Human Embryonic Stem Cells Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

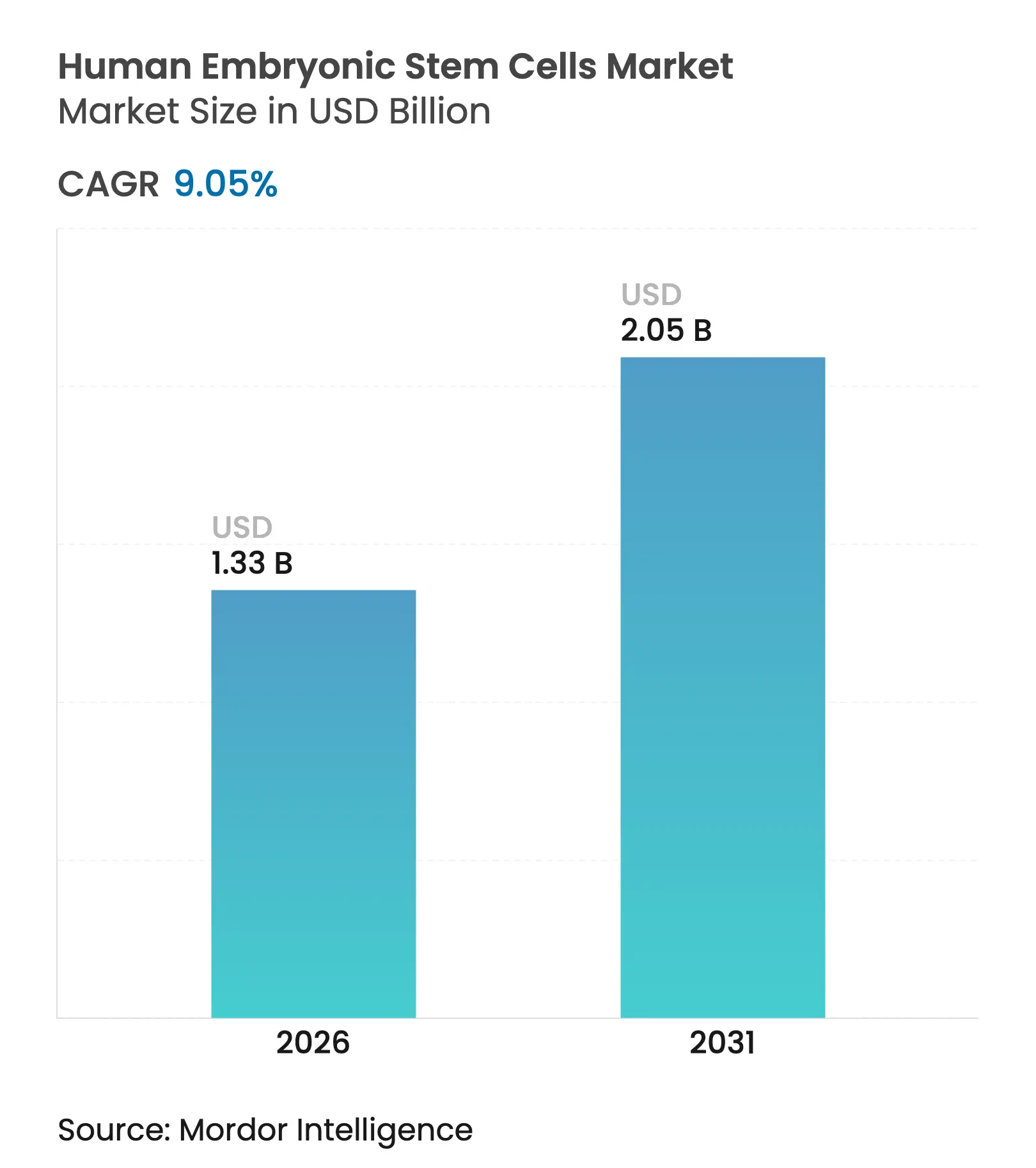

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 9.05 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Human Embryonic Stem Cells Market Analysis by Mordor Intelligence

Advances in CRISPR-enabled line engineering, a steadily growing pool of ethically sourced surplus IVF embryos, and the commercial availability of xeno-free GMP culture systems collectively expand therapeutic horizons across cardiac, retinal, and endocrine disorders. Industrial uptake rises as automated, closed-system bioprocessing cuts contamination risk and doubles batch throughput, sharpening the competitive edge for early movers in the human embryonic stem cells market.[1]Source: Rebecca Ihilchik & Stacey Johnson, “AI-Enabled Biomanufacturing Innovation Enhances Affordability and Access to Cell and Gene Therapies,” ISCT Global, isctglobal.org Regulatory support, exemplified by the FDA’s RMAT pathway and Japan’s fast-track approvals, accelerates clinic-to-market timelines and attracts multi-billion-dollar funding commitments. Meanwhile, cross-disciplinary collaborations between gene-editing pioneers and manufacturing specialists compress development cycles and broaden intellectual-property defensibility within the human embryonic stem cells market. Heightened ethical activism and rising cost pressures remain watchpoints, but technology-driven productivity gains are on track to offset near-term headwinds.

Key Report Takeways

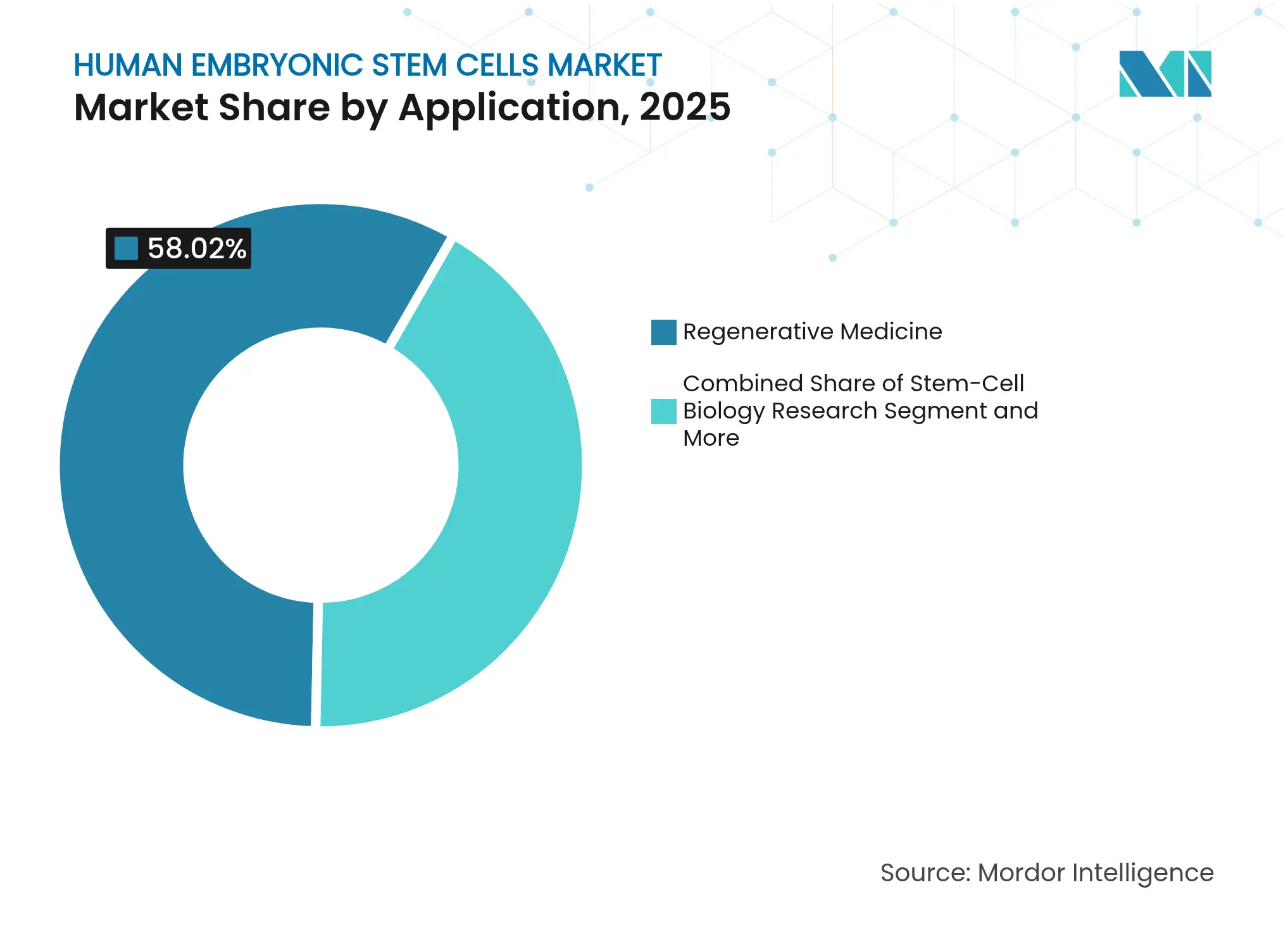

- By application, regenerative medicine held 58.02% of the human embryonic stem cells market share in 2025, while stem-cell biology research is advancing at a 10.45% CAGR through 2031.

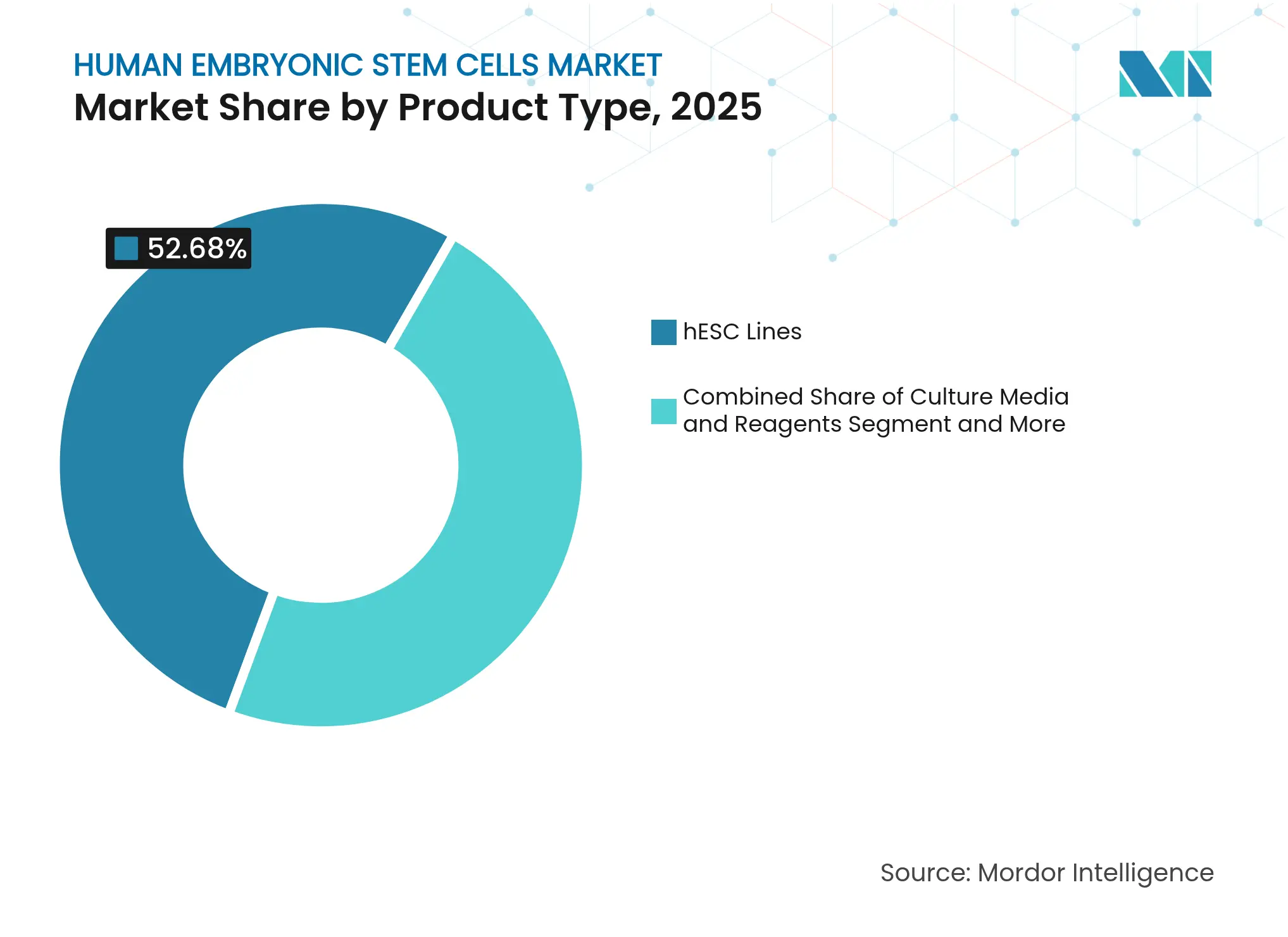

- By product type, hESC lines commanded 52.68% share of the human embryonic stem cells market size in 2025; culture media & reagents are projected to expand at an 11.21% CAGR between 2026 and 2031.

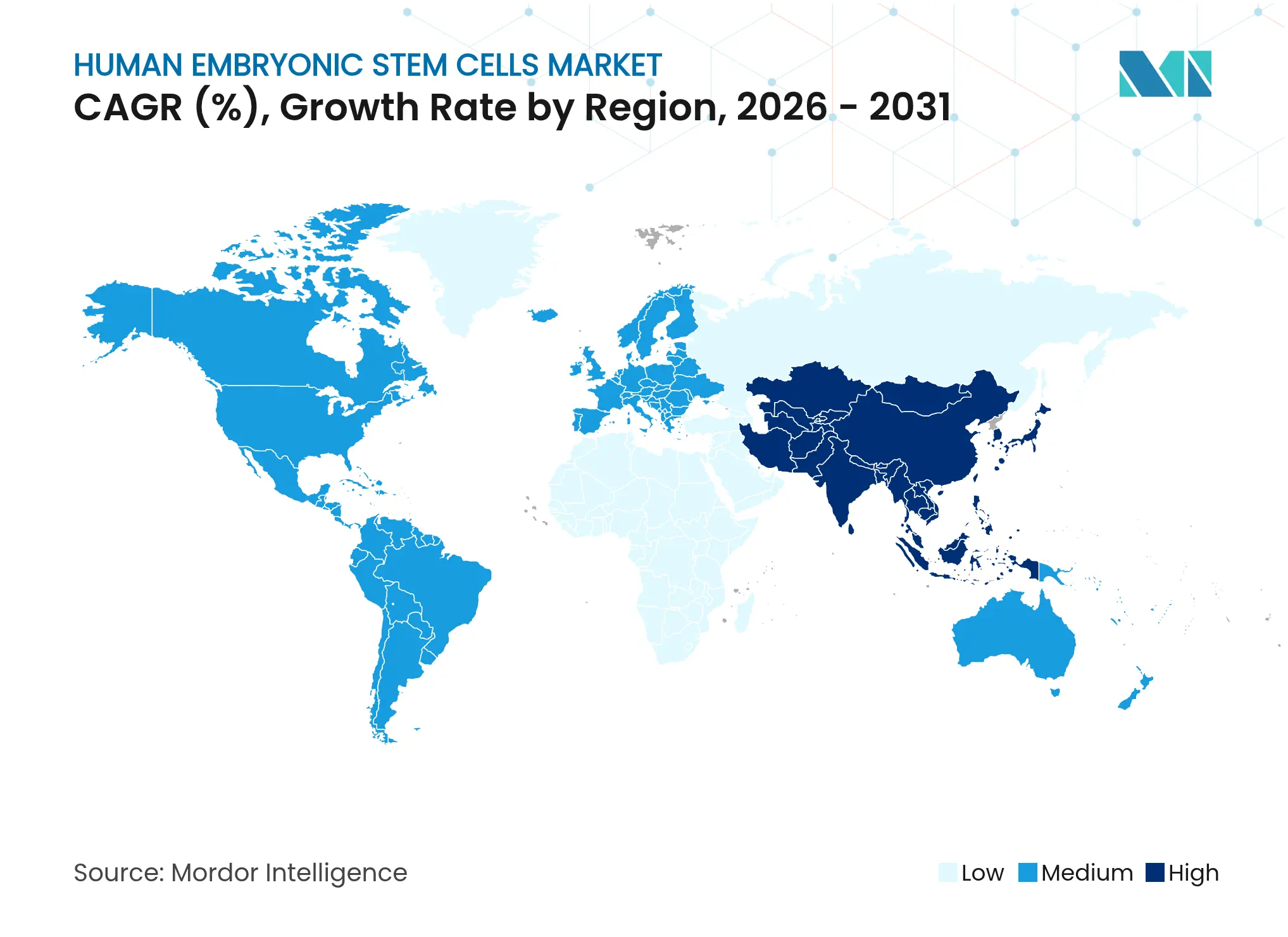

- By geography, North America led with 41.74% revenue share in 2025, whereas Asia-Pacific is forecast to deliver the fastest growth at an 10.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Human Embryonic Stem Cells Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Prevalence of Cardiac and Malignant Diseases

High Prevalence of Cardiac and Malignant Diseases

| +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

Global, with concentration in North America & Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Rising Demand for Regenerative Medicine

Rising Demand for Regenerative Medicine

| +2.1% | Global, led by APAC growth markets | Long term (≥ 4 years) | |||

Growing Government and Private Funding Programs

Growing Government and Private Funding Programs

| +1.5% | North America, Europe, Japan | Short term (≤ 2 years) | |||

CRISPR-enabled hESC Line Engineering

CRISPR-enabled hESC Line Engineering

| +1.2% | Global, with R&D centers in US, UK, Japan | Medium term (2-4 years) | |||

Xeno-free GMP Culture Systems Lower Contamination Risk

Xeno-free GMP Culture Systems Lower Contamination Risk

| +0.9% | Global manufacturing hubs | Short term (≤ 2 years) | |||

Surplus IVF Embryos Expanding Ethical hESC Supply

Surplus IVF Embryos Expanding Ethical hESC Supply

| +0.7% | Regions with established IVF infrastructure | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Prevalence of Cardiac and Malignant Diseases

Cardiovascular disorders and cancer together account for the majority of mortality worldwide, creating sustained clinical demand for multi-lineage repair solutions. Human embryonic stem-cell-derived cardiac spheroids restore contractility in porcine infarct models and are now entering first-in-human ischemic cardiomyopathy trials. hESC-derived islet cells (VX-880) achieved insulin independence in 10 of 12 type 1 diabetes patients, underscoring the breadth of application potential. Commercial interest intensifies as population-level spending on cardiac care exceeds USD 350 billion, positioning cardiometabolic programs as headline value drivers within the human embryonic stem cells market. Additive-manufacturing breakthroughs, such as 3-D-printed myocardium scaffolds seeded with hESCs, further shorten translational pathways.[2]Source: Sena Quinn, “3D-Printing Heart Tissue With Human Stem Cells,” Lifeboat Foundation, lifeboat.com Collectively, these data validate disease-modifying potential and reinforce premium pricing opportunities through 2030.

Rising Demand for Regenerative Medicine

More than 1,200 active cell and gene therapy trials in the United States showcase how regenerative medicine is moving from fringe to frontline care. Allogeneic platforms that rely on human embryonic stem cells enable off-the-shelf dosing, solving historical scale limitations of autologous procedures. Japan’s 60-plus iPS cell studies illustrate how cohesive policy, reimbursement clarity, and manufacturing incentives foster accelerated adoption. The FDA’s landmark approval of a mesenchymal stromal cell therapy signals regulator readiness to clear clinically validated products, indirectly benefiting hESC developers. Vision-restoration successes using hESC-derived corneal epithelium (≥90% efficacy) elevate public trust, fueling positive feedback loops for patient recruitment and investor inflows.

Growing Government and Private Funding Programs

CIRM’s USD 5 billion endowment anchors the United States as a capital-rich environment for translational research. Public grants de-risk early studies, crowding-in venture capital and strategic pharma partnerships across the human embryonic stem cells market. Japan’s conditional approval framework complements state-backed infrastructure spending, prompting global firms to locate GMP suites near Tokyo for faster market entry. On the private side, multi-year agency contracts—such as BARDA’s stem-cell-derived platelet program—illustrate expanding defense and emergency-response use cases that diversify revenue streams. These parallel funding channels magnify discovery velocity and compress commercialization risk.

CRISPR-Enabled hESC Line Engineering

CRISPR prime editing achieves 36–73% on-target efficiencies in pluripotent cells, enabling rapid construction of isogenic disease models and low-immunogenicity therapeutic lines. Cas12a-multiplex systems now permit simultaneous insertion of multiple edits, accelerating candidate screening cycles. Proof-of-concept work eliminating HLA-A, -B, and -C antigens shows promise for universal donor cells, although transplant rejection in immunocompetent mice underscores the need for combinatorial immune-evasion strategies. Large-scale variant libraries generated at the Wellcome Sanger Institute provide unmatched resources for target validation and toxicity screening. Cumulatively, precision editing lowers downstream attrition and enhances product-portfolio optionality across the human embryonic stem cells market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Treatment and Production Cost

High Treatment and Production Cost

| -1.4% | Global, particularly in cost-sensitive markets | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

Global, particularly in cost-sensitive markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Stringent and Heterogeneous Global Regulations

Stringent and Heterogeneous Global Regulations

| -1.1% | Global, with varying regional intensity | Long term (≥ 4 years) | |||

Fast-Growing iPSC Alternatives Cannibalise Funding

Fast-Growing iPSC Alternatives Cannibalise Funding

| -0.8% | Global R&D centers | Medium term (2-4 years) | |||

Social-Media–Driven Ethical Activism Dampens Adoption

Social-Media–Driven Ethical Activism Dampens Adoption

| -0.6% | Primarily Western markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Treatment and Production Cost

Current hESC-based therapies often exceed USD 100,000 per dose, driven by manual clean-room operations and low process yields. AI-guided robotics slash labor inputs by 50% and deliver lot-to-lot consistency, pointing to breakeven manufacturing at sub-USD 50,000 within five years. Thermo Fisher’s USD 475 million CDMO site in New Jersey exemplifies industry-scale investment targeting cost compression and regulatory compliance. Modular robotic clusters reproducibly handle expansion, harvesting, and final fill-finish, shortening campaign times and reducing batch failure risk. Predictive AI models from Northeastern University further optimize nutrient feeds and passage timing, pushing yields toward industrial benchmarks. These gains must sustain momentum to offset payer scrutiny and price-sensitive emerging-market demand.

Stringent and Heterogeneous Global Regulations

Developers navigate a patchwork of approval requirements, from the EU’s 2027 SoHO regulation to the FDA’s stepped enforcement against unlicensed clinics.[3]Source: Sarah Rosenthaler, “New EU Regulation on Substances of Human Origin,” Schoenherr, schoenherr.eu Japan’s embryo-model guidelines, due for revision in 2025, illustrate how forward-looking policy can spur investment yet also reshape compliance workloads. The International Society for Cell & Gene Therapy’s APAC roadmaps aim at harmonization, but until adopted, divergent dossiers inflate administrative cost. US political discourse around federal funding bans adds uncertainty to long-range capital planning.

Segment Analysis

By Application: Regenerative Medicine Drives Clinical Translation

Regenerative medicine captured 58.02% of the human embryonic stem cells market share in 2025, buoyed by clinical readouts such as +5.5-letter visual-acuity gains for OpRegen in geographic atrophy patients. Spinal cord repair, pancreatic islet replacement, and cardiac remuscularization now headline multi-center trials, reinforcing the segment’s dominant revenue trajectory. As more programs secure RMAT or Sakigake designations, payers gain real-world evidence to justify reimbursement, fueling a virtuous adoption cycle within the human embryonic stem cells market.

Stem-cell biology research, registering a 10.45% CAGR to 2031, benefits from automated genome-editing screens and organoid platforms capable of recapitulating human tissue complexity. CRISPR-powered lineage-tracing and high-content phenomics shorten target-identification timelines, while novel organoid co-culture systems elevate disease-model accuracy five-fold. As academic core facilities transition to fee-for-service models, research spending funnels back into reagents and line-licensing royalties, enlarging recurring-revenue pools for supply-chain participants. The human embryonic stem cells market size for discovery applications is projected to climb steadily as multiplex screens become integral to precision-medicine pipelines.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: hESC Lines Dominate Despite Culture Media and Reagents Growth

Commercially established hESC lines held 52.68% share of the human embryonic stem cells market size in 2025, underpinned by scalable master-cell-bank infrastructure and mature regulatory precedents. Universal-donor editing strategies promise broader patient coverage without bespoke manufacturing, keeping line licensing attractive for big pharma seeking rapid entry. GMP culture media, reagents, and ancillary kits form a high-margin supply tier; customized xeno-free formulations from Lonza lock in recurring demand through process validation cycles.

Culture media and reagents, expanding at an 11.21% CAGR, ride the personalized-medicine wave, particularly for inherited disorders where patient-specific corrections minimize rejection risk. Instruments and consumables suppliers leverage this shift by bundling hardware-software suites, evidenced by Terumo-CiRA’s automated iPS cell workstations that achieve 90% labor savings. As COGS decline, autologous pipelines could capture niche orphan-disease markets, complementing mass-market allogeneic products.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained 41.74% of global revenue in 2025, anchored by robust NIH and CIRM funding, RMAT-enabled fast-track reviews, and extensive CDMO capacity. Stanford-led cardiac trials, Northwestern’s spinal cord initiatives, and Thermo Fisher’s new Princeton site collectively exhibit the region’s lab-to-launch integration. Political uncertainty around federal funding for embryonic research poses a strategic risk, but diversified private investment cushions potential public-budget fluctuations.

Asia-Pacific is the fastest-growing cluster, advancing at an 10.98% CAGR through 2031 on the back of Japan’s conditional-approval regime and China’s state-backed research parks. Over 60 active Japanese clinical trials highlight regulatory agility, while Sumitomo Pharma and Nikon-Lonza manufacturing alliances demonstrate capital inflows from multinational partners. Government grants cover facility build-outs and workforce training, amplifying local supply-chain maturity within the human embryonic stem cells market.

Europe’s outlook hinges on effective rollout of the SoHO regulation in 2027. Germany and the United Kingdom maintain leading academic clusters; the UK’s code of practice for synthetic embryos signals policy innovation that may shape continental standards. France and Italy focus on ophthalmology and cartilage repair niches, while Scandinavian consortia invest in cryogenic logistics to widen patient access. Western European reimbursement hurdles persist, but cross-border collaboration and EU-wide HTA reforms are expected to streamline market access for certified products.

Competitive Landscape

Market Concentration

Competition is moderate, characterized by a mix of large-cap pharmaceuticals and niche biotechs pursuing first-in-class indications. Vertex Pharmaceuticals leveraged focused R&D spend to deliver VX-880 data showing insulin independence in 83% of treated patients, validating the value of single-asset depth. Lineage Cell Therapeutics exemplifies pipeline breadth, running concurrent late-stage ophthalmology and early spinal-cord programs to hedge development risk. Astellas Pharma’s robotics alliance with Yaskawa points to manufacturing scalability as a key battleground, where cycle-time reductions translate directly into competitive pricing.

Emerging technology entrants, including Nikon and OmniaBio, monetize AI-enabled quality-control algorithms, differentiating on cost-per-million-cells metrics. Universal-donor cell engineering is a white-space arena, with academic-industry consortia racing to refine multi-gene-edited platforms that can evade complement and NK-cell responses.

As patent cliffs approach for first-generation hESC lines, brand equity will increasingly hinge on manufacturing competency and clinical-outcomes datasets rather than basic IP protection. The overall tenor of competition suggests further consolidation as scale becomes indispensable to navigate global regulatory divergence.

Human Embryonic Stem Cells Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: The Allen Institute and NYSCF partnered to integrate structural cell tags into ethnically diverse stem-cell libraries to improve disease-model inclusivity.

- September 2024: EPFL inaugurated SCOL, a shared organoid and iPSC facility available to all campus research groups for translational stem-cell projects.

Table of Contents for Human Embryonic Stem Cells Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1High prevalence of cardiac & malignant diseases

- 4.2.2Rising demand for regenerative medicine

- 4.2.3Growing government & private funding programs

- 4.2.4CRISPR-enabled hESC line engineering

- 4.2.5Xeno-free GMP culture systems lower contamination risk

- 4.2.6Surplus IVF embryos expanding ethical hESC supply

- 4.3Market Restraints

- 4.3.1High treatment & production cost

- 4.3.2Stringent & heterogeneous global regulations

- 4.3.3Fast-growing iPSC alternatives cannibalise funding

- 4.3.4Social-media–driven ethical activism dampens adoption

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter’s Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers/Consumers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value – USD)

- 5.1By Application

- 5.1.1Regenerative Medicine

- 5.1.2Stem-Cell Biology Research

- 5.1.3Tissue Engineering

- 5.1.4Toxicology Testing

- 5.2By Product Type

- 5.2.1hESC Lines

- 5.2.2Culture Media & Reagents

- 5.2.3Instruments & Consumables

- 5.3By Geography

- 5.3.1North America

- 5.3.1.1United States

- 5.3.1.2Canada

- 5.3.1.3Mexico

- 5.3.2South America

- 5.3.2.1Brazil

- 5.3.2.2Argentina

- 5.3.2.3Rest of South America

- 5.3.3Europe

- 5.3.3.1Germany

- 5.3.3.2United Kingdom

- 5.3.3.3France

- 5.3.3.4Italy

- 5.3.3.5Spain

- 5.3.3.6Rest of Europe

- 5.3.4APAC

- 5.3.4.1China

- 5.3.4.2Japan

- 5.3.4.3India

- 5.3.4.4Australia

- 5.3.4.5South Korea

- 5.3.4.6Rest of APAC

- 5.3.5Middle East & Africa

- 5.3.5.1GCC

- 5.3.5.2South Africa

- 5.3.5.3Rest of MEA

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1Astellas Pharma Inc.

- 6.4.2Thermo Fisher Scientific Inc.

- 6.4.3Merck KGaA

- 6.4.4STEMCELL Technologies Inc.

- 6.4.5Takara Bio Inc.

- 6.4.6Lineage Cell Therapeutics Inc.

- 6.4.7PeproTech Inc.

- 6.4.8PromoCell GmbH

- 6.4.9Vertex Pharmaceuticals

- 6.4.10Lonza Group AG

- 6.4.11BD Biosciences

- 6.4.12GE HealthCare

- 6.4.13ViaCyte Inc.

- 6.4.14Fate Therapeutics

- 6.4.15BlueRock Therapeutics

- 6.4.16Cynata Therapeutics

- 6.4.17Pluri Inc.

- 6.4.18Organovo Holdings Inc.

- 6.4.19Samsung Biologics

- 6.4.20Cell Engineering Corp.

- 6.4.21Janssen (Cell Therapy Grp)

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Human Embryonic Stem Cells Market Report Scope

Human embryonic stem cells are pluripotent stem cells that are extracted from the inner cell mass of a blastocyst, which is an early-stage pre-implantation embryo. These stem cells are used for the treatment of various diseases.

The human embryonic stem cells market is segmented by application and geography. By application, the market is segmented into regenerative medicine, stem cell biology research, tissue engineering, and toxicology testing. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of USD value.