Stem Cell Banking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

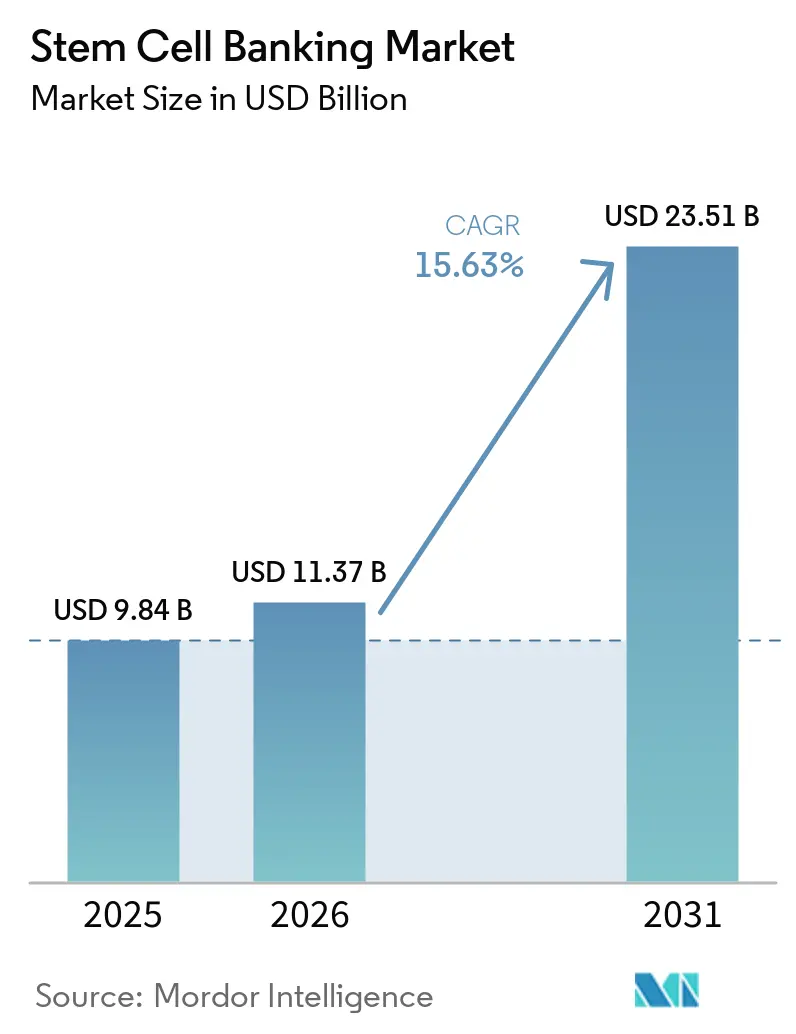

| Market Size (2026) | USD 11.37 Billion |

| Market Size (2031) | USD 23.51 Billion |

| Growth Rate (2026 - 2031) | 15.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stem Cell Banking Market Analysis by Mordor Intelligence

The Stem Cell Banking Market size was valued at USD 9.84 billion in 2025 and is estimated to grow from USD 11.37 billion in 2026 to reach USD 23.51 billion by 2031, at a CAGR of 15.63% during the forecast period (2026-2031).

The stem cell banking market is experiencing significant growth as preserved biological material becomes integral to long-term care planning, driven by advancements in cell and gene therapy programs nearing routine clinical use. Expanding therapeutic validation across hematological, neurological, and autoimmune applications is boosting confidence in the relevance of banked cord blood and perinatal tissues. Regulatory progress is further supporting the market by establishing clearer standards for human cells and tissue products, enabling operators to align collection, storage, and processing systems with clinical and industrial requirements. As a result, competition in the stem cell banking market is shifting focus from basic storage capacity to inventory quality, advanced processing capabilities, regulatory compliance, and support for both family banking and therapy development pathways.

Key Report Takeaways

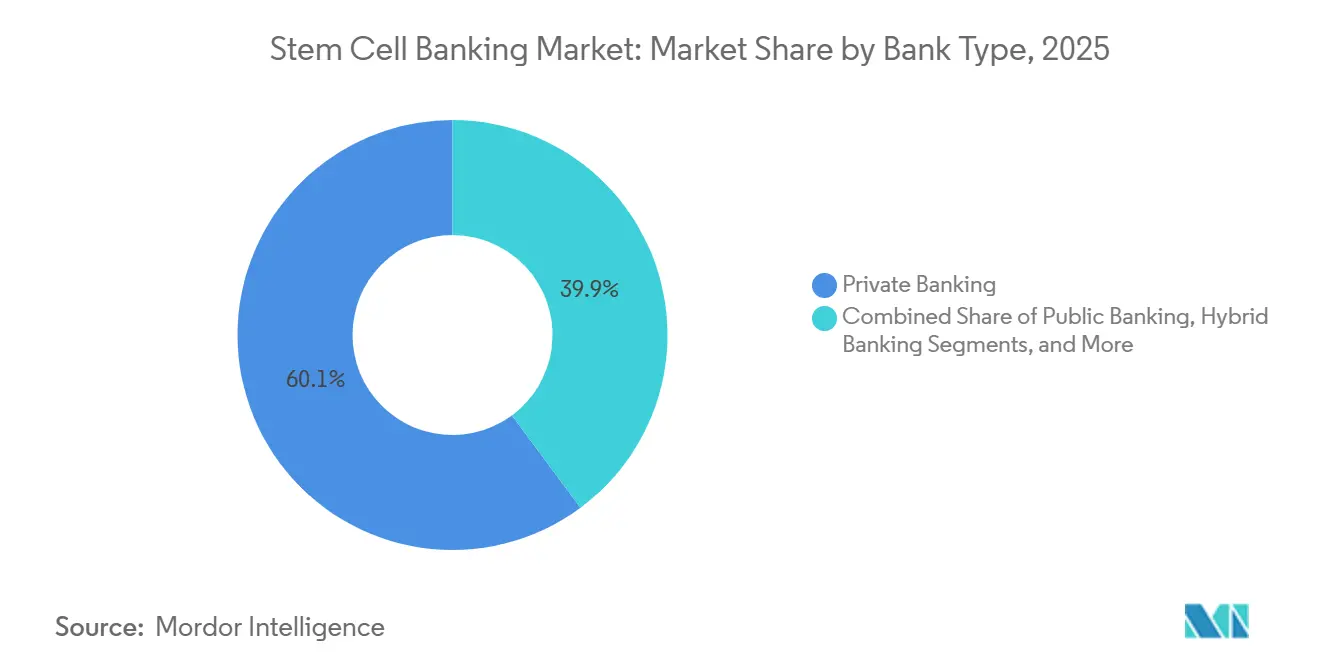

- By bank type, private banking held 60.15% of the stem cell banking market share in 2025, while hybrid banking is projected to record the fastest CAGR of 17.10% through 2031.

- By stem cell source, umbilical cord blood accounted for 45.25% of the stem cell banking market size in 2025, while adipose tissue-derived stem cells are forecasted to expand at a 17.20% CAGR through 2031.

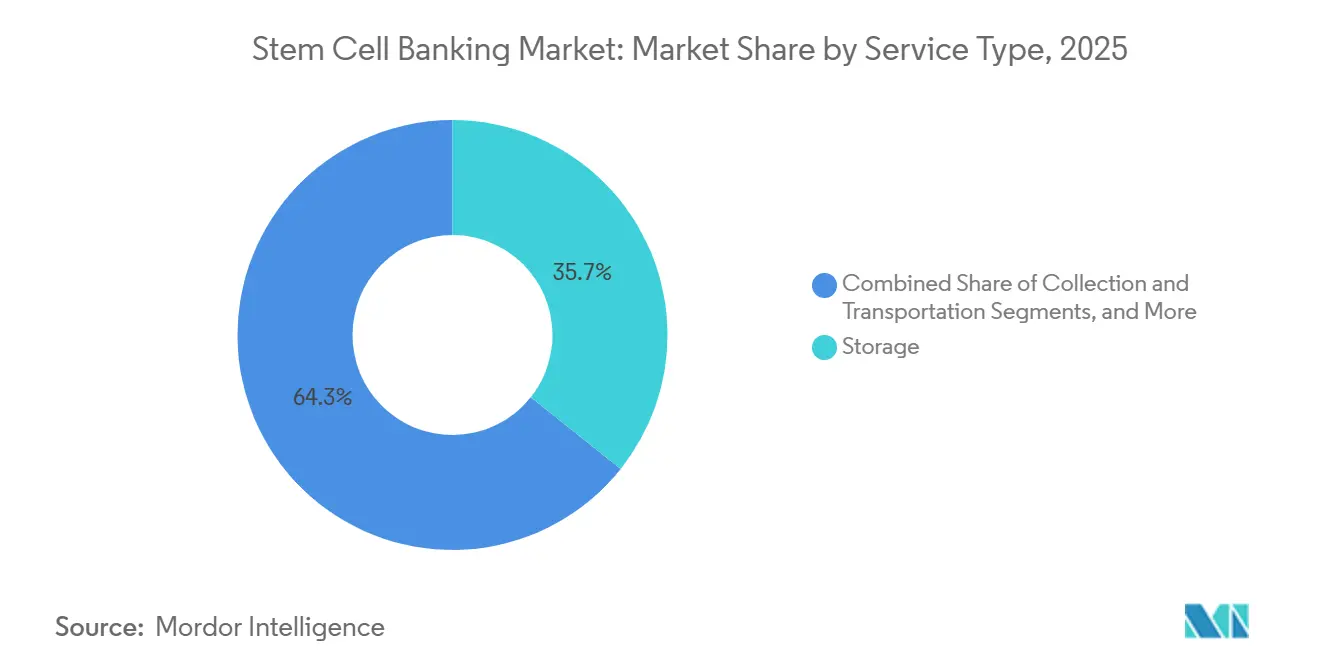

- By service type, storage services led with 35.66% share in 2025, while processing services are expected to grow at a 16.95% CAGR through 2031.

- By application, personalized banking represented 45.30% share in 2025, while research and drug discovery are expected to grow at a 17.25% CAGR through 2031.

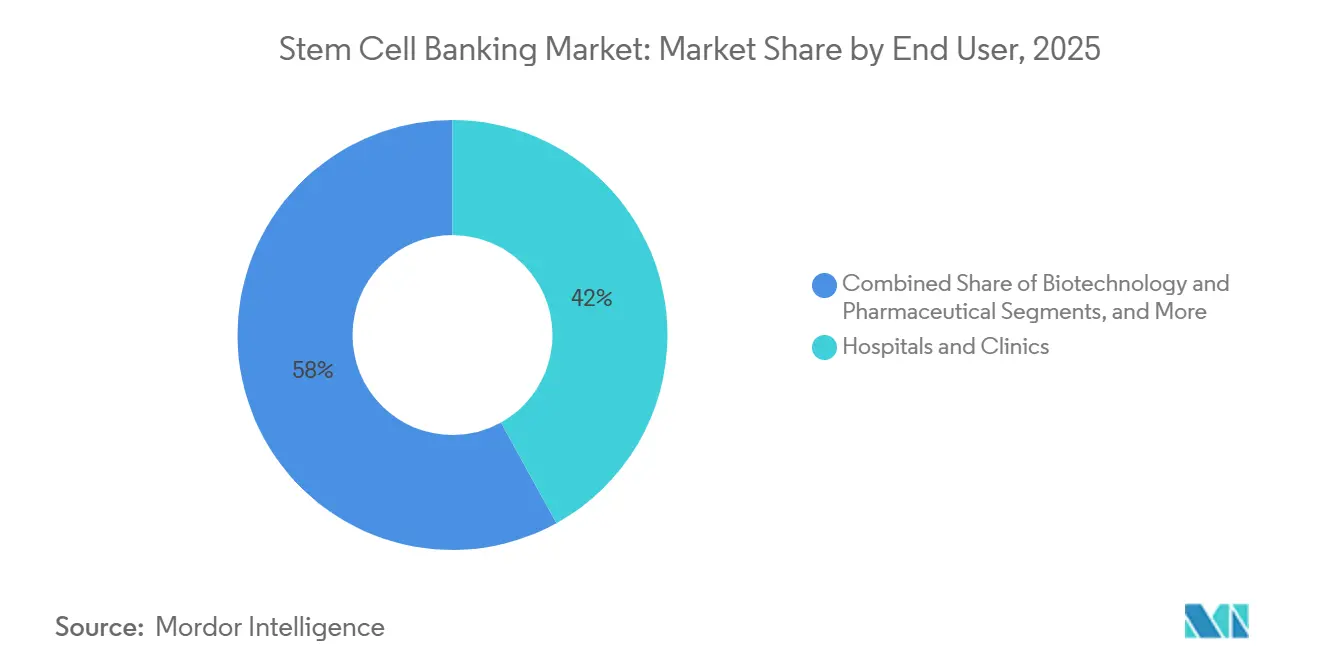

- By end user, hospitals and clinics held 41.95% share in 2025, while biotechnology and pharmaceutical companies are projected to grow at a 17.35% CAGR through 2031.

- By geography, North America retained 40.60% share in 2025, while Asia-Pacific is expected to post the fastest CAGR of 16.67% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stem Cell Banking Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for cord blood and cord tissue preservation | +3.5% | Global, with peak intensity in North America and APAC | Short term (≤ 2 years) |

| Expansion of regenerative medicine and cell therapy research | +3.2% | North America and EU, with spillover to APAC | Medium term (2-4 years) |

| Rising use of private family banking as a long-term healthcare option | +2.8% | APAC core, especially China and India, and North America | Short term (≤ 2 years) |

| Increasing acceptance of allogeneic stem cell transplantation | +2.0% | Global, especially the United States, Germany, and China | Medium term (2-4 years) |

| Rising banking of perinatal tissues beyond cord blood | +1.5% | North America, Western Europe, and Singapore | Medium term (2-4 years) |

| Automation and closed-system cryopreservation improvements | +1.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Cord Blood and Cord Tissue Preservation

The stem cell banking market is experiencing growth due to the expanded utility of cord blood, which is no longer limited to legacy blood cancer treatments. The approval of omidubicel-onlv for severe aplastic anemia in December 2025 marked a significant shift by introducing a chemically enhanced cord blood product to a new clinical setting and raising manufacturing standards. Similarly, cord tissue banking is advancing as mesenchymal stem cells from umbilical cord tissue demonstrate strong proliferative capacity and lower contamination risks under GMP-feasible production conditions. This scientific progress enables private operators to offer bundled cord blood and cord tissue services at birth, increasing revenue per family without altering collection methods. Demand is now driven by delivery-time awareness, counselor access, and clear communication of future-use value.

Expansion of Regenerative Medicine and Cell Therapy Research

The growing focus on regenerative medicine and cell therapy is driving demand for reliable biological materials, transforming stem cell banks into active supply platforms. Clinical programs now require standardized inventories rather than isolated units. For instance, a phase 2 trial demonstrated a 96% one-year survival rate and no severe graft-versus-host disease using pooled cord blood products, highlighting the importance of large, well-characterized inventories.[1]AABB Regulatory Affairs Committee, “Regulatory Update, AABB Releases New FDA eHCTERS Toolkit,” AABB, aabb.org Additionally, advancements in allogeneic hematopoietic stem cell transplantation for transfusion-dependent thalassemia are broadening demand for matched allogeneic units. This shift underscores the increasing relevance of pharmaceutical supply contracts and research procurement agreements alongside family subscriptions.

Rising Use of Private Family Banking as a Long-Term Healthcare Option

Private family banking remains the primary revenue driver in the stem cell banking market, accounting for a 60.15% share in 2025. Family-directed storage ensures steady subscription revenue and higher customer retention compared to donation-based models. The market is shifting toward premium multi-tissue enrollment, where families store cord blood, cord tissue, placental material, and related samples under a single plan. StemCyte International’s launch of an insurance-linked public cord blood access service in Taiwan in November 2025 demonstrated how hybrid pricing models can enhance affordability, boost enrollment, and maintain clinical access pathways. Successful operators are innovating with bundled offerings and flexible entry points rather than relying solely on traditional storage contracts.

Increasing Acceptance of Allogeneic Stem Cell Transplantation

Wider acceptance of allogeneic transplantation is expanding the stem cell banking market beyond traditional use cases. A 2024 randomized phase 3 trial revealed that combining haploidentical peripheral blood stem cells with unrelated cord blood improved disease-free and overall survival rates in hematological malignancies, strengthening the clinical value of well-matched cord blood units.[2]Swiss Stem Cell Biotech AG, “Hybrid Stem Cell Bank, Protect the Future Today,” Swiss Stem Cell Biotech AG, sscb-stembiotech.ch In 2025, Cellenkos received FDA clearance for a phase 2 trial of CK0801, an allogeneic cord blood-derived regulatory T-cell therapy for aplastic anemia, showcasing new immune-regulatory applications for cord blood. HLA-diverse populations, often underserved by conventional donor registries, continue to rely on cord blood access, ensuring the relevance of public and hybrid inventories as transplant methods evolve.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High lifetime cost of collection, processing, and storage | -1.8% | Global, most acute in South America and the Middle East and Africa | Short term (≤ 2 years) |

| Uncertain clinical utilization rate of stored units | -1.5% | North America and Europe, where litigation risk is highest | Medium term (2-4 years) |

| Regulatory complexity across public, private, and cross-border operations | -0.9% | Europe and APAC multi-jurisdiction markets | Medium term (2-4 years) |

| Limited donor awareness and birth-time conversion rates | -0.8% | Middle East and Africa, South America, and tier 2 and 3 APAC cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Lifetime Cost of Collection, Processing, and Storage

The stem cell banking market faces affordability challenges as private enrollment combines collection fees, processing charges, and long-term storage costs, making it a significant financial decision for families. This issue is more pronounced in high-birth markets where medical needs are high, but disposable incomes are limited, slowing market penetration despite growing awareness. Operators also face high costs due to compliance systems, testing, cryogenic infrastructure, and logistics. Hybrid and insurance-linked models are emerging to distribute costs across broader participation, easing entry for families. However, cost remains a key restraint, especially in balancing premium service standards with affordability in price-sensitive markets.

Uncertain Clinical Utilization Rate of Stored Units

The market is constrained by the low clinical utilization rate of privately stored units, which impacts how families and physicians perceive value. Overstated marketing claims, unsupported by evidence, increase skepticism and complicate renewal decisions as long-term contracts mature. Families often compare the likelihood of use against storage costs, while clinicians prioritize evidence-backed applications. Additionally, the rise of haploidentical peripheral blood transplantation has reduced unrelated cord blood procedures in some centers, making private storage seem less urgent. Stem cell banks must focus on credible clinical pathways, realistic use cases, and regenerative medicine to strengthen their value proposition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bank Type: Private Models Dominate, Hybrid Architecture Accelerates

In 2025, private banking accounted for 60.15% of bank-type revenue, highlighting the stem cell banking market's reliance on family-funded enrollments and recurring storage contracts. This model ensures predictable cash flow, supports upselling into multi-tissue packages, and reduces dependence on grants or public reimbursements. Personalized enrollment provides operators direct customer access, simplifying retention, renewals, and add-on services. While public and hybrid formats gain attention, private banking remains the commercial core due to families' willingness to invest in perceived long-term benefits when counseling, pricing, and hospital access align.

Public banking enhances transplant access, diversifies donor pools, and supports allogeneic treatment pathways reliant on well-matched inventories. Its importance grows in underrepresented populations where unrelated cord blood serves as a critical alternative. Hybrid banking, growing at a 17.10% CAGR through 2031, combines family value with broader clinical utility. Switzerland’s hybrid model and StemCyte’s insurance-linked initiative in Taiwan demonstrate how hybrid architecture can enhance affordability and participation while maintaining clinical quality.

By Stem Cell Source: Adipose Tissue Emerges as the High-Growth Frontier

Umbilical cord blood held 45.25% of the stem cell banking market in 2025, driven by its established clinical use and trust in preservation practices. It remains central to family banking programs due to its association with childbirth, well-understood storage methods, and validated historical use. Cord tissue is increasingly paired with cord blood, enhancing source diversification without altering the collection window. Placental and dental stem cells are offered in select programs but remain supplementary rather than primary drivers.

Adipose tissue-derived stem cells, growing at a 17.20% CAGR through 2031, are gaining traction due to minimally invasive collection and higher mesenchymal cell yield. Developers prefer defined, traceable starting materials for therapeutic applications, making adipose banking relevant for industrial procurement. Standardized closed-system processing and GMP-ready workflows enhance consistency, supporting large-scale use in therapy and research. While cord blood anchors current volumes, adipose tissue drives forward momentum in the market.

By Service Type: Storage Leads Revenue, Processing Commands Strategic Priority

Storage services led the market with a 35.66% share in 2025, reflecting the value of long-term contracts. Every enrolled unit transitions into preservation, giving storage a significant installed base advantage. Families often prioritize storage when evaluating banking options, ensuring its commercial prominence despite evolving technical expectations. However, as the market matures, buyers increasingly focus on pre-storage processes rather than just preservation duration.

Processing, growing at a 16.95% CAGR through 2031, is becoming a key differentiator as pharmaceutical and research customers demand controlled workflows, viability testing, and standardized cell handling. Closed-system and GMP-compliant processing are central to meeting these needs, especially for therapy developers. Testing and analysis, including HLA typing and sample characterization, are also gaining importance, shifting service leadership from basic preservation to integrated workflows.

By Application: Personalized Banking Anchors Revenue, R&D Discovery Leads Growth

Personalized banking held a 45.30% share in 2025, serving as the largest application and revenue anchor for the stem cell banking market. Family-directed storage supports recurring fees, bundled perinatal services, and clear customer ownership from enrollment. Urban households increasingly view preserved biological material as a long-term medical asset, reinforcing personalized banking's centrality. It generates a broad subscription base and facilitates cross-selling across perinatal samples, ensuring stable revenue even as the market diversifies.

Research and drug discovery, growing at a 17.25% CAGR through 2031, reflects biopharma companies' preference for outsourcing cell therapy development. These companies value characterized cell starting materials from specialized repositories over building internal systems. Standardized input materials are critical as cell therapy programs scale, increasing the market size for research and drug discovery. Transplantation remains vital, with evidence supporting the role of unrelated cord blood in combination graft strategies.

By End User: Hospital Networks Set Baseline, Biotech Firms Drive Acceleration

Hospitals and clinics accounted for 41.95% of the stem cell banking market in 2025, reflecting their roles as collection points and clinical decision-makers. Positioned at the intersection of childbirth, transplant referrals, and physician counseling, hospitals influence demand and operational execution. They connect banking providers to transplant programs, quality expectations, and institutional purchasing relationships, solidifying their position as the largest end-user group despite expanding procurement patterns.

Biotechnology and pharmaceutical firms, growing at a 17.35% CAGR through 2031, are driving market acceleration by integrating stem cell banking with industrial therapy development. These firms demand lot consistency, characterization data, and GMP-grade handling, distinguishing their needs from hospitals or families. Research institutes and specialty laboratories are also shifting toward structured repository partnerships, elevating the value of accredited, high-capability operators in the market.

Geography Analysis

In 2025, North America led the stem cell banking market with a 40.60% share, driven by strong private banking penetration, established hospital networks, and a mature quality framework supporting clinical and family-directed storage. The U.S. remains the region's anchor due to advanced accreditation standards and institutional infrastructure. Regulatory clarity further enhances demand by standardizing collection, processing, and registration practices. North America's combination of scale, trust, and operational discipline continues to benefit established players.

Europe remains a key market, though consolidation is reshaping its structure. In May 2025, FamiCord AG acquired majority stakes in Czech and Slovak stem cell banks, along with patents for cell preservation processes tied to personalized health therapies. This reflects a shift toward fewer, well-capitalized operators with broader technical capabilities, moving away from a fragmented market of smaller local banks.

Asia-Pacific is the fastest-growing region, with a 16.67% CAGR projected through 2031, supported by large birth cohorts and rising adoption of private and hybrid models. China and India drive demand due to favorable demographics, urban income growth, and supportive biotech policies. The region is advancing as operators integrate preservation services with regenerative medicine programs and product development. Taiwan’s insurance-linked model from StemCyte exemplifies flexible enrollment structures expanding access while maintaining clinical pathways.

The Middle East, Africa, and South America currently hold smaller market shares but offer long-term growth potential. High birth rates and increasing middle-class healthcare spending create opportunities for expansion, provided affordability and awareness challenges are addressed.

Competitive Landscape

In the stem cell banking market, a limited number of dominant players hold significant influence across key regions. Prominent examples include Europe’s FamiCord AG, North America’s CooperSurgical and ViaCord, mainland China’s China Cord Blood Corporation, and Singapore’s Cordlife Group. These operators leverage extensive inventories, strong brand recognition, and advanced operating systems, creating substantial barriers for smaller entrants.

Strategic developments in the market highlight a shift toward capability-driven growth. FamiCord AG’s 2025 acquisitions in the Czech Republic and Slovakia extended beyond volume, incorporating patents for cell preservation methods tailored to personalized health applications. StemCyte’s November 2025 launch in Taiwan, linked to insurance, focused on innovative access design and hybrid enrollment rather than geographic expansion.

Opportunities in the market are concentrated in specific niches rather than broad expansion. Adipose-derived stem cell banking is gaining relevance due to regulatory advancements and closed-system processing, making it attractive for industrial users. Insurance-linked hybrid banking is another area of interest, particularly in Asian and emerging markets where affordability limits traditional private enrollment. Pharmaceutical-grade processing also presents growth potential, as therapy developers demand compliant, traceable materials, raising entry barriers for operators without advanced technical systems.

Stem Cell Banking Industry Leaders

CBR Systems, Inc.

Cordlife Group Limited

Cryo-Cell International, Inc.

LifeCell International Private Limited

ViaCord, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: FamiCord AG acquired majority stakes in Národní Centrum Pupečníkové Krve and Rodinná Banka Perinatálnych a Mezenchymálnych Buniek, strengthening its presence in Central Europe and obtaining patent rights related to cell preservation technologies.

- May 2026: AABB launched a new FDA eHCTERS toolkit to streamline establishment registration and enhance compliance for operators of human cells, tissues, and related products.

- February 2026: GwoXi Stem Cell submitted a Drug Master File to the FDA for its Adipose-Derived Mesenchymal Stem Cell Starting Material Bank, encompassing donor screening, GMP manufacturing, quality testing, and stability data.

- December 2025: The FDA approved omidubicel-onlv for severe aplastic anemia, expanding the clinical applications of cord blood-derived cell therapy and increasing manufacturing expectations across the industry.

- November 2025: StemCyte International introduced Taiwan's first insurance-linked public cord blood access service, utilizing a public inventory of over 36,000 units and establishing a hybrid access model for cell therapy protection.

Global Stem Cell Banking Market Report Scope

As per the scope of the report, stem cell banking is the process of collecting, processing, and cryopreserving potent stem cells (usually from a newborn's umbilical cord or adult tissues) so they remain viable for decades. These preserved cells can later be used in medical therapies and regenerative medicine to treat serious illnesses like blood disorders and certain cancers.

The stem cell banking market is segmented by bank type, stem cell source, service type, application, end-user, and geography. By bank type, the market includes public banking, private banking, and hybrid banking. By stem cell source, the market is segmented into umbilical cord blood, umbilical cord tissue, placental stem cells, dental stem cells, bone marrow-derived stem cells, adipose tissue-derived stem cells, and others. By service type, the market is categorized into collection and transportation, processing, testing and analysis, and storage. By application, the market is segmented into personalized banking, regenerative medicine, cell therapy, research and drug discovery, and transplantation. By end-user, the market includes hospitals and clinics, biotechnology and pharmaceutical companies, research institutes, and specialty laboratories. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Public Banking |

| Private Banking |

| Hybrid Banking |

| Umbilical Cord Blood |

| Umbilical Cord Tissue |

| Placental Stem Cells |

| Dental Stem Cells |

| Bone Marrow-Derived Stem Cells |

| Adipose Tissue-Derived Stem Cells |

| Others |

| Collection and Transportation |

| Processing |

| Testing and Analysis |

| Storage |

| Personalized Banking |

| Regenerative Medicine |

| Cell Therapy |

| Research and Drug Discovery |

| Transplantation |

| Hospitals and Clinics |

| Biotechnology and Pharmaceutical Companies |

| Research Institutes |

| Specialty Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Bank Type | Public Banking | |

| Private Banking | ||

| Hybrid Banking | ||

| By Stem Cell Source | Umbilical Cord Blood | |

| Umbilical Cord Tissue | ||

| Placental Stem Cells | ||

| Dental Stem Cells | ||

| Bone Marrow-Derived Stem Cells | ||

| Adipose Tissue-Derived Stem Cells | ||

| Others | ||

| By Service Type | Collection and Transportation | |

| Processing | ||

| Testing and Analysis | ||

| Storage | ||

| By Application | Personalized Banking | |

| Regenerative Medicine | ||

| Cell Therapy | ||

| Research and Drug Discovery | ||

| Transplantation | ||

| By End User | Hospitals and Clinics | |

| Biotechnology and Pharmaceutical Companies | ||

| Research Institutes | ||

| Specialty Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the stem cell banking market by 2031?

The stem cell banking market is projected to reach USD 23.51 billion by 2031, up from USD 11.37 billion in 2026, at a CAGR of 15.63%.

Which bank type leads revenue in stem cell banking?

Private banking led the bank-type segment with a 60.15% share in 2025, supported by recurring subscription revenue and family-directed storage demand.

Which stem cell source is growing the fastest through 2031?

Adipose tissue-derived stem cells are the fastest-growing source segment, with a 17.20% CAGR through 2031, supported by higher mesenchymal cell yield and improving GMP workflows.

Why is processing becoming more important than storage alone?

Processing is rising in importance because therapy developers need controlled, traceable, and GMP-compliant starting material, which makes quality preparation more valuable than freezer capacity alone.

Which region leads current revenue and which region is growing fastest?

North America held the largest regional share at 40.60% in 2025, while Asia-Pacific is forecast to grow the fastest at a 16.67% CAGR through 2031.

What is driving demand from biotechnology and pharmaceutical companies?

These companies are increasingly sourcing characterized and compliant stem cell material from specialized repositories instead of maintaining internal banks, which is why the end-user segment is projected to grow at 17.35% through 2031.

Page last updated on: