Malaysia Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

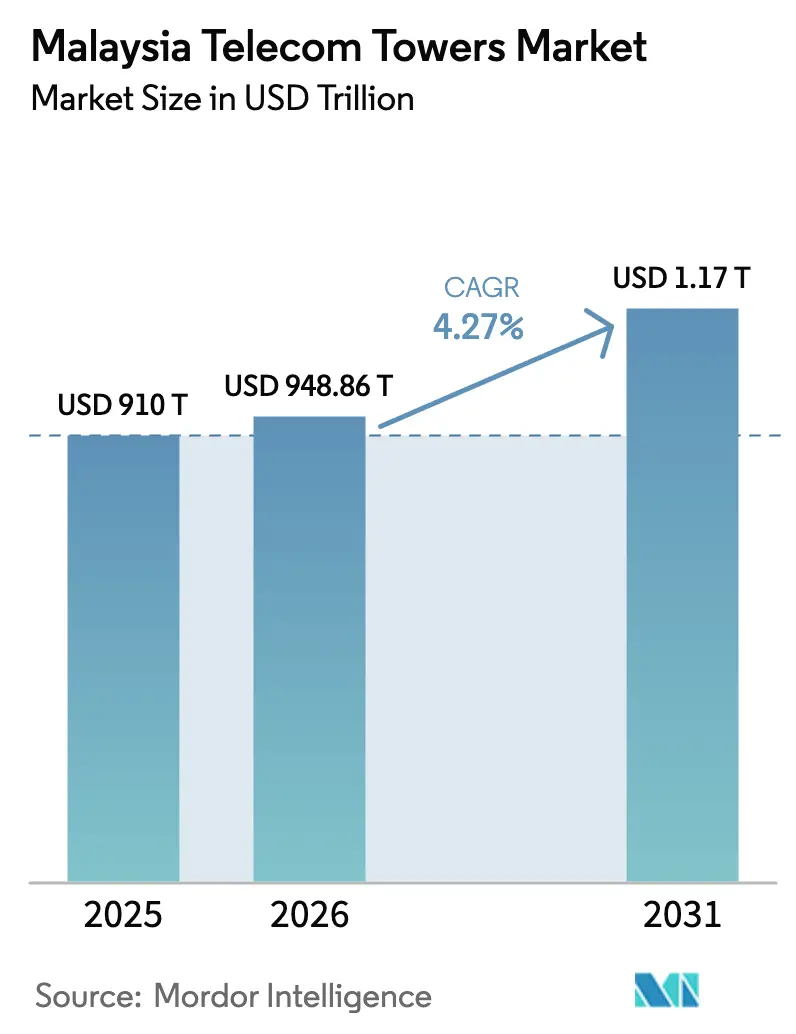

| Base Year Market Size (2025) | USD 910 Billion |

| Market Size (2026) | USD 948.86 Billion |

| Market Size (2031) | USD 1169.18 Billion |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Telecom Towers Market Analysis by Mordor Intelligence

Malaysia Telecom Towers Market size in 2026 is estimated at USD 948.86 million, growing from 2025 value of USD 910 million with 2031 projections showing USD 1169.18 million, growing at 4.27% CAGR over 2026-2031.

Rising 5G coverage needs, the JENDELA connectivity program, and industry-wide moves to divest passive assets collectively shape the current growth outlook. Most new demand originates from parallel 5G network construction, while rural gaps continue to require traditional macro sites that support JENDELA targets. Consolidation among TowerCos is accelerating, enabling scale advantages in energy management, tenancy optimization, and regulatory compliance. At the same time, renewable-powered sites are beginning to temper operating costs in remote corridors, and the nationwide Multi-Operator Core Network (MOCN) arrangement is helping incumbents rationalize capex without compromising service quality.

Key Report Takeaways

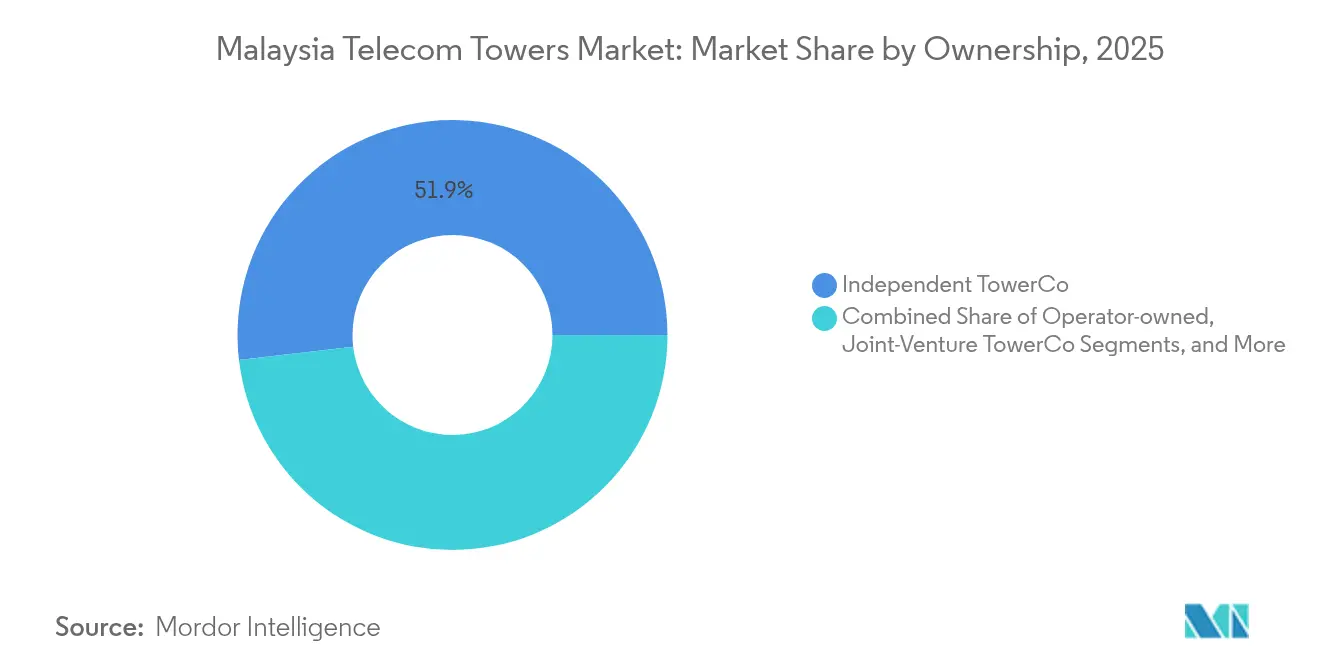

- By ownership, independent TowerCos led with 51.86% of the Malaysia telecom tower market share in 2025; the same segment is projected to post a 7.7% CAGR through 2031.

- By installation type, ground-based structures commanded 60.95% of the Malaysia telecom tower market size in 2025, whereas rooftop deployments are advancing at a 5.29% CAGR to 2031.

- By fuel type, grid/diesel hybrid systems accounted for 80.72% of the Malaysia telecom tower market size in 2025, while renewable-powered sites are forecast to expand at a 19.52% CAGR through 2031.

- By tower type, monopoles captured 49.73% revenue in 2025, while stealth and concealed structures recorded the fastest CAGR at 6.83% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dual-network 5G rollout accelerating new macro and small-cell sites | +1.2% | Urban corridors in Klang Valley, Penang, Johor Bahru | Medium term (2-4 years) |

| Government JENDELA targets pushing rural tower builds | +0.8% | East Malaysia and northern peninsular states | Long term (≥ 4 years) |

| Mobile-data surge demanding 4G/5G densification and co-locations | +0.9% | Nationwide, highest in tourism and business hubs | Short term (≤ 2 years) |

| State-TowerCo consolidation unlocking capex for upgrades | +0.6% | All states, concentrated around multitenant clusters | Medium term (2-4 years) |

| Solar-hybrid power lowering OPEX for off-grid corridors | +0.4% | Remote highways, islands, and off-grid corridors | Long term (≥ 4 years) |

| Land-owner credit access program speeding site acquisition | +0.3% | Fragmented rural parcels in East Malaysia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dual-network 5G rollout accelerating new macro and small-cell sites

Malaysia’s shift from a single wholesale 5G model to two parallel networks forces operators to duplicate coverage footprints in high-value areas. U Mobile secured regulatory approval in March 2025 to deploy the country’s second 5G network, immediately inking tower access deals with EdgePoint Infrastructure and EDOTCO [1]Alexander Wong, “U Mobile Receives MCMC Award Letter to Deploy Malaysia’s Second 5G Network,” SoyaCincau, soyacincau.com. The need for differentiated services prompts additional macro towers and small cells in dense precincts where spectrum reuse drives performance. Parallel builds keep tenancy ratios healthy for independent TowerCos despite infrastructure sharing through the fully operational six-way MOCN framework.

Government JENDELA targets pushing rural tower builds

JENDELA mandates near-universal broadband by 2025, extending obligations into regions that lack immediate commercial return. The Communications Ministry emphasized Sabah tourist hotspots in April 2025 as priority zones ahead of Visit Malaysia 2026 [2]Bernama, “Step Up Internet Quality at Sabah Tourist Spots Ahead of VM2026,” Free Malaysia Today, freemalaysiatoday.com. MCMC followed with intensified field tests to enforce quality standards, compelling operators to add macro sites even where population density is low. Funding models mix federal subsidies and TowerCo leasing to compensate for slender revenue streams, ensuring continued activity in remote East Malaysia.

Mobile-data surge demanding 4G/5G densification and co-locations

Per-user mobile data consumption is projected to climb from 21.6 GB a month in 2024 to 51.9 GB in 2029, a 140% jump. 84% of mobile subscriptions are expected to adopt 5G by 2029, putting pressure on existing macro grids. Operators, therefore, seek co-location agreements that spread electronics across shared towers while adding capacity sectors. Although the six-way MOCN arrangement streamlines active-layer sharing, physical towers still require extra load-bearing upgrades for additional antenna arrays and microwave dishes.

State-TowerCo consolidation unlocking capex for upgrades

Asset-light strategies gain traction as carriers monetize passive infrastructure. Khazanah Nasional increased its stake in EDOTCO to 32% in March 2025, aligning sovereign wealth with TowerCo expansion plans. Parent operator Axiata, back in profit by FY 2024, uses proceeds to fund core RAN modernization. Similar divestment reviews at EdgePoint Infrastructure reveal strong private-equity interest, though valuations remain sensitive to tenancy outlook. Consolidation delivers unified maintenance regimes, group-wide energy procurement, and portfolio-level ESG reporting that appeal to both lenders and enterprise clients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-level permitting complexity and fees | -0.7% | Selective pressure in Selangor, Penang, Johor | Short term (≤ 2 years) |

| Uncertain 5G monetization curbing operator CAPEX | -0.9% | Nationwide revenue models for all MNOs | Medium term (2-4 years) |

| Limited RE supply slowing green-tower programs | -0.3% | Industrial belts with high grid demand | Long term (≥ 4 years) |

| Dual-network duplication risk lowering tenancy ratios | -0.5% | Existing portfolios in mature urban clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

State-level permitting complexity and fees

Land use, aesthetic controls, and local taxation vary markedly among Malaysia’s 13 states. In developed Selangor and Penang, extra environmental studies and community consultations lengthen approval windows, delaying much-needed 5G densification. MCMC’s April 2025 warning that telcos face penalties for poor service quality heightens urgency but does not override state authority [3]Heirul Kamel, “MCMC to Crack Down on Telcos Over Poor Internet Access,” Lowyat.net, lowyat.net. TowerCos, therefore, dedicates liaison teams to harmonize documentation, yet still budget longer lead times and higher compliance costs compared with federal approvals.

Uncertain 5G monetization curbing operator CAPEX

Malaysia achieved 82.4% population-area 5G coverage and 53.35% adoption by December 2024. Even so, average revenue per user has not risen proportionately, raising questions about return on investment under the dual-wholesale model. The GSMA cautioned in April 2025 that investment appetites might stay subdued until pricing clarity improves. Dell’Oro Group forecasts operator capex-to-revenue ratios sliding from 16% in 2024 to 14% by 2027, signaling cautious spend on new towers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos widen lead through scale efficiency

Independent TowerCos captured 51.86% of Malaysia's telecom tower market share in 2025, translating into the largest revenue pool within the sector. Their share is projected to climb on a 7.7% CAGR as operators divest aging portfolios and prioritize spectrum upgrades. The Malaysia telecom tower industry demonstrates that neutral hosts can raise tenancy ratios faster than vertically integrated entities because every MNO seeks quick, capex-light coverage solutions. EDOTCO’s revenue grew 9.64% and operating profit 23.24% in 2024, affirming that lean cost structures and systematic power-savings programs underpin margin expansion.

Joint-venture TowerCos offer a bridge model; OCK Group’s Laotian expansion via a 70% government joint venture indicates how regional diversification enhances earnings resilience. Operator-owned and MNO-captive towers still serve mission-critical traffic in legacy areas but now face growing economic pressure to unlock trapped capital. As the Malaysia telecom tower market advances toward 2030, independent players are expected to dominate strategic corridors and roll out smart-monitoring platforms that optimize energy, security, and predictive maintenance.

By Installation: Ground-based strength balanced by urban rooftop momentum

Ground-based structures delivered 60.95% of Malaysia's telecom tower market size in 2025, benefiting from cost-effective builds on available land parcels across rural peninsular districts. They remain vital for wide-area macro coverage, especially under JENDELA obligations. Conversely, rooftop deployments enjoy a 5.29% CAGR through 2031 as city councils increasingly favor unobtrusive solutions that preserve skyline aesthetics. The Malaysia telecom tower market, therefore, splits between rural reach and urban capacity, with many operators adopting mixed portfolios that cap average build cost while maximizing densification potential.

Rooftop towers often integrate stealth panels and compact antennas, mitigating visual impact and easing municipal approvals. They also shorten fiber backhaul distances in dense precincts, improving latency for 5G enterprise use cases. The six-way MOCN framework further elevates rooftop appeal; shared active equipment reduces the load per operator, allowing lighter structures and smaller floorprints in premium locations.

By Fuel Type: Renewable adoption accelerates despite grid preference

Grid/diesel hybrid solutions maintained 80.72% of Malaysia's telecom tower market size in 2025 because mains electricity access remains widespread in the peninsular states. Diesel generators still back up critical sites, especially those hosting multiple operators. However, renewable-powered towers post a robust 19.52% CAGR to 2031 as sustainability targets climb corporate agendas. EdgePoint’s 5.9 kWp solar-hybrid site, unveiled in April 2025, achieved a 78% annual CO₂ reduction, delivering proof of concept for tropical solar viability.

Limited renewable-energy supply and high upfront costs slow wider rollout, yet Malaysia’s Corporate Green Power Program encourages long-term power-purchase agreements. TowerCos increasingly bundle solar arrays, lithium-ion batteries, and smart controllers to lower diesel truck rolls and improve uptime along remote highway corridors. As carbon reporting becomes a stakeholder expectation, renewable assets are poised to differentiate portfolios and attract sustainability-linked financing.

By Tower Type: Monopole prevalence challenged by stealth solutions

Monopoles held 49.73% revenue share in 2025 and remain favored for quick deployment, small footprint, and modular extension capability. Their single-column design aligns with suburban zoning rules, allowing easier approvals than lattice alternatives. Yet stealth and concealed formats grow at 6.83% CAGR because community pushback against visual clutter intensifies in affluent districts. These designs disguise antennas within flagpoles, signage, or building facades, commanding higher rents but unlocking sites otherwise off-limits to conventional towers.

Lattice and guyed structures address exceptional height and loading demands, particularly for broadcast or rugged terrains, but their share is dwindling as operators restructure networks for dense 5G. The Malaysia telecom tower market thus pivots toward flexible form factors that balance capacity with compliance, ensuring that design considerations incorporate both engineering and neighborhood acceptance.

Geography Analysis

Peninsular Malaysia anchors network revenue, with Klang Valley, Penang, and Johor Bahru generating the bulk of tower leasing due to concentrated population and rapid enterprise digitization. These metropolitan clusters lead small-cell experimentation and rooftop demand, complementing broader macro grids that sustain mobility flows along interstate highways. Independent TowerCos dominate ownership across these corridors, leveraging multitenancy economics and streamlined permitting to keep pace with data traffic growth and SLA targets.

East Malaysia, covering Sabah and Sarawak, demonstrates contrasting economies. Topography, sparser settlements, and higher logistics costs elevate build expenses, yet tourism and resource sectors create pockets of premium demand. The federal push to improve connectivity at Sabah tourist sites ahead of Visit Malaysia 2026 brings new federal-state coordination, pairing JENDELA subsidies with carrier commitments to deliver quality targets. Renewable-powered towers see earlier adoption here, given limited grid reach and high diesel logistics.

State-specific permitting rules shape deployment cadence across both regions. Selangor’s stricter aesthetic criteria prolong urban rooftop approval, while Kelantan offers streamlined protocols aimed at accelerating rural builds. The Malaysia telecom tower market, therefore, requires nuanced roll-out sequencing that weighs commercial density, subsidy availability, and administrative timelines. The national MOCN helps equalize service parity, yet physical tower siting must still navigate local ordinances and land-owner negotiations.

Competitive Landscape

The Malaysia telecom tower market shows moderate concentration with three large independent TowerCos, EDOTCO, EdgePoint Infrastructure, and OCK Group, controlling a majority of third-party assets. EDOTCO alone manages more than 20,000 regional sites, and its parent Axiata is evaluating strategic options worth about USD 3 billion. EdgePoint’s regional portfolio exceeds 15,400 sites, including around 1,800 in Malaysia; potential sale discussions by DigitalBridge underline sustained investor appetite. OCK Group, while smaller domestically, leverages ASEAN expansion to balance exposure and positions itself for high-growth renewable retrofits.

Competitive edges increasingly hinge on energy solutions, regulatory mastery, and digital analytics rather than pure tower count. EdgePoint’s solar-hybrid launch differentiates its ESG credentials and lowers lifecycle OPEX, while EDOTCO pilots advanced battery analytics and AI-driven preventive maintenance to raise uptime. Smaller regional players exploit local relationships to secure municipal rooftop rights, forming niche clusters that later become acquisition targets for larger TowerCos.

The six-way MOCN environment reshapes bargaining power. Operators benefit from shared active layers, while TowerCos must maintain flexible commercial models to secure multitenant commitments under potentially lower average tenancy ratios. Companies prepared to integrate small-cell hosts, street-level poles, and indoor DAS within a single leasing framework stand to capture incremental revenue as 5G use cases diversify.

Malaysia Telecom Towers Industry Leaders

EDOTCO Group Sdn Bhd

EdgePoint Infrastructure Sdn Bhd.

OCK Group Bhd

D'Harmoni Telco Infra Sdn.Bhd.

PDC Telecommunication Services Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EdgePoint Towers launched Malaysia’s first solar-hybrid site featuring 5.9 kWp PV panels and battery storage, cutting annual emissions by 78% and enabling 100% renewable power during optimal hours.

- March 2025: U Mobile received the MCMC Letter of Award to build Malaysia’s second 5G network, ushering in a dual-network era.

- March 2025: Khazanah Nasional raised its stake in EDOTCO to 32% after purchasing an 11% holding from INCJ.

- February 2025: Maxis introduced a solar-based energy service for its tower footprint to lower carbon intensity and fuel expenses.

- January 2025: The six-way Multi-Operator Core Network covering Celcom, Digi, Maxis, U Mobile, TM, and YTL Communications became fully operational nationwide.

Malaysia Telecom Towers Market Report Scope

Telecom towers play a fundamental role in wireless transmission by supporting antennas and communication equipment. These towers facilitate mobile networks, covering vast areas and ensuring seamless signal broadcasting and reception between mobile devices and the network. Telecom towers come in various designs and sizes, such as lattice towers, monopoles, and guyed towers, tailored to specific locations and network requirements.

The Malaysia telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), by installation (rooftop and ground-based), and by fuel type (renewable and non-renewable).

The Market Sizes and Forecasts are Provided in Terms of Installed Base (in Thousand Units) for all the Above Segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the Malaysia telecom tower market in 2026?

The Malaysia telecom tower market size is valued at USD 948.86 million in 2026.

What is the expected growth rate for tower revenue through 2031?

Market value is projected to rise at a 4.27% CAGR, reaching USD 1169.18 million by 2031.

Which ownership model leads tower deployments?

Independent TowerCos hold 51.86% market share and show a 7.7% CAGR outlook.

Why are rooftop towers gaining traction?

Urban densification and stricter zoning rules favor compact rooftop sites, which are growing at a 5.29% CAGR.

How fast are renewable-powered towers expanding?

Renewable sites exhibit a 19.52% CAGR as operators seek lower OPEX and sustainability gains.

What is the key challenge slowing new tower builds?

State-level permitting complexity and fee variability lengthen approval cycles, hindering rapid expansion.

Page last updated on: