAGR through 2031.

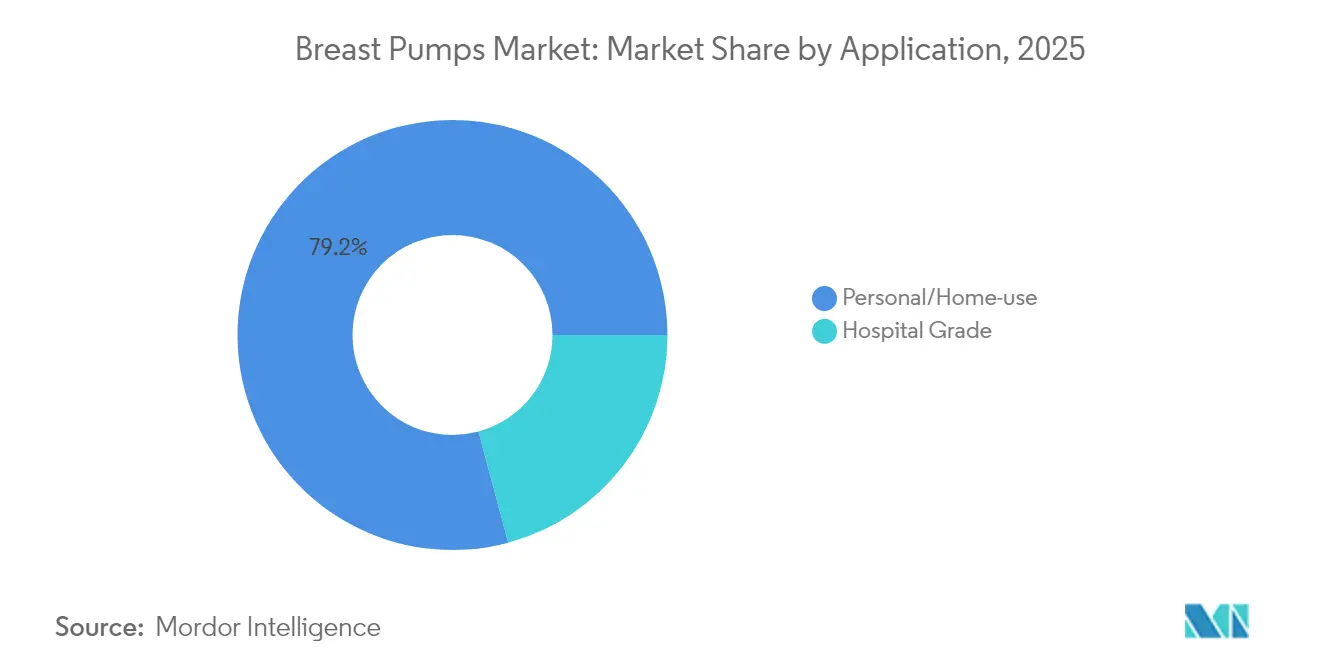

- By application, personal/home use accounted for 79.18% of the breast pumps market size in 2025, whereas hospital-grade applications are expanding at a 10.31% CAGR through 2031.

- By distribution channel, on-line platforms captured 48.12% of sales in 2025 and are accelerating at a 12.02% CAGR to 2031.

- By geography, North America commanded 35.12% of global revenue in 2025; Asia-Pacific is advancing at a 9.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breast Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global female-workforce participation | +1.8% | Global; APAC concentration | Medium term (2-4 years) |

| Expansion of maternity-leave and lactation-room mandates | +2.1% | North America and EU; expanding to APAC | Short term (≤2 years) |

| Rapid e-commerce penetration for mother-and-baby products | +1.5% | Global; led by North America and China | Short term (≤2 years) |

| Accelerating adoption of hands-free wearable pumps | +2.3% | North America and EU; premium global segments | Medium term (2-4 years) |

| ESG-led shift toward BPA-free silicone kits | +0.9% | Developed markets | Long term (≥4 years) |

| AI-enabled lactation-tracking ecosystems | +1.2% | North America and EU early adoption; APAC to follow | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Global Female-Workforce Participation

Rising labor-force participation keeps expanding the breast pumps market because working mothers need efficient pumping tools during office hours. A 2024 cross-sectional study found exclusive-breastfeeding rates of 20.36% in U.S. states with paid family-leave laws versus 18.48% in states without such support.[1]Julia Rosenberg, Deanna Nardella, and Veronika Shabanova, “State Paid Family Leave Policies and Breastfeeding Duration: Cross-Sectional Analysis of 2021 National Immunization Survey-Child,” International Breastfeeding Journal, biomedcentral.com These differences translate directly into demand for portable, hospital-strength devices that help women meet lactation goals while maintaining careers. Consumer-goods leaders such as Nestlé have added maternal-nutrition SKUs in India and Southeast Asia, signaling private-sector confidence in sustained growth. As more women enter office, retail, and manufacturing jobs, the need for reliable, closed-system electric pumps rises steadily.

Expansion of Maternity-Leave & Lactation-Room Mandates

Regulators on both sides of the Atlantic boosted demand by stipulating access to lactation spaces and equipment. The Pregnant Workers Fairness Act obliges U.S. employers to supply reasonable accommodations for pumping activities.[2]Food and Drug Administration, “Implementation of the Pregnant Workers Fairness Act,” Federal Register, federalregister.gov European directives push similar reforms, and corporate compliance is driving bulk procurement of multi-user hospital-grade pumps. Turn-key pod providers such as Mamava report a broad uptick in workplace installations, underlining how policy creates predictable demand. Longer paid-leave durations also stretch the overall pumping period, reinforcing replacement purchases and accessory sales.

Rapid E-Commerce Penetration for Mother-and-Baby Products

Direct-to-consumer websites now account for nearly half of global revenue because they remove intermediary costs and integrate seamlessly with insurance platforms. On-line channels are growing at 12.34% per year, well ahead of brick-and-mortar stores. Yet counterfeit accessories remain a real threat, especially on open marketplaces that lack robust vetting. U.S. regulators cite traceability gaps on inbound parcels from overseas sellers, putting pressure on authorized distributors to emphasize authenticity guarantees. Strong margins and data-driven marketing continue to entice manufacturers toward e-commerce expansion.

Accelerating Adoption of Hands-Free Wearable Pumps

Wearable pumps have reshaped user expectations by enabling discreet expression without interrupting daily activities. Medela’s Swing Maxi hands-free unit delivers 11.8% more milk output than older models, while Willow’s 3.0 design offers 360-degree mobility with full app control.[3]Medela, “Swing Maxi Hands-Free Electric Breast Pump,” Medela, medela.com Hardware advances coupled with digital analytics motivate premium pricing and stimulate frequent upgrades. Journalists have noted how insurance coverage meets cutting-edge design to unlock a new era of consumer-focused pumping solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device cost vs. manual expression | -1.4% | Global; strongest in emerging markets | Short term (≤2 years) |

| Supply-chain exposure to medical-grade plastics price swings | -0.8% | Global manufacturing; concentrated in APAC | Medium term (2-4 years) |

| Counterfeit accessories on on-line marketplaces | -0.6% | Global e-commerce; highest in unregulated markets | Short term (≤2 years) |

| Data-privacy concerns around connected pumps | -0.4% | North America and EU; spreading worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device Cost vs. Manual Expression

Premium wearable units can exceed USD 400, which restricts uptake among price-sensitive shoppers. Insurance typically covers only basic electric models, so advanced app-linked features often still require out-of-pocket spending. While cost-of-ownership studies favor electric pumps on time savings, many families in low- and middle-income economies still view manual expression as more economical despite higher physical strain.

Supply-Chain Exposure to Medical-Grade Plastics Price Swings

Medical-device makers report logistics and resin costs equal to 20% of revenue. PTFE and cyclic-olefin copolymer shortages, amplified by geopolitical friction, disrupt production schedules and raise end-user prices. The FDA’s Office of Supply Chain Resilience is tasked with smoothing inventories, yet near-term volatility persists, forcing many firms to stockpile raw material or embrace 3-D printing to buffer shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product – Closed-System Dominance Reflects Safety Priorities

Closed-system pumps commanded 69.52% of revenue in 2025, and their CAGR out to 2031 is pegged at 9.96%. Contamination-prevention backflow barriers satisfy strict NICU protocols, which amplifies institutional orders. The Medela Symphony PLUS, designed for multi-user hospital programs, epitomizes this safety-first trend. Open-system pumps still appeal to budget-focused families because of lower acquisition prices, yet their share keeps sliding as insurers upgrade reimbursement schedules to include closed architectures.

In consumer environments, parents increasingly select closed-system kits even for occasional use because they want hospital-grade hygiene at home. Greater awareness of infection-control guidelines, broadcast through pediatric-society advisories, reinforces that preference. Manufacturers now emphasize easy-to-sterilize components and spill-proof diaphragms in marketing copy, which further strengthens closed-system adoption.

By Technology – Electric Pumps Lead Innovation Wave

Electric designs held 60.74% of global revenue during 2025. They promise hospital-strength suction, programmable cycles, and superior milk output. The electric segment’s 8.88% CAGR reflects continual motor-efficiency improvements and widening battery-life ranges. Manual pumps retain appeal for travel and silent operation but face gradual displacement as electric price points fall.

Battery-powered units bridge the gap between wall-plug performance and wearable freedom. New entrants are merging brushless DC motors with compact lithium-polymer cells, trimming weight without reducing suction. Smart-sensor feedback loops provide real-time pressure adjustments, and companion apps log output in graphical dashboards. These upgrades position electric formats as the default choice for both first-time and experienced users.

By Application – Personal Use Dominates While Hospital Adoption Accelerates

Personal/home pumps represented 79.18% of the breast pumps market size in 2025, a figure bolstered by insurance mandates that cover at least one electric unit per birth. Social-media communities amplify best-practice sharing, motivating mothers to schedule regular pumping sessions and purchase aftermarket parts.

Hospital-grade equipment, however, is climbing at a 10.31% CAGR through 2031. NICU administrators appreciate multi-user durability and higher vacuum consistency, which help establish supply for preterm infants. Formal lactation-consultant programs, such as those in Mumbai’s public hospitals, validate the clinical impact of guided pumping routines and reinforce capital purchases of high-end systems.

By Distribution Channel – E-Commerce Transformation Accelerates

On-line portals captured 48.12% of 2025 revenue and are set to overtake physical outlets before 2027. Digital storefronts integrate eligibility checks with insurers, allowing same-day approvals and swift dispatch. Influencer reviews plus user-generated content serve as persuasive selling tools and cut customer-service costs.

Brick-and-mortar pharmacies and baby boutiques still matter, especially for first-time parents who prefer hands-on demonstrations. Retailers are responding with hybrid models where shoppers order on-line but collect in-store, ensuring authenticity and immediate pickup. Regulatory oversight, such as the Consumer Product Safety Commission’s 2025 nursing-pillow standard, underscores the need for compliant product assortments across every channel.

Geography Analysis

North America retained 35.12% of global revenue in 2025, propelled by insurance reimbursement, strict employer accommodations, and high per-capita disposable income. The breast pumps market size in the region is forecast to reach nearly USD 2.09 billion by 2031. Federal funding has also spurred R&D around AI-enabled lactation monitoring, which feeds premium adoption rates.

Europe ranks second thanks to generous maternity-leave statutes and a culture that values breast-feeding. Competitive intensity is rising after Willow acquired Elvie’s assets, consolidating wearable intellectual property under a U.S. brand umbrella. Sellers who emphasize data security and CE-mark compliance hold an edge with regulatory bodies.

Asia-Pacific stands out with a 9.78% CAGR and is on track to narrow the gap with mature Western markets. South Korea’s KRW 10 trillion healthcare overhaul reserved funds for maternal-care devices, and India’s swelling female-workforce base underpins steady urban demand. Multinationals like Nestlé invest aggressively in regional product localization, including pumps engineered for smaller body frames and local voltage standards.

Latin America and the Middle East & Africa are earlier in the adoption curve yet exhibit strong e-commerce growth. Local distributors often bundle pumps with prenatal vitamin kits to overcome lower brand recognition. Incentive programs run by health ministries in Brazil and the Gulf Cooperation Council frame breast-feeding as a national health priority, indirectly stimulating pump purchases.

Regulatory Landscape

Breast pumps are regulated as medical devices in most major markets, which affects time-to-market and the depth of required documentation by technology type. In the United States, the FDA classifies powered breast pumps as Class II devices (21 CFR 884.5160, Product Code HGX) that generally require 510(k) premarket notification, while nonpowered manual breast pumps fall under Class I (21 CFR 884.5150) and are generally exempt from premarket notification when conditions for exemption are met.

In Europe, electric breast pumps are governed under the Medical Device Regulation (EU) 2017/745 (MDR) and are commonly treated as Class IIa active devices, which brings notified-body conformity assessment and post-market obligations into commercialization planning. In China, the NMPA regulates breast pumps under its medical-device registration regime (including requirements aligned to the Regulations for the Supervision and Administration of Medical Devices, State Council Order No. 739), with technical standards such as QB/T 5136-2017 referenced for automatic breast pumps; in October 2025, a new quality classification specification (T/IGIA 029-2025) for infant automatic breast pumps was issued, indicating tighter performance and quality differentiation benchmarks for suppliers operating in the country.

Value Chain Analysis

The value chain runs from component sourcing (motors/miniature diaphragm pumps, PCBAs, lithium-ion battery packs, and medical-grade silicone contact parts such as flanges and valves) to device design and manufacturing (tooling, molding, electronics integration, and assembly). It then extends through regulatory and quality compliance (QMS/technical files and testing), followed by channel execution through hospital procurement, retail, and rapidly scaling e-commerce with insurance-linked ordering. Manufacturing and subcomponent ecosystems are heavily concentrated in China, with electronics integration and development capacity clustered in Guangdong (notably Shenzhen, Dongguan, and Guangzhou) and cost-efficient component production concentrated in Zhejiang (including Ningbo and Cixi).

Downstream, distribution increasingly combines direct-to-consumer fulfillment with payer and durable medical equipment pathways, particularly for personal/home-use devices where reimbursement and delivery speed influence conversion. For brands selling into the United States and Europe, compliance work and traceability requirements pull more activity into final assembly, quality testing, labeling, and packaging steps that align with FDA classification and broader export-readiness standards, while core manufacturing remains outsourced to Asian supplier bases. In this setup, resin and medical-grade plastics volatility, accessory authenticity control on open marketplaces, and multi-sourcing of critical components become central to continuity planning.

Competitive Landscape

Competition remains moderate. Medela leverages hospital partnerships and ISO-13485 credentials to defend leadership, while Philips Avent cross-promotes pumps with bottle systems. Willow pushes the high-margin wearable niche and, after absorbing Elvie’s IP, aims for global scale in app-centric devices.

Ameda launched the GLO wearable in June 2025 to reclaim hospital-grade credibility in the consumer arena. Momcozy joined the race with the ultra-slim Air 1, further crowding the hands-free sub-segment. Supply-chain robustness is now a decisive factor; firms with multi-continent resin sources and in-house molding secure better fill rates during volatility. Post-market surveillance capabilities mandated under ISO/TR 20416 also favor incumbents that can manage field data efficiently.

Intellectual-property litigation is likely to intensify around suction technologies and flange ergonomics as the breast pumps industry innovates. Portfolio rationalization could continue, with mid-tier players seeking alliances to share software-development costs and regulatory burdens.

Breast Pumps Industry Leaders

Koninklijke Philips NV

Medela AG

Pigeon Corporation

Willow Innovations Inc.

Spectra Baby

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace area sits at the intersection of hands-free pumping, measurable milk-expression outcomes, and clinical protocols that can be translated into product features. In May 2026, peer-reviewed evidence in Acta Obstetricia et Gynecologica Scandinavica reported that a modified suction pattern (adding a 5-minute nutritive suction cycle after 15 minutes of standard suction) increased milk yield in the first four days postpartum, reinforcing demand for programmable cycles and evidence-aligned settings in electric and wearable pumps.

Another opportunity is tighter integration of pumps into organized maternal and neonatal care pathways and coverage expansion efforts. Scotland's 2025-2030 Breastfeeding and Infant Feeding Strategic Framework reported progress by June 2026, including full implementation of cue-based feeding and Kangaroo Care across multiple neonatal units, which supports hospital-grade adoption and standardization of lactation support workflows. In the United States, the FDA pathway remains clear for powered pumps as Class II devices (21 CFR 884.5160, Product Code HGX) and manual pumps as Class I (21 CFR 884.5150), while policy initiatives such as Vermont's 2026 H.691 bill (introduced) that proposes mandatory insurance coverage for breastfeeding equipment and lactation support highlight ongoing payer-policy activity that can widen access when manufacturers align products and distribution to coverage requirements.

Recent Industry Developments

- May 2026: Medela Insurance Connect launches, a digital route to access insurance-covered breast pumps. The platform centralizes verification and fulfillment across payer networks, strengthening the online and payer-linked channel for personal/home-use devices. This move mirrors growing payer-policy activity and could widen access as distribution aligns with coverage requirements.

- April 2026: Vermont's H.691 bill proposing mandatory insurance coverage for breastfeeding equipment and lactation support was introduced in the state legislature, signaling payer-policy momentum that could reshape reimbursement pathways for consumer and hospital-grade pumps. Stakeholders anticipate streamlined access for insured patients if enacted.

- June 2025: Ameda introduced the GLO Wearable Breast Pump, a clinician-led wearable system. The launch positions wearables more prominently in clinical workflows and consumer markets, raising feature and performance benchmarks for competing hands-free products.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from breast pump devices used to express milk, across home and hospital-grade use. It includes manual, battery-powered, and electric pumps sold through offline and online channels, and it is measured at global level in USD.

Scope exclusions: Excludes disposable or add-on nursing items such as storage bags, nipple shields, and single-use bottle liners.

Segmentation Overview

- By Product

- Open-System Breast Pump

- Closed-System Breast Pump

- By Technology

- Manual Breast Pump

- Battery-Powered Breast Pump

- Electric Breast Pump

- By Application

- Personal/Home-use

- Hospital Grade

- By Distribution Channel

- Offline Retail (Pharmacies, Baby-Stores)

- Online/E-commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand pool and the purchasing rules, especially for hospital-grade setups and reimbursed consumer pumps. We use public health and demographic series such as births and fertility indicators from sources like the World Bank and the United Nations, then we pair those with country health ministry releases that describe maternal and newborn care programs.

To ground the supply and trade side, we also review customs statistics and tariff schedules published by agencies such as the USITC and UN Comtrade, plus standards and safety references from bodies such as the FDA and ISO where applicable. Company filings, product brochures, investor presentations, and reputable press are reviewed to understand pricing ladders, channel mix, and product refresh cycles, and patent databases are checked to spot technology direction, for example wearable form factors and app connectivity. In some cases, we use paid subscriptions for company financials and for shipment-level import and export checks to validate scale. The sources listed here are illustrative only, since many other references are used for collection and cross-checking.

Primary Interviews and Surveys

Primary calls and short surveys are used to test the adoption curve and the price points that end users actually pay, which is not always visible in public sources. We speak with manufacturers, distributors, hospital procurement staff, lactation professionals, and retail or e-commerce channel participants across major regions, and then we adjust assumptions when consistent gaps show up between countries or channels.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | APAC: 47% |

| Mid tier: 52% | Functional/Unit leaders: 26% | EMEA: 35% |

| Smaller Players: 19% | Managers: 58% | Americas: 18% |

Market-Sizing & Forecasting

The core model is built using a top-down demand pool approach, where births by country and breastfeeding participation are used to reconstruct the addressable user base, and then pump penetration is applied for home use and institutional demand. After that, price bands are assigned by technology, manual, battery-powered, and electric, and by selling route, online versus offline, so the value outcome follows from a clear volume and ASP logic.

To keep the numbers practical, we cross-check totals using selective bottom-up approximations such as channel checks on unit sales ranges, sampled retail pricing, and supplier revenue disclosures where they are available. Inputs that matter for this market include annual live births, maternal employment rates, reimbursement coverage or benefit rules, hospital-grade rental versus purchase patterns, and the shift toward closed-system and wearable designs, since these can change both units and ASPs. For the forecast, we mainly use scenario analysis supported by year-by-year trend smoothing, so high-impact variables like reimbursement tightening or a faster move to wearables can be tested in a controlled way. When a country has limited visibility on unit splits, we use proxy ratios from similar markets and then re-check them with local interviews before finalizing.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals such as trade flows, published birth trends, pricing snapshots, and the interview feedback collected across regions and channels. If a country or segment result looks out of line, the drivers are re-tested, and we re-contact relevant participants to confirm whether the change is real or a modeling artifact.

Before sign-off, the file goes through step-by-step analyst reviews that check arithmetic consistency, unit economics, and year-over-year movements, and any large variance is documented with a clear reason. Reports are refreshed annually, and interim updates are triggered when material events occur, such as policy changes in reimbursement, major pricing resets, or meaningful channel shifts. Right before delivery, a final pass is completed so clients receive the most current version available.

Mordor Intelligence's Breast Pumps Market Size Versus Other Published Estimates

It is normal to see different market sizes for breast pumps because publishers do not always count the same product set, years, and pricing rules. The spread also comes from how demand is constructed, which can be based on births and penetration, or based on broader maternal care spending that indirectly pulls in adjacent items.

Some published figures roll nursing accessories and feeding add-ons into the same number, and that can lift the total even if pump units are similar. In Mordor Intelligence, the value is limited to breast pump devices only and excludes disposable nursing items, and currency timing and online price discounting are refreshed to reduce overstatement in fast-moving channels.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.93 B (2026) | |

| Global Consultancy A | USD 3.36 B (2025) | Uses a different base year and a longer horizon, and its published summary does not clearly separate pump device revenue from adjacent nursing and feeding items, which can change the effective scope and the implied ASP path. |

| Trade Journal B | USD 3.23 B (2024) | Often presented as a headline press estimate with limited visibility on channel-level pricing and reimbursement effects, and the year used is earlier, which can understate markets where online mix and wearable adoption rose quickly after 2024. |

Reading the three numbers together, the main takeaway is that scope and year choice matter as much as the growth rate itself. By tying demand to births, usage penetration, and observable price bands, the market size becomes easier to replicate and to explain, and differences can be traced back to a small set of assumptions instead of opaque roll-ups.

Key Questions Answered in the Report

What is the current value of the breast pumps market?

The market is valued at USD 3.93 billion in 2026 and is forecast to grow to USD 5.91 billion by 2031.

Which product type holds the largest breast pumps market share today?

Closed-system pumps dominate with a 69.52% share because hospitals and parents both prioritize contamination prevention.

Why are wearable pumps growing so quickly?

Hands-free designs allow mothers to pump discreetly during work and daily tasks, and premium models integrate with mobile apps, driving a 2.3% positive impact on overall CAGR.

How big is the online channel for breast pumps sales?

E-commerce platforms now contribute 48.12% of global revenue and are expanding at a 12.02% CAGR thanks to direct-to-consumer logistics and simplified insurance reimbursement.

Which region is the fastest-growing?

Asia-Pacific is advancing at a 9.78% CAGR, supported by healthcare infrastructure upgrades and higher female-workforce participation.

What is the main barrier to smart-pump adoption in emerging markets?

High upfront prices relative to manual expression remain the biggest restraint, reducing projected CAGR by 1.4% in cost-sensitive segments.

Page last updated on: