Sri Lanka Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

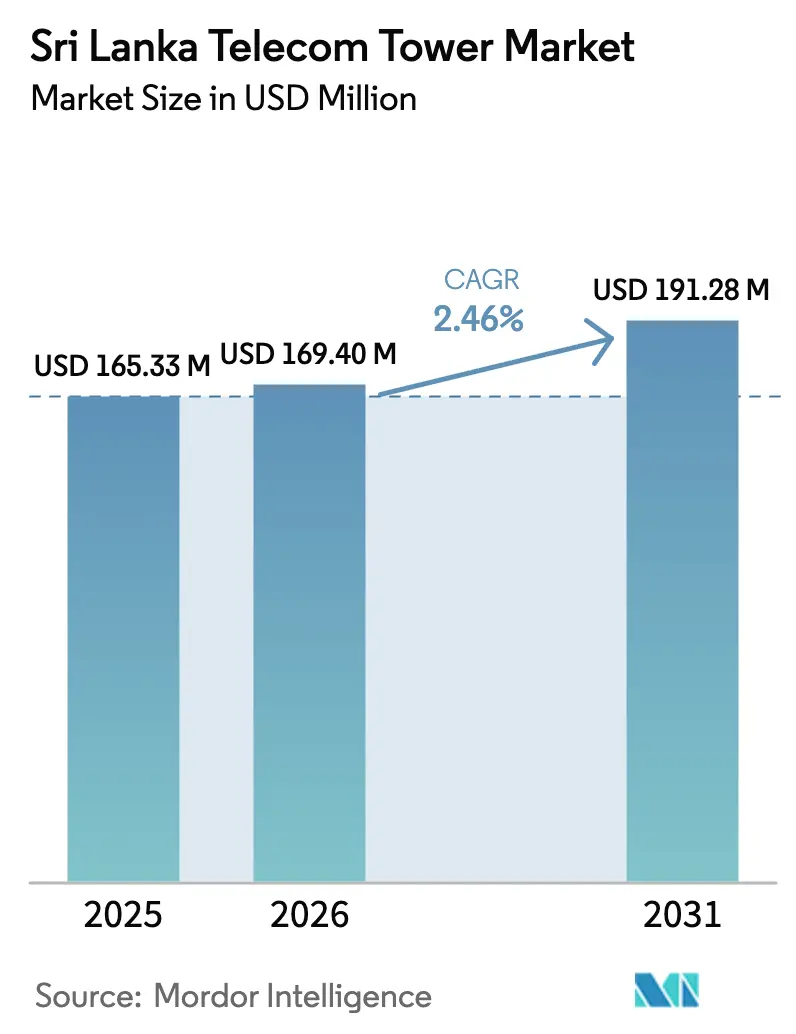

| Base Year Market Size (2025) | USD 165.33 Million |

| Market Size (2026) | USD 169.4 Million |

| Market Size (2031) | USD 191.28 Million |

| Growth Rate (2026 - 2031) | 2.46% CAGR |

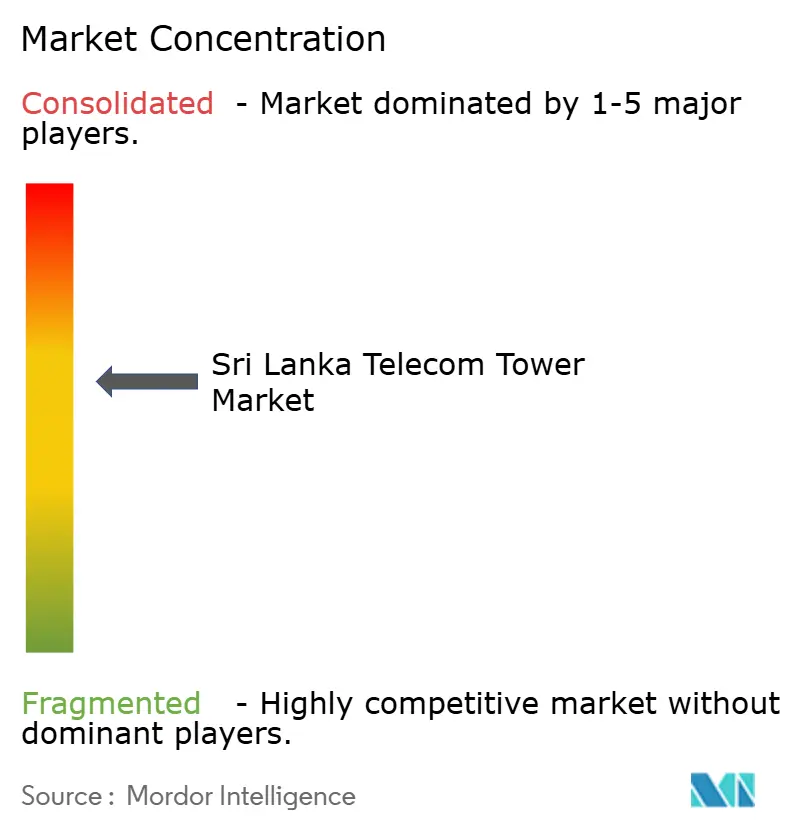

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sri Lanka Telecom Tower Market Analysis by Mordor Intelligence

The Sri Lanka Telecom Tower Market size is expected to grow from USD 165.33 million in 2025 to USD 169.4 million in 2026 and is forecast to reach USD 191.28 million by 2031 at 2.46% CAGR over 2026-2031.

Infrastructure revenue now comes mainly from densification rather than green-field builds as operators fill coverage gaps in suburban and rural zones. Regulatory reform that, for the first time in 28 years, permits third-party tower companies signals an enduring shift toward infrastructure-sharing business models and asset-light balance sheets. Energy-cost volatility is prompting power-system diversification, while renewed spectrum planning for 5G drives site-upgrade activity. Competitive tension remains high despite a shrinking operator count because independent tower companies are scaling faster than operator-owned portfolios. These factors collectively frame a measured yet structurally important growth trajectory for the Sri Lanka telecom tower market.

Key Report Takeaways

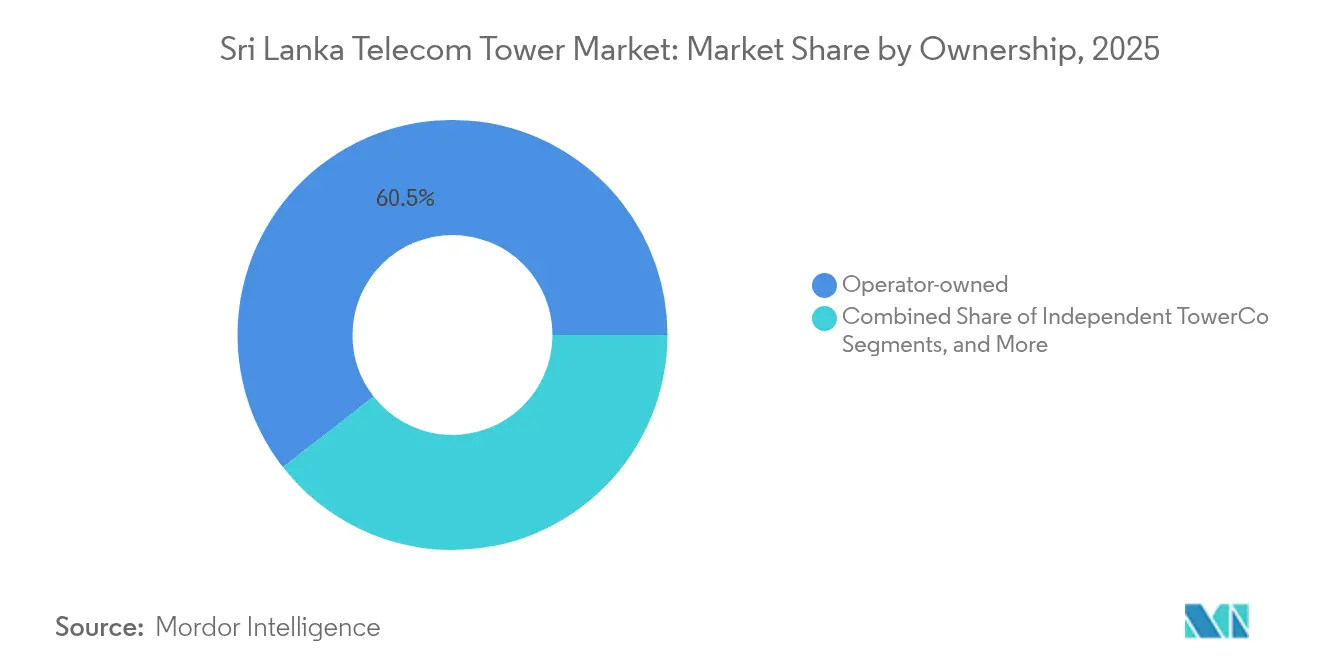

- By ownership, operator-owned structures held 60.55% of the Sri Lanka telecom tower market share in 2025, whereas independent tower companies are expanding at a 22.53% CAGR to 2031.

- By installation type, ground-based towers accounted for 79.90% of the Sri Lanka telecom tower market size in 2025, while rooftop sites are forecast to post the fastest 9.86% CAGR through 2031.

- By fuel type, grid/diesel hybrids commanded 71.10% of the Sri Lanka telecom tower market size in 2025, and renewable-powered sites are projected to advance at a 10.35% CAGR to 2031.

- By tower type, monopoles led with a 45.05% share in 2025; stealth or concealed designs are set to deliver the highest 9.92% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sri Lanka Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 4G densification and planned 5G NSA rollouts | +0.8% | Colombo, Kandy, Galle corridors | Medium term (2-4 years) |

| Government Digital Economy Masterplan 2024 (100% 4G by 2026) | +0.6% | National, prioritizing rural zones | Short term (≤2 years) |

| Surging mobile data consumption per user | +0.4% | Urban and peri-urban clusters | Long term (≥4 years) |

| Infrastructure-sharing incentives and tax holidays | +0.3% | Nationwide | Medium term (2-4 years) |

| Rural fiber backhaul gaps spurring microwave towers | +0.2% | Northern and Eastern provinces | Medium term (2-4 years) |

| Colombo Port City smart-district small-cell demand | +0.1% | Colombo metro | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

4G densification and planned 5G NSA rollouts

Operators have finished pilot 5G trials that clocked peak speeds above 2 Gbps; commercial launches now hinge on tower-level fiber upgrades from 300 Mbps to multi-gigabit capacity. Massive-MIMO radios already installed on one-fifth of macro sites are firmware-ready for 5G, limiting new-tower counts while amplifying modification workloads. Rural districts lag in 4G experience, so microwave-linked towers are in demand where fiber economics falter. The push toward nationwide 4G coverage by 2026 compresses build calendars, favoring independent tower companies able to execute faster site turns. These combined needs elevate the Sri Lanka telecom tower market as tower swaps, power-system upgrades, and new rooftop infills all feed incremental revenue [1]Dialog Axiata PLC, “Dialog Axiata Rebounds in Q3 2024,” dialog.lk.

Government Digital Economy Masterplan 2024 (100% 4G by 2026)

The master plan obliges operators to cover every populated Grama Niladhari division within 18 months, catalyzing 276 new tower builds partly funded by public capital expenditure. Fiscal constraints mean public funds alone are insufficient, so the new third-party-tower framework channels private investment into rural coverage. Tax holidays of up to five years for towers commissioned in underserved regions improve return on invested capital under low-tenancy scenarios. Infrastructure sharing clauses make a tenancy ratio of 1.8x the basic compliance threshold, ensuring sustainable economics for tower companies in low-ARPU zones. Resultant rural builds broaden the Sri Lanka telecom tower market footprint while narrowing the digital divide [2]TRC Sri Lanka, “Guidelines on Infrastructure Sharing,” trc.gov.lk .

Surging mobile data consumption per user

Average data use crossed 17 GB per subscriber per month in 2025, more than doubling since 2023 as video streaming, gaming, and hybrid-work traffic surged. Fixed-broadband uptake remains below 10%, so cellular networks shoulder primary internet loads, intensifying congestion in Western and Central provinces. Operators must add sectors and small cells to raise spectral efficiency, which pushes demand for lightweight rooftop poles and street-level micro-sites. Capacity upgrades also require higher backhaul throughput that older microwave hops cannot provide, nudging the market toward fiberized high-bandwidth towers. Data-driven tower demand will therefore underpin steady tenancy growth across the Sri Lanka telecom tower market.

Infrastructure-sharing incentives and tax holidays

A 50% import-duty waiver for shared passive gear such as power systems, shelters, and mounts, combined with corporate-tax relief for the first five years of operation, materially improves project net present value. EDOTCO Services Lanka, with a 2.34x tenancy ratio, illustrates the economics of higher sharing: EBITDA per tower is 38% above the operator-owned average. The amended Telecommunications Regulatory Commission Act now obliges licensees to justify any refusal to co-locate, removing a historic barrier to multi-tenant expansion. As more portfolios migrate from single-operator control to tower-company ownership, improved utilization will stabilize lease rentals and increase the investible scale of the Sri Lanka telecom tower market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Forex shortage and steel / RF-equipment import delays | -0.7% | Nationwide | Short term (≤2 years) |

| Sovereign credit risk pushing up cost of capital | -0.5% | Nationwide | Medium term (2-4 years) |

| Community EMF concerns delaying permits | -0.3% | Dense urban zones | Long term (≥4 years) |

| Diesel-genset opex spikes after subsidy removal | -0.2% | Rural off-grid sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Forex shortage and steel / RF-equipment import delays

A chronic dollar deficit has forced banks to ration letters of credit, elongating lead times for imported steel and antennas. Project cycles that once took 90 days now stretch to 150 days, locking up developer capital and delaying revenue recognition. Local fabrication is limited to light-duty lattice segments that cannot substitute for high-spec monopoles, so tower builders must absorb spot-priced steel costs or postpone projects. Import bottlenecks likewise affect 5G-ready radios, slowing the network-upgrade wave that would otherwise grow tenancies. The resulting friction lowers near-term growth in the Sri Lanka telecom tower market until forex liquidity normalizes [3]Ceylon Electricity Board, “Annual Report 2024,” ceb.gov.lk .

Sovereign credit risk pushing up cost of capital

Sri Lanka’s country-risk premium widened to 750 basis points over the US Treasuries in late 2024, nudging local lending rates to 18% for infrastructure borrowers. High carrying costs make it harder for tower companies to hit internal hurdle rates, especially in rural builds with lower ARPU density. International tower-co entrants demand dollar-linked leases, but operators balk at the pass-through risk, leading to prolonged contract negotiations. Elevated borrowing costs also impact refinance schedules for legacy portfolios, squeezing free cash flow and limiting discretionary capex. Consequently, investment pacing in the Sri Lanka telecom tower market remains closely tied to sovereign-risk sentiment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Operator Control Drives Market Structure

Operator-owned towers commanded 60.55% of the Sri Lanka telecom tower market in 2025, underscoring the legacy strategy of retaining passive assets within the network core. Independent tower companies, though still a minority, are recording a 22.53% CAGR and are forecast to represent the largest incremental addition to the Sri Lanka telecom tower market size over 2026-2031. Dialog Axiata’s post-merger rationalization of overlapping Airtel sites yields both decommissioning savings and tenancy creation as spare load-bearing capacity becomes leasable.

A parallel monetization wave is emerging as SLT-Mobitel and Hutch weigh carve-outs to raise cash for 5G spectrum outlays. Portfolio hand-offs to tower-cos typically lift tenancy ratios by 30-40 basis points within two years, translating into better capital efficiency for operators and higher EBITDA multiples for tower-service providers. The ownership mix is therefore expected to tilt steadily toward independent structures, reinforcing specialization trends that define the mature tiers of the global telecom-tower sector.

By Installation: Ground-Based Dominance with Rooftop Growth

Ground-based sites generated 79.90% of 2025 service revenue, a figure that will inch downward as rooftop builds capture dense-urban traffic. Rooftops are on track for a 9.86% CAGR, reflecting both the scarcity of green-field land parcels in Colombo and the radio-frequency advantages of closer proximity to users. A new municipal guideline capping macro-tower height at 30 meters inside administrative Colombo has further accelerated the rooftop shift.

Rooftop leases average 15-20% below stand-alone site rentals, yet yield comparable returns due to lower capex and faster commissioning. Building-owner agreements typically lock in 10-year terms with annual escalators, offering stable cost visibility for operators. The trend adds structural diversity to the Sri Lanka telecom tower market and invites niche providers that specialize in building-integrated antenna systems.

By Fuel Type: Grid Hybrid Systems Face Renewable Transition

Grid/diesel hybrids made up 71.10% of the Sri Lanka telecom tower market size in 2025; ongoing diesel-subsidy withdrawals and fuel-tax hikes raise operating expenditure for these setups by 18% year-on-year. Solar-battery hybrids combined with lithium-ion storage now clear the five-year payback hurdle at diesel prices above LKR 325 per liter, catalyzing a 10.35% CAGR in renewable-powered sites.

Net-metering rules allow tower-cos to export surplus solar power to the grid, adding auxiliary revenue streams that shorten payback further. The Ministry of Power’s target of 70% renewable energy in the national mix by 2030 dovetails with corporate ESG mandates, positioning solarized towers as branding assets beside their cost benefits. As macroeconomic pressure on foreign exchange persists, local-currency solar capex offers a hedge against imported fuel volatility, reinforcing the renewable shift in the Sri Lanka telecom tower market.

By Tower Type: Monopole Leadership with Stealth Innovation

Monopoles led the 2025 revenue table with a 45.05% slice of the Sri Lanka telecom tower market. Their fast erection schedules, compact footprint, and mid-range load capacity suit both rural macros and suburban infills. Looking ahead, the 9.92% CAGR in stealth or concealed structures will be propelled by planning-authority pressure to mitigate visual clutter, especially around heritage zones and high-value real estate.

Stealth designs such as street-lamp integrates, flagpoles, and camouflaged penthouses cost up to 40% more than bare monopoles but deliver win-rate advantages in permit-challenged neighborhoods. The arrival of 3.5 GHz 5G spectrum, which demands shorter inter-site distances, amplifies the need for low-profile structures congruent with urban aesthetics. Innovation in composite materials and modular panels will further cut lead times, reinforcing the stealth segment’s pull on the Sri Lanka telecom tower market.

Geography Analysis

Western Province retained 42.00% of active tenancies in 2025, reflecting Colombo’s concentration of enterprise and residential demand. Within the province, Port City adds a multiyear pipeline of small-cell nodes, distributed antenna systems, and rooftop poles integrated into mixed-use high-rises. Colombo municipal incentives now waive tower-permit fees for concealed installations that meet aesthetic standards, nudging operators toward premium stealth products.

The Northern and Eastern provinces, while generating only 18.00% of 2025 tower revenue, log the fastest tenancy growth because rural coverage duties align with the Digital Economy Masterplan. Microwave backhaul remains the cornerstone technology here as fiber rollout lags due to rocky terrain and security clearances. Independent tower-cos that master solar-powered, low-maintenance site designs stand to win deployment rounds funded by universal-service subsidies.

Central and Southern provinces, driven by tourism and agribusiness, have moved from coverage to capacity upgrades. New expressway corridors have prompted roadside macro-tower clusters where traffic patterns justify three-tenant economics. Collectively, these regions illustrate the balancing act between urban densification and rural inclusion that shapes the Sri Lanka telecom tower market landscape.

Competitive Landscape

Dialog Axiata’s merger with Airtel Lanka cements a 45% revenue share, yet also compels tower-portfolio right-sizing to eradicate overlapping metal. The operator has flagged 450 redundant sites for lease-back or decommissioning, opening tenancy opportunities for EDOTCO and potential new entrants. SLT-Mobitel, the second-largest player, is evaluating a sale-and-lease-back of 1,200 towers to unlock capital for 150 MHz of mid-band 5G spectrum earmarked for 2026 auctions.

EDOTCO Services Lanka runs the largest independent portfolio at 696 sites and a 2.34x tenancy ratio, far above the national average of 1.7x. Its strategy couples proactive co-location marketing with energy-as-a-service packages that guarantee 99.9% uptime. The company’s swap-debt refinancing in 2025 trimmed the weighted average cost of capital by 110 basis points, enhancing bid competitiveness for upcoming universal-service projects.

Potential new tower-co entrants include international specialists American Tower and Helios Towers, both of which have filed expressions of interest with TRCSL for green-field quota allocations. The amended licensing regime mandates compliance with open-access provisions, leveling the playing field for newcomers. Consequently, while the Sri Lanka telecom tower market shows moderate concentration today, structural entry doors are now open and operational excellence will dictate future share shifts.

Sri Lanka Telecom Tower Industry Leaders

EDOTCO Services Lanka (Private) Limited

Dialog Axiata PLC

SLT-Mobitel (Sri Lanka Telecom PLC)

Hutchison Telecommunications Lanka (Pvt) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: SLT-Mobitel concluded 5G-Advanced trials surpassing 5 Gbps peak throughput, validating upcoming site-upgrade requirements.

- August 2024: Starlink Lanka received TRCSL approval to offer satellite broadband services, adding a competitive alternative for rural connectivity.

- June 2024: Dialog Axiata completed its share-swap acquisition of Bharti Airtel Lanka, reducing the operator pool from five to four.

- May 2024: TRCSL amended the Telecommunications Regulatory Commission Act, allowing third-party companies to build and operate towers after 28 years of operator exclusivity.

Sri Lanka Telecom Tower Market Report Scope

The telecommunication market is largely concerned with the operations and provision of infrastructure for transmitting data - voice, image, sound, text, and video. To expand its network and services, the telecommunication market relies on towers, which are used to mount telecommunication networking and power equipment.

The Report Covers Sri Lanka Telecom Tower Companies and the Market is Segmented by Ownership (Operator-Owned, Private-Owned, MNO Captive Sites), by Installation (Rooftop, Ground-Based), by Fuel Type (Renewable, Non-Renewable). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid / Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid / Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the Sri Lanka telecom tower market in 2026?

The market stands at USD 169.4 million in 2026 and is projected to reach USD 191.28 million by 2031.

What is the forecast CAGR for Sri Lanka’s tower sector through 2031?

The market is expected to register a 2.46% CAGR over the 2026-2031 period.

Which ownership model is growing fastest?

Independent tower companies are expanding at a 22.53% CAGR thanks to regulatory liberalization and tax incentives.

How are energy costs affecting tower operations?

Diesel-subsidy removal is inflating hybrid-system opex, accelerating a shift toward solar-battery power solutions.

What impact will 5G have on new tower builds?

5G roll-outs primarily drive site upgrades and densification; new builds will concentrate in urban rooftops and smart-district small cells.

Which province shows the highest near-term tenancy growth?

Northern and Eastern provinces exhibit the fastest tenancy growth due to universal-service builds aimed at closing rural coverage gaps.

Page last updated on: