Bangladesh Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

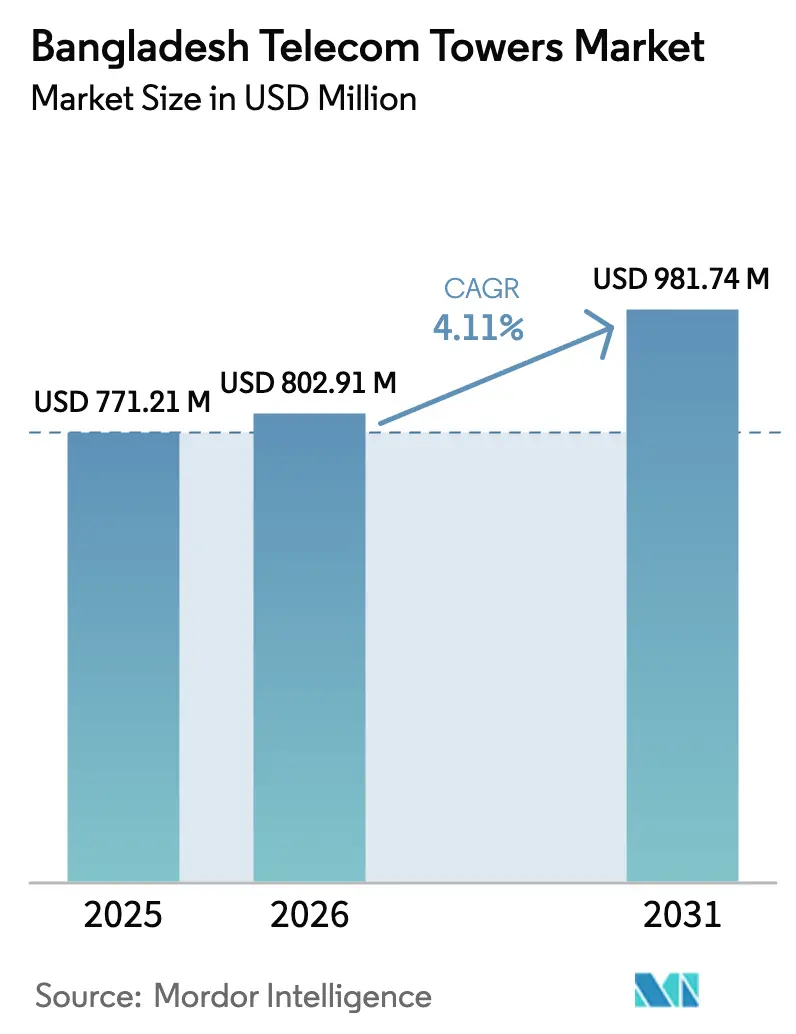

| Base Year Market Size (2025) | USD 771.21 Million |

| Market Size (2026) | USD 802.91 Million |

| Market Size (2031) | USD 981.74 Million |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

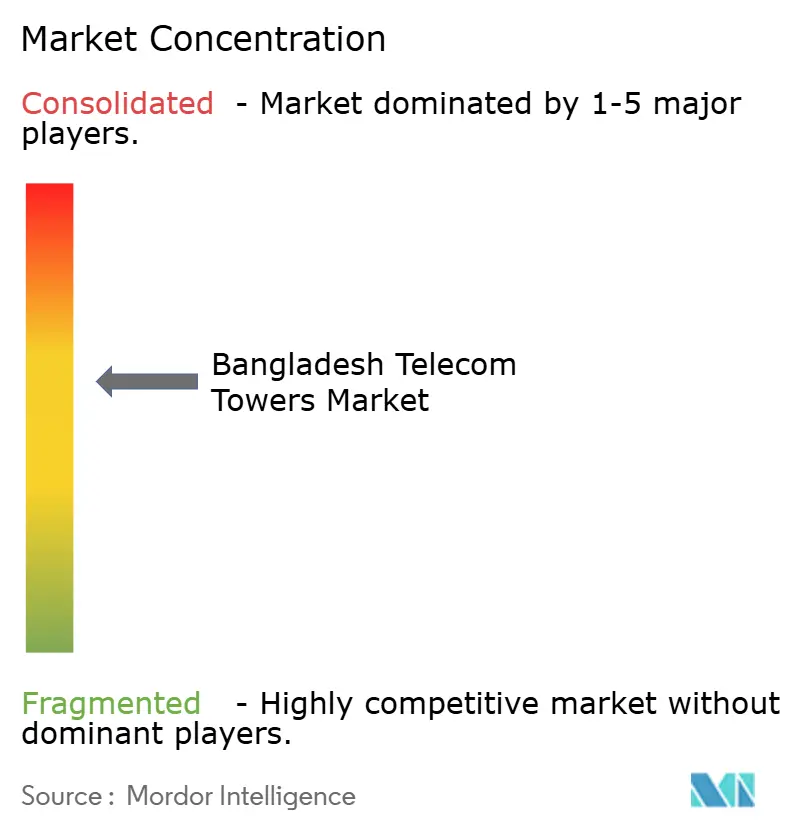

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Telecom Towers Market Analysis by Mordor Intelligence

The Bangladesh Telecom Towers Market size was valued at USD 771.21 million in 2025 and estimated to grow from USD 802.91 million in 2026 to reach USD 981.74 million by 2031, at a CAGR of 4.11% during the forecast period (2026-2031).

This growth comes as operators shift from aggressive build-outs to optimization of existing infrastructure, emphasizing tower sharing, hybrid-power upgrades, and selective densification. Independent TowerCos dominate the Bangladesh telecom tower market, reflecting the success of the asset-light approach favored by mobile network operators (MNOs). Ground-based sites remain the backbone of network coverage, yet rooftop additions, stealth structures, and renewable-powered systems are scaling faster as urban data demand rises and sustainability targets tighten. Spectrum-related cash pressures, Taka depreciation, and intensified climate-resilience standards temper capex, but they also widen the addressable opportunity for specialized TowerCos that can bundle power, maintenance, and fiber backhaul into value-added leasing models. In short, the Bangladesh telecom tower market continues to progress, but the path forward revolves around efficiency, collaboration, and differentiated service offerings.

Key Report Takeaways

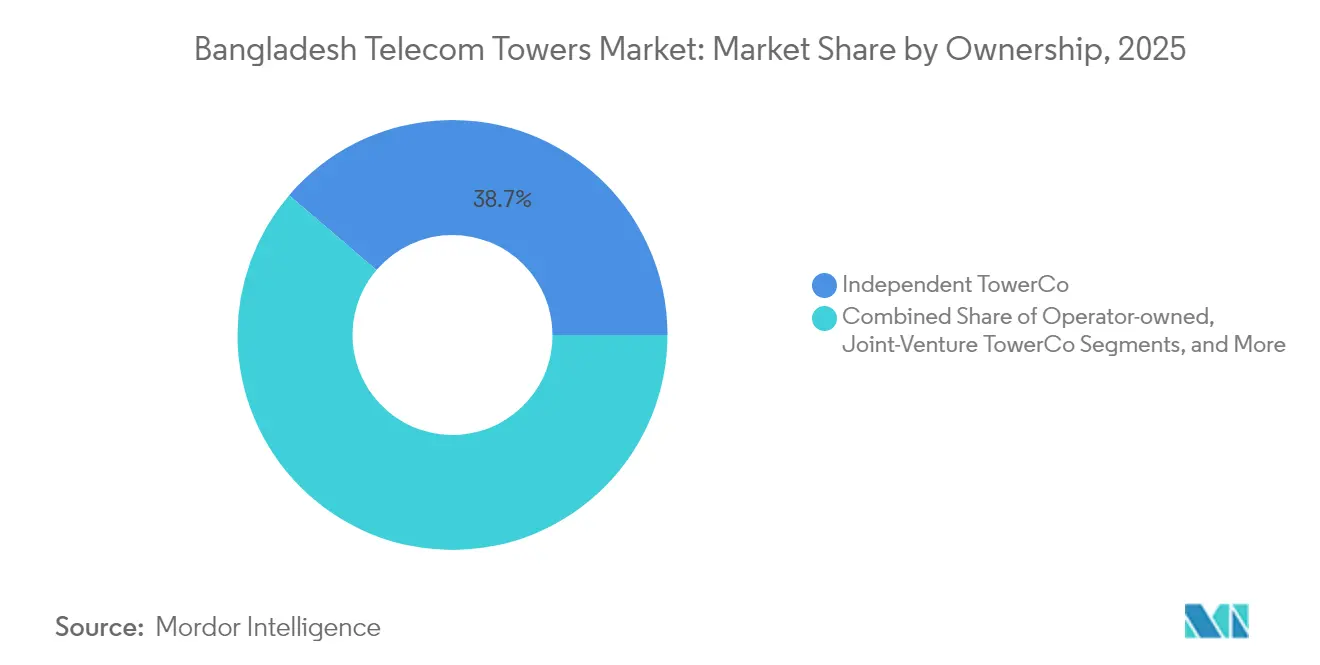

- By ownership, independent TowerCos led with 38.74% revenue share in 2025, while joint-venture TowerCos are projected to expand at a 10.11% CAGR to 2031.

- By installation, ground-based sites captured 73.65% of the Bangladesh telecom tower market share in 2025, whereas rooftop sites are forecast to post a 6.62% CAGR through 2031.

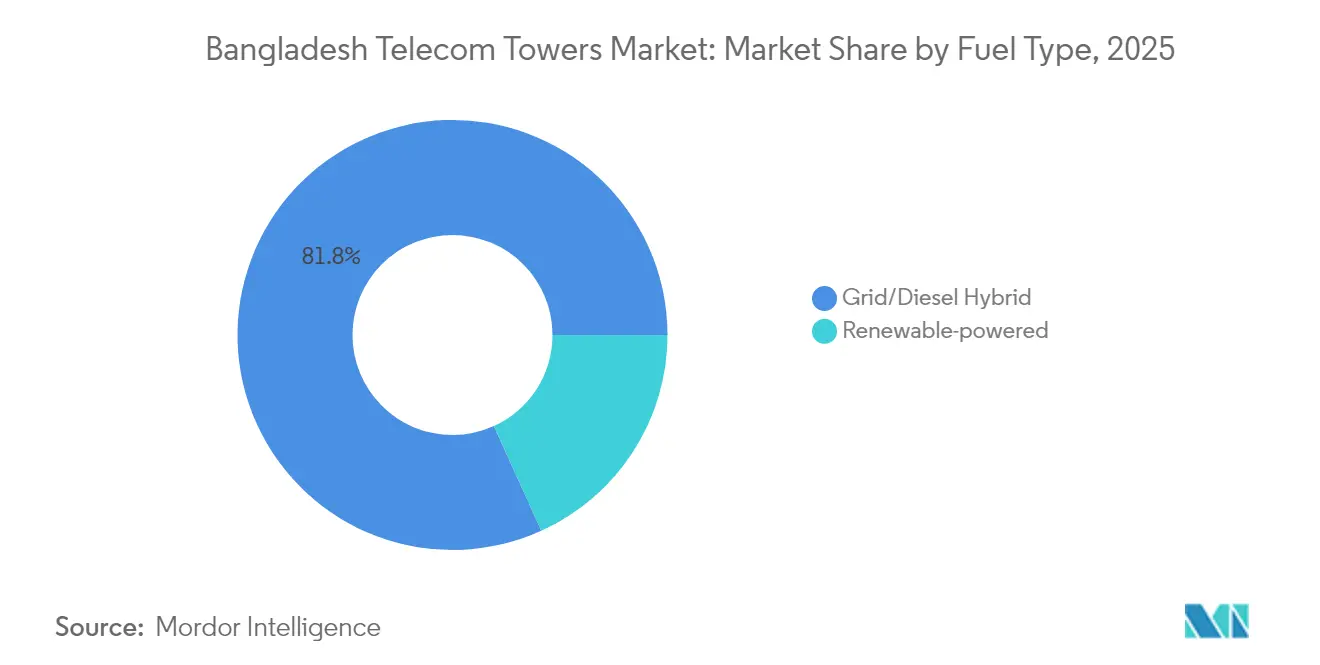

- By fuel type, grid/diesel hybrids accounted for 81.78% of the Bangladesh telecom tower market size in 2025, and renewable-powered sites are on track for a 16.98% CAGR to 2031.

- By tower type, monopoles held 55.02% of the Bangladesh telecom tower market size in 2025 value, but stealth towers are expected to grow at a 9.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 4G subscriber growth and impending 5G rollout | +1.2% | National, with concentration in Dhaka, Chittagong, Sylhet | Medium term (2-4 years) |

| Government tower-sharing policy and licensing of independents | +0.8% | National, with rural focus under Digital Bangladesh | Long term (≥ 4 years) |

| Rural coverage push under “Digital Bangladesh” | +0.9% | Rural areas, particularly northern and coastal regions | Long term (≥ 4 years) |

| Rising data traffic and smartphone penetration | +0.7% | Urban centers expanding to semi-urban areas | Medium term (2-4 years) |

| Back-haul fiber mandates creating new co-siting demand | +0.5% | National, with priority on highway corridors | Medium term (2-4 years) |

| Islamic-finance backed green-tower SLB deals | +0.3% | National, with emphasis on renewable energy zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 4G subscriber growth and impending 5G rollout

Bangladesh added millions of new 4G users in 2024, and Banglalink alone recorded a 23% year-over-year jump to 22 million subscribers [1]TBS Report, “Banglalink’s Revenue Up by 6% in Jan–March,” The Business Standard, tbsnews.net. Each incremental smartphone prompts extra carrier aggregation layers, higher-order MIMO, and new small-cell infill, factors that lift tenancy ratios at existing towers and stimulate ground lease extensions. Anticipated 700 MHz and C-band auctions intensify this need, because contiguous spectrum blocks favor consolidated radio stacks best served by shared, upgrade-ready sites. The Bangladesh telecom tower market, therefore, gains from synchronized MNO demand for power-efficient, fiber-fed locations capable of hosting both LTE and 5G radios. TowerCos that pre-wire for high load factors are positioned to turn spectrum shortages into premium co-location margins.

Government tower-sharing policy and licensing of independents

The Bangladesh Telecommunication Regulatory Commission’s (BTRC) move to issue independent tower licenses unlocked a wave of sale-and-leaseback (SLB) deals, culminating in Summit Towers’ USD 100 million pickup of 2,012 Banglalink structures. Policy support lowers duplication, speeds rural builds, and lets MNOs recycle capital into spectrum. As these regulations mature, the Bangladesh telecom tower market benefits from contractual visibility through 10- to 15-year master lease agreements that combine index-linked rentals, energy-as-a-service modules, and co-branding clauses. Small indigenous TowerCos enjoy a home-field edge in land acquisition and community outreach, translating policy signals into practical rollout momentum.

Rural coverage push under “Digital Bangladesh”

Universal-service obligations require thousands of new macro sites in peripheral zones where grid reliability is weak and subscriber densities are low. The Bangladesh telecom tower market, therefore, prioritizes modular designs, satellite backhaul, and solar-battery hybrids that keep opex predictable. Islamic finance structures such as Sukuk are emerging to fund these assets because they meet both Sharia compliance and environmental stewardship benchmarks, streamlining access to concessional liquidity. Providers that excel at integrating local contractor networks, micro-logistics, and remote monitoring will unlock long-tail revenue streams while fulfilling national inclusion goals.

Rising data traffic and smartphone penetration

Bangladesh reached record data consumption levels in 2024, pushing Grameenphone to expand capex even as it paid a 330% cash dividend. Higher volume per user elevates network load, forcing carriers to supplement rooftop sites and improve sectorized configurations. The Bangladesh telecom tower market gains directly through higher tenancy and new equipment mounts, but indirectly through differentiated backhaul offerings that valorize fiber-rich locations. Landlords who can guarantee low-latency links and energy resilience achieve stronger renewal pricing and lower churn.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High spectrum fees squeeze MNO capex | -0.6% | National, affecting all operators | Short term (≤ 2 years) |

| Grid unreliability elevates diesel-opex | -0.4% | Rural and semi-urban areas with poor grid connectivity | Medium term (2-4 years) |

| Cyclone/flood-proofing standards inflate refurbishment capex | -0.3% | Coastal regions and flood-prone areas | Long term (≥ 4 years) |

| Taka depreciation raises import costs for steel and RF gear | -0.5% | National, affecting equipment procurement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High spectrum fees squeeze MNO capex

Reserve prices for the 700 MHz band stand at BDT 263 crore per MHz, compelling operators to channel scarce funds into license fees rather than towers [2]Mahmudul Hasan, “Govt Proposes Conditional Concessions Over 700 MHz Spectrum Auction,” The Daily Star, thedailystar.net. Immediate cash drains slow new site orders and elongate payment cycles to TowerCos. Yet the same constraint encourages asset monetization, producing larger tower portfolios under professional management. Consequently, the Bangladesh telecom tower market experiences a short-term order dip but enjoys a medium-term boost once SLB proceeds recycle into co-location contracts.

Grid unreliability elevates diesel opex

Outages exceeding one hour now affect roughly 40% of Teletalk sites [3]Masudul Hoque, “Teletalk Struggles to Keep Up With Private Operators Despite 20 Years in Service,” UNB News, unb.com.bd . Diesel gensets remain the fallback, but fuel price volatility and rising carbon scrutiny shrink profit margins. TowerCos that deploy lithium-ion batteries, remote energy management, and solar can shave diesel runtime by 50%. Over time, the Bangladesh telecom tower market tilts toward providers offering comprehensive green-power packages that guarantee uptime and lock in predictable energy costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Cement Leadership

Independent TowerCos captured a 38.74% Bangladesh telecom tower market share in 2025, a testament to their superior capital structures and operational focus. The Bangladesh telecom tower market size tied to these players is expected to grow faster than operator-owned portfolios, owing to cash-hungry MNOs that view infrastructure divestment as a financing valve. In contrast, joint-venture TowerCos, combining overseas expertise with Bangladeshi stakeholder networks, are forecast to log a 10.11% CAGR, outpacing all other ownership models. As sale-and-leaseback activity accelerates, captive MNO assets will shrink, though operators are likely to retain strategic sites such as switching centers and cross-border interconnect gateways to safeguard service quality.

Second-order effects include a rising role for tower-level energy-as-a-service contracts and proactive fiber cross-leasing that uplift tenancy ratios. Portfolio scale allows independents to bargain down equipment prices and secure concessional green finance, reinforcing a virtuous cycle. For investors, the Bangladesh telecom tower market delivers predictable long-term cash flows anchored in inflation-indexed leases and resilient mobile data demand.

By Installation: Ground-based Dominance, Rooftop Momentum

Ground-based structures represented 73.65% of the 2025 value, underlining their suitability for broad macro coverage across Bangladesh’s flat terrain. This slice of the Bangladesh telecom tower market size remains indispensable for meeting Digital Bangladesh obligations, plus the 90% population-coverage target. Yet rooftop towers are set to clock a 6.62% CAGR, the fastest within the installation slate, reflecting rapid urbanization and zoning restrictions that limit greenfield footprints in Dhaka and Chittagong.

Rooftop demand also rises due to enterprise small-cell deployments and indoor coverage upgrades sparked by e-commerce and fintech traffic surges. Landlords appreciate the lighter structural load and swifter permitting cycle. For TowerCos, rooftops carry higher tenancy potential per square meter and lower land-lease costs, boosting return on invested capital. The Bangladesh telecom tower market, therefore, bifurcates into scale-oriented macro portfolios and premium-priced urban micro clusters.

By Fuel Type: Hybrids Rule, Renewables Race Ahead

Grid/diesel hybrids continued to command 81.78% of the 2025 value, but renewable-powered sites are growing at a striking 16.98% CAGR, buoyed by falling solar LCOE and Islamic-finance aligned Sukuk that funds green upgrades. Operators pursue solarization not only for ESG compliance but also to mitigate diesel theft and price swings. When combined with lithium-ion storage and intelligent controllers, hybrids can slash fuel burn by half and shrink maintenance cycles.

The Bangladesh telecom tower market size tied to renewably powered assets is projected to triple by 2031, reshaping opex profiles. Innovative vendors package power-purchase agreements with uptime guarantees, letting TowerCos capitalize on predictable energy savings. Meanwhile, the government’s carbon-credit framework under discussion could offer additional upside via tradable certificates once finalized.

By Tower Type: Monopoles Lead, Stealth Towers Accelerate

Monopoles secured 55.02% revenue in 2025, prized for their streamlined erection and lower land requisites. They remain the go-to choice for both rural highways and peri-urban clusters. However, stealth or concealed towers are poised for a 9.02% CAGR as municipalities tighten skyline regulations and residents demand aesthetic harmony. Materials innovation, fiberglass radomes, camouflaged cladding, and integrated lighting cut visual intrusion and smooth permitting.

Stealth adoption also correlates with premium rent; landlords typically accept thinner profit margins in exchange for reduced community opposition. Consequently, the Bangladesh telecom tower market records higher lease rates per square foot for concealed solutions, partially offsetting their steeper capex. Lattice and guyed towers maintain niche relevance where height requirements surpass 60 meters or soil conditions favor anchor-wire designs.

Geography Analysis

Dhaka Division hosts the densest cluster of sites and generates the lion’s share of the Bangladesh telecom tower market size, reflecting its 9 million-plus population and concentration of financial and tech hubs. Grameenphone, Banglalink, and Robi each target sub-1 km inter-site distances here to sustain voice and data KPIs, pushing up tenancy ratios and ARPU premiums. Chittagong Division ranks second, propelled by port-driven logistics traffic and special economic zones; tower demand leans toward cyclone-resilient monopoles and redundant fiber loops that guarantee uptime even during storm surges.

Northern regions, Rangpur and Rajshahi, along with western Khulna, record lower revenue per tower yet feature the highest growth prospects under Digital Bangladesh. Government subsidies and Islamic green bonds encourage TowerCos to pilot solar-satellite hybrids in off-grid villages, forging the final link in national coverage. Coastal belts face stricter wind-load standards after the 2024 Cyclone Midhili incident, driving refurbishments that raise site-level opex but widen the moat for well-capitalized TowerCos. Across all zones, the Bangladesh telecom tower market benefits from converging urban and rural strategies that combine traditional macros, rooftop infill, and renewable mini-grids.

Competitive Landscape

Bangladesh sustains a moderately concentrated playing field, with the top five TowerCos. Summit Towers leads indigenous peers after its Banglalink portfolio acquisition, while multinats like edotco emphasize scale-linked energy savings. Foreign entrants eye rural concessions but often team with locals to navigate land tenure, zoning, and political dynamics. Technology partnerships also shape rivalry; Grameenphone’s six-year Ericsson deal layers AI-powered OSS/BSS onto the radio network, raising expectations for always-on performance.

Service diversification acts as a key differentiator. Summit offers turnkey energy-as-a-service contracts, while edotco advertises a 49% carbon-reduction benchmark on solarized sites. Smaller firms carve niches in rooftop aggregation, stealth fabrication, or satellite backhaul positioning. Overall, the Bangladesh telecom tower market tilts toward providers that couple capex agility with end-to-end power, fiber, and regulatory solutions.

Bangladesh Telecom Towers Industry Leaders

EDOTCO Group Sdn Bhd

Summit Towers Limited

Kirtonkhola Tower Bangladesh Limited (Confidence Group)

iSON Tower Bangladesh Ltd. (iSON Group)

Frontier Towers Bangladesh Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The government floated conditional 5–10% spectrum price reductions contingent on accelerated network upgrades and quality of service benchmarks.

- February 2025: Grameenphone declared a 330% cash dividend worth BDT 4,455 crore (USD 37.1 million), underlining robust free cash flow.

- January 2025: Ericsson signed a six-year IT transformation pact with Grameenphone, embedding AI-driven automation across OSS/BSS stacks.

- January 2025: Starlink Services Bangladesh Limited received two ten-year licenses for commercial satellite internet, introducing a non-terrestrial alternative for rural connectivity.

- February 2024: Summit Towers closed its USD 100 million purchase of 2,012 Banglalink towers under a 12-year master lease.

Bangladesh Telecom Towers Market Report Scope

Telecommunication towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The Bangladeshi telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), installation (rooftop and ground-based), and fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of installed base (thousand units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

What is the current value of the Bangladesh telecom tower market?

The market was valued at USD 802.91 million in 2026 and is projected to reach USD 981.74 million by 2031.

How fast is renewable power adoption at tower sites growing?

Renewable-powered locations are forecast to post a 16.98% CAGR as operators and TowerCos pursue lower opex and ESG targets.

Which ownership model holds the largest slice of tower assets?

Independent TowerCos lead with 38.74% share following high-profile sale-and-leaseback deals.

Why are rooftop towers becoming more popular in Bangladesh?

Urban densification, zoning limits on greenfield land, and faster deployment cycles make rooftops the fastest-growing installation category at 6.62% CAGR.

How does spectrum cost affect tower deployment?

Elevated reserve prices pressure MNO capex, temporarily slowing new builds but driving tower asset divestments that ultimately expand co-location demand.

What role do stealth towers play in urban areas?

Concealed structures grow at 9.02% CAGR because municipal regulations and community aesthetics favor low-visibility solutions.

Page last updated on: