Immortalized Cell Line Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.52 Billion |

| Market Size (2031) | USD 8.04 Billion |

| Growth Rate (2026 - 2031) | 7.82% CAGR |

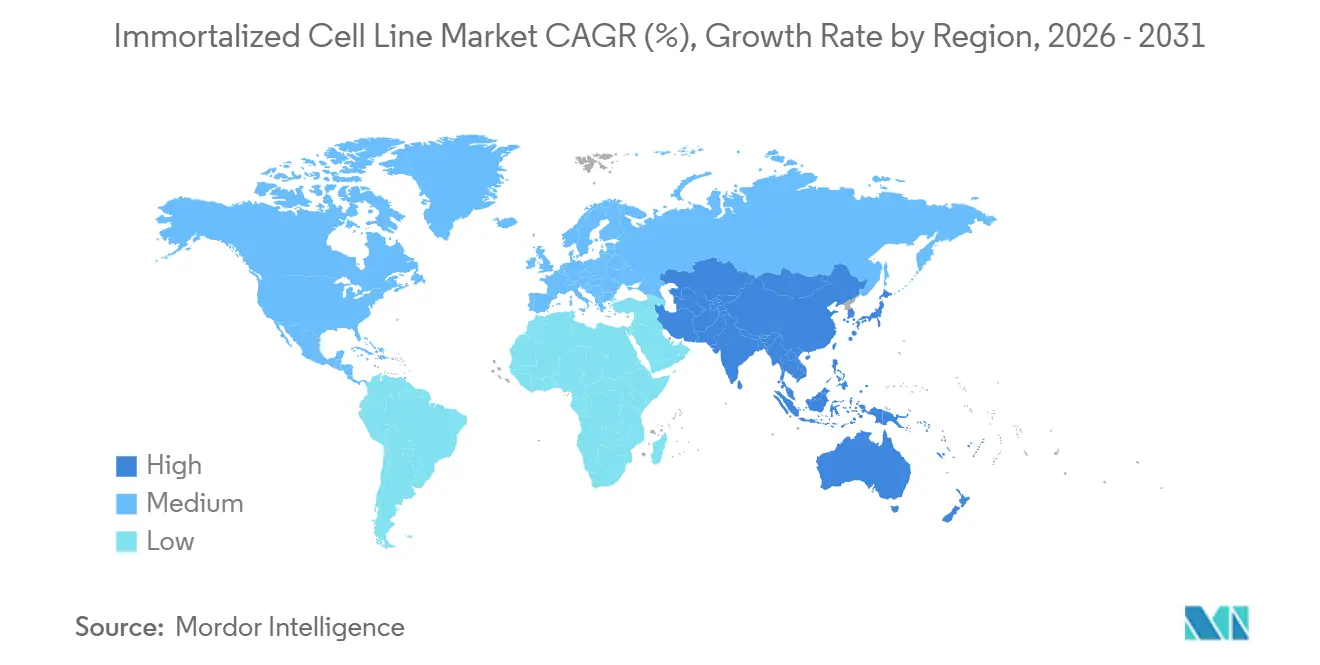

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Immortalized Cell Line Market Analysis by Mordor Intelligence

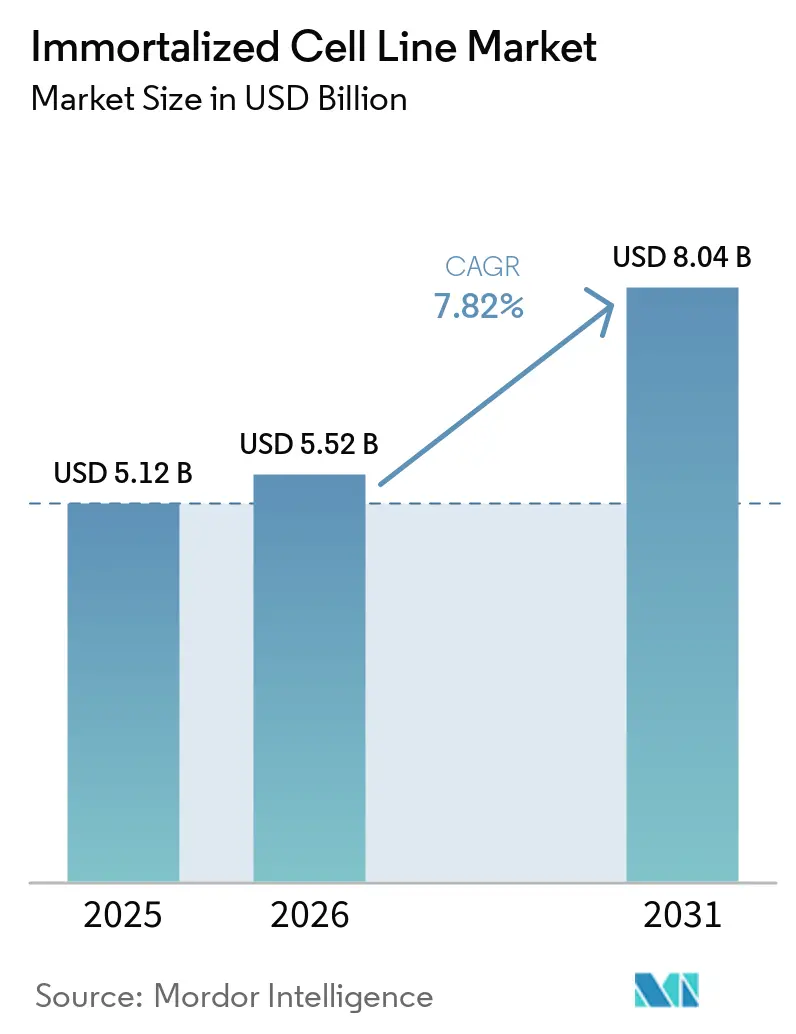

The Immortalized Cell Line Market size is projected to expand from USD 5.12 billion in 2025 and USD 5.52 billion in 2026 to USD 8.04 billion by 2031, registering a CAGR of 7.82% between 2026 to 2031.

The market remains tied to biologics manufacturing and drug discovery programs because continuous cell lines deliver the reproducibility and scale that primary cells cannot maintain across extended passages. Demand is also being lifted by the larger pipeline of monoclonal antibodies and viral vectors, wider use of CRISPR-based disease models, and tighter expectations around cell line authentication from regulators such as the FDA, EMA, and ICH. These shifts are moving the immortalized cell line market away from a simple reagent model and toward a higher-value platform model where documentation, characterization, and validation matter as much as biological performance. The same cell lines now serve several application layers at once, which strengthens demand for suppliers that can support both research use and production use. As a result, competition in the immortalized cell line market is increasingly centered on regulatory readiness, quality systems, and portfolio breadth rather than on vial pricing alone.

Key Report Takeaways

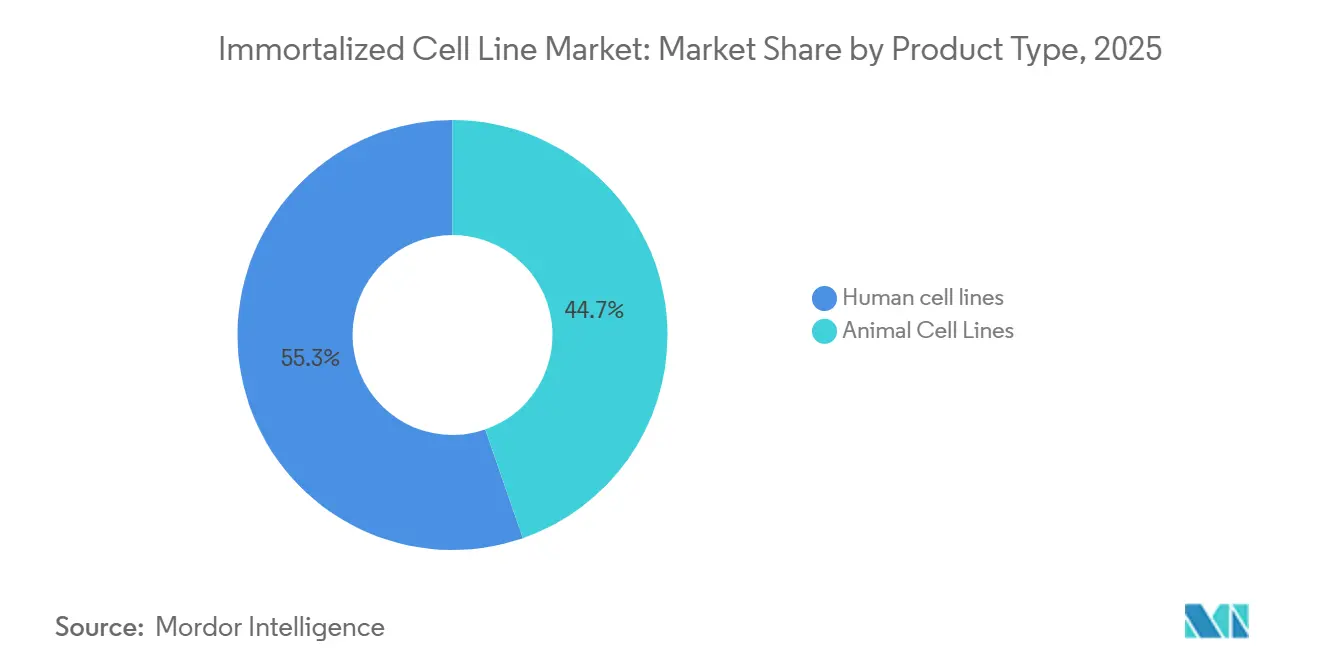

- By product type, human cell lines held 55.3% of the immortalized cell line market share in 2025 and are also the fastest-growing category at an 8.4% CAGR through 2031.

- By immortalization method, viral-mediated approaches accounted for 40.2% of revenue in 2025, while hTERT-mediated immortalization is forecast to grow fastest at an 8.5% CAGR through 2031.

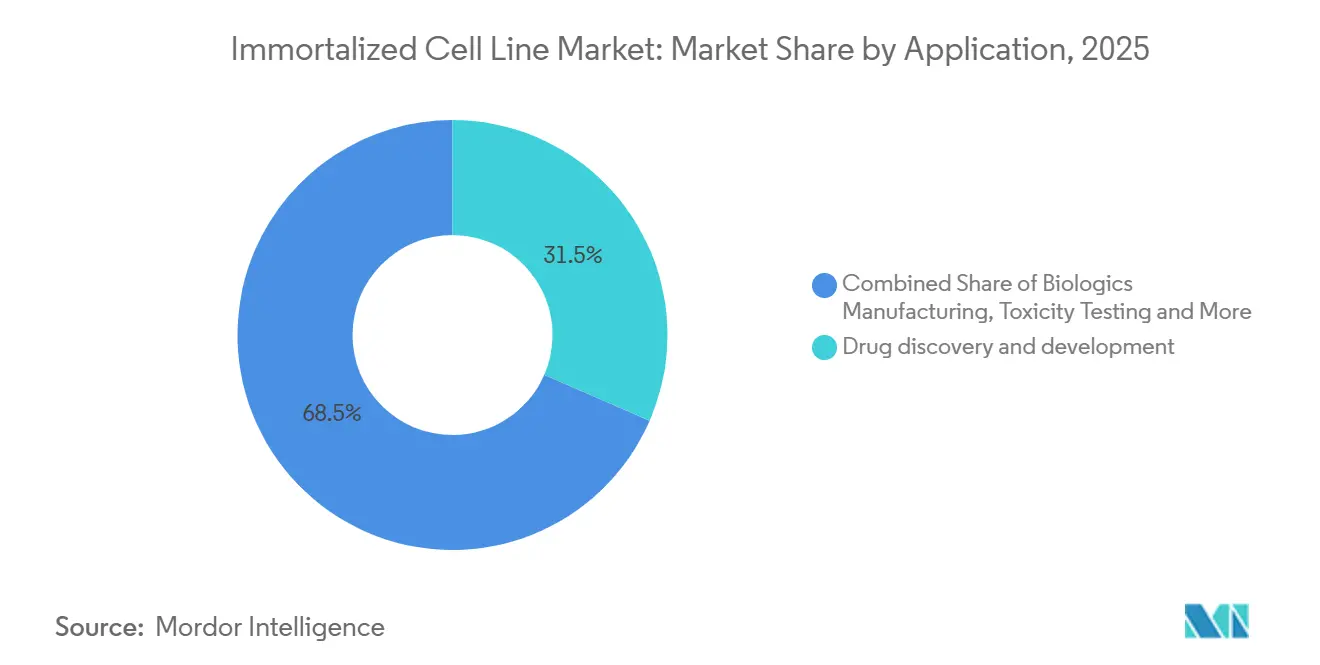

- By application, drug discovery and development represented 31.5% of revenue in 2025, while biologics manufacturing is projected to expand fastest at an 8.3% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 42.5% of revenue in 2025, while CROs and CDMOs are expected to grow fastest at an 8.8% CAGR through 2031.

- By geography, North America held 38.2% of revenue in 2025, while Asia-Pacific is projected to record the fastest growth at an 8.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Immortalized Cell Line Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologics And Viral Vector Pipeline Expansion | +2.8% | Global, concentrated in North America, Europe, and China | Medium term (2-4 years) |

| Drug Discovery And Toxicity-Screening Intensity | +1.9% | Global, especially North America, Europe, and India | Short term (≤ 2 years) |

| CRISPR-Engineered Disease Models | +1.4% | North America and Europe core, with spillover to South Korea and Japan | Medium term (2-4 years) |

| Authentication And Traceability Mandates | +0.8% | Global, with strongest regulatory effect in North America and Europe | Medium term (2-4 years) |

| Cultivated Meat And Non-Therapeutic Cell Demand | +0.5% | North America, the Netherlands, Singapore, and early gains in Israel | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Biologics and Viral Vector Pipeline Expansion

The immortalized cell line market is benefiting from the widening need for continuously passaging GMP-qualified substrates across biologics and gene therapy production programs. Mammalian continuous cell lines, especially CHO and HEK293 derivatives, remain central to approved recombinant protein production, while HEK293-derived systems are also critical for AAV and lentiviral vector manufacturing. Lonza’s May 2026 launch of the Xcite AAV stable producer cell line platform showed a 10-fold to 15-fold increase in AAV titer versus transient transfection and pointed to a cost-of-goods reduction of 80% or more, which shows how quickly stable producer formats are moving into commercial use[1]Lonza, “Lonza Expands AAV Offering With Xcite AAV Stable Producer Cell Line Platform to Industrialize Viral Vector Manufacturing,” Lonza Media Advisory. That performance matters because high-dose neurological programs have often pushed transient systems beyond workable cost limits. As stable-cell-line AAV production becomes more practical, the immortalized cell line market is seeing stronger demand for qualified producer lines, cell banking, and analytical support. This shift also favors suppliers that can connect upstream cell line design with downstream manufacturing documentation in one platform.

Drug Discovery and Toxicity-Screening Intensity

The immortalized cell line market continues to draw support from high-throughput screening, where continuous lines remain the standard base for repeatable assay performance. More complex assay formats such as 3D spheroids, organoid co-cultures, and organ-on-a-chip systems still depend on cell lines that can hold stable behavior over longer experimental windows. Merck KGaA’s October 2025 partnership with Promega, built on the company’s earlier acquisition of HUB Organoids, shows that suppliers are investing in assay systems that place immortalized lines inside more advanced screening environments rather than replacing them. The FDA’s April 2026 draft guidance on safety assessment for genome editing in human gene therapy products also increases the need for validated cell-based potency and functional assays across development programs. That requirement expands the number of authenticated human cell models needed per program. The immortalized cell line market therefore gains not only from higher research volume, but also from stricter validation expectations built into modern drug development pathways.

CRISPR-Engineered Disease Models

The immortalized cell line market is also being reshaped by CRISPR, which is turning standard cell lines into programmable disease models with higher research value. NIST reported in April 2025 that CRISPR/Cas9-mediated insertion of a single-copy hTERT construct into human primary CD8+ T cells produced a line that expanded more than 26 million times while maintaining normal karyotype and surface marker profiles. A 2026 PLOS One study showed that combining PCNA overexpression with HDR pathway modulation improved precise knock-in efficiency in difficult immortalized models such as HepG2 and MCF7 by up to 38.7%. These findings reduce the technical barrier for generating isogenic cell line pairs, which are widely valued for phenotypic target validation. As these workflows become easier to standardize, the immortalized cell line market is likely to see broader demand for off-the-shelf edited panels rather than purely bespoke engineering services. That change could shift value toward suppliers that can industrialize CRISPR-edited catalog products with strong documentation.

Authentication and Traceability Mandates

The immortalized cell line market is gaining support from stricter authentication and traceability requirements across research and regulated use settings. The ANSI/ATCC ASN-0002-2022 standard requires at least 13 STR loci for human cell line authentication, and associated cGMP testing services emphasize retention of raw electropherogram records for 5 years. The International Cell Line Authentication Committee registry, as discussed in a 2025 peer review study, listed 593 misidentified or cross-contaminated lines in its version 13 update. A 2026 review estimated that irreproducible preclinical research, with cell line misidentification as a major contributor, costs USD 28 billion annually in the United States alone. Those conditions raise spending on STR profiling, LIMS integration, and compliant banking services. The immortalized cell line market is therefore adding a quality-control revenue layer around the core cell catalogue business, and integrated suppliers are capturing more of that spend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Development, Validation, And QC Costs | -1.8% | Global, most acute for mid-size biotechs in North America and Europe | Medium term (2-4 years) |

| Biosafety And Donor-Traceability Scrutiny | -1.2% | Global, with strongest regulatory influence in North America, Europe, and Japan | Long term (≥ 4 years) |

| Misidentification, Contamination, And Genetic Drift | -0.9% | Global, with disproportionate impact in academic and emerging-market settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Development, Validation, and QC Costs

The immortalized cell line market still faces a clear restraint in the cost of moving a line from research use into GMP-qualified production use. That process requires STR profiling, mycoplasma testing, adventitious agent screening, viral safety evaluation, karyotyping, and stability assessment, which extends both timelines and budgets for each program[2]U.S. Food and Drug Administration, “Q5A(R2) Viral Safety Evaluation of Biotechnology Products Derived From Cell Lines of Human or Animal Origin, Guidance for Industry, Availability,” Federal Register. The need to show genetic stability from the master cell bank through the end-of-production cell window raises the burden further for developers with several early-stage assets. Smaller biotechs often respond by delaying full characterization or by relying on CDMOs that already hold validated parental lines. That dependence shifts pricing power toward integrated service providers and reduces flexibility for firms that want to own their full cell line development path. It also limits the pace at which new entrants can scale in the immortalized cell line market.

Biosafety and Donor-Traceability Scrutiny

The immortalized cell line market also faces friction from rising scrutiny around biosafety and donor traceability. Regulators increasingly expect clear origin records, robust testing, and well-controlled documentation for human and animal derived cell substrates used in development or manufacturing. The January 2024 finalization of ICH Q5A(R2) through the FDA increased the analytical burden tied to viral safety evaluation for products derived from continuous human or animal cell lines. Those expectations can be managed by large established suppliers, but they are harder for smaller entrants that do not already have viral clearance and traceability systems in place. The result is slower onboarding of new lines into regulated use and a higher preference for suppliers with established compliance records. This keeps barriers to entry elevated across the immortalized cell line market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Human Lines Anchor Both Volume and Value

Human cell lines held 55.3% of revenue in 2025, and that made them the largest product category in the immortalized cell line market. The same segment is also projected to expand at an 8.4% CAGR through 2031, which means its growth is being driven by structural demand rather than by a short-term mix shift from animal lines. Human lines stay central because they model human disease biology more directly, support human-relevant antibody work, and serve as viral vector substrates in gene therapy programs. HEK293, HeLa, and Jurkat lines remain widely used across oncology, toxicology, and vector production workflows. This breadth keeps the human line segment at the center of procurement decisions across the immortalized cell line industry.

Engineered derivatives are gaining more commercial weight within this segment because they support tighter batch consistency and more application-specific use cases. A 2025 study in Stem Cell Research & Therapy reported consistent batch-to-batch extracellular vesicle profiles from hTERT-immortalized MSC lines, which supports their use in therapeutic EV platforms. Animal cell lines still retain an essential role, especially CHO for recombinant protein production and Vero or BHK-21 for established vaccine and research workflows. At the same time, the spread of bovine, equine, and other species-specific lines into cultivated meat and veterinary applications is expanding the reachable demand pool for the immortalized cell line market. Regulatory testing demands for animal-derived lines also favor suppliers that already operate established biosafety and characterization laboratories.

By Immortalization Method: Viral Dominance Contested by hTERT’s Safety Profile

Viral-mediated immortalization accounted for 40.2% of revenue in 2025, which kept it as the largest method segment in the immortalized cell line market. Its large installed base reflects decades of use with SV40, HPV E6/E7, and adenoviral tools for generating highly proliferative research lines. The method also holds a stable demand floor because vaccine production substrates such as Vero and MDCK remain tied to long-established processes. Even so, hTERT-mediated immortalization is projected to grow at an 8.5% CAGR through 2031, making it the fastest-growing method segment. That faster growth reflects a stronger safety profile because hTERT extends replicative lifespan without the same disruption of p53 or pRB pathways associated with viral oncoproteins.

The NIST study published in 2025 strengthened this direction by showing that precision hTERT knock-in can produce immortalized primary human CD8+ T cells with stable karyotype and preserved immunologic features. Hybridoma fusion remains relevant in legacy monoclonal antibody workflows and in polyclonal antibody generation, even though recombinant platforms continue to take share. Spontaneous and chemical immortalization methods stay niche, but they are drawing attention in food biotechnology where non-GMO positioning carries regulatory weight in some jurisdictions. For buyers across the immortalized cell line industry, the choice of method now reflects a clearer tradeoff between historical robustness, safety profile, and downstream regulatory burden.

By Application: Drug Discovery Holds the Core, Biologics Manufacturing Accelerates

Drug discovery and development represented 31.5% of revenue in 2025, which gave it the largest application share in the immortalized cell line market size. This segment remains anchored in target identification, hit-to-lead work, and ADME or toxicology screening, where repeatable cellular models are essential. Biologics manufacturing is the fastest-growing application and is projected to expand at an 8.3% CAGR through 2031 as monoclonal antibodies, bispecifics, antibody-drug conjugates, and viral vectors move through development and commercial scaling. WuXi Biologics introduced the WuXia293Stable platform in 2025, and the company stated that the HEK293-based stable system reached up to 5.0 g/L monoclonal antibody titers at 2,000 L fed-batch scale[3]WuXi Biologics, “WuXi Biologics Launches HEK293 Stable Cell Line Platform WuXia293Stable for Development and Manufacturing of Difficult-to-Express Molecules,” WuXi Biologics. That kind of production performance shows why manufacturing-grade continuous lines are becoming more valuable across the immortalized cell line market.

Cancer research also benefits from the release of rarer disease models, including the first publicly accessible immortalized cell line for desmoid tumors in March 2024, which improved in vitro options for a previously underrepresented area. Vaccine development remains strategically important because continuous substrate lines are part of preparedness planning and established manufacturing pathways. The 2024 ICH Q5A(R2) revision explicitly addressed the use of next-generation sequencing as a replacement for conventional virus detection methods in relevant applications. Gene and cell therapy research adds another fast-moving layer of demand, with separate needs for viral producer cell lines and immune cell models used in therapeutic development.

By End User: Pharma Leadership Intact, CRO and CDMO Procurement Keeps Rising

Pharmaceutical and biotechnology companies accounted for 42.5% of revenue in 2025, which kept them as the largest end-user group in the immortalized cell line market. These companies buy catalogued lines for internal R&D and also sponsor bespoke line development for proprietary biologic and cell therapy programs. CROs and CDMOs are the fastest-growing end-user group and are forecast to grow at an 8.8% CAGR through 2031 as outsourcing of cell line development and banking continues to deepen. Charles River Laboratories’ February 2025 agreement with Singapore General Hospital showed this shift clearly because it covered cGMP cell banking and NGS-based characterization services for allogeneic CAR-T Phase I trials. This pattern shows how service providers are moving beyond research banking and into clinical-grade support within the immortalized cell line market.

Academic and research institutes still make up a large installed base, but their buying behavior is different because they place more emphasis on catalogue breadth, authentication records, and material transfer flexibility than on GMP compliance. Diagnostic laboratories remain the smallest defined end-user segment, although their use of reference standards and quality control cell lines is increasing steadily. The larger procurement shift is toward integrated platform agreements that cover development, characterization, and long-term supply rather than single-vial purchases. That change is concentrating more spend with suppliers that can support the full life cycle from discovery through commercial banking.

Geography Analysis

North America accounted for 38.2% of global revenue in 2025, which gave the region the largest share of the immortalized cell line market size. The region holds this lead because it combines dense biopharmaceutical R&D activity with a mature network of GMP-grade cell banking facilities and a regulatory system that expects detailed cell substrate characterization. The FDA’s April 2026 draft guidance on genome editing safety assessment adds to that demand because it places greater weight on authenticated and characterized cell-based assays during development. GI Partners’ formation of Rose BioSolutions in May 2026 from Charles River’s divested CDMO and Cell Solutions businesses also showed that capital continues to flow into North American cell solutions infrastructure. South America remains much smaller, and activity there is tied mainly to Brazil’s biosimilar ambitions and Argentina’s growing CRO base, while limited GMP-grade banking infrastructure keeps most demand closer to research-grade use.

Europe provides steady demand for the immortalized cell line market because it has a mature pharmaceutical and biotechnology base and a consistent regulatory framework. Servier inaugurated its Bio-S bioproduction unit in France in November 2024 with an investment of EUR 86 million, which supported clinical biologics production using mammalian continuous cell lines. The region is also facing tighter process expectations through proposed revisions to GMP guidance for advanced therapy medicinal products, which would raise compliance standards for manufacturers using immortalized substrates. The Middle East and Africa is still at an early stage, but healthcare modernization in the GCC and WuXi Biologics’ 2025 memorandum with Qatar Free Zones Authority indicate an early buildout of regional manufacturing interest.

Asia-Pacific is the fastest-growing regional block in the immortalized cell line market and is projected to expand at an 8.9% CAGR through 2031. China is the largest force inside that growth story because public R&D spending, repository building, and CDMO expansion are all moving at the same time. The National Stem Cell Resource Center was actively building shared repositories of immortalized human cell lines in 2025, which supports both academic use and long-term ecosystem depth. WuXi Biologics also reported 16.7% year-on-year revenue growth in 2025 and added a record 209 new integrated projects, which shows the scale of manufacturing momentum in the region. PackGene Biotech’s October 2025 filing of FDA Drug Master Files for 2 proprietary HEK293 cell banks is also important because it places Chinese cell line assets more directly within the U.S. gene therapy regulatory path. India is also building downstream demand for the immortalized cell line market through growth in biotech activity and outsourcing demand, even though upstream production infrastructure remains earlier in its development curve.

Competitive Landscape

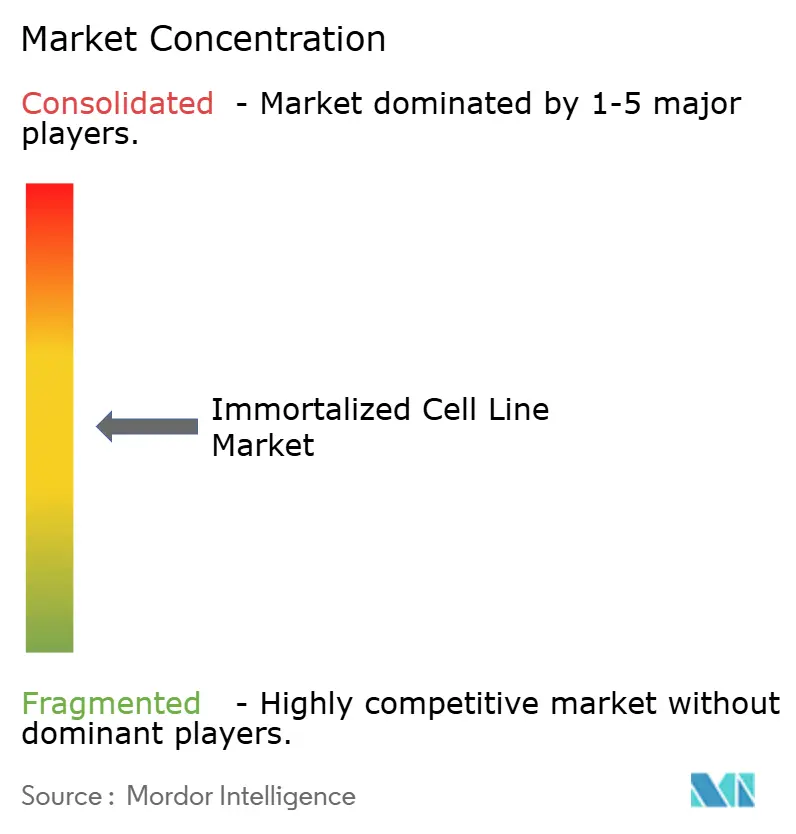

The immortalized cell line market is moderately concentrated around a small upper tier that includes Thermo Fisher Scientific, Lonza Group, Merck KGaA, Sartorius AG, and WuXi AppTec, along with specialized repositories such as ATCC and DSMZ. These larger companies compete across cell line development, GMP banking, characterization, and bioprocess support rather than through standalone catalog sales. That operating model gives them a structural advantage because proprietary CHO and HEK293 parental lines are bundled with process knowledge, documentation, and regulatory history that are difficult for customers to move elsewhere without major comparability work. Thermo Fisher Scientific’s April 2026 launch of the Gibco CHOvantage GS Cell Line Development Kit was aimed directly at this need, with reported titers of at least 7 g/L, stable pools in 4 weeks, and clone selection within 14 weeks under a royalty-free clinical-stage licensing model. Sartorius also expanded its position in 2026 through a new genetically engineered CHO host cell line paired with its CellCelector automation platform, which strengthens customer retention by combining cell assets with equipment workflow.

The specialist tier competes on different terms inside the immortalized cell line market. Repositories such as ATCC, DSMZ, and the Coriell Institute focus more on catalogue depth, provenance, and transfer flexibility than on large-scale GMP manufacturing. Specialist firms such as InSCREENeX and KBI Biopharma through Selexis also hold defensible positions in tissue-specific continuous lines and CHO expression platforms. AGC Biologics’ December 2025 partnership with ATUM to integrate the Leap-In Transposase platform shows how mid-tier CDMOs are using external technology to reduce development time and narrow the speed gap with larger integrated players.

Another defining feature of the immortalized cell line market is that a single line can support several demand layers at once. HEK293-derived lines, for example, can support toxicology research, viral vector production, and broader assay development, which means suppliers with broad platform reach can serve multiple customer groups from one biological foundation. Pricing also varies sharply between research-grade vials and fully documented GMP master cell banks, which pushes competition toward quality systems and regulatory capability rather than simple unit pricing. The market is also seeing IP spillover into non-therapeutic uses, including engineered bovine lines designed for cultivated meat bioreactor applications, which shows how proprietary cell line value is moving beyond pharmaceutical settings. As compliance expectations rise, pure catalogue vendors face more pressure, while integrated service providers gain from long-term supply relationships, technical lock-in, and broader platform relevance across the immortalized cell line market.

Immortalized Cell Line Industry Leaders

Lonza Group

Thermo Fisher Scientific

WuXi AppTec

Merck KGaA

Sartorius AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Lonza launched the Xcite AAV stable producer cell line platform, delivering a 10-fold to 15-fold titer improvement over transient transfection and a potential cost-of-goods reduction of 80% or more. The platform makes stable-cell-line AAV manufacturing commercially viable for high-dose neurological gene therapy indications.

- May 2026: GI Partners completed the acquisition of Charles River Laboratories' CDMO and Cell Solutions businesses, forming independent entity Rose BioSolutions with end-to-end capabilities across plasmid DNA, viral vectors, and cellular materials. The divestiture restructures competitive dynamics in the North American cell banking sector.

- April 2026: Thermo Fisher Scientific launched the Gibco CHOvantage GS Cell Line Development Kit, an integrated CHO platform achieving at least 7 g/L titers in fed-batch, stable pools in 4 weeks, and clone selection within 14 weeks under a royalty-free clinical-stage licensing model.

Global Immortalized Cell Line Market Report Scope

As per the scope of the report, an immortalized cell line is a population of cells that has been modified or has naturally acquired the ability to divide indefinitely in culture. Unlike normal cells, which have a limited lifespan due to senescence, immortalized cells can proliferate endlessly under proper conditions, making them valuable for research, medical, and biotechnological applications.

The segmentation of the immortalized cell line market is categorized by product type, immortalization method, application, end user, and geography. By product type, the market is divided into human cell lines and animal cell lines. By immortalization method, it includes viral-mediated immortalization, hTERT-mediated immortalization, hybridoma fusion, and spontaneous and chemical immortalization. By application, the market covers drug discovery and development, toxicity testing, cancer research, biologics manufacturing, vaccine development, and gene and cell therapy research. By end user, the segmentation includes pharmaceutical and biotechnology companies, academic and research institutes, CROs and CDMOs, and diagnostic laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Human Cell Lines |

| Animal Cell Lines |

| Viral-mediated Immortalization |

| hTERT-mediated Immortalization |

| Hybridoma Fusion |

| Spontaneous and Chemical Immortalization |

| Drug Discovery and Development |

| Toxicity Testing |

| Cancer Research |

| Biologics Manufacturing |

| Vaccine Development |

| Gene and Cell Therapy Research |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| CROs and CDMOs |

| Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Human Cell Lines | |

| Animal Cell Lines | ||

| By Immortalization Method | Viral-mediated Immortalization | |

| hTERT-mediated Immortalization | ||

| Hybridoma Fusion | ||

| Spontaneous and Chemical Immortalization | ||

| By Application | Drug Discovery and Development | |

| Toxicity Testing | ||

| Cancer Research | ||

| Biologics Manufacturing | ||

| Vaccine Development | ||

| Gene and Cell Therapy Research | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Academic and Research Institutes | ||

| CROs and CDMOs | ||

| Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the immortalized cell line space by 2031?

It is projected to reach USD 8.04 billion by 2031, rising from USD 5.52 billion in 2026 at a 7.82% CAGR.

Which product category leads revenue and growth?

Human cell lines lead both measures, with 55.3% revenue share in 2025 and an 8.4% CAGR through 2031.

Why are human cell lines seeing such strong demand?

They are closely tied to human disease modeling, antibody research, and viral vector production, which makes them useful across both discovery and manufacturing settings.

Which region is growing fastest through 2031?

Asia-Pacific is the fastest-growing region with an 8.9% CAGR through 2031, supported by biopharma investment, repository expansion, and CDMO growth in China, India, and Japan.

Why are CROs and CDMOs gaining share in procurement?

Biopharma companies are outsourcing more cell line development and banking work to providers that can deliver GMP-compliant banks and analytical support on tighter timelines.

What are the main risks affecting adoption and profitability?

The largest constraints are high validation and QC costs, tighter biosafety and traceability requirements, and persistent risks around misidentification, contamination, and genetic drift.

Page last updated on: