Sports Optic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.45 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sports Optic Market Analysis by Mordor Intelligence

The sports optic market size reached USD 2.45 billion in 2026 and is projected to climb to USD 3.01 billion by 2031, reflecting a CAGR of 4.2% over the forecast period. Growth momentum stems from steady participation in hunting, competitive shooting, and wildlife tourism, which collectively shield demand from short-term macroeconomic fluctuations. Premiumization is accelerating as manufacturers embed laser rangefinding, gyro-stabilization, and augmented-reality overlays that justify price points above USD 1,000. Meanwhile, ongoing material-science breakthroughs, such as ultra-high refractive-index and low-dispersion glass, are lowering lens mass without sacrificing optical throughput, a benefit prized on multi-day backcountry trips. Competitive strategies increasingly revolve around vertical integration into sensor fabrication and direct-to-consumer distribution that bypasses 40-50% retail mark-ups, while sustained wildlife conservation funding in the United States and Japan underwrites stable binocular replacement cycles.

Key Report Takeaways

- By product type, binoculars led with 37.83% of the sports optic market share in 2025; rangefinders are projected to expand at a 5.67% CAGR through 2031.

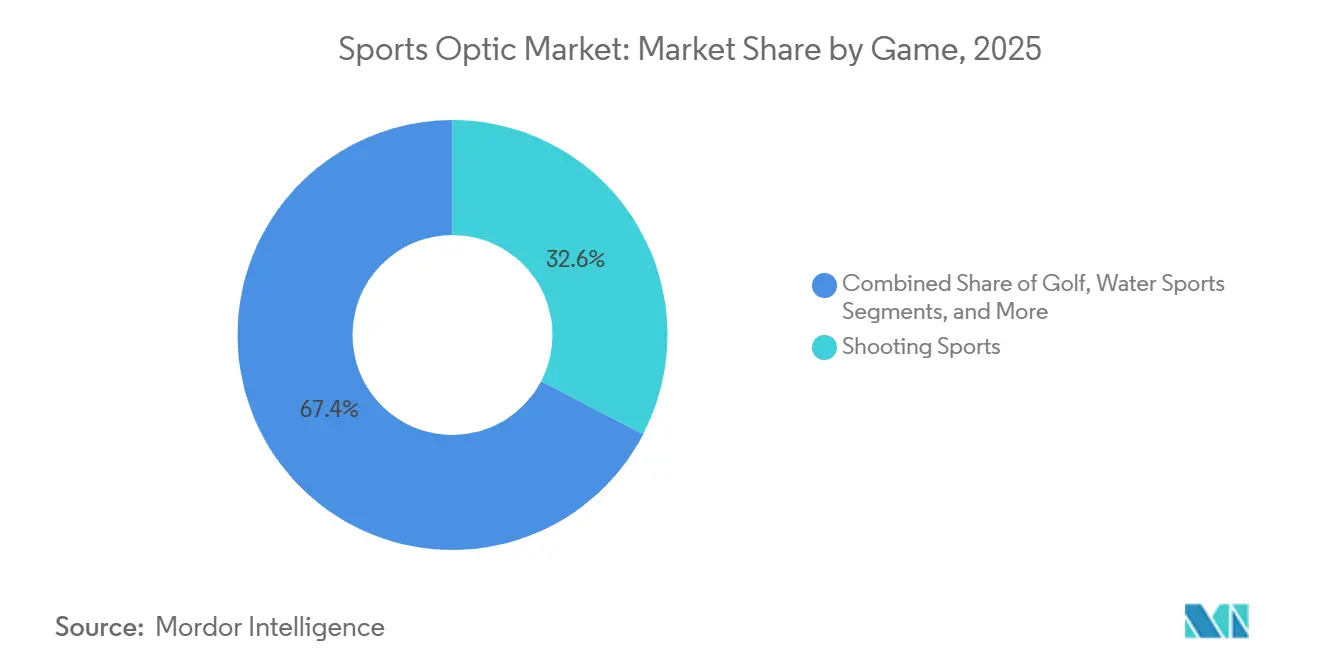

- By game, shooting sports commanded 32.63% of the sports optic market size in 2025, whereas water sports are advancing at a 5.76% CAGR to 2031.

- By geography, North America accounted for 38.73% of the sports optic market size in 2025, while Asia Pacific is expected to register the fastest 5.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sports Optic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enhanced optical clarity through high-density, low-dispersion glass | +0.8% | Global, with premium adoption in North America and Europe | Medium term (2-4 years) |

| Growing popularity of precision shooting competitions | +0.7% | North America, Europe, with emerging adoption in Asia Pacific | Short term (≤ 2 years) |

| Expansion of wildlife and outdoor adventure tourism | +0.9% | Global, with pronounced growth in Asia Pacific and South America | Long term (≥ 4 years) |

| Defense-to-civilian transfer of advanced stabilization technologies | +0.6% | North America and Europe, with spillover to Middle East | Medium term (2-4 years) |

| Integration of augmented-reality overlays in sports optics | +0.5% | North America and Asia Pacific early adopters | Long term (≥ 4 years) |

| 5G-enabled smart binoculars enhancing live fan engagement | +0.4% | Urban centers in North America, Europe, and Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Enhanced Optical Clarity Through High-Density, Low-Dispersion Glass

Material-science gains are raising baseline expectations for image brightness and edge-to-edge sharpness. Nikon’s 2024 glass series achieves refractive indices as high as 2.31, allowing engineers to slim objective diameters by up to 20% without compromising twilight performance.[1]Nikon Corporation, “Nikon Introduces Ultra-High Refractive Index Glasses for Advanced Optical Systems,” Corporate Press Release, nikon.com SCHOTT’s N-SF66 formulation adds apochromatic correction that erases color fringing past 800 meters, a spec welcomed by long-range rifle competitors. Volume adoption is accelerating because precision glass molding now replicates complex aspheric profiles at six-figure annual output, chopping per-unit lens costs by roughly 35%. Weight savings resonate with birders trekking remote blinds and with elderly Japanese tourists whose binocular choices increasingly hinge on sub-600-gram payloads. Together, these advances push premium optics into mid-tier price bands, broadening the addressable base of the sports optic market.

Growing Popularity of Precision Shooting Competitions

Regulatory shifts inside organized marksmanship are widening the feature checklist for optics. The International Shooting Sports Federation lifted the magnification ceiling to 16× in 2024, immediately increasing demand for variable-power scopes, which were previously confined to hunting. The Civilian Marksmanship Program logged 47,000 competitors that year, and survey data show nearly seven in ten swapped optics within 12 months of attending an event. Mandatory first-focal-plane reticles and tool-less turret adjustments now direct spending toward USD 1,200-2,500 models, where margins exceed 55%. This competition-driven refresh cycle supports steady unit growth even as the overall firearms market matures, directly buoying the sports optic market.

Expansion of Wildlife and Outdoor Adventure Tourism

Outdoor recreation delivers a durable consumption tailwind because spending mixes gear, travel, and services. The U.S. Fish and Wildlife Service tallied 96 million wildlife watchers in 2022, and expenditures on equipment reached USD 12.58 billion, up 18% from 2016.[2]U.S. Fish and Wildlife Service, “2022 National Survey of Fishing, Hunting, and Wildlife-Associated Recreation,” fws.gov India’s tiger reserves generated INR 226 billion (USD 2.7 billion) in economic value in 2024, converting predictable permit windows into spikes in binocular rental for tour operators. Japan’s aging population, whose park visitation rose 23% from 2020 to 2024, gravitates towards lightweight, high-eye-relief binoculars that offset presbyopia, reinforcing premium demand. Such demographic breadth cushions the sports optic market against consumer electronics substitution.

Defense-to-Civilian Transfer of Advanced Stabilization Technologies

Gyro-stabilization and thermal fusion are no longer exclusive to military inventories. BAE Systems migrated naval fire-control stabilizers into sub-USD 1,000 marine binoculars that counteract 12-degree vessel roll, broadening offshore usage.[3]BAE Systems, “Gyro-Stabilization Technology for Marine Applications,” baesystems.com L3Harris scaled image-intensifier tubes for civilian night-vision, recording 34% volume growth in 2024 on the back of revised U.S. hunting rules that allow night-time hog control. Elbit Systems cut thermal-core costs below USD 400 when runs exceed 50,000, setting the stage for mass-market binoculars that blend visible, thermal, and range data by the end of the decade. As technology cascades down, mid-tier brands unable to integrate sensors risk erosion of share within the sports optic market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price volatility of rare-earth glass and coatings | -0.5% | Global, with acute impact on mid-tier product manufacturers | Short term (≤ 2 years) |

| Increasing preference for smartphone zoom as substitute | -0.6% | Urban markets in North America, Europe, and Asia Pacific | Medium term (2-4 years) |

| Stringent export controls on advanced night-vision modules | -0.3% | Export-dependent manufacturers targeting Middle East and Africa | Long term (≥ 4 years) |

| Emerging environmental compliance costs for optics recycling | -0.2% | European Union, with gradual adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Volatility of Rare-Earth Glass and Coatings

Lanthanum and cerium oxides swing wildly because 70% of output originates from China, where 2024 price bands fluctuated 50% inside one calendar year. Spot surges compress mid-tier margins by 3-5 percentage points, forcing brands to choose between pass-through surcharges and promotional discounts. The European Critical Raw Materials Act now requires 10% domestic sourcing by 2030, compelling EUR 2 billion (USD 2.26 billion) in plant investment that smaller optics houses struggle to finance. Without hedging contracts or vertical glass fabrication, these firms face cost structures that undercut their competitiveness in the sports optic market.

Increasing Preference for Smartphone Zoom as Substitute

Periscope lenses and computational photography entice casual spectators to skip dedicated binoculars. Apple’s iPhone 16 Pro Max delivers true 5× optical zoom, providing image reach comparable to 6× binoculars for the 1.3 billion installed user base. Samsung and Google have introduced 10× optical and AI-boosted super-resolution, which mimics 8× daylight magnification. Yet smartphones falter in stereoscopic depth, field-of-view breadth, and low-light detail, which are acute pain points for hunters judging range at dawn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rangefinders Accelerate on Multi-Function Integration

Rangefinders are projected to grow at a 5.67% CAGR, outpacing the overall sports optic market by 135 basis points as laser distance measurement shifts from novelty to necessity in golf and precision shooting. Binoculars still dominate the sports optic market with a 37.83% share in 2025, yet smartphone cannibalization tempers their unit trajectory as casual spectators increasingly rely on periscope phone lenses. Rifle scopes remain the second-largest revenue pillar, benefiting from U.S. hunting-license renewals that averaged 15.2 million per year through 2024. Telescopes post stable growth in the astronomy niche, while red-dot and holographic sights track the adoption of concealed carry.

Functional convergence blurs category lines such as Sony’s 4.5-millimeter LiDAR package now fits inside binocular barrels, enabling products such as Swarovski’s EL Range TA, which integrates rangefinding and ballistic calculation into a 32-ounce chassis. Garmin’s Approach Z30 overlays GPS course maps on laser data, turning single-purpose rangefinders into situational-awareness devices. As software layers thicken, firms that master firmware updates and mobile-app ecosystems will capture recurring revenue, reinforcing their position within the sports optic market.

By Game: Water Sports Propel Demand for Ruggedized Marine Optics

Water sports exhibit the fastest 5.76% CAGR as regatta rulebooks and offshore fishing tournaments codify standards for optical equipment. Steiner’s Navigator 7×50c delivers Sports-Auto-Focus that locks targets from 20 meters to infinity, meeting U.S. Coast Guard visibility mandates. Leica’s Noctivid maritime binoculars push 92% light transmission at dawn and dusk, a time window critical for spotting channel markers and marine wildlife.

Shooting sports, though large at 32.63% of 2025 revenue, grow more slowly as demographic shifts temper hunting license issuances in the United States and tighter gun laws in Western Europe dampen new shooter inflows. Golf finds itself in late-cycle adoption, where 68% of low-handicap players already own distance tools, leaving growth to replacement cycles. Cycling and motorsport optics add incremental units for spectators seeking on-course magnification but remain single-digit slices of the sports optic market.

Geography Analysis

North America commanded 38.73% of the sports optic market size in 2025 thanks to high discretionary income and entrenched hunting culture. Replacement cycles, not first-time adoption, now drive purchases, pushing brands toward feature-rich upgrades like thermal-fusion binoculars and first-focal-plane scopes. Binocular rental programs at U.S. national parks and concessionaires extend product reach to casual users but rarely translate into immediate sales.

Asia Pacific is poised for the quickest 5.55% CAGR through 2031, underpinned by China’s 520 million outdoor enthusiasts who increasingly purchase gear online via Tmall and JD.com, where Nikon and Bushnell hold a combined 42% channel share. Japan’s senior-heavy visitor base favors sub-600-gram devices with extended eye relief, reinforcing lightweight engineering trends. India adds volume via wildlife-sanctuary tourism, where tour operators bundle premium binocular rentals at USD 10-18 per day, nurturing trial among first-time users who later convert to ownership.

Europe constitutes a mature yet price-resilient region where brand heritage commands loyalty. Austrian and German firms protect share through proprietary glass melts and lifetime warranties. However, looming environmental take-back rules elevate end-of-life recycling costs, nudging manufacturers toward modular designs that simplify disassembly.

South America presents nascent but promising opportunities centered on Brazil’s Atlantic rain-forest ecotourism and Argentina’s fly-fishing circuits. The Middle East and Africa remain fragmented; South African safari lodges procure spotting scopes en masse, while United Arab Emirates shooting ranges import premium scopes to serve expatriate communities seeking authentic competition experiences.

Mordor Intelligence provides coverage of the sports optic market across other key regional markets. Detailed country-level analysis extends to China incorporating local coverage and market participation, as required.

Regulatory Landscape

Sports optics are subject to product-performance standards, eye-safety requirements, and trade compliance that varies by region and end use. ISO published ISO 14133:2025 (June 2025) with updated specifications for binoculars, monoculars, and spotting scopes, while ASTM expanded sports protection coverage via ASTM F0803-25 (September 2025) for selected sports eye protectors and updated ASTM F2879-22(2026) (June 17, 2026) for airsoft protective eyewear. In Europe, product-safety alignment continues under the PPE framework (EU 2016/425), with 2026 updates referencing harmonized standards, and EN 16830:2026 became mandatory from April 1, 2026 for sunglasses and sports goggles, increasing documentation and testing requirements for brands selling across EU channels.

Trade and cross-border controls also affect the cost and availability of higher-spec optical modules. In the United States, tariff uncertainty increased after the U.S. Court of International Trade ruled in May 2026 that 10% global tariffs under Section 122 of the Trade Act of 1974 are unlawful, which complicates landed-cost planning for import-heavy optics portfolios. China continues to issue and update safety-related standards affecting optical instruments, including GB 47498.2-2026 published April 30, 2026 for protection against light hazards for ophthalmic instruments, and these overlapping regimes raise compliance overhead for manufacturers that reuse shared components, coatings, and optical sub-assemblies across sports, outdoor, and adjacent optical categories.

Value Chain Analysis

The sports optic value chain begins with upstream materials and precision components, especially optical glass, coatings, prisms, mechanical housings, and, increasingly, electronics such as laser emitters, sensors, IMUs, and embedded compute for rangefinding, stabilization, and AR overlays. Suppliers of rare-earth-dependent glass inputs and coating chemistries drive cost volatility, while OEMs and ODMs differentiate through proprietary glass melts, coating stacks, assembly tolerances, and firmware that supports ballistic calculators, connectivity, and on-device UI. Brands also invest in software and update capabilities to sustain premiumization and to support integrated products such as rangefinding binoculars and GPS-enabled rangefinders.

Midstream manufacturing typically combines precision lens grinding or molding, prism fabrication, coating deposition, mechanical assembly, optical collimation, and environmental testing for waterproofing and shock resistance. Downstream, go-to-market spans specialty retailers and sporting goods chains, as well as direct-to-consumer channels that reduce 40-50% retail mark-ups, plus e-commerce marketplaces in Asia Pacific such as Tmall and JD.com that expand reach. After-sales services (warranties, repairs, firmware updates) and accessories (mounts, cases, tripods, phone adapters) increase lifetime value, while institutional and rental channels (tour operators, national parks, ranges) widen trial and brand visibility even when immediate unit conversion is limited.

Competitive Landscape

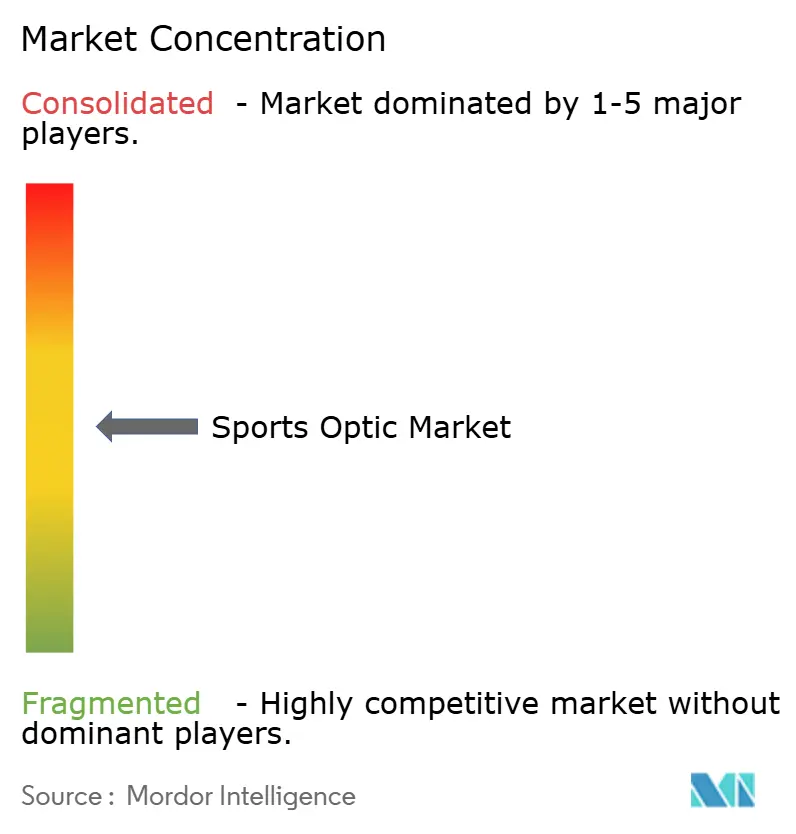

The sports optic market remains moderately fragmented, with the top 10 players holding roughly half of the combined revenue, resulting in a market concentration score of 6. Manufacturers differentiate through glass chemistry, coating stacks, and increasingly, embedded software. European stalwarts Swarovski, Zeiss, and Leica sustain price premiums of 200% or more by delivering optical clarity that outperforms Asian imports in low-light field tests. North American contenders Vortex and Bushnell lean on unconditional lifetime warranties and accessory ecosystems that raise switching costs. Direct-to-consumer insurgents such as Athlon and Maven bypass 40-50% retail mark-ups, enabling them to price Japanese ED-glass scopes 30-40% below incumbents while preserving margin.

Strategic moves skew toward M&A and sensor integration. Vista Outdoor’s USD 3.35 billion sale to MNC Capital folded Bushnell, Simmons, and Tasco into an entity primed to negotiate bulk rare-earth contracts, targeting manufacturing cost cuts of up to 12%. Revelst’s 2024 purchase of SVP Worldwide assets adds Vietnamese and Thai factories, reducing tariff exposure and rare-earth sourcing risk.

On the standards front, the European Telecommunications Standards Institute codified augmented-reality interface protocols in 2024, setting a platform layer that could shift value capture from hardware to software. Firms lacking firmware and mobile-app capabilities risk relegation to commodity status inside the sports optic market.

Sports Optic Industry Leaders

Nikon Corporation

Carl Zeiss AG

Bushnell Corporation (VISTA OUTDOOR)

TRIJICON inc.

SWAROVSKI OPTIK

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Entry and mid-tier optics are one area with room to move beyond smartphone zoom, particularly via ruggedization, low-light transmission, and stabilized viewing, while staying within accessible price points. Bushnell's April 2026 launch of its A-Series line for outdoor discovery underscores an effort to broaden the casual-user funnel with binoculars and monoculars closer to everyday outdoor use cases. That positioning can complement exposure from rental and on-site use at national parks and wildlife-tourism locations. Brands that combine these accessible products with stronger warranties, repair programs, and app-enabled feature upgrades can capture replacement-led demand without directly competing with flagship phone camera capabilities.

A second opportunity is connected and sensor-fused sports optics, where functionality convergence already shows up across laser rangefinding, GPS overlays, and embedded ballistic computation. Garmin's January 2026 integration of real-time weather data into the Approach Z30 rangefinder through a partnership with The Weather Company illustrates how service data layers can be pulled into handheld optics to improve decision support. It also points to recurring revenue through software features, while raising the need for manufacturers to strengthen firmware and companion-app ecosystems and to tighten component sourcing strategies to reduce exposure to rare-earth price swings and shifting tariff rules.

Recent Industry Developments

- May 2026: Nikon Corporation announced the development of the NIKKOR Z 120-300mm f/2.8 TC VR S lens for professional sports and general photography. The development supports Nikon's high-end sports imaging roadmap and strengthens its ecosystem pull-through among users who cross-shop dedicated optics and imaging gear.

- April 2026: Bushnell launched the A-Series outdoor optics line, adding new binoculars and monoculars positioned for outdoor discovery use cases. The launch broadens Bushnell's addressable customer base toward casual and first-time users, supporting volume growth where smartphone substitution pressure is more pronounced.

- September 2024: Swarovski Optik launched EL Range TA binoculars with integrated laser rangefinding and ballistic calculators, priced at USD 4,299. The product reinforced premium multifunction integration and raised competitive benchmarks for rangefinding binoculars, accelerating differentiation above the USD 1,000 tier.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The sports optic market is defined as the revenue generated from optical viewing and aiming devices used for sports and outdoor activities, including observation and distance measuring use cases, and tracked in value terms in USD across major regions.

Scope exclusions: This sizing excludes military procurement programs, industrial inspection optics, and medical or lab optical instruments that are not purchased for sports or recreation.

Segmentation Overview

- By Product Type

- Telescopes

- Binoculars

- Rifle Scopes

- Rangefinders

- Other Product Types

- By Games

- Shooting Sports

- Golf

- Water Sports

- Wheel Sports

- Other Games

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean fact base from outdoor participation indicators, firearm and hunting activity, and consumer durable spending because these signals influence how often sports optics are purchased and replaced. For that, we relied on public sources such as US Fish and Wildlife Service survey tables, National Shooting Sports Foundation releases, US International Trade Commission import and tariff data, UN Comtrade trade statistics, and selected peer reviewed optics and materials papers to understand product performance shifts that can lift average selling prices.

To connect demand with supply reality, we also reviewed company filings and investor presentations for revenue clues, product launches, and channel commentary, and then cross checked those points against reputed press coverage and association updates. Where public disclosures were thin, a paid subscription for company financials and news intelligence was used to spot directional changes like margin pressure, inventory cycles, and regional exposure. These desk sources are illustrative rather than exhaustive, and other public references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, distributors, specialty retailers, and category experts who track riflescopes, binoculars, rangefinders, and telescopes in day to day selling. Inputs were validated across APAC, EMEA, and the Americas so we could confirm adoption patterns by sport, typical price ladders, and how promotional seasons and regulation changes flow through to demand.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | APAC: 42% |

| Mid tier: 51% | Functional/Unit leaders: 34% | EMEA: 31% |

| Smaller Players: 15% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

The model is built using a top-down approach where participation and equipment ownership signals are translated into an addressable buyer pool, which is then adjusted by replacement cycles and product mix to estimate annual value by region. To keep totals realistic, we corroborated results with selective bottom-up approximations, such as sampling typical unit volumes by channel and applying observed average selling prices, followed by checks against distributor feedback.

Key inputs that shaped the math included participation trends in hunting, shooting sports, golf, and water activities, replacement and upgrade frequency for optics, the mix shift between entry and premium products, price movement tied to glass and electronics content (especially for rangefinders), and regional trade flow direction that can indicate supply availability. When primary inputs varied by geography, gaps were handled using conservative ranges and then narrowed through follow up until the assumptions stayed consistent with what respondents reported.

For forecasting, scenario analysis was applied around a central case so the outlook stayed tied to expected outdoor recreation demand, regulation stability, and pricing. The variables were rolled forward with simple, explainable trajectories, and the sensitivity of the total to mix and pricing was tested before finalizing the curve.

Data Validation & Update Cycle

Outputs are checked through multiple steps, starting with internal variance tests across regions, product types, and implied spending per participant, which helps catch inflated totals early. If the model shows a sharp swing that does not match known demand signals, we re-check the input series and, when needed, re-contact respondents to confirm what changed and whether it was temporary.

Before sign-off, another analyst reviews key assumptions, currency conversions, and year over year movements so the story matches the numbers. The report is refreshed annually, and interim updates are made when material events occur, such as trade restrictions, sudden demand shocks, or major channel disruptions. Right before delivery, a final pass is done so clients receive the latest updated view.

Mordor Intelligence's Sports Optic Market Size Measured Against Other Published Estimates

Published market values for sports optics can differ even when the topic looks identical, because each publisher sets its own product list, base year, and conversion choices. Differences also come from how demand is linked to participation, how pricing is moved forward, and how often assumptions are refreshed.

The main gap comes from whether estimates fold tactical and defense oriented optics into the same bucket, where Mordor Intelligence counts only sports and recreation demand and then validates sizing using participation based demand pools and channel feedback instead of relying mainly on broad category revenue splits.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.45 B (2026) | |

| Global Consultancy A | USD 2.18 B (2025) | Uses an earlier base year and a narrower product grouping, and the scope language does not clearly separate sports only demand from adjacent tactical use, which can shift the starting value and the implied upgrade cycle. |

| Industry Publisher B | USD 2.40 B (2025) | Leans on a broad category total with limited visibility on how ASP progression and regional currency timing are handled, which can smooth out mix effects between binoculars, riflescopes, and rangefinders. |

Overall, the spread across publishers is mostly explained by scope boundaries, base year choice, and how pricing and mix are carried through the forecast. By keeping the demand pool tied to sports participation and validating assumptions with channel level feedback, our estimate stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

How large is the sports optic market in 2026 and what growth rate is expected?

The sports optic market size reached USD 2.45 billion in 2026 and is forecast to grow at a 4.2% CAGR to USD 3.01 billion by 2031.

Which product category is growing fastest within sports optics?

Laser rangefinders are projected to expand at a 5.67% CAGR as integrated distance measurement becomes standard in golf and precision shooting.

Why are water sports optics gaining traction?

Regatta rules and offshore fishing tournaments mandate waterproof, compass-equipped binoculars, pushing water-sports demand at a 5.76% CAGR.

What regions will drive future sales of sports optics?

Asia Pacific is expected to post the quickest 5.55% CAGR, fueled by rising outdoor recreation in China, Japan, and India.

How are smartphones affecting entry-level binocular sales?

Periscope zoom modules in flagship phones satisfy casual spectators, trimming sub-USD 200 binocular demand while leaving premium segments intact.

Page last updated on: