Indonesia Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

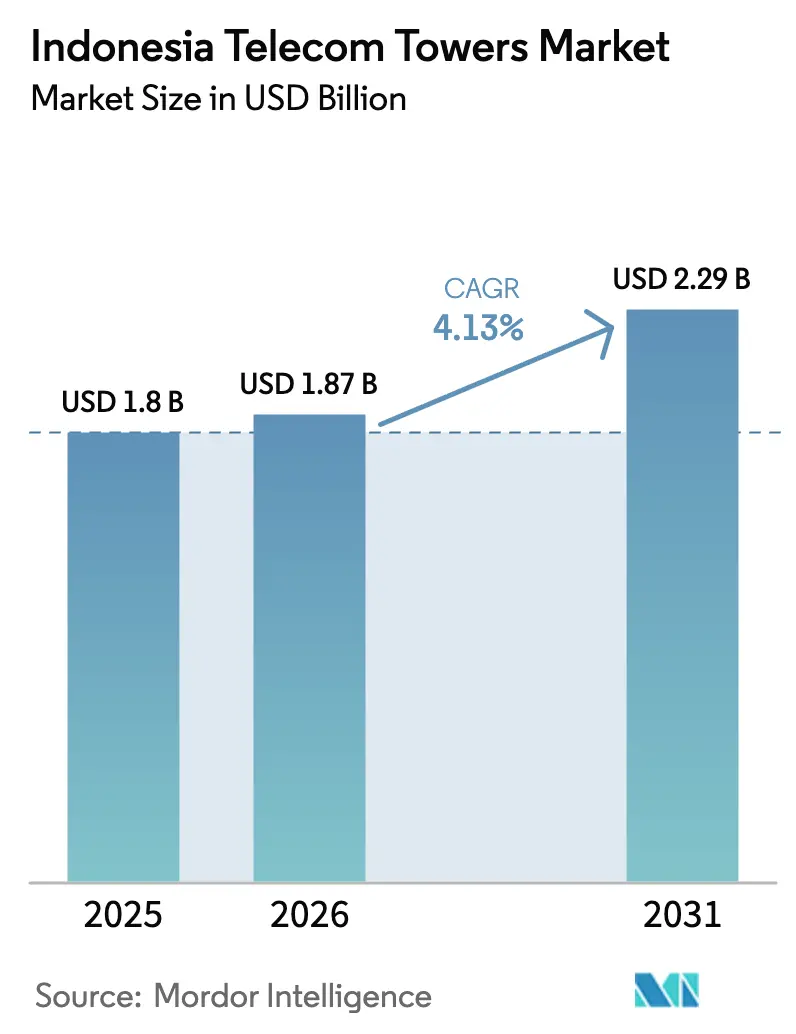

| Base Year Market Size (2025) | USD 1.8 Billion |

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Telecom Towers Market Analysis by Mordor Intelligence

Indonesia Telecom Towers Market size in 2026 is estimated at USD 1.87 billion, growing from 2025 value of USD 1.8 billion with 2031 projections showing USD 2.29 billion, growing at 4.13% CAGR over 2026-2031.

This steady climb is anchored in the nation’s role as Southeast Asia’s largest digital economy, 5G spectrum auctions covering 700 MHz, 2.6 GHz, and 26 GHz frequencies, and rural connectivity mandates that stimulate continuous infrastructure roll-outs. Independent tower companies are scaling portfolios quickly through sale-leaseback transactions, while rooftop and stealth structures multiply in dense urban zones to meet data-traffic spikes. Renewable-powered sites, supported by ESG-linked financing, are carving out a fast-growing niche that lowers life-cycle costs and carbon footprints. Consolidation, highlighted by Mitratel’s aggressive acquisitions and the pending XL Axiata-Smartfren merger, is recalibrating tenancy ratios, competitive tactics, and capital allocation across the Indonesian telecom towers market.

Key Report Takeaways

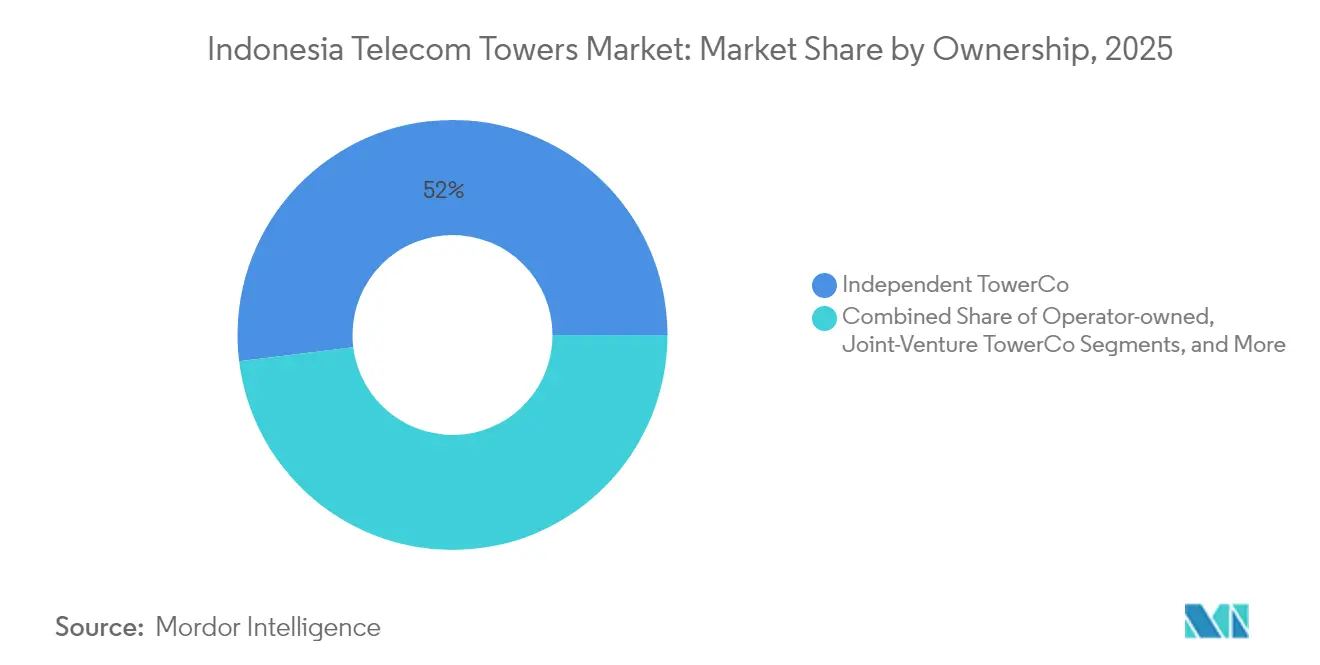

- By ownership, independent tower companies led with 51.95% revenue share in 2025; the segment is projected to expand at a 7.35% CAGR through 2031.

- By installation, ground-based sites accounted for 64.92% of the Indonesian telecom towers market share in 2025, while rooftop deployments are poised for a 5.67% CAGR to 2031.

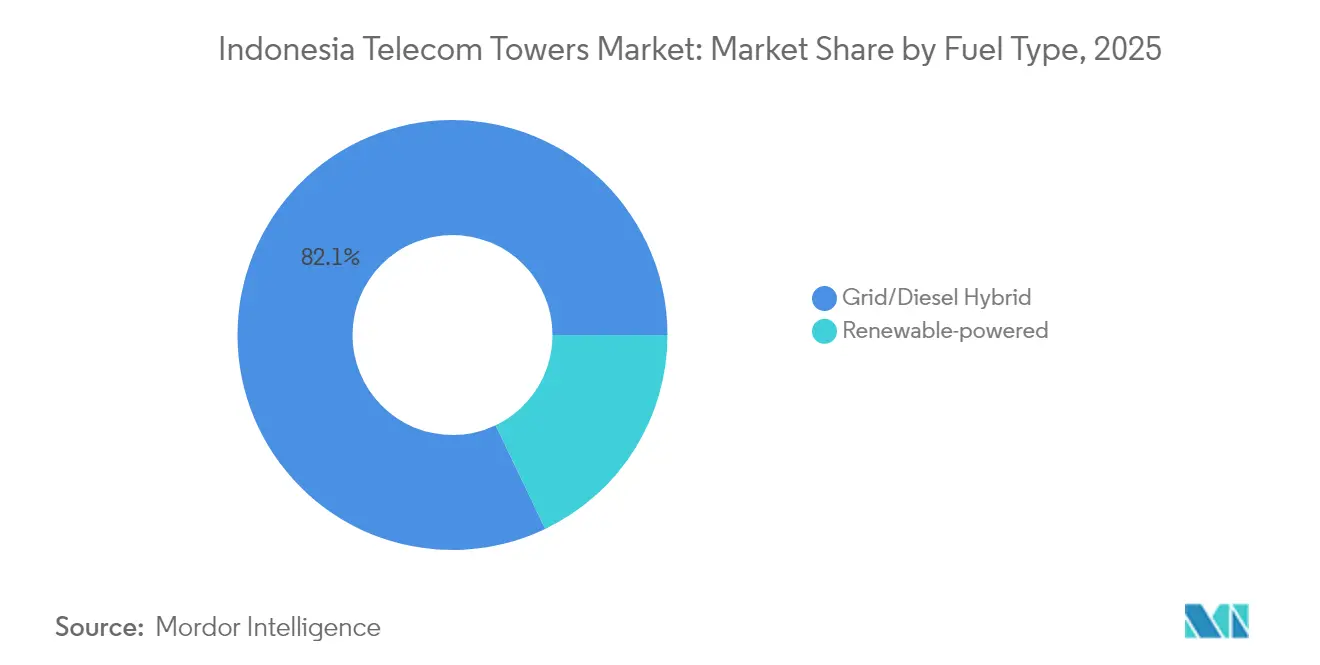

- By fuel type, grid/diesel hybrids commanded 82.10% share of the Indonesian telecom towers market size in 2025; renewable-powered towers are forecast to grow at a 19.85% CAGR through 2031.

- By tower type, monopole structures held a 46.02% share in 2025, whereas stealth/concealed designs are advancing at a 10.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide 5G spectrum release and rollout momentum | +1.2% | National with early gains in Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| Rural 4G connectivity mandates and BAKTI subsidies | +0.8% | 3T regions | Long term (≥ 4 years) |

| Accelerating sale-leaseback deals by MNOs | +0.9% | Java and Sumatra | Short term (≤ 2 years) |

| 3G switch-off unlocking spare tower capacity | +0.4% | Primarily urban areas | Short term (≤ 2 years) |

| TowerCo move into fiber-to-tower and edge micro-DC services | +0.6% | High-density corridors | Medium term (2-4 years) |

| Surge in ESG-linked, lower-cost green-site financing | +0.3% | Remote and off-grid zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nationwide 5G Spectrum Release and Rollout Momentum

Indonesia is auctioning 700 MHz, 2.6 GHz, and 26 GHz bands in 2025, enabling differentiated coverage and capacity layers that require dense site grids and new antenna configurations. TowerCos are pre-positioning capital to support 13 priority zones, including the new capital city and six Super Priority Tourism Destinations, giving the Indonesian telecom towers market predictable multi-year revenue streams [1]Ministry of Communication and Information Technology, “Rencana Pelelangan Spektrum 2025,” kominfo.go.id. Mitratel has expanded its service lines to include edge infrastructure and antenna sharing that align with 5G architectural needs.

Rural 4G Connectivity Mandates and BAKTI Subsidies

Through the BAKTI Universal Service Obligation program, 1,665 subsidized and 4,995 blended-financing sites are earmarked for remote islands and underserved frontier areas. These contracts de-risk long-haul deployments and lock in annuity income for tower providers while furthering national inclusion goals [2]BAKTI, “Program USO 2025,” bakti.kominfo.go.id.

Accelerating Sale-Leaseback Deals by MNOs

Mobile network operators are divesting passive assets to fund spectrum fees estimated at IDR 41.9 trillion and to preserve balance-sheet flexibility. The XL Axiata-Smartfren merger is expected to catalyze additional divestitures after network integration, lifting tenancy ratios and portfolio scale for independent TowerCos [3]PT XL Axiata Tbk, “Proposed Merger with Smartfren,” xlaxiata.co.id.

3G Switch-Off Unlocking Spare Tower Capacity

Legacy 3G networks are being dismantled ahead of 5G roll-outs, freeing space and structural load for new radios without fresh site builds. Tower operators can add tenants and upsell equipment upgrades to enrich revenue per tower while helping MNOs migrate spectrum to higher-efficiency technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lease-rate renegotiation pressure from MNOs | −0.6% | Competitive urban markets | Short term (≤ 2 years) |

| High leverage amid rising interest-cost environment | −0.4% | National | Medium term (2-4 years) |

| Municipal crack-downs on unlicensed BTS structures | −0.3% | West Java and urban centers | Short term (≤ 2 years) |

| LEO-satellite backhaul substituting remote towers | −0.2% | Remote islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lease-Rate Renegotiation Pressure from MNOs

Post-merger, the combined XL Axiata-Smartfren entity wields 94.5 million subscribers and aims for USD 300-400 million in annual synergies, sharpening its stance during lease renewals. Urban markets with site overlap face heightened risk of churn or rate compression, prompting TowerCos to bundle fiber, power, and managed services to protect yields.

High Leverage Amid Rising Interest-Cost Environment

Net debt-to-EBITDA ratios, such as Tower Bersama’s 4.6x, expose operators to refinancing strain as interest costs climb. Providers are exploring green bonds and infrastructure funds to refinance debt and to channel capex toward renewable-powered sites that carry lower operating expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent Tower Companies Reshape Asset Control

Independent TowerCos captured 51.95% of the Indonesian telecom towers market in 2025, validating a model that unlocks capital for MNOs and boosts network agility. Mitratel alone operates 39,259 sites after purchasing 1,800 towers from IOH and Gametraco, cementing its leadership in the Indonesian telecom towers market size expansion. Higher tenancy ratios of 1.51x versus sub-1.3x at operator-owned portfolios drive stronger cash yields and fuel further acquisitions.

The pace of sale-leasebacks suggests that independent providers will remain the sector’s growth engine through 2031. Joint-venture structures appear in selective high-value corridors, while captive MNO portfolios focus on mission-critical or regulatory sites. Asset-light trends and the need to fund 5G capex mean divestments will stay elevated, keeping the Indonesian telecom towers market on a consolidation path that favors scaled independents for improved bargaining power and network reach.

By Installation: Rooftop Uptick Complements Ground-Based Dominance

Ground-based towers held 64.92% of the Indonesian telecom towers market share in 2025, delivering wide-area coverage across the archipelago’s varied topography. Rooftop structures, however, posted a 5.67% CAGR, reflecting densification needs in Jakarta, Surabaya, and other metros where land scarcity and zoning hurdles challenge new ground builds. Rooftops provide faster permits, lower land rent, and close-in coverage that supports millimeter-wave 5G.

Outside Java, macro ground sites remain indispensable for cost-effective coverage of sparsely populated islands. Dual-strategy portfolios that blend rooftops for capacity and ground sites for reach enable TowerCos to match evolving operator demand. This mix gives the Indonesian telecom towers market flexibility to accommodate both high-growth urban data loads and rural connectivity mandates.

By Fuel Type: Renewable Solutions Accelerate Cost and Carbon Wins

Grid/diesel hybrids dominated with 82.10% share in 2025, but renewable-powered sites are scaling at a 19.85% CAGR as solar prices fall and battery storage improves. JETRO-backed solar hybrids can cut diesel burn by 78%, shrinking operating costs that can otherwise run 30-40% of a remote tower’s expense base. ESG-linked financing instruments further shave funding costs and enhance investor appeal for TowerCos that decarbonize portfolios.

Protelindo, Mitratel, and EdgePoint have each launched solar pilot programs targeting 3T regions where grid power is costly or absent. Lower fuel logistics, improved uptime, and regulatory goodwill position renewables as a strategic lever that widens margins and future-proofs assets, enriching the Indonesia telecom towers market size trajectory through 2031.

By Tower Type: Stealth and Micro Designs Address Visual and Zoning Barriers

Monopole structures held a 46.02% share in 2025 due to their versatile cost-height profile, yet stealth towers are expanding at a 10.18% CAGR as municipalities tighten visual-impact rules. Mitratel’s glass-fiber micro towers shed 60% of weight, allowing easier rooftop placement and lower wind-load requirements while meeting aesthetic standards.

Stealth formats such as concealed monopoles, camouflaged palms, and light poles support densification without community pushback. They also expedite permitting in heritage or tourism districts, making them integral to small-cell 5G rollouts. Together with classic lattice or guyed options for rural spans, the expanding design palette enables tailored deployments that reinforce growth across the Indonesian telecom towers market.

Geography Analysis

Java’s corridors anchor demand, housing 41% of Mitratel’s inventory and the nation’s densest data traffic zones. Urban sprawl and e-commerce adoption force operators to layer capacity sites atop existing macro grids, fueling rooftop and stealth installations. Sumatra holds 28.9% of portfolio sites, leveraging economic corridors in Medan and Palembang that rely on resource extraction and industrial clusters.

The outer islands collectively host 59% of towers, underscoring national coverage commitments. Sulawesi and Kalimantan see expanding tower footprints to serve nickel processing hubs and the new capital city, while Bali-Nusa Tenggara and Maluku-Papua receive BAKTI-backed builds to bridge coverage gaps. Border regions adjacent to Singapore, Malaysia, Timor Leste, and Papua New Guinea feature strategic installations that blend commercial duties with sovereignty objectives, offering incremental revenue channels within the Indonesian telecom towers market.

Remote deployments face severe logistical and power challenges. Specialized “Merah Putih” BTS units and solar-hybrid kits mitigate fuel reliance, while satellite backhaul augments fiber links across straits. Local tower firms offer permitting agility and community reach, but scaled nationals leverage purchasing power and engineering depth. The resulting geography mix balances high-ARPU metro nodes with policy-driven rural builds, sustaining the long-run growth outlook for the Indonesian telecom towers market size.

Competitive Landscape

Three independent players, Mitratel, Protelindo, and Tower Bersama, dominate national footprints, with Mitratel alone operating 39,259 sites. Its EBITDA margin surpasses 80% on rising tenancy ratios and ecosystem diversification into fiber, managed services, and power-as-a-service. Protelindo and Tower Bersama counter with regional depth and bundled solutions that include microwave backhaul and in-building systems.

Competition intensifies as the USD 6.5 billion XL Axiata-Smartfren merger readies to rationalize overlapping sites by 20-25%. TowerCos must defend lease renewals through superior uptime, fiber capillarity, and green-power offerings. Edge compute co-location is emerging as a differentiator, and agreements with data-center operators unlock higher-margin revenue streams beyond passive rent.

Mitratel’s eleven-line ecosystem strategy spans tower leasing, small cells, IBS, IoT hosting, and drone-assisted inspections. Protelindo explores green bonds to refinance debt while expanding solar capacity. Tower Bersama invests in AI-driven site analytics to optimize asset utilization. These pivots signal a turn toward platform plays that stretch value extraction across the Indonesian telecom towers industry without diluting core tenancy economics.

Indonesia Telecom Towers Industry Leaders

PT Dayamitra Telekomunikasi Tbk (Mitratel)

PT Profesional Telekomunikasi Indonesia Tbk (Protelindo)

PT Tower Bersama Infrastructure Tbk (TBIG)

PT Centratama Menara Indonesia (EdgePoint)

PT Bali Towerindo Sentra Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: NTT East Corporation announced a strategic USD 2.5 billion (IDR 4 trillion) investment in PT Integrasi Jaringan Ekosistem (WEAVE), acquiring 49% ownership to accelerate nationwide FTTH and edge infrastructure deployment.

- February 2025: The Ministry of Communication and Digital Affairs published auction rules for 1.4 GHz spectrum with 80 MHz bandwidth to enable 100 Mbps broadband speeds and encourage community-network models.

- January 2025: Indosat Ooredoo Hutchison partnered with ZTE to extend rural 4G coverage through advanced radio access equipment optimized for remote terrains.

- December 2024: XL Axiata and Smartfren signed a definitive agreement forming PT XLSmart Telecom Sejahtera, creating a 94.5 million-subscriber entity targeting USD 300-400 million annual synergies.

- December 2024: Telkomsel teamed with Tencent and M Cash Integrasi to build AI-powered palm biometric and eKYC solutions for enterprise clients.

- November 2024: PT Solusi Sinergi Digital (SURGE/WIFI) inked an MoU with NTT e-Asia for nationwide fiber backbone, FTTH, and fixed-wireless access projects.

Indonesia Telecom Towers Market Report Scope

Telecommunication towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The Indonesia telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), by installation (rooftop, and ground-based), and by fuel type (renewable and non-renewable).

The market size and forecasts are provided in terms of installed base (Thousand Units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

What is the current value of the Indonesia telecom towers market?

The market is valued at USD 1.87 billion in 2026 and is projected to reach USD 2.29 billion by 2031.

How fast are renewable-powered tower sites growing?

Renewable-powered sites are expanding at a 19.85% CAGR as TowerCos decarbonize portfolios and cut operating costs.

Why are independent tower companies gaining share in Indonesia?

Operators are selling passive assets to fund spectrum fees and 5G roll-outs, enabling independents to capture 51.95% share in 2025.

Which installation type is rising quickest in urban Indonesia?

Rooftop towers are the fastest-growing installation category with a 5.67% CAGR driven by densification needs in major cities.

How will the XL Axiata–Smartfren merger affect tower leasing rates?

The merged operator’s larger scale increases bargaining power, which could pressure lease renewals, especially in overlapping urban sites.

What role does BAKTI play in rural tower expansion?

BAKTI subsidies de-risk 1,665 fully funded and 4,995 blended-financing sites, ensuring connectivity in remote 3T regions while providing TowerCos with long-term revenue certainty.

Page last updated on: