Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

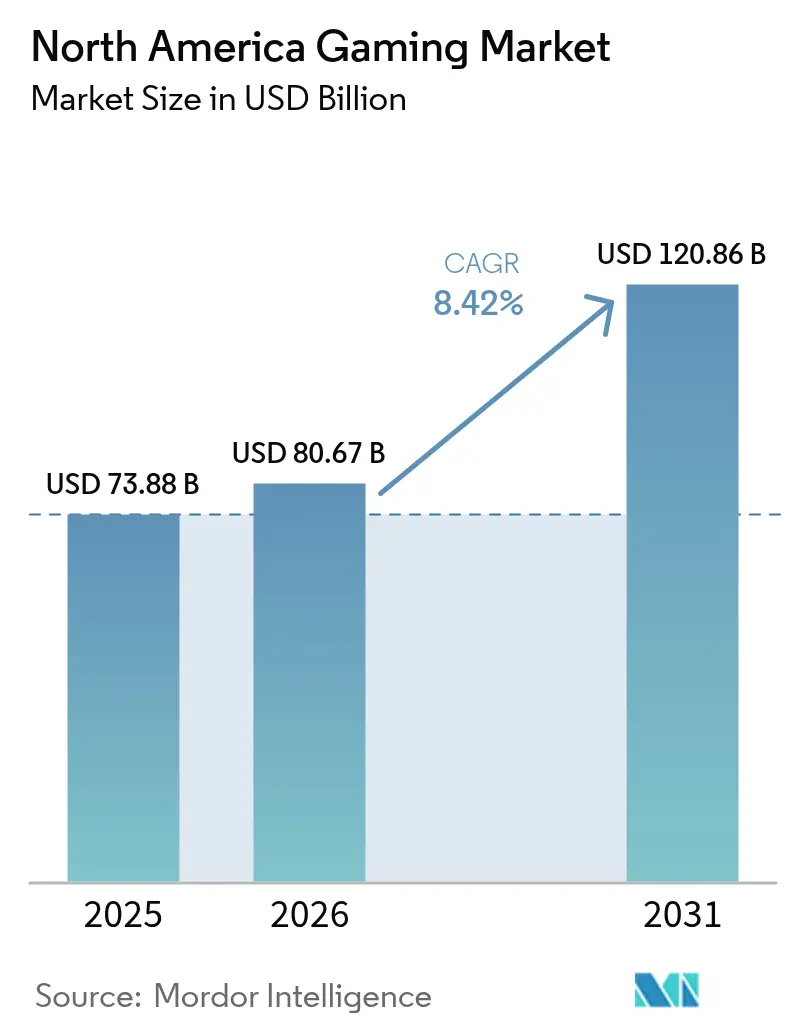

| Base Year Market Size (2025) | USD 73.88 Billion |

| Market Size (2026) | USD 80.67 Billion |

| Market Size (2031) | USD 120.86 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Gaming Market Analysis by Mordor Intelligence

The North America gaming market size is projected to expand from USD 73.88 billion in 2025 and USD 80.67 billion in 2026 to USD 120.86 billion by 2031, registering a CAGR of 8.42% between 2026 to 2031. A structural pivot toward hybrid monetization that layer’s advertising and subscriptions on top of evergreen live operations now underpins revenue growth, while mobile platforms capture discretionary spending that hardware upgrade cycles no longer fully address. United States publishers continue to dominate absolute revenue, yet Mexico’s mobile-first audience is scaling faster, propelled by 85% smartphone penetration and cloud streaming that eliminates console barriers. Platform boundaries are eroding as studios rely on cross-engine workflows to ship simultaneous console, PC, mobile and cloud launches, compressing development cycles but intensifying competition for attention. Investor focus has therefore shifted from unit sales to lifetime value as artificial-intelligence targeting and predictive retention models lift margins even when hardware volumes soften.

Key Report Takeaways

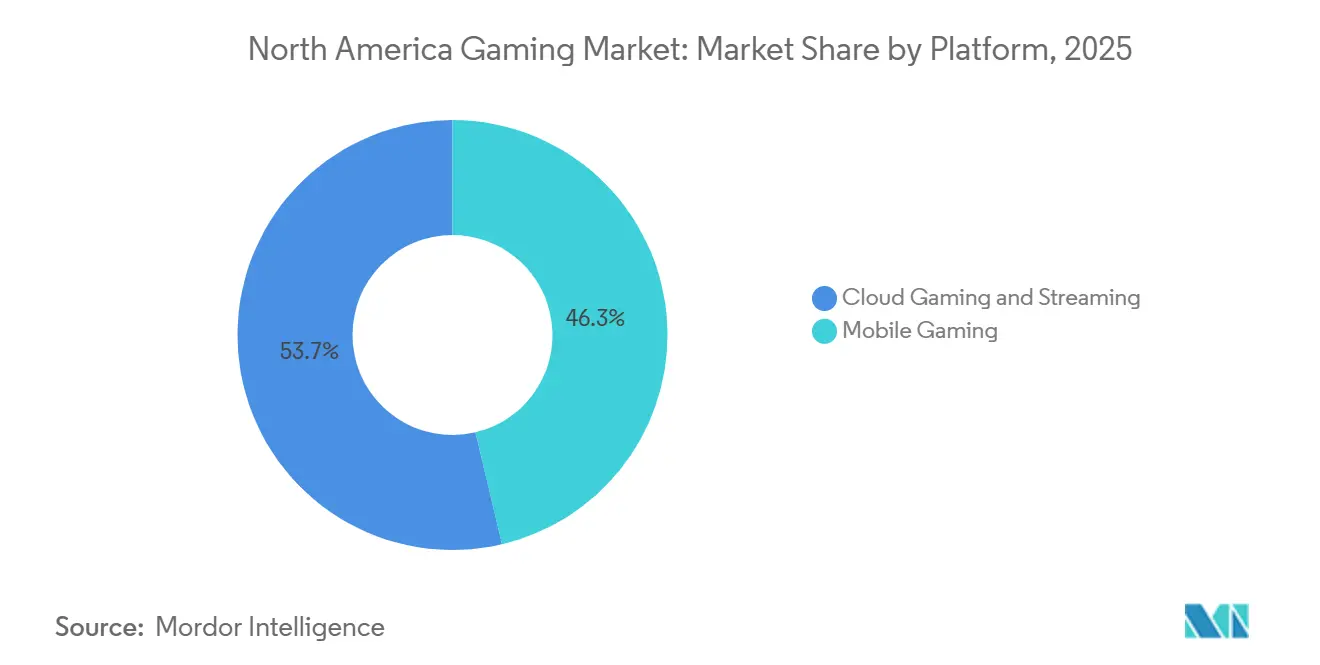

- By platform, mobile gaming led with 46.31% revenue share in 2025, while cloud gaming and streaming is advancing at an 8.91% CAGR through 2031.

- By revenue model, free-to-play and microtransaction formats accounted for 49.87% of 2025 revenue, whereas subscription services are forecast to grow at a 9.11% CAGR to 2031.

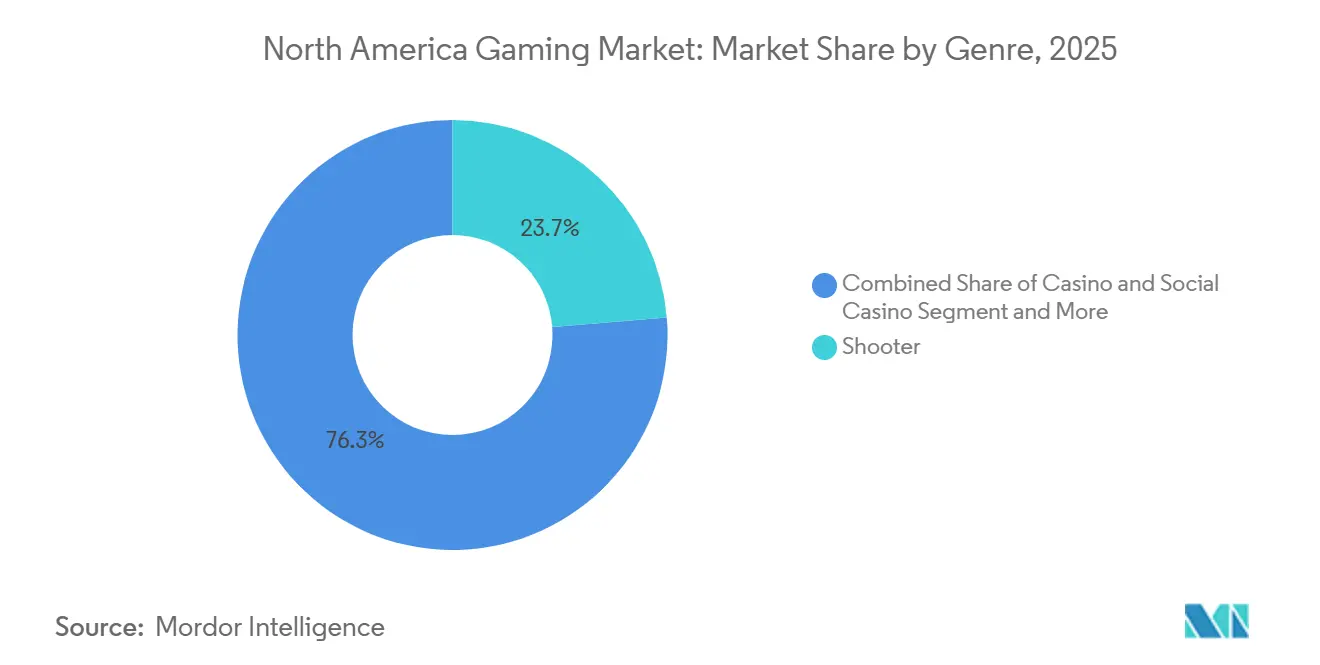

- By genre, shooter titles captured 23.71% share of the North America gaming market size in 2025, and casino and social casino games are projected to expand at an 8.77% CAGR between 2026-2031.

- By gamer type, casual gamers represented 41.26% of the mix in 2025 and social gamers are growing at an 8.79% CAGR to 2031.

- By geography, the United States commanded 82.42% North America gaming market share in 2025, while Mexico is forecast to post the fastest 9.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Gaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Mobile-First Casual Gaming Spend | +1.80% | United States, Mexico, Canada | Medium term (2-4 years) |

| Subscription Services Gaining ARPU via Price-Tier Stacking | +1.50% | United States, Canada | Short term (≤ 2 years) |

| Cross-Platform Engine and Live-Ops Tool Adoption Lowering Development Cycles | +1.20% | United States, Canada | Medium term (2-4 years) |

| Esports Sponsorship Inflows and Media-Rights Escalation | +0.90% | United States, Canada | Long term (≥ 4 years) |

| Cloud/Edge Infrastructure Cuts Hardware Barriers for AAA Experiences | +0.80% | United States, Canada, Mexico | Long term (≥ 4 years) |

| AI-Driven User-Acquisition and Retention Modelling Boosts LTV | +0.70% | United States, Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Mobile-First Casual Gaming Spend

Mobile platforms captured 46.31% of 2025 regional revenue, yet in-app purchase values on United States iOS devices fell 3.47% year-over-year, while advertising income jumped 26.7%, proving that reach now trumps microtransaction depth.[1]Sensor Tower, “Mobile Game Market Insights 2024-2025,” sensortower.com Mexico mirrors this pattern, with 78 million gamers delivering USD 2.2 billion in 2024 value at a 9.8% growth clip thanks to mobile usage exceeding 73% of players.[2]Deloitte, “Digital Media Trends: Gaming and Esports 2025,” www2.deloitte.com Publishers therefore treat lightweight titles as acquisition funnels, inserting rewarded video and subscription upsells that lifted the top 100 United States mobile games’ direct-to-consumer receipts 46% year-over-year.

Subscription Services Gaining ARPU via Price-Tier Stacking

Subscription revenue is tracking a 9.11% CAGR as operators add ad-supported starter tiers beneath premium plans. Xbox Game Pass surpassed 35 million users by mid-2025, and a July 2024 price hike showed no material churn, pushing average revenue per user higher.[3]Microsoft Corporation, “Fiscal Year 2025 Earnings Report,” microsoft.com Hybrid monetization now captures 61.7% of gaming spend because it simultaneously monetizes committed enthusiasts and price-sensitive casual players.[4]Bain and Company, “Gaming Industry Monetization Trends 2025,” bain.com North America’s disposable-income profile supports premium tiers, while ad-subsidized options extend reach into Mexico’s fast-growing mobile cohort.

Cross-Platform Engine and Live-Ops Tool Adoption Lowering Development Cycles

Multiplatform releases expanded 40% from 2021-2024 as Unity and Unreal abstracted hardware differences, letting small studios grow cross-platform output 71%. Cloud-based live-operations suites such as PlayFab push balance tweaks or seasonal events server-side, reducing patch lead times and fuelling rapid content iteration. The democratization of AAA tools enables niche creators to challenge incumbents, yet also compresses differentiation as photoreal assets and analytics become table stakes.

Esports Sponsorship Inflows and Media-Rights Escalation

Traditional sports deals are lifting valuation benchmarks: the National Basketball Association’s 11-year, USD 76 billion package, the National Hockey League’s USD 11 billion Canadian rights, and the National Football League’s USD 111 billion renewal anchor sponsor expectations. Casino and gaming backers already produced USD 387.6 million in measured social value across United States leagues. Esports franchises now negotiate multi-year agreements that transform leagues from marketing loss leaders into stand-alone profit nodes, provided viewership momentum sustains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hardware Refresh Slump Post-COVID and Macro Headwinds | -1.20% | United States, Canada | Short term (≤ 2 years) |

| Rising Acquisition Costs and Ad-Signal Loss on Mobile | -0.90% | United States, Canada, Mexico | Medium term (2-4 years) |

| Regulatory Scrutiny on Loot-Boxes and Data Privacy | -0.60% | United States, Canada | Long term (≥ 4 years) |

| Talent Layoffs Eroding Institutional Knowledge and Delaying Releases | -0.50% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hardware Refresh Slump Post-COVID and Macro Headwinds

PlayStation 5 shipments fell 27.3% in 2024 to 15.8 million units, and Xbox hardware revenue slipped 29% in fiscal Q2 2025 as inflation tempered premium hardware demand. A lengthening console cycle caps the addressable audience for USD 70 titles, pressuring publishers to support legacy devices and cloud outlets, which in turn dilutes the visual leap that once justified new silicon.

Rising Acquisition Costs and Ad-Signal Loss on Mobile

Apple’s App Tracking Transparency and Google’s Privacy Sandbox curtailed third-party IDs, driving the top 1% of iOS winning bids for high-value gamers up roughly 140% in 2024. Incumbents with sizable first-party datasets can still train accurate look-alike models, but independent studios face margin squeeze as customer acquisition outpaces lifetime value. Consolidation accelerates as smaller teams join larger ecosystems to regain targeting efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Mobile Leads, Cloud Accelerates

Mobile retained 46.31% share of overall 2025 revenue, yet the North America gaming market size narrative is shifting as advertising replaced shrinking iOS in-app purchase spend, which dipped 3.47% year-over-year. Console performance softened alongside a 27.3% PlayStation 5-unit decline and a 29% Xbox hardware revenue drop, signalling install-base stagnation. Cloud gaming, projected to jump from USD 1.4 billion in 2025 to USD 18.3 billion by 2030, delivers AAA experiences without USD 500 consoles, helping Mexico’s fast-rising cohort and lifting regional growth.

Cross-platform engines let studios amortize assets across console, PC, mobile and cloud, but this convergence increases QA complexity and platform-holder revenue-share exposure. Multiplatform launches rose 40% between 2021-2024; small teams saw a 71% surge, proving that tooling democratization undercuts the moat once enjoyed by major publishers. The North America gaming market now rewards agile studios that optimize UI and balance for heterogeneous screens while leveraging first-party storefronts to escape 30% mobile tariffs.

By Revenue Model: Subscriptions Capture Wallet Share

Hybrid ecosystems blending subscriptions, ads and microtransactions now generate 61.7% of total spend, dwarfing one-off sales. The North America gaming market share for free-to-play and microtransactions sat at 49.87% in 2025, but subscriptions are the fastest component with a 9.11% CAGR outlook. Game Pass’s 35 million base validates multilevel pricing, while a 2024 fee hike confirmed pricing power.

High-spending whales still skew economics 0.02% of global installs created 20% of worldwide gaming revenue in 2025 yet ad-supported starter tiers broaden funnels before premium upsells. Direct-to-consumer storefronts grew 46% year-over-year as publishers chase higher takes versus platform fees. Over time, the North America gaming industry expects revenue to cluster around subscription bundles enriched by cosmetic microtransactions that stretch spending arcs well beyond launch month.

By Genre: Casino Mechanics Go Mainstream

Shooter franchises retained 23.71% 2025 share, buoyed by Call of Duty crossing USD 1 billion in its first month after the October 2024 Black Ops 6 launch. Casino and social casino titles, however, own the fastest 8.77% CAGR to 2031, with United States social casino revenue hitting USD 6.6 billion in 2024.

Sports games leverage traditional media rights, whose ballooning values spill into in-game sponsorship fees. Meanwhile, puzzle and casual apps embed gacha and loot-box loops, blending into casino dynamics and inviting heightened scrutiny. Regulatory momentum, led by Washington State’s 2025 age-verification law, could temper aggressive random-reward design.

By Gamer Type: Social Interaction Extends Lifecycles

Casual gamers formed 41.26% of the player mix in 2025, yet social gamers are expanding fastest at 8.79% CAGR thanks to sandbox universes such as Roblox, which logged 88.9 million daily actives and USD 919 million Q3 2024 revenue. Competitive and esports players, though a minority, deliver premium lifetime values through cosmetics and season passes that signal rank.

AI-based personalization engines adopted by 62% of studios tailor events and difficulty in real time, constraining churn. The North America gaming market size for community-driven platforms therefore grows disproportionately because network effects foster self-sustaining engagement as user-generated content refreshes catalogues without heavy publisher capex.

Geography Analysis

The United States contributed 82.42% of 2025 revenue, supported by entrenched console ecosystems and subscription penetration topping 35 million Game Pass accounts. Yet iOS in-app purchase volumes slipped 3.47% year-over-year while ad receipts grew 26.7%, compelling publishers to pivot toward hybrid monetization. Added pressure stems from state-by-state regulation such as Washington’s 2025 loot-box age checks, which fragment compliance regimes.

Canada mirrors United States behaviour but at smaller scale; its USD 11 billion, 12-year National Hockey League rights agreement elevates sponsorship pricing in sports and esports tie-ins. Cloud streaming uptake is notable because broadband penetration outpaces console replacement, enabling AAA play on mid-tier PCs and tablets.

Mexico represents the high-growth outlier with a 9.23% CAGR forecast as 85% smartphone penetration and 78 million gamers fuel a USD 2.2 billion 2024 base. Cloud services bypass USD 500 console barriers, and publishers localize content plus alt-cash payments to capture this mobile-first audience. Over the horizon, rising Mexican spend will slowly dilute United States dominance, though per-capita outlays remain wider north of the border.

Competitive Landscape

The top 10 publishers control roughly 60-70% of console and PC receipts, yielding a moderately concentrated field where scale in first-party data and intellectual property confers edge. Microsoft’s USD 68.7 billion Activision Blizzard purchase in 2023 folded Call of Duty, World of Warcraft and Candy Crush into a unified Game Pass funnel that exploits Azure cloud reach. Sony counters with PlayStation Plus catalogue depth but faces hardware softness that constrains exclusive sales leverage.

Mobile remains fragmented, yet escalating user-acquisition costs push independents toward partnerships or acquisition. AI adoption, now present in 62% of studios, is the tactical differentiator: deeper data lakes enable superior churn models, widening the retention gap versus smaller peers.

User-generated ecosystems such as Roblox and Fortnite Creative divert both developer talent and audience time, encouraging incumbents to launch creator tooling and revenue splits to keep players inside proprietary worlds. White-space still exists in narrative-driven indies and social simulation niches, especially for localized Spanish content targeting Mexico’s accelerating base.

North America Gaming Industry Leaders

Activision Blizzard, Inc.

Electronic Arts Inc.

Microsoft Corporation

Sony Interactive Entertainment LLC

Nintendo Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: OverActive Media agreed to acquire Spanish brands KOI and Movistar Riders in an all-stock deal worth CAD 11.7 million to expand its EMEA esports footprint.

- March 2025: Inspired Entertainment’s Interactive revenue climbed 45% year over year to USD 11.6 million, buoyed by North American launches such as MGM Bonus City in Michigan.

- February 2025: Relo Metrics partnered with Meltwater to merge AI sponsorship analytics with media-intelligence datasets for sports and entertainment rights holders.

- February 2025: Unity posted Q4 2024 revenue of USD 456.84 million (-25% YoY) yet saw 38% of creators upgrade to Unity 6 and 15% growth in subscription income, spotlighting traction for its Vector AI ad stack.

- February 2025: Nintendo cut FY 2025 hardware guidance to 11 million units after a 27.7% Q3 revenue dip to JPY 423.919 billion (USD 2.787 billion).

- January 2025: Microsoft announced 39% year-over-year gaming revenue growth, with Xbox content and services up 50% and hardware down 13%.

North America Gaming Market Report Scope

The North America Gaming Market Report is Segmented by Platform (Console Gaming, PC Gaming, Mobile Gaming, Cloud Gaming and Streaming), Revenue Model (Premium, Free-to-Play/Micro-Transactions, Subscription Services, Advertising and In-Game Purchases), Genre (Shooter, Sports, Role-Playing/Adventure, Strategy, Puzzle and Casual, Casino and Social Casino), Gamer Type (Casual Gamers, Competitive/Esports Gamers, Hardcore/Core Gamers, Social Gamers), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Platform

| Console Gaming |

| PC Gaming |

| Mobile Gaming |

| Cloud Gaming and Streaming |

By Revenue Model

| Premium (Full-Priced) |

| Free-to-Play/Micro-transactions |

| Subscription Services |

| Advertising and In-Game Purchases |

By Genre

| Shooter |

| Sports |

| Role-Playing/Adventure |

| Strategy |

| Puzzle and Casual |

| Casino and Social Casino |

By Gamer Type

| Casual Gamers |

| Competitive/Esports Gamers |

| Hardcore/Core Gamers |

| Social Gamers |

By Country

| United States |

| Canada |

| Mexico |

| By Platform | Console Gaming |

| PC Gaming | |

| Mobile Gaming | |

| Cloud Gaming and Streaming | |

| By Revenue Model | Premium (Full-Priced) |

| Free-to-Play/Micro-transactions | |

| Subscription Services | |

| Advertising and In-Game Purchases | |

| By Genre | Shooter |

| Sports | |

| Role-Playing/Adventure | |

| Strategy | |

| Puzzle and Casual | |

| Casino and Social Casino | |

| By Gamer Type | Casual Gamers |

| Competitive/Esports Gamers | |

| Hardcore/Core Gamers | |

| Social Gamers | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What drives revenue growth across North America gaming?

Hybrid monetization that layers subscriptions and advertising on top of live-operations lifts lifetime value while mobile and cloud access keep new players joining.

Which platform is growing fastest?

Cloud gaming and streaming posts the highest 8.91% projected CAGR to 2031 because edge computing reduces latency and removes console cost barriers.

How large is Mexico's role in regional expansion?

Mexico is forecast to deliver a 9.23% CAGR through 2031, the strongest in the region, as 85% smartphone penetration and cloud streaming open AAA experiences to mobile-first players.

Why are subscription programs critical for publishers?

Services such as Game Pass surpassed 35 million users and survived 2024 price increases, proving that tiered subscriptions raise average revenue per user without sparking mass churn.

What regulatory issues are most pressing now?

Loot-box transparency and mandatory age verification, led by Washington State legislation and a Federal Trade Commission inquiry, are reshaping compliance for monetization design.

How does artificial intelligence influence competitive advantage?

Sixty-two percent of studios already apply AI for predictive churn modeling and personalized content, letting data-rich publishers cut acquisition costs and stretch player lifecycles.

Page last updated on: