Ruggedized Network Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

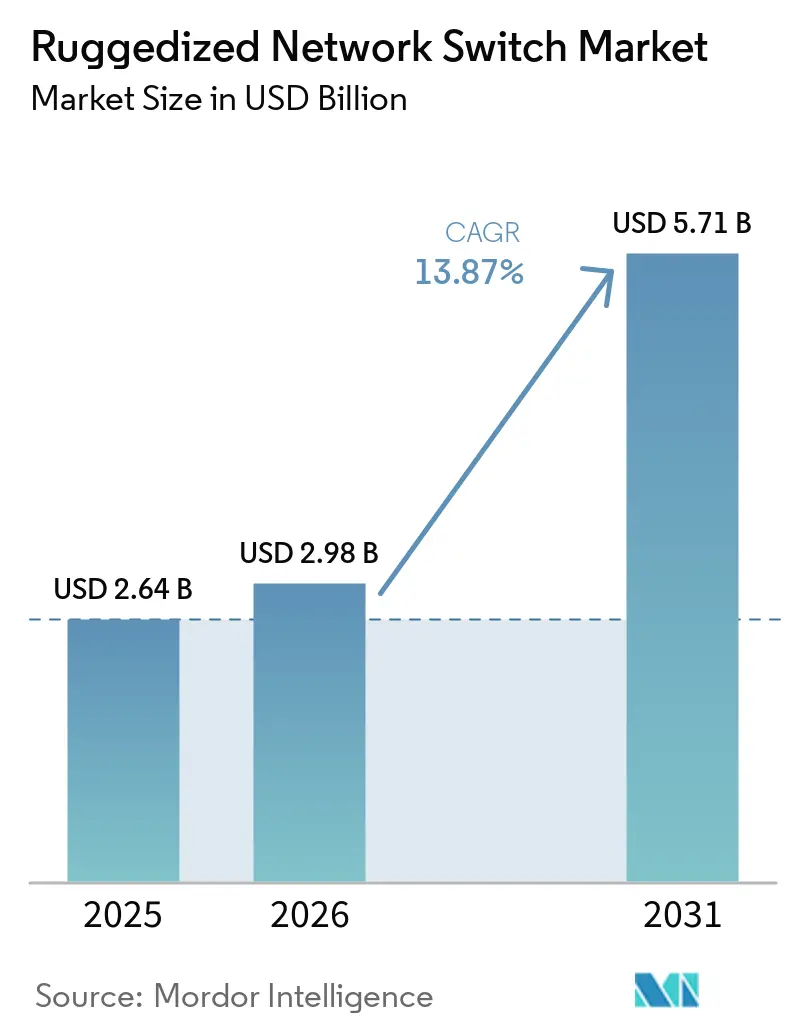

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 5.71 Billion |

| Growth Rate (2026 - 2031) | 13.87% CAGR |

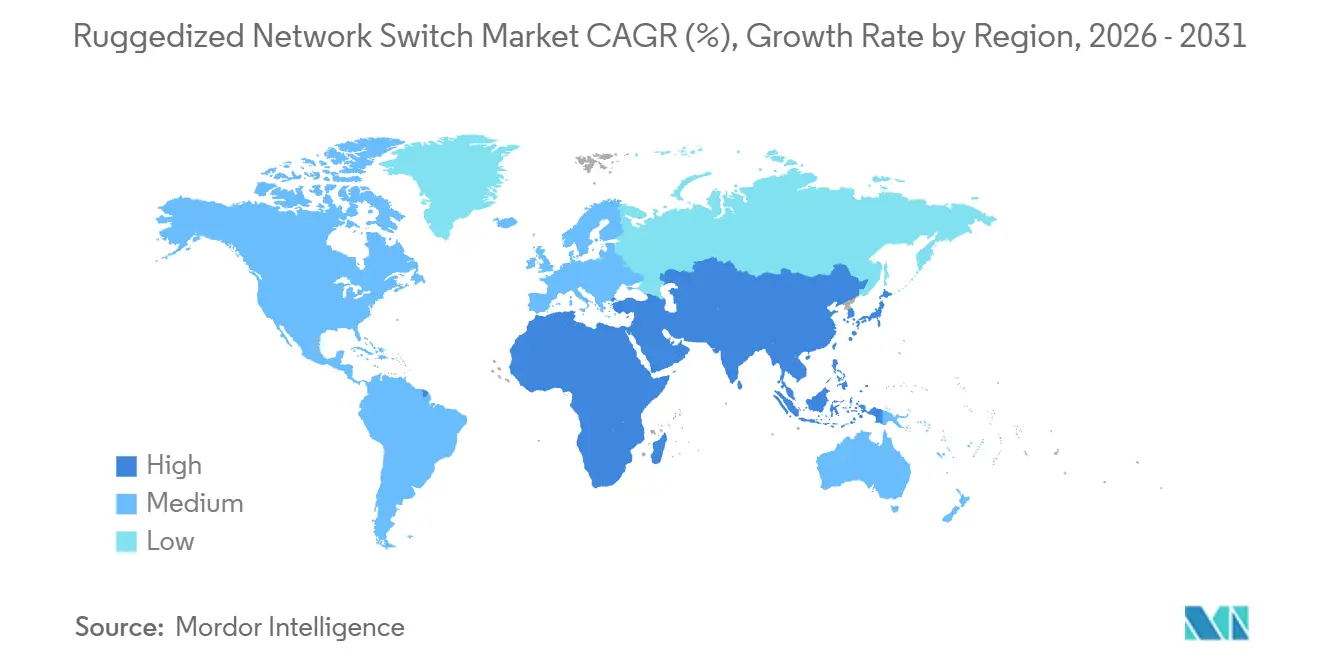

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ruggedized Network Switch Market Analysis by Mordor Intelligence

The ruggedized network switch market size is projected to expand from USD 2.64 billion in 2025 and USD 2.98 billion in 2026 to USD 5.71 billion by 2031, registering a CAGR of 13.87% between 2026 and 2031. Heightened deployment of the industrial Internet of Things in harsh locations, defense programs that push tactical edge computing, and rapid rail expansion across Asia-Pacific and the Middle East are the pivotal factors behind this robust trajectory. Adoption of Time-Sensitive Networking (TSN) in automotive and process automation, cybersecurity mandates such as IEC 62443-4-2, and the emergence of 25 Gbps and 40 Gbps port speeds are strengthening the technology roadmap. Investment momentum is further reinforced by grid-modernization awards in the United States, the European Union’s 5G corridor directive, and autonomous mining initiatives in Australia and Chile. Although rising component lead-times and the capital premium of ruggedized equipment pose near-term challenges, total cost-of-ownership benefits over 10-year life cycles and widening regulatory backing counterbalance these headwinds.

Key Report Takeaways

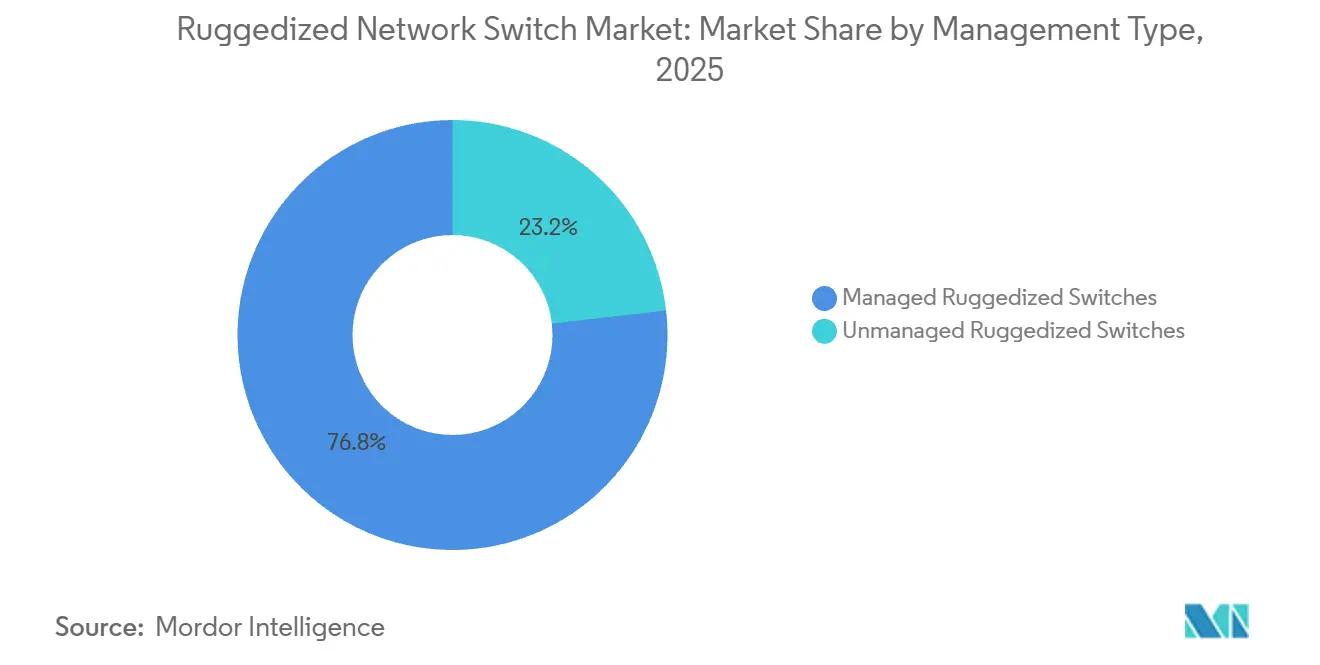

- By management type, managed architectures held 76.82% revenue share in 2025 and are advancing at a 14.22% CAGR through 2031.

- By port speed, 1 GbE and below held 47.36% revenue share in 2025, and the 25 Gbps and 40 Gbps tier is the fastest growing, expanding at an 18.73% CAGR during 2026-2031.

- By enterprise size, large enterprises accounted for 68.55% of revenue in 2025, yet small and medium enterprises are advancing at a 16.88% CAGR through 2031.

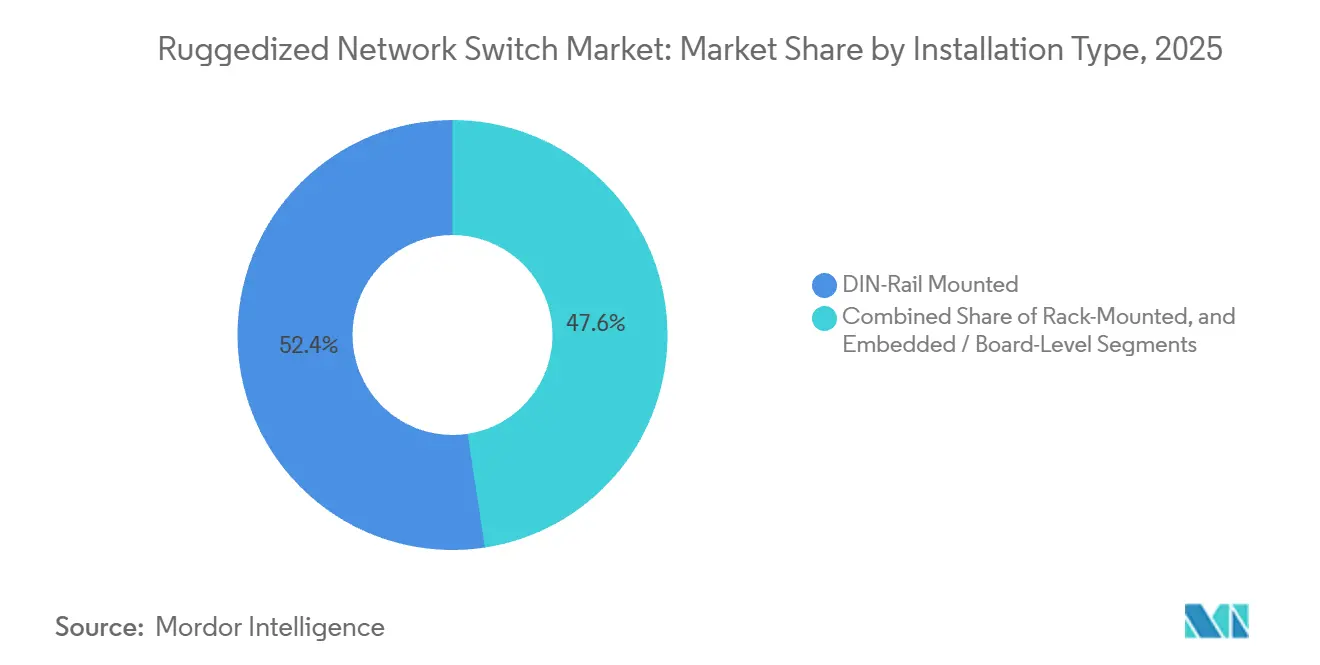

- By installation type, DIN-Rail Mounted held 52.41% revenue share of the ruggedized network switch market in 2025, yet the embedded installation type is advancing at a 16.88% CAGR through 2031.

- By end-user industry, transportation commanded the highest growth outlook, with a 15.91% CAGR to 2031, while industrial applications retained 30.58% of the ruggedized network switch market's 2025 demand.

- By geography, North America led with 35.92% revenue share in 2025, yet Asia-Pacific is on course to post a 16.18% CAGR and overtake in incremental value by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ruggedized Network Switch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of Time-Sensitive Networking Standards | 3.20% | Global, strongest in Germany, Japan, United States | Medium term (2-4 years) |

| Expansion of Rail Transit Infrastructure Worldwide | 2.90% | Asia-Pacific core, Middle East, Europe | Long term (≥ 4 years) |

| Rising Defense Modernization Budgets | 2.40% | North America, Europe, Middle East, Asia-Pacific | Medium term (2-4 years) |

| Growing Demand for Edge Computing at the Rugged Edge | 2.10% | Global mining, offshore oil and gas | Short term (≤ 2 years) |

| Increasing Adoption of Industrial IoT in Harsh Environments | 1.80% | North America and Europe manufacturing, Asia-Pacific energy | Short term (≤ 2 years) |

| Emergence of 5G-Enabled Rugged Edge Devices | 1.50% | Asia-Pacific, Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration of Time-Sensitive Networking Standards

TSN protocols, notably IEEE 802.1AS for time synchronization and 802.1Qbv for traffic scheduling, enable deterministic Ethernet that replaces proprietary fieldbus systems in factory automation. Siemens introduced TSN-enabled SCALANCE XM-400 switches that deliver sub-1 µs jitter, unlocking precision motion control on automotive assembly lines.[1]Siemens AG, “SCALANCE XM-400 Industrial Ethernet Switches,” Siemens.com The unified IEC/IEEE 60802 profile published in 2024 guarantees multi-vendor interoperability, lowering integration risk for plant operators IEC.CH. Moxa’s EDS-4000 series couples TSN with IEC 62443-4-2 security to meet dual determinism and cyber-resilience requirements in critical infrastructure. In-vehicle Ethernet adoption for battery management and advanced driver-assistance systems extends TSN demand into the transportation backbone.

Expansion of Rail Transit Infrastructure Worldwide

China already operates 46,000 km of high-speed rail and targets 70,000 km by 2035, each trainset requiring EN 50155-graded switches for passenger information, signaling, and diagnostics. India has 945 km of metro lines in service and more than 1,200 km under construction, including Delhi Metro Phase IV valued at INR 600 billion (USD 7.2 billion).[2]Delhi Metro Rail Corporation, “Phase IV Expansion Projects,” Delhimetrorail.com Indonesia’s Jakarta-Bandung route, operational since 2023, is spurring parallel projects across Southeast Asia. Mature markets are also refreshing installed bases; Scotland’s 2026 audit listed 1,017 ruggedized IP switches due for end-of-life replacement. Middle-East megaprojects such as Riyadh Metro and Turkey’s Bosphorus tunnel specify fanless, desert-rated switches to ensure reliability under extreme heat.

Rising Defense Modernization Budgets

The United States has earmarked USD 143.2 billion for RDTandE in fiscal 2026, with USD 28.9 billion funneled to cyberspace and space systems that rely on tactical edge networks. DISA’s Joint Regional Security Stacks specify MIL-STD-810H-qualified switches that withstand contested electromagnetic environments. NATO members pledging 2% of GDP to defense spending are modernizing forward bases with ruggedized IP backbones. Australia’s AUD 368 billion (USD 245 billion) AUKUS submarine program and South Korea’s KF-21 fighter line include Ethernet backbones for sensor fusion and mission systems. Certification alignment with STANAG and MIL-STD standards places additional emphasis on suppliers with established defense pedigrees.

Growing Demand for Edge Computing at the Rugged Edge

Latency-intensive analytics are moving to field locations to avoid the millisecond penalties of back-and-forth cloud hops. Fortescue’s autonomous haulage in the Pilbara processes lidar and camera feeds locally, trimming round-trip latency from 200 ms to under 10 ms. The U.S. Department of Energy awarded USD 3.46 billion for grid-resilience upgrades that embed IEC 61850-3-classified switches in substations. Dominion Energy’s USD 9.8 billion grid plan spans 12,000 substations that require environmental-hardened switches for distributed energy resource integration. Automated ports in Los Angeles and Melbourne use edge compute for crane collision avoidance, with hardware hardened for salt fog and vibration. Collectively, these deployments demonstrate the value proposition for high-bandwidth port speeds at the harsh edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure | –2.1% | Global small and medium enterprises | Short term (≤ 2 years) |

| Complex Certification and Compliance Requirements | –1.6% | Europe, North America, maritime, oil and gas | Medium term (2-4 years) |

| Supply Chain Vulnerabilities for Hardened Components | –1.3% | Asia-Pacific semiconductor hubs, U.S. defense | Short term (≤ 2 years) |

| Thermal Management Challenges in Compact Designs | –0.9% | Middle East desert, Arctic offshore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure

Price premiums ranging from 300% to 500% over commercial Ethernet hardware discourage cash-constrained operators, even though failure rates and maintenance spending favor ruggedized equipment over a decade. Municipalities frequently defer switch upgrades despite the verified cyber threats flagged in Scotland’s 2026 asset review. Small manufacturers often prolong legacy gear through patchwork firmware lifts rather than full refreshes, widening the cyber-exposure window. Although leasing models and subscription purchasing reduce initial outlay, their adoption outside large enterprises remains early stage. Bridging this funding gap is essential for broad-based market acceleration.

Complex Certification and Compliance Requirements

Endurance tests outlined in MIL-STD-810H and ATEX Zone 2 lengthen time-to-market by up to 24 months and add USD 0.5-2 million in non-recurring engineering costs. DNV-GL maritime approval requires rigorous vibration and salt-fog testing, with reinspection required after every hardware change.[3]DNV GL, “Maritime Type Approval and Certification,” Dnv.com EN 50155 for rail, UL 61010-2-201 for North America, and overlapping CE and CCC markings further balkanize requirements, compelling vendors to carry multiple product variants. The resulting complexity reduces economies of scale, inflates inventory, and discourages smaller entrants from expanding globally.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Management Type: Cybersecurity Mandates Favor Managed Architectures

The managed tier seized 76.82% of 2025 revenue as operators adopted IEC 62443-4-2 security baselines, VLAN segmentation, and role-based authentication. This dominance continues, with a 14.22% CAGR that lifts the segment’s ruggedized network switch market size throughout the forecast. Managed switches also anchor Time-Sensitive Networking rollouts, because 802.1Qbv and 802.1AS require centralized scheduling and clock distribution. Unmanaged models still serve isolated conveyor systems and brownfield sites, but the risk calculus is tilting firmly toward managed infrastructure. Vendors have responded with zero-touch provisioning and cloud dashboards that lower the skills barrier for smaller plants, helping managed penetration deepen across emerging economies.

Unmanaged devices retain tactical relevance where deterministic traffic, air-gapped architectures, or budget ceilings prevail. However, ransomware campaigns targeting industrial control systems and regulatory scrutiny under the European Union’s Network and Information Security Directive 2 are pushing operators toward visibility and control. As managed functionality becomes table stakes, price erosion is narrowing the premium, further swinging preference in its favor.

By Port Speed: Multi-Gigabit Uplinks Drive Edge Aggregation

Ports of 1 Gbps and below accounted for 47.36% of the installed base in 2025, but the 25 Gbps and 40 Gbps classes are expanding fastest at 18.73% through 2031 as edge modules process video analytics, digital-twin telemetry, and lidar streams. This speed tier accounts for the highest incremental ruggedized network switch market share gain in the period. Autonomous mining trucks generate several terabits daily, necessitating 25 Gbps uplinks between pit switches and surface hubs. The intermediate 2.5 Gbps and 5 Gbps lanes provide cost-effective upgrades over existing Cat5e cabling, bridging the gap without immediate fiber investment.

Ten-gigabit uplinks remain the workhorse for metro-rail Wi-Fi and smart-grid substations, balancing bandwidth with manageable thermal envelopes in fanless casings. Higher brackets, such as 100 Gbps and 400 Gbps, are technically feasible but hampered by heat dissipation and the scarcity of wide-temperature optics. Research into heat-pipe substrates and nano-porous coatings aims to ease these constraints, paving the way for the gradual introduction in offshore wind control rooms and forward command posts.

By Enterprise Size: Large Enterprises Dominate, SMEs Seek Modular Solutions

Large enterprises held the largest revenue share of 71.28% in 2025. Large organizations leverage volume contracts and vendor-managed inventory to standardize ruggedized switch fleets across thousands of nodes, consolidating the bulk of market value. They frequently bundle lifecycle services, spares, firmware governance, and field support into capital plans. Small and medium enterprises are advancing at a 15.63% CAGR through 2031; however, they face sticker shock and integration complexity that slow uptake. To close this gap, suppliers are rolling out modular chassis with field-swappable SFPs and power supplies, allowing SMEs to scale incrementally and align cash flow with production cycles.

Cloud-based orchestration further democratizes adoption by automating firmware pushes and topology discovery, easing the burden on plants without dedicated network teams. Leasing agreements and outcome-based pricing also lower entry barriers. Subsidy programs embedded in the European Union’s Digital Decade plan and several U.S. state-level modernization grants are catalyzing SME investment in sectors such as food processing and regional logistics hubs.

By Installation Type: DIN-Rail Dominates Industrial Automation

The DIN-rail mounted format held the largest share of 52.41% share in 2025, underpinning industrial control cabinets, rolling-stock equipment bays, and field enclosures, making it the most prevalent installation type. Quick clip-on assembly, compact depth, and front-access cabling enable rapid swap-outs that minimize line stoppage. Rack-mounted 19-inch units address data-center-like environments, including mining control rooms and substation master racks, where structured cabling and airflow management are available.

Embedded or board-level switches witnessed the highest CAGR of 16.88% during 2026 and 2031, satisfying UAVs, remotely operated vehicles, and compact signaling gear, where weight and volume ceilings preclude an external chassis. Vendors now design common ASIC and PCB platforms that adapt to multiple form factors, streamlining certification and material procurement. For operators, a unified hardware pedigree simplifies spares pools, staff training, and firmware commonality across an estate that might span pits, plants, rolling stock, and roadside cabinets.

By End-User Industry: Transportation Overtakes Industrial Growth

Industrial sites accounted for 30.58% of 2025 spending, but transportation will register the swiftest CAGR of 15.91% to 2031 as intelligent transportation systems (ITS), connected rail, and automated ports scale aggressively. The ITS surge is anchored by standards such as ITU-T Y.4232 that codify roadside perception architectures, driving demand for EN 50155-certified switches in roadside cabinets. Rail modernization programs, both high-speed intercity and urban metro, impose stringent shock, vibration, and temperature envelopes, fueling high-volume refreshes of legacy serial backbones.

Defense, oil and gas, and mining remain resilient verticals, distinguished by mandatory MIL-STD-810H, ATEX, and IEC 61850-3 stamps that ban commodity hardware. Offshore wind is another emerging pocket where DNV-GL-approved switches installed in nacelles and tower bases must resist salt-fog, humidity, and extreme cold. Water utilities and smart buildings make up a long tail of applications, collectively representing stable, if fragmented, incremental volumes.

Geography Analysis

North America generated 35.92% of 2025 revenue due to the United States’ USD 3.46 billion Grid Resilience program and Dominion Energy’s USD 9.8 billion grid plan that rolled out thousands of IEC 61850-3 substations. Federal Highway Administration guidance issued in 2026 extends ruggedized equipment into temporary work-zone ITS, broadening addressable volume.[4]Federal Highway Administration, “Work Zone Intelligent Transportation Systems Guidance,” Fhwa.dot.gov Defense spending tied to the Joint Cyber Warfighting Architecture continues to favor locally sourced, MIL-STD-qualified vendors.

Asia-Pacific is the fastest growing, recording a 16.18% CAGR that builds on China’s 70,000 km high-speed rail goal, India’s metro pipeline, and Australia’s automation-heavy mining sector. Japan and South Korea advance TSN-infused automotive lines and defense initiatives, while Indonesia’s Jakarta-Bandung opening has nudged Thailand and Malaysia to progress their own corridors. Private 5G trials in ports across Singapore, Busan, and Ningbo require TSN-capable switches that interwork with RedCap radios.

Europe combines mature industrial estates with policy-driven digital infrastructure. The European Union’s January 2026 delegated act mandates 5G underlay along Trans-European Transport Network corridors by 2030, accelerating roadside unit rollouts. Germany’s automotive OEMs, Spain’s metro clusters, Poland’s freight-rail upgrades, and North Sea offshore wind farms all contribute diversified demand. Supply-chain sovereignty concerns are spurring localized production, such as ECRIN Systems’ France-built Quartz switch. The Middle East pushes ruggedized switching into harsh desert metros and Gulf port expansions, while Latin America’s mining and near-shoring factories provide steady, if smaller, opportunities. Africa remains nascent but shows traction in South African port automation and Nigerian free-trade-zone logistics.

Competitive Landscape

The market structure is moderately concentrated, with established leaders such as Moxa, Siemens, and Belden anchoring the top tier through decades of incumbency across rail, energy, and defense sectors. These players benefit from long-standing customer relationships, proven reliability in mission-critical environments, and strong certification portfolios. At the same time, niche vendors like Antaira and EtherWAN carve out competitive positions by offering highly specialized solutions, particularly DIN-rail and board-level designs tailored for compact, space-constrained industrial panels. Across the market, key innovation themes center on Time-Sensitive Networking (TSN) integration, emerging 5G RedCap backhaul use cases, and the adoption of zero-trust security overlays.

Recent developments highlight a shift in both technology and supply chain strategies. The launch of Quartz by ECRIN Systems in January 2026 reflects a broader reshoring trend, where companies aim to localize manufacturing to enhance resilience and reduce geopolitical risk. Concurrently, patent activity indicates a growing focus on advanced thermal management technologies such as heat-pipe designs and nano-porous substrates, which enable higher port density without relying on active cooling. Participation in standards committees is also becoming a strategic advantage, allowing vendors early visibility into evolving protocols and giving them a head start in aligning product roadmaps.

At the same time, the competitive landscape is being reshaped by the rise of software-defined networking approaches. Startups offering software-defined overlays are gaining traction among operators seeking centralized control and policy-driven network management, as opposed to traditional VLAN-based configurations. This shift reflects a broader industry movement toward abstraction and automation, which could challenge hardware-centric incumbents over time. As a result, vendors that successfully integrate software capabilities with their hardware offerings are likely to be better positioned in the evolving market.

Ruggedized Network Switch Industry Leaders

Moxa Inc.

Antaira Technologies, LLC

Westermo Network Technologies AB

Belden Inc.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ECRIN Systems released the Quartz TSN-ready, IEC 62443-4-2-certified switch, assembled in France to meet European content mandates.

- January 2026: The European Union issued a delegated act requiring 5G coverage along TEN-T corridors by 2030, catalyzing demand for ruggedized switches for roadside backhaul.

- November 2025: Advantech launched MIC-3850: a robust, certified Ethernet switch card with unmatched port density for railway and industrial systems.

- November 2025: HMS Networks launched new N-Tron NT110-FX2, NT111-FX3, and NT112-FX4 unmanaged Ethernet switches built for harsh industrial environments.

Global Ruggedized Network Switch Market Report Scope

The Ruggedized Network Switch Market includes industrial Ethernet switching devices designed for reliable operation in extreme environmental conditions, supporting mission-critical connectivity across sectors such as industrial automation, transportation, utilities, and defense. These switches ensure deterministic, high-availability communication for industrial and outdoor applications.

The Ruggedized Network Switch Market Report is Segmented by Management Type (Managed Ruggedized Switches, and Unmanaged Ruggedized Switches), Port Speed (1 GbE and Below, 2.5/5 GbE, 10 GbE, 25/40 GbE, 100 GbE, and 400 GbE and Above), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Installation Type (DIN-Rail Mounted, Rack-Mounted, Embedded / Board Level), End-User Industry (Industrial, Transportation, Military and Defense, Oil and Gas, Mining and Metals, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Managed Ruggedized Switches |

| Unmanaged Ruggedized Switches |

| 1 GbE and Below |

| 2.5/5 GbE Multi-Gig |

| 10 GbE |

| 25/40 GbE |

| 100 GbE |

| 400 GbE and Above |

| Small and Medium Enterprises |

| Large Enterprises |

| DIN-Rail Mounted |

| Rack-Mounted |

| Embedded / Board-Level |

| Industrial |

| Transportation |

| Military and Defense |

| Oil and Gas |

| Mining and Metals |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Management Type | Managed Ruggedized Switches | |

| Unmanaged Ruggedized Switches | ||

| By Port Speed | 1 GbE and Below | |

| 2.5/5 GbE Multi-Gig | ||

| 10 GbE | ||

| 25/40 GbE | ||

| 100 GbE | ||

| 400 GbE and Above | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Installation Type | DIN-Rail Mounted | |

| Rack-Mounted | ||

| Embedded / Board-Level | ||

| By End-User Industry | Industrial | |

| Transportation | ||

| Military and Defense | ||

| Oil and Gas | ||

| Mining and Metals | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the ruggedized network switch market be by 2031?

Mordor Intelligence projects the ruggedized network switch market size to reach USD 5.71 billion by 2031, expanding at a 13.87% CAGR from 2026.

Which management type is leading sales?

Managed architectures contributed 76.82% revenue in 2025 and hold the dominant ruggedized network switch market share through 2031 due to cybersecurity mandates such as IEC 62443-4-2.

What port speed shows the fastest growth?

The 25 Gbps and 40 Gbps class records the quickest expansion at an 18.73% CAGR because edge micro-data-centers aggregate video and sensor data at higher bandwidths.

Which end-user vertical is growing most rapidly?

Transportation exhibits the fastest growth, advancing at a 15.91% CAGR as intelligent transportation systems, rail modernization, and automated ports require EN 50155-compliant switching.

Why is Asia-Pacific the fastest expanding region?

Asia-Pacific posts a 16.18% CAGR thanks to China’s 70,000 km high-speed rail target, India’s metro build-out, and large-scale mining automation in Australia.

Page last updated on: