Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

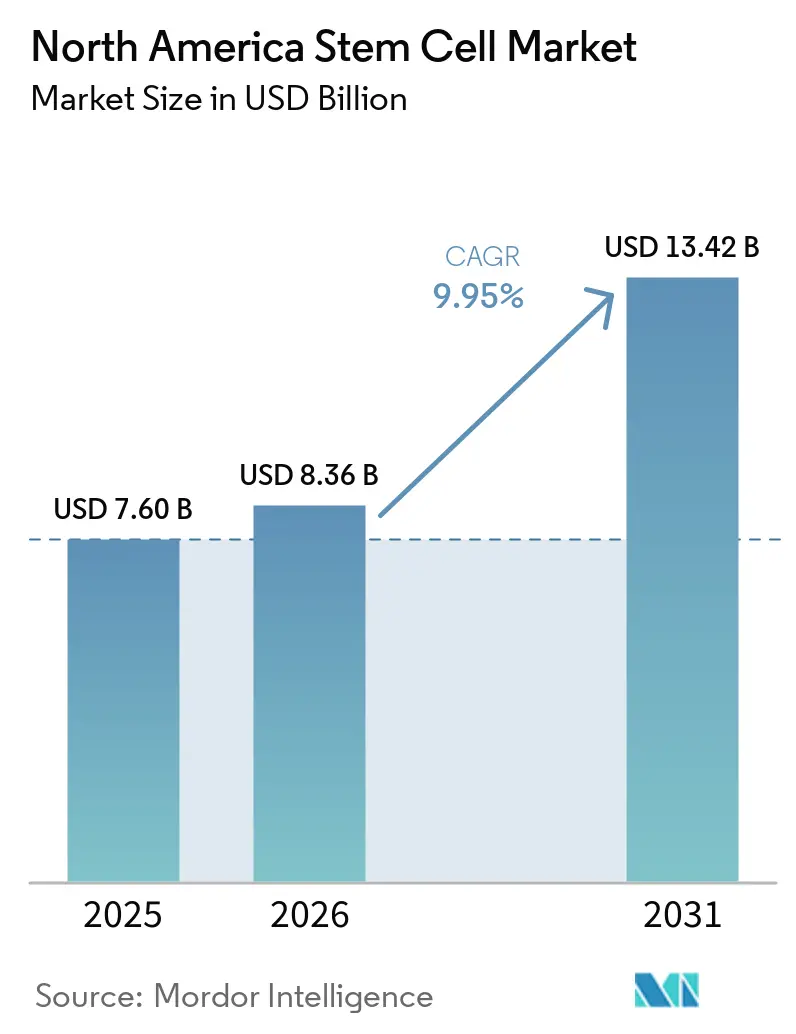

| Base Year Market Size (2025) | USD 7.60 Billion |

| Market Size (2026) | USD 8.36 Billion |

| Market Size (2031) | USD 13.42 Billion |

| Growth Rate (2026 - 2031) | 9.95% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Stem Cell Market Analysis by Mordor Intelligence

The North America Stem Cell Market size is expected to grow from USD 7.60 billion in 2025 to USD 8.36 billion in 2026 and is forecast to reach USD 13.42 billion by 2031 at 9.95% CAGR over 2026-2031. A decisive mix of accelerated FDA pathways, deep private-equity liquidity and hospital-based manufacturing hubs is propelling the North America stem cell market toward sustained double-digit expansion. Fast-track and Regenerative Medicine Advanced Therapy (RMAT) designations are shrinking development timelines, while Pentagon and Veterans Affairs grants are moving battlefield innovations into civilian care settings, further enlarging the addressable patient pool. In parallel, corporate decarbonization targets are steering capital toward “green bioprocessing,” giving early movers a cost and branding edge. Collectively, these demand-side and supply-side forces reinforce the region’s standing as the global test bed for next-generation regenerative therapies.

Key Report Takeaways

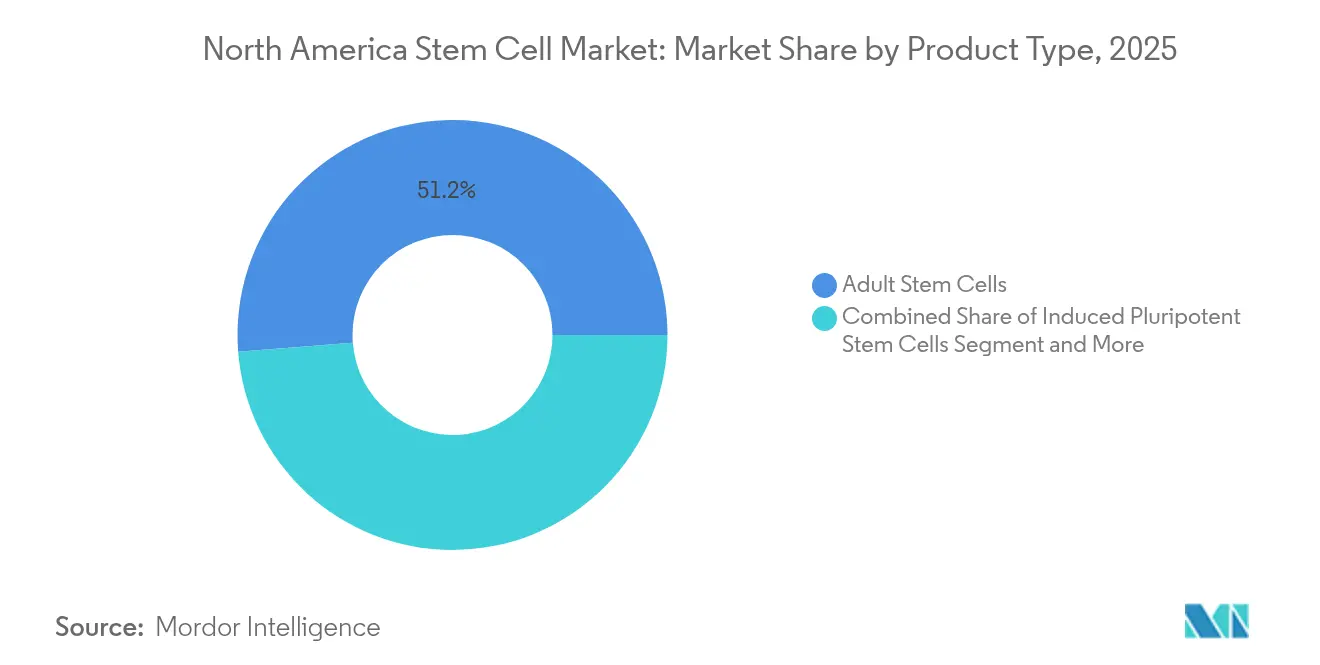

- By product type, adult stem cells held 51.25% of North America stem cell market share in 2025; induced pluripotent stem cells (iPSCs) are projected to expand at a 9.71% CAGR through 2031.

- By application, orthopedic treatments captured 24.75% revenue share in 2025, whereas neurological disorders are forecast to accelerate at an 11.21% CAGR to 2031.

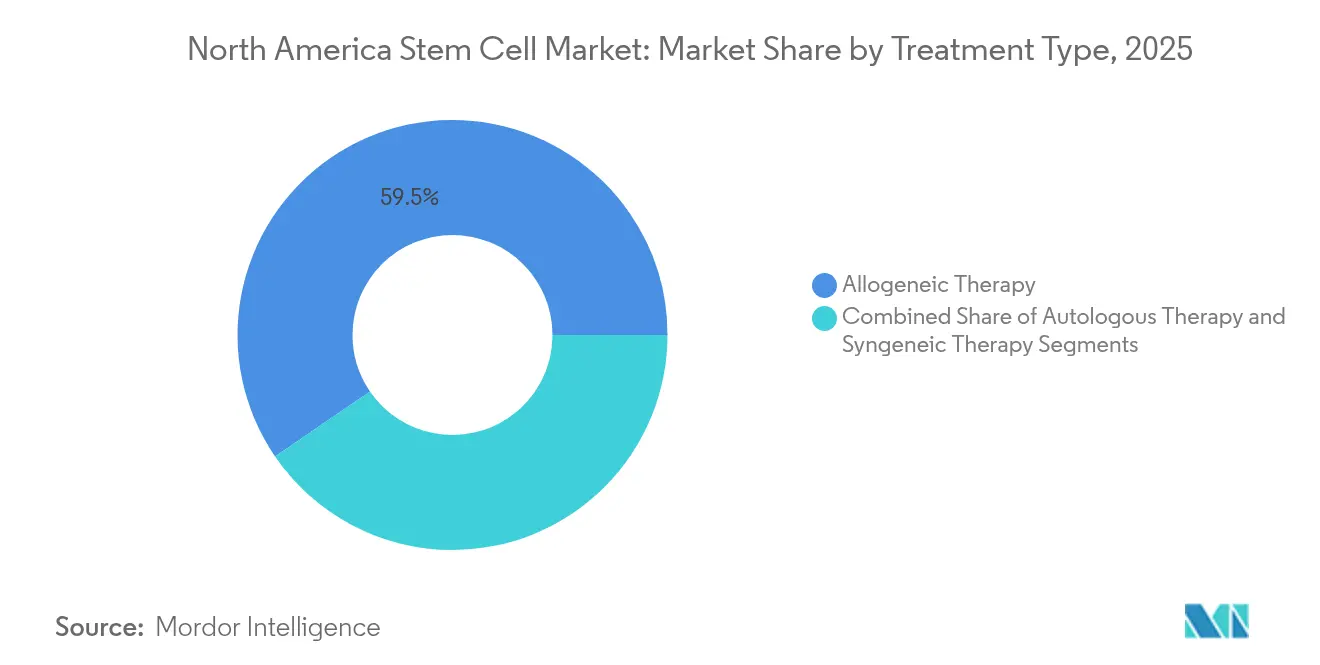

- By treatment type, allogeneic therapy commanded 59.55% share of the North America stem cell market size in 2025; autologous therapy is advancing at an 11.45% CAGR over 2026-2031.

- By end user, academic and research institutes accounted for 35.90% share in 2025, while biopharma and biotech firms are set to grow at a 11.78% CAGR through 2031.

- By geography, the United States led with 87.75% revenue share in 2025; Canada is forecast to post the fastest 11.62% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Stem Cell Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated FDA Fast-Track and RMAT Designations | +1.8% | United States, with spillover to Canada | Short term (≤ 2 years) |

| Surge in Private Equity Funding for off-the-shelf MSC Platforms | +1.5% | North America, concentrated in biotech hubs | Medium term (2-4 years) |

| Expansion of Hospital-Affiliated Stem-Cell Centers across the U.S. | +1.2% | United States, regional hospital networks | Medium term (2-4 years) |

| Integration of CRISPR with iPSC Pipelines | +1.4% | North America, with R&D concentration in major cities | Long term (≥ 4 years) |

| Pentagon & VA Grants for War-Injury Regenerative Programs | +0.9% | United States, military medical centers | Short term (≤ 2 years) |

| Corporate Decarbonization Policies Boosting "Green Bioprocessing" Demand | +0.7% | North America, manufacturing-intensive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated FDA Fast-Track and RMAT Designations

A broader RMAT mandate has re-charted the North America stem cell market by halving historical development timelines. Approval of remestemcel-L for pediatric graft-versus-host disease validated mesenchymal stem-cell efficacy and emboldened sponsors to file similar applications in neurology and cardiology.[1]Source: American Association of Blood Banks, “FDA Approves First Cell Therapy for Rare Eye Disease,” aabb.org Encelto, the first encapsulated allogeneic gene therapy for rare eye disease, further shows regulators’ tolerance for innovative delivery platforms. As potency assays gain consensus, industry analysts expect RMAT approvals to cover at least 25 distinct indications by 2028, cementing the North America stem cell market as the world’s regulatory bellwether.

Surge in Private Equity Funding for Off-the-Shelf MSC Platforms

Series A and Series B rounds topping USD 20 million now routinely target automated allogeneic manufacturing lines. Kincell Bio’s USD 22 million raise earmarked solely for scaling multipurpose mesenchymal stromal cell (MSC) production underscores investors’ tilt toward platforms with economy-of-scale upside. With per-dose costs projected to drop from USD 500,000 to USD 50,000 once automation matures, the North America stem cell market is witnessing a venture-capital-driven race to build the region’s first vertically integrated “cell-factories.”

Expansion of Hospital-Affiliated Stem-Cell Centers Across the U.S.

Not-for-profit hospital systems are internalizing regenerative workflows. Cryo-Cell International’s Durham facility typifies the trend—combining patient intake, cell processing and clinical trials under one roof. Each satellite lowers referral leakage and shortens vein-to-vein times, giving hospitals cost containment benefits while widening access to community-based populations. Graduate medical institutions are adopting similar hubs, embedding translational research directly into patient pathways.

Integration of CRISPR With iPSC Pipelines

Century Therapeutics’ CRISPR-edited iPSC line, designed to evade host immune surveillance, moved into Phase I trials after demonstrating consistent knock-in efficiencies above 80%. Parallel efforts at Northeastern University apply machine-learning algorithms to predict editing success and culture-media adjustments, cutting batch-failure rates by an estimated 35%. These advances shift the North America stem cell market from manual protocols toward digitally-controlled production, aligning precision engineering with regulatory reproducibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High COGS of GMP-Scale Allogeneic Manufacturing | -2.1% | North America, manufacturing-intensive regions | Medium term (2-4 years) |

| Patchwork State-Level Reimbursement Rules | -1.6% | United States, state-by-state variation | Short term (≤ 2 years) |

| Donor-Shortage Risk in Autologous Supply Chains | -1.3% | North America, donor registry dependent regions | Long term (≥ 4 years) |

| Tumorigenicity Concerns Slowing Pluripotent Approvals | -1.8% | North America, regulatory oversight regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High COGS of GMP-Scale Allogeneic Manufacturing

GMP-grade allogeneic therapies still cost 3-4 times more than traditional biologics because of intensive quality controls and skilled-labor demands.[2]Source: BioProcess International Staff, “Automation of Cell Therapy Biomanufacturing,” bioprocessintl.com Automation platforms from Ori Biotech promise 70% labor savings, yet capital outlays remain prohibitive for emerging firms. Contract development and manufacturing organizations (CDMOs) are experiencing overcapacity in some segments while facing shortages in specialized capabilities, creating pricing volatility that impacts overall market economics.

Patchwork State-Level Reimbursement Rules

Florida’s 2025 statute permitting physician-supervised, non-FDA-approved treatments exemplifies the fragmented reimbursement environment. Divergent payor criteria across Anthem, Cigna and Medicare complicate coding and claims, forcing providers to maintain multilayer billing protocols. Uneven coverage prolongs time-to-revenue and clouds market-size visibility, particularly for small clinics that anchor rural demand. The lack of standardized reimbursement criteria also limits the ability of healthcare systems to develop consistent treatment protocols, potentially impacting clinical outcomes and cost-effectiveness analyses

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Adult Stem Cells Hold the Revenue Lead While iPSC Momentum Builds

Adult stem cells controlled 51.25% of the North America stem cell market in 2025, supported by decades of safety data and streamlined regulatory precedent. Their entrenched clinical use in orthopedic, hematology and autoimmune disorders secures recurrent demand, yet scalability limits remain for large-volume indications. Induced pluripotent counterparts, though smaller today, are climbing at a 9.71% CAGR as CRISPR integration and closed-system bioreactors overhaul production economics.

AI-guided culture optimization is expected to trim Induced Pluripotent Stem Cells (iPSCs) batch failures and compress costs, positioning gene-edited lines for broad allogeneic deployment over the next decade. Ethical constraints continue to confine human embryonic cells to niche research programs, ensuring adult and iPSC lines will shape the commercial core of the North America stem cell industry landscape. The competitive dynamics between these product types are increasingly driven by manufacturing economics rather than purely scientific considerations, with companies seeking the optimal balance between safety, efficacy, and commercial viability.

By Application: Orthopedic Dominance Faces Neurological Upswing

Orthopedic procedures represented 24.75% of 2025 revenue, leveraging well-established intra-articular and spinal applications that align with surgeons’ familiarity and reimbursement pathways. However, neurological indications are projected to post an 11.21% CAGR as first-in-human trials for Parkinson’s disease, spinal cord injury and multiple sclerosis validate durable functional improvements.

Robust Defense Department funding for traumatic brain and nerve injury accelerates translational pipelines, reinforcing confidence among civilian payors. Oncology, cardiovascular and wound-care segments provide ancillary upside but will require continued process-yield gains to temper cost-of-goods concerns across the North America stem cell market. The application landscape is increasingly driven by unmet medical need rather than technical feasibility, with companies focusing on conditions where stem cells can provide unique therapeutic benefits unavailable through traditional pharmaceuticals.

By Treatment Type: Allogeneic Scale Meets Autologous Personalization

Allogeneic therapies delivered 59.55% share of the North America stem cell market size in 2025 because one donor lot can treat hundreds of patients, optimizing facility utilization. Yet, autologous therapy’s 11.45% CAGR highlights how donor-mobilization advances and point-of-care systems make same-day interventions feasible, cutting logistics overhead.

Hybrid “personalized off-the-shelf” concepts—universal donor cells engineered to evade host immunity—are under evaluation, promising to blend allogeneic scale with autologous safety. If validated, they could redirect share within the North America stem cell market by 2030. Companies are pursuing hybrid approaches that combine the scalability benefits of allogeneic manufacturing with the safety advantages of autologous treatment, potentially creating new market segments that bridge traditional treatment categories.

By End User: Academia Leads, Biopharma Accelerates

Academic and research institutes captured 35.90% share in 2025, leveraging grant funding and IRB infrastructure to initiate first-in-human studies. Hospitals are fast-tracking internal centers to retain patients, while cord-blood banks position themselves as upstream suppliers of validated cell lines.

Biopharma and biotech firms, expanding at a 11.78% CAGR, are shifting from licensing dependence to in-house commercialization. Their scaling ambitions—fueled by private-equity injections—translate into heightened demand for automated consumables and analytics software, deepening supply-chain resilience for the broader North America stem cell industry. The end-user landscape is increasingly characterized by collaboration rather than competition, with academic institutions partnering with biopharma companies to leverage complementary strengths in research and commercialization.

Geography Analysis

The United States accounted for 87.75% of 2025 revenue and remains the regulatory and manufacturing nucleus of the North America stem cell market. RMAT designations, plus a clustering effect in Boston and the Bay Area, anchor capital inflows and talent. Florida’s permissive 2025 legislation is catalyzing a new cohort of physician-owned clinics, albeit with mixed payer acceptance.

Canada, projected to log a 11.62% CAGR, benefits from a CAD 30 million federal infusion to expand STEMCELL Technologies’ Vancouver plant, reinforcing domestic GMP capacity and attracting U.S. clinical-trial collaborations. Nationwide single-payer health coverage may streamline reimbursement once clinical efficacy thresholds are met, positioning Canada as a high-growth adjunct within the North America stem cell market.

Mexico’s share is modest but rising on medical tourism; however, regulatory opacity and uneven facility accreditation temper near-term expansion. Cross-border knowledge exchange and manufacturing partnerships suggest incremental harmonization over the next five years, reinforcing continental supply security for the North America stem cell market.

Competitive Landscape

Thermo Fisher Scientific, and Merck KGaA and dominate equipment, reagents and contract manufacturing niches, supplying standardized platforms that underpin GMP compliance. Meanwhile, therapy-focused firms such as Mesoblast, Fate Therapeutics and Lineage Cell Therapeutics advance late-stage pipelines across orthopedics, oncology and neurology. AstraZeneca’s USD 425 million purchase of EsoBiotec illustrates big-pharma appetite for bolt-on cell therapy know-how.

Automation specialists like Cellares and Ori Biotech stake their value on turnkey manufacturing suites capable of 70% labor savings, setting new cost baselines and intensifying price competition in the North America stem cell market. ESG-driven “green bioprocessing” partnerships between Cytiva and Cellular Origins provide early-mover advantages among buyers aiming to cut carbon footprints by 25%.

Disruptors integrating CRISPR editing with iPSC allogeneic lines, such as Century Therapeutics, may redraw competitive boundaries by merging scalability with immune evasion. Should universal donor constructs reach pivotal-trial success, incumbent autologous platforms may confront accelerated obsolescence, raising strategic impetus for joint ventures and technology licensing within the North America stem cell market.

North America Stem Cell Industry Leaders

Becton, Dickinson and Company

Thermo Fisher Scientific

Lineage Cell Therapeutics, Inc.,

Merck KGaA (Sigma Aldrich)

Bristol-Myers Squibb Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Maryland Stem Cell Research Fund awarded USD 18 million to early-stage regenerative projects.

- March 2025: RegeneCyte received FDA approval for its cord-blood stem-cell therapy, marking a milestone for perinatal stem-cell applications.

- July 2024: The Government of Canada invested USD 22.5 million to expand STEMCELL Technologies’ British Columbia biomanufacturing facility, expected to create over 1,000 jobs.

North America Stem Cell Market Report Scope

As per the scope of the report, stem cells are biological cells that can differentiate into other types of cells. Additionally, various types of stem cells are used for therapeutic purposes. With multiple applications at the clinical stage for various diseases, these are being explored extensively by a large number of biopharmaceutical companies in recent times. The North America Stem Cell Market is segmented by Product Type (Adult Stem Cell, Human Embryonic Cell, Pluripotent Stem Cell, and Other Product Types), Application (Neurological Disorders, Orthopedic Treatments, Oncology Disorders, Injuries and Wounds, Cardiovascular Disorders, and Other Applications), Treatment Type (Allogeneic Stem Cell Therapy, Auto logic Stem Cell Therapy, and Syngeneic Stem Cell Therapy) and Geography. The report offers the value (in USD million) for the above segments.

By Product Type

| Adult Stem Cells |

| Induced Pluripotent Stem Cells |

| Human Embryonic Stem Cells |

| Other Product Types |

By Application

| Neurological Disorders |

| Orthopedic Treatments |

| Oncology Disorders |

| Cardiovascular Disorders |

| Injuries and Wounds |

| Other Applications |

By Treatment Type

| Allogeneic Therapy |

| Autologous Therapy |

| Syngeneic Therapy |

By End User

| Hospitals & Specialty Clinics |

| Academic and Research Institutes |

| Biopharma and Biotech Firms |

| Stem-Cell Banks |

| Other End Users |

By Geography

| United States |

| Canada |

| Mexico |

| By Product Type | Adult Stem Cells |

| Induced Pluripotent Stem Cells | |

| Human Embryonic Stem Cells | |

| Other Product Types | |

| By Application | Neurological Disorders |

| Orthopedic Treatments | |

| Oncology Disorders | |

| Cardiovascular Disorders | |

| Injuries and Wounds | |

| Other Applications | |

| By Treatment Type | Allogeneic Therapy |

| Autologous Therapy | |

| Syngeneic Therapy | |

| By End User | Hospitals & Specialty Clinics |

| Academic and Research Institutes | |

| Biopharma and Biotech Firms | |

| Stem-Cell Banks | |

| Other End Users | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current North America stem cell market size?

The North America stem cell market size is USD 8.36 billion in 2026.

What CAGR is expected for the market through 2031?

The market is projected to grow at a 9.95% CAGR between 2026 and 2031.

Which product type dominates revenue?

Adult stem cells lead with 51.25% market share, owing to their long-standing safety record.

Why are neurological applications gaining traction?

Breakthrough trials in Parkinson’s disease and spinal cord injury are driving an 11.21% CAGR in neurological segments.

How are automation platforms influencing manufacturing costs?

Solutions from companies like Cellares could cut labor expenses by up to 70%, lowering per-dose prices and accelerating scale-up.

Which geography shows the fastest growth?

Canada is expected to register a 11.62% CAGR over 2026-2031, supported by federal investment in biomanufacturing infrastructure.

Page last updated on: