Adult Stem Cells Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

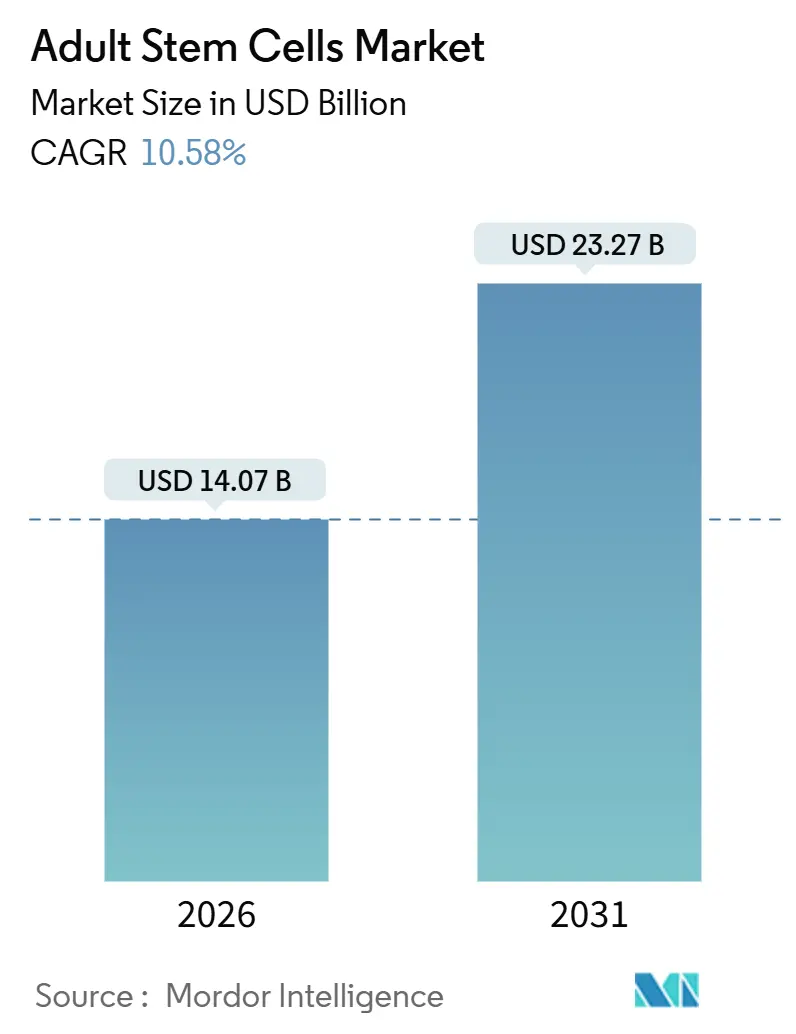

| Market Size (2026) | USD 14.07 Billion |

| Market Size (2031) | USD 23.27 Billion |

| Growth Rate (2026 - 2031) | 10.58% CAGR |

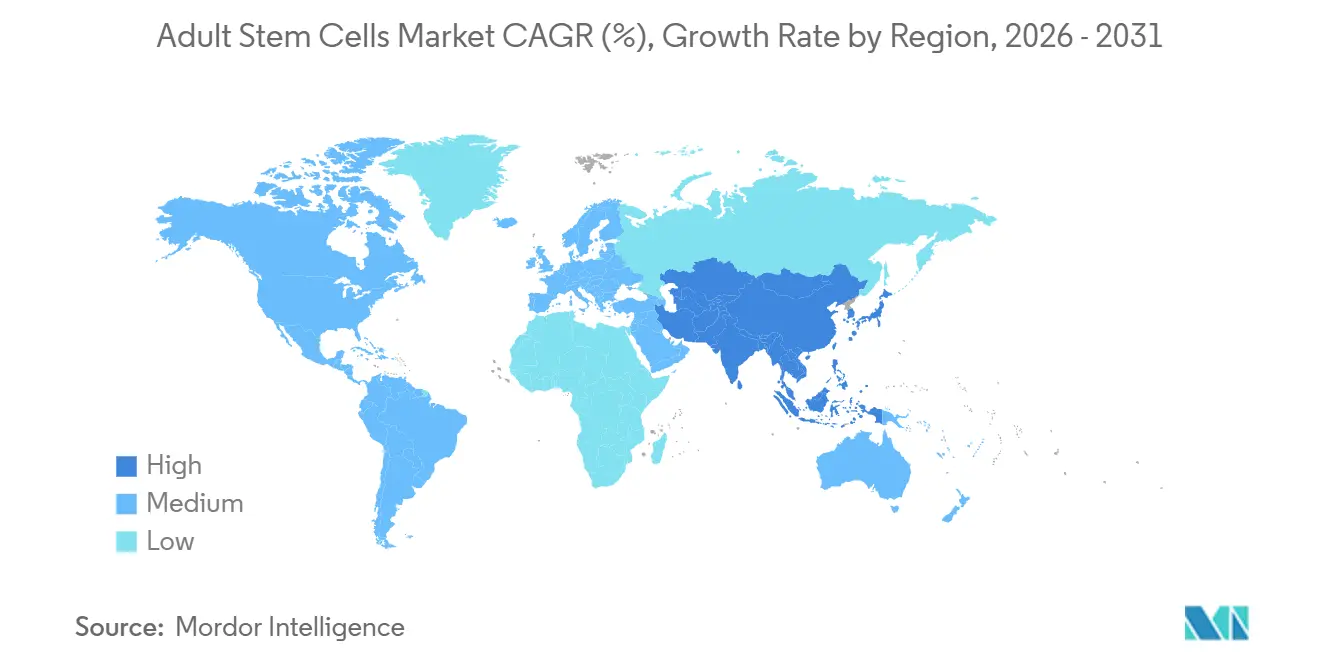

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adult Stem Cells Market Analysis by Mordor Intelligence

The Adult Stem Cells Market size is estimated at USD 14.07 billion in 2026, and is expected to reach USD 23.27 billion by 2031, at a CAGR of 10.58% during the forecast period (2026-2031).

This growth reflects regulatory green lights such as the FDA’s first-in-class approval of Ryoncil in 2024 and the EMA’s conditional nod for Zemcelpro in 2025, alongside manufacturing breakthroughs that are trimming the cost of goods by up to 40% through AI-driven quality control and closed-system bioreactors[1]Nature Biotechnology, “AI-Driven Quality Control for Stem Cell Manufacturing,” nature.com . Allogeneic products currently dominate the adult stem cells market, yet autologous platforms are advancing more quickly, buoyed by personalized safety profiles. Peripheral and umbilical blood sources are eroding bone marrow's historical lead thanks to non-invasive collection protocols, while regenerative medicine applications still account for well over 90% of revenue. Geographically, North America is the most significant contributor, but Asia-Pacific is outpacing every other region on the back of rapid clinical-trial activity and streamlined approval pathways.

Key Report Takeaways

- By therapy type, allogeneic products held 58.13% of the Adult Stem Cells market share in 2025, whereas autologous therapies are projected to expand at a 13.41% CAGR to 2031.

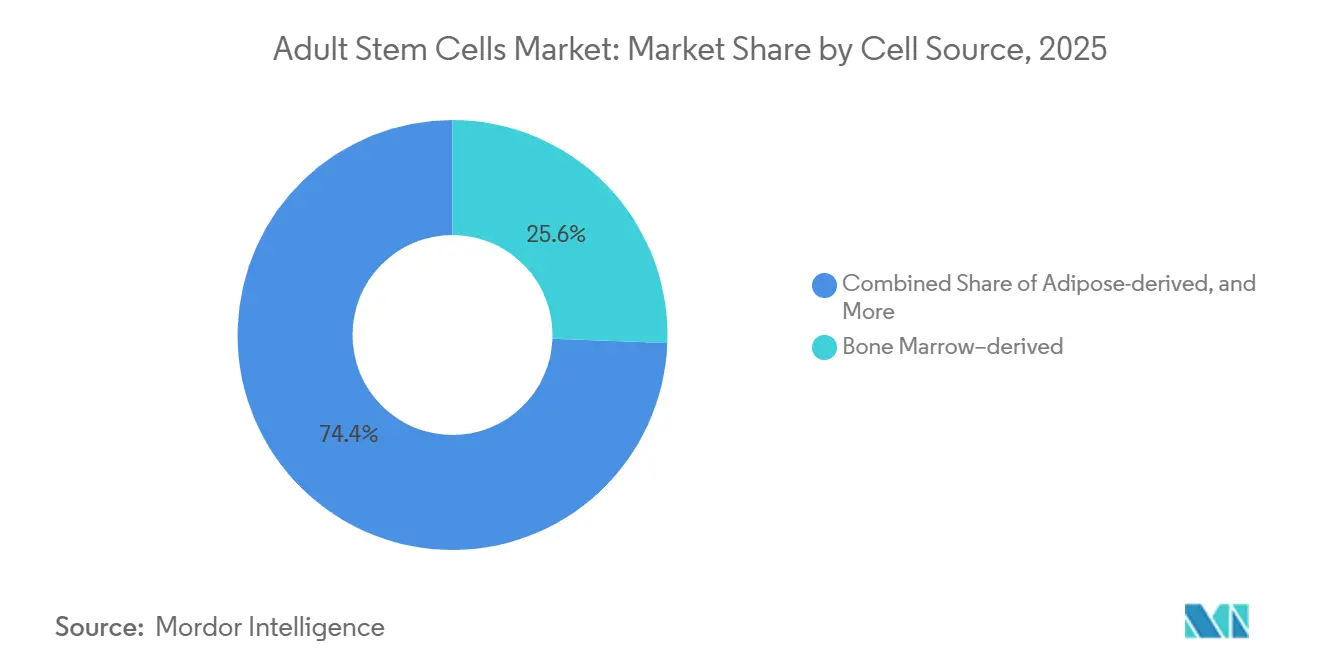

- By cell source, bone marrow retained 25.55% of 2025 revenue, while peripheral and umbilical blood sources are forecast to grow at a 13.25% CAGR through 2031.

- By application, regenerative medicine accounted for 92.53% of the Adult Stem Cells market in 2025, and drug discovery is advancing at a 12.85% CAGR through 2031.

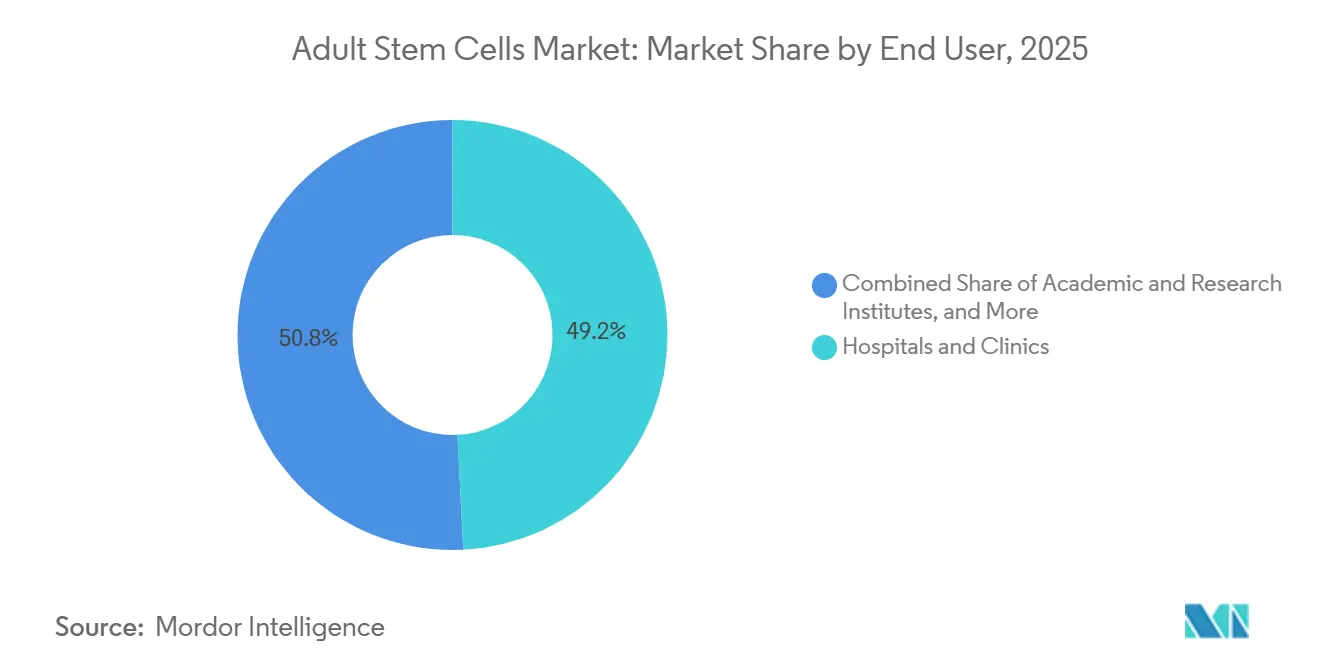

- By end user, hospitals and clinics accounted for 49.23% of 2025 sales, yet contract research organizations are recording the fastest growth at 11.55% CAGR through 2031.

- By geography, North America led with a 44.23% revenue share in 2025, while Asia-Pacific recorded the fastest regional CAGR of 12.81% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Adult Stem Cells Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic & Degenerative Disease Burden | +2.3% | Global, acute in North America & Europe | Long term (≥ 4 years) |

| Advances in Bioreactor and Xeno-Free Manufacturing | +1.8% | North America & EU hubs, spillover to Asia-Pacific | Medium term (2–4 years) |

| Expanding Government & Private Funding | +1.5% | North America, China, Japan | Medium term (2–4 years) |

| Regulatory Incentives (FDA RMAT, EMA PRIME) | +2.0% | North America & EU, adoption in South Korea & Japan | Short term (≤ 2 years) |

| IPSC-Derived MSC Platforms | +1.7% | Global, led by U.S. & Japan | Long term (≥ 4 years) |

| AI-Driven QC & Process Analytics | +1.2% | North America, EU, China | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic & Degenerative Disease Burden

Cardiovascular diseases claimed 19.8 million lives in 2024, and heart failure afflicts 64 million patients who still face 50% five-year mortality despite optimal therapy[2]World Health Organization, “Cardiovascular Diseases,” who.int. Mesenchymal stromal cells reduced heart-failure hospitalizations by 35% in a recent Phase 3 trial, framing them as adjuncts rather than replacements for devices[3]The Lancet, “Mesenchymal Stromal Cells for Heart Failure,” thelancet.com. Diabetes prevalence is projected to hit 783 million by 2045, yet durable glycemic control remains elusive in most patients, positioning adipose-derived cells for pancreatic islet regeneration. Together, these trends are expanding the eligible patient pool at an 8%–10% annual clip, and early payer analyses suggest that cell therapies can rival lifelong pharmacotherapy in cost-effectiveness when clinical durability exceeds 2 years.

Advances in Bioreactor and Xeno-Free Manufacturing

Lonza’s hollow-fiber Quantum platform achieves 10-fold higher cell densities than in T-flasks while preserving critical surface markers at> 95%. Clinical-grade xeno-free media, driven by human platelet lysate, have replaced fetal bovine serum in 70% of commercial processes, shaving four to six months from regulatory review. Vertical-wheel systems reduce batch variability to below 15%, and automated platforms like AutoCRAT reduce operator touch time by 60%. Collectively, these innovations are pushing the Adult Stem Cells market cost curves down from USD 150,000 per batch in 2024 to a projected USD 80,000 by 2028, widening access in price-sensitive regions.

Expanding Government & Private Funding Pipelines

The NIH boosted its regenerative medicine budget to USD 1.5 billion for 2024, prioritizing iPSC and gene-editing programs[4]National Institutes of Health, “NIH Regenerative Medicine Budget,” nih.gov . Venture capital poured USD 2.8 billion into stem-cell companies in 2024, led by Sana Biotechnology’s USD 300 million raise. China’s Ministry of Science and Technology launched a USD 500 million fund in 2025 while Japan earmarked JPY 20 billion for iPSC cardiomyocyte work, aiming for three cardiac approvals by 2028. Cross-border pharmaceutical partnerships further validate the platform, accelerating commercialization cycles

Regulatory Incentives for Adult Stem Cells Development

Eighteen candidates received FDA RMAT status in 2025, enabling rolling BLA submissions and trimming development timelines by a year. The EMA’s PRIME scheme provided early advice to 12 MSC programs in 2024, while Japan’s conditional approval framework enabled Heartseed to commercialize iPSC cardiomyocytes based on Phase 2 efficacy data. South Korea’s fast-track act covered five autologous therapies in 2025, demonstrating the global spread of pro-innovation policies.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Therapy/Manufacturing Cost & Weak Reimbursement | -0.9% | Global, acute in U.S. & EU | Long term (≥ 4 years) |

| Regulatory Heterogeneity and Long Approval Timelines | -0.6% | Global, fragmented in Asia-Pacific & South America | Medium term (2–4 years) |

| Donor Epigenetic Drift | -0.4% | Global manufacturing sites | Medium term (2–4 years) |

| Dependency on Single-Use Plastics | -0.3% | North America & EU clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Therapy/Manufacturing Cost & Weak Reimbursement

Patient-specific therapies range from USD 200,000 to USD 500,000 per course, reflecting the costs of in-house manufacturing and disposables. Medicare covers fewer than 10 indications as of 2026, leaving large-volume conditions such as osteoarthritis and heart failure unfunded[5]Centers for Medicare & Medicaid Services, “National Coverage Determination for Stem Cell Transplantation,” cms.gov. European HTA bodies require five years of durability before green-lighting payments. Still, most trials offer only two-year data, supply-chain bottlenecks, highlighted by a 2024 shortage of single-use plastic bioreactor bags, compound financial pressure. Outcomes-based contracts are emerging as a potential source of relief but shift risk to manufacturers.

Regulatory Heterogeneity and Long Approval Timelines

Stem-cell products navigate divergent classifications: the FDA requires a full BLA, whereas Brazil treats minimally manipulated autologous cells as medical devices. Follow-up requirements vary from 1 year in Japan to 3 years in China, forcing sponsors into parallel trials that inflate costs by 30%. Potency assay standards also vary, hindering global comparability despite ISCT guidelines. These inconsistencies can stretch development to a decade, deterring early-stage investors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cell Source: Peripheral Blood Gains on Mobilization Protocols

Bone marrow-derived cells accounted for 25.55% of the Adult Stem Cells market share in 2025, thanks to decades of clinical precedent in hematopoietic transplantation. Peripheral and umbilical blood sources, however, are growing at a 13.25% CAGR, fueled by CXCR4 antagonist-based mobilization that yields 5-10 million CD34+ cells per apheresis session. Adipose-derived MSCs produce 500-fold more cells per gram than bone marrow, making them attractive for large-batch allogeneic runs even though their osteogenic potential lags 20%–30% in head-to-head studies.

Umbilical cord blood banking surpassed 5 million stored units globally in 2025, with private banks in China and India capturing most new collections. Fresh FDA draft guidance now mandates 15-year stability validation, a bar that threatens under-capitalized banks. Next-generation mobilizers allow single-session peripheral collections, cutting costs by 40% and boosting donor convenience.

By Application: Drug Discovery Scales on Organoid Adoption

Regenerative medicine accounted for 92.53% of the Adult Stem Cells market in 2025, with cardiovascular, orthopedic, and neurological programs contributing the bulk of revenue. Drug discovery applications are expanding at a 12.85% CAGR as pharma switches to iPSC-derived hepatocytes, cardiomyocytes, and neurons that predict human toxicity with 85% sensitivity. Patient-derived models informed the design of AMX0035 in ALS and underpinned its FDA nod in 2024.

Organoids that replicate organ architecture are replacing 2D cultures in 40% of early-stage screens, raising translational success rates from 10% to 18%. European REACH rules mandating non-animal safety testing further increase demand for stem-cell assays. Service CROs have seized the opportunity, bundling potency assays and disease modeling into turnkey packages.

By Therapy Type: Autologous Gains on Safety Profile

Allogeneic therapies accounted for 58.13% of the Adult Stem Cells market in 2025, driven by their off-the-shelf availability, which shortens initiation from 6 weeks to 2 days. Yet autologous options are growing faster, at a 13.41% CAGR, because they sidestep immune rejection and qualify for streamlined regulation in several countries. Donor-specific antibody formation undercuts efficacy in about 30% of allogeneic recipients after the third infusion.

Hybrid approaches use gene-edited iPSC-NK cells that express HLA-E and delete CD38 to evade immune recognition and extend persistence to 28 days. Japan and South Korea reimburse autologous MSCs more generously than allogeneic products, thereby reinforcing demand in Asia-Pacific.

By End User: CROs Capture Outsourcing Wave

Hospitals and clinics accounted for 49.23% of Adult Stem Cells market sales in 2025 through point-of-care autologous injections for osteoarthritis and wound healing. CRO revenue is growing at a 11.55% CAGR as pharma outsources cell-line development, potency testing, and regulatory documentation, which can cost up to USD 2 million per program. Asia-Pacific CDMOs such as WuXi AppTec deliver the same GMP services at 40% lower cost, accelerating market penetration.

Academic demand remains strong, accounting for one-quarter of reagents used to probe differentiation pathways that feed future pipelines. Big Pharma is shifting from outsourcing to ownership; Pfizer stood up an internal iPSC platform in 2024, and Roche spent USD 1.2 billion to acquire a cardiomyocyte library, signaling longer-term vertical integration.

Geography Analysis

North America commanded 44.23% of the 2025 adult stem cells market share, anchored by FDA approvals and a USD 1.5 billion NIH budget that funded 120 clinical studies. Boston and San Francisco supply 60% of U.S. production capacity, leveraging local venture funding and academic expertise. Canada issued three conditional approvals in 2025, while Mexico has emerged as a budget-friendly destination for autologous procedures, albeit with patchy oversight.

Asia-Pacific leads growth at a 12.81% CAGR. China registered more than 200 active trials in 2025, and its fast-track pathway cleared five MSC products for COVID-19-related ARDS. Japan granted Heartseed’s iPSC cardiomyocytes conditional approval within 7 years of Phase 1 data, half the historic timeline. South Korea is building a national HLA-typed MSC bank, and India drew 50,000 foreign patients for stem-cell care in 2025 despite uneven regulation.

Europe remains a pivotal contributor. The EMA okayed Zemcelpro for critical limb ischemia in 2025, and NICE issued positive reimbursement guidance for Strimvelis earlier in 2024. France is co-funding a Lyon manufacturing hub, while the United Arab Emirates and South Africa are piloting early programs amid reimbursement gaps.

Competitive Landscape

The adult stem cells industry is moderately fragmented. Top players Mesoblast, Lonza, Thermo Fisher Scientific, Inc., Fate Therapeutics, and Osiris Therapeutics own the largest slices. Yet, white space abounds in indications such as critical limb ischemia and spinal cord injury. Fate Therapeutics and Heartseed pursue platform strategies with iPSC master cell banks supplying multiple programs, whereas BrainStorm focuses on ALS and progressive MS.

Technology adoption is a differentiator. Lonza’s Cocoon closed-system bioreactor has sealed 15 deals since its 2024 debut, cutting contamination risks tenfold compared to open flasks. Sana Biotechnology is developing hypoimmune iPSC cells designed to evade both T cells and NK cells, potentially obsoleting HLA matching. Combination approaches remain underexplored; fewer than 5 trials have paired MSCs with checkpoint inhibitors despite promising preclinical synergy.

Regulatory compliance is becoming a moat. Facilities with FDA-certified processes can charge 20% premiums and secure exclusive hospital contracts, concentrating revenue among established producers. Patent estates reinforce barriers, with Mesoblast holding 150 patents on MSC potency assays and Fate filing 80 on iPSC differentiation.

Adult Stem Cells Industry Leaders

Mesoblast

Lonza

Thermo Fisher Scientific, Inc.

Fate Therapeutics

Osiris Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Nature Cell announced the U.S. expansion of Vascostem for critical limb ischemia after favorable pilot outcomes.

- August 2025: Hope Biosciences received Regenerative Medicine Advanced Therapy (RMAT) status for adipose-derived MSCs to treat multiple sclerosis, following promising Phase 2 data.

Global Adult Stem Cells Market Report Scope

As per the report's scope, adult stem cells are undifferentiated cells found in specific tissues of the body after development. They can self‑renew and to generate specialized cell types of the organ or tissue in which they reside. Their primary role is to replenish dying cells and repair damaged tissues, maintaining normal function throughout life. Unlike embryonic stem cells, they are present in juvenile and adult organisms, including humans.

The adult stem cells market segmentation includes cell source, application, therapy type, end user, and geography. By cell source, the market is segmented into bone marrow–derived, adipose-derived, peripheral/umbilical blood–derived, and dental-pulp & other adult sources. By application, the market is segmented into regenerative medicine, drug discovery & development, and disease modelling & toxicology. By therapy type, the market is segmented into autologous and allogeneic. By end user, the market is segmented into hospitals & clinics, academic & research institutes, pharmaceutical & biotechnology companies, and contract research organizations. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Bone Marrow-derived |

| Adipose-derived |

| Peripheral / Umbilical Blood-derived |

| Dental-pulp & Other Adult Sources |

| Regenerative Medicine |

| Drug Discovery & Development |

| Disease Modelling & Toxicology |

| Autologous |

| Allogeneic |

| Hospitals & Clinics |

| Academic & Research Institutes |

| Pharmaceutical & Biotechnology Companies |

| Contract Research Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Cell Source | Bone Marrow-derived | |

| Adipose-derived | ||

| Peripheral / Umbilical Blood-derived | ||

| Dental-pulp & Other Adult Sources | ||

| By Application | Regenerative Medicine | |

| Drug Discovery & Development | ||

| Disease Modelling & Toxicology | ||

| By Therapy Type | Autologous | |

| Allogeneic | ||

| By End User | Hospitals & Clinics | |

| Academic & Research Institutes | ||

| Pharmaceutical & Biotechnology Companies | ||

| Contract Research Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of the adult stem cells field?

The space is valued at USD 14.07 billion in 2026 and is projected to reach USD 23.27 billion by 2031.

Which therapy type is expanding most rapidly?

Autologous platforms are posting a 13.41% CAGR through 2031, outpacing allogeneic products.

How fast are Asia-Pacific revenues growing?

Regional sales are advancing at a 12.81% CAGR, the quickest pace worldwide.

What remains the biggest hurdle to reimbursement in the United States?

Medicare currently covers fewer than 10 stem-cell indications, leaving high-volume conditions such as osteoarthritis and heart failure unfunded.

By how much can next-generation bioreactor technology reduce production costs?

Automated, xeno-free systems are projected to cut cost-of-goods from USD 150,000 per batch in 2024 to roughly USD 80,000 by 2028.

Which company currently commands the largest share among manufacturers?

Mesoblast leads, followed closely by Lonza, Thermo Fisher Scientific, Fate Therapeutics, and Osiris Therapeutics.

Page last updated on: