Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Wrist Dive Computer Market is Segmented by Display Type (AMOLED, MIP, E-Ink, Hybrid Dual-Layer), Connectivity (Stand-Alone, Bluetooth/Smartphone-synced, Air-Integrated), End-User (Recreational/Civilian, Commercial and Military, Technical/Professional), Distribution Channel (Online, Offline), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

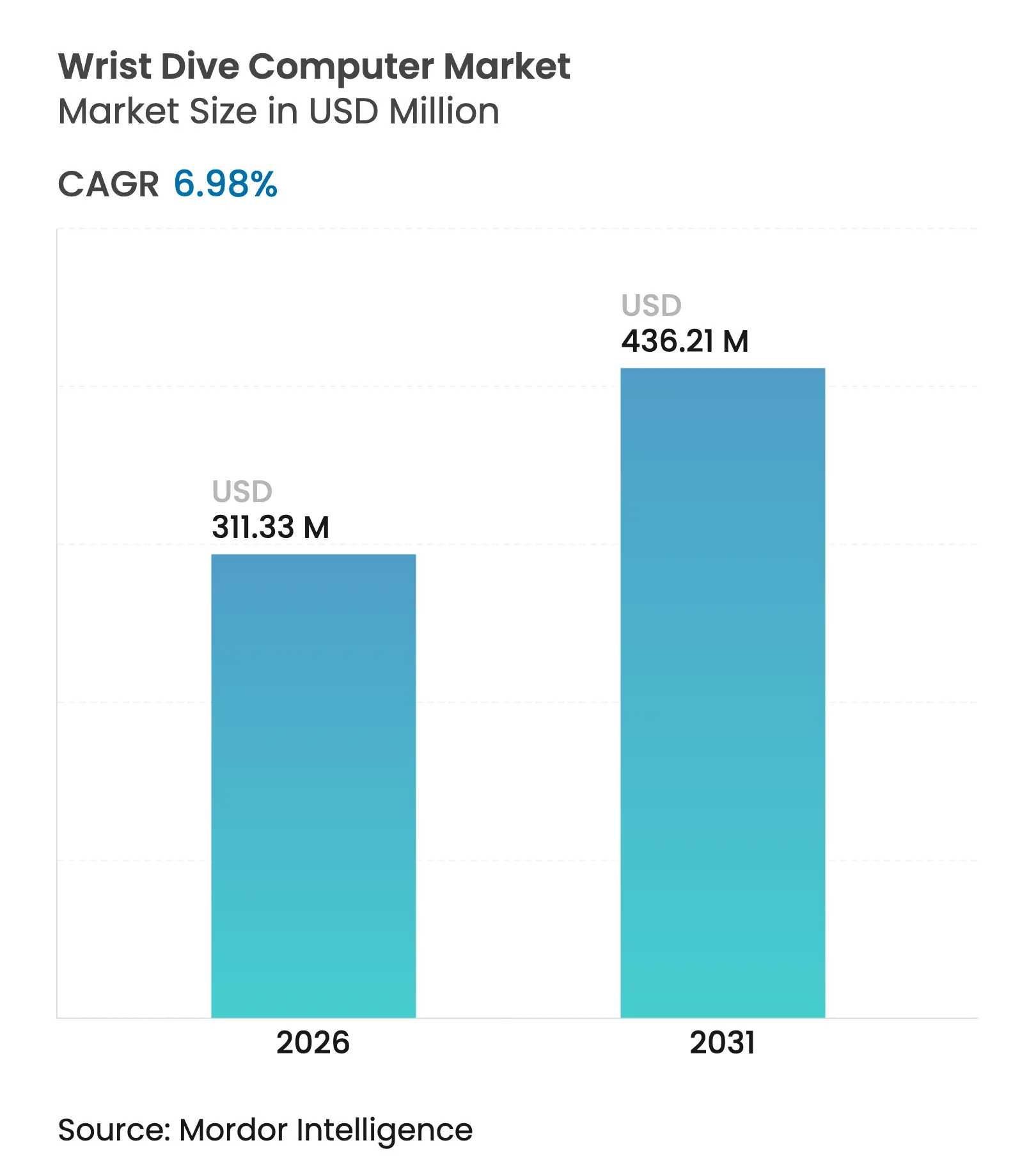

| Market Size (2026) | USD 311.33 Million |

| Market Size (2031) | USD 436.21 Million |

| Growth Rate (2026 - 2031) | 6.98 % CAGR |

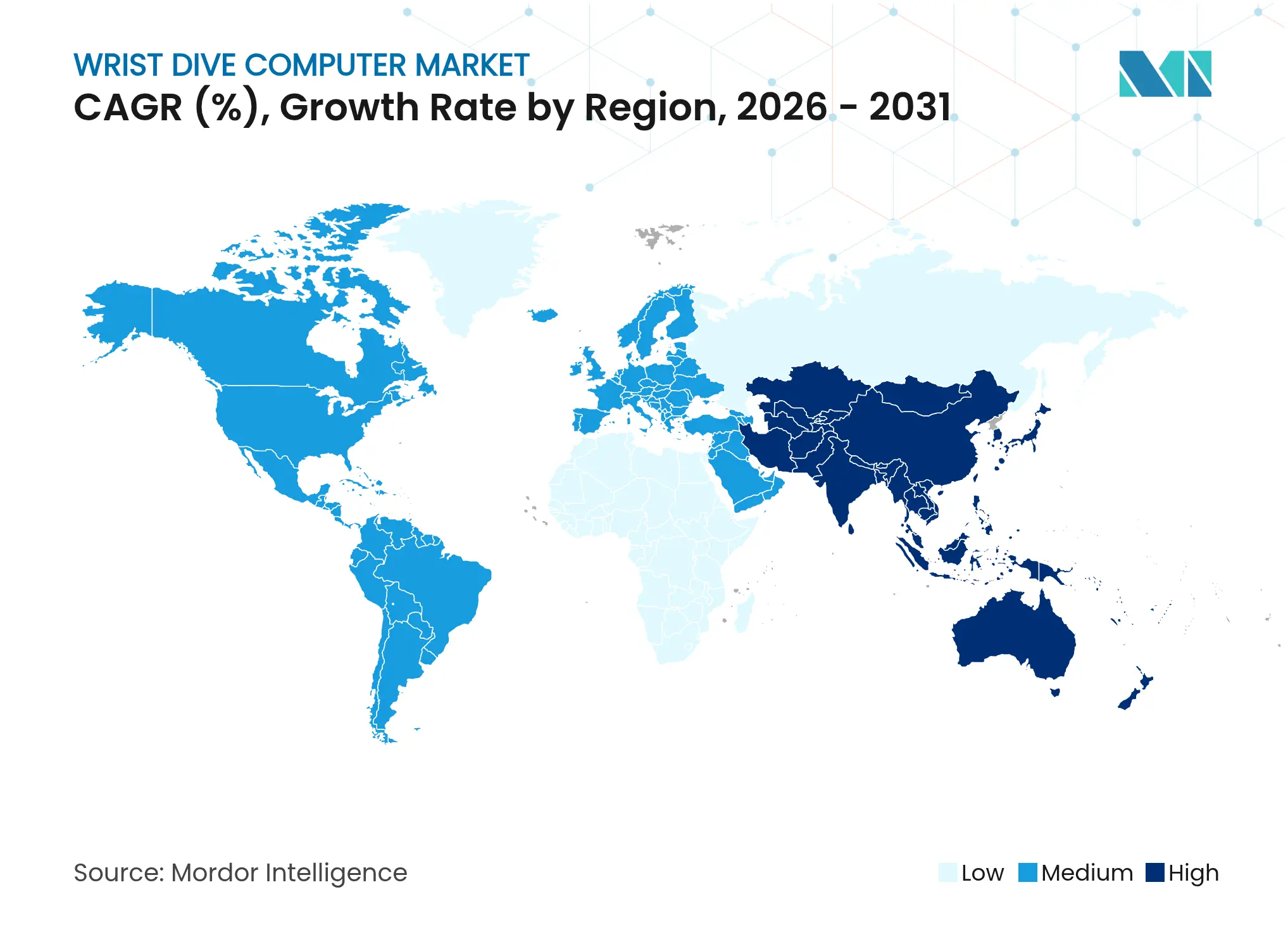

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The wrist dive computer market size in 2026 is estimated at USD 311.33 million, growing from 2025 value of USD 291.02 million with 2031 projections showing USD 436.21 million, growing at 6.98% CAGR over 2026-2031. Rapid growth springs from rising recreational diving participation, accelerated smartwatch convergence, and continuous advances in display, sensor, and connectivity technologies. Manufacturers now differentiate mainly on AMOLED visibility, air-integration accuracy, and cloud-based analytics that enrich post-dive safety reviews. Consumer-electronics giants such as Apple have lowered entry barriers and shifted buyer expectations toward multi-sport wearables that double as full-featured dive instruments, compelling legacy brands to recalibrate product roadmaps. Meanwhile, supply-chain recovery after the 2023 semiconductor crunch lets vendors shift capital from component procurement to firmware innovation, refining decompression algorithms and predictive gas-consumption models.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rise in recreational diving and

water-sports tourism

Rise in recreational diving and

water-sports tourism

| +1.8% | Asia-Pacific, Caribbean, Global spillover | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:Asia-Pacific, Caribbean, Global spillover |

Impact Timeline

:

Medium term (2-4 years)

|

Shift from console gauges to compact

wrist computers

Shift from console gauges to compact

wrist computers

| +1.2% | North America, Europe, Developed Asia-Pacific | Short term (≤ 2 years) | |||

Increasing adoption of

air-integrated and wireless transmitters

Increasing adoption of

air-integrated and wireless transmitters

| +1.5% | North America, Europe, Global | Medium term (2-4 years) | |||

Growing popularity of technical and

rebreather diving courses

Growing popularity of technical and

rebreather diving courses

| +0.9% | North America, Europe, Select Asia-Pacific | Long term (≥ 4 years) | |||

Rapid smartwatch convergence

Rapid smartwatch convergence

| +1.1% | Developed markets worldwide | Short term (≤ 2 years) | |||

Expansion of dive-safety data

analytics and cloud logbooks

Expansion of dive-safety data

analytics and cloud logbooks

| +0.7% | Connected markets worldwide | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rise in recreational diving and water-sports tourism

Global scuba activity reached 33.1 million dives in 2024, with 62% logged in developing nations that are upgrading marina facilities and hyperbaric chambers to court adventure travelers.[1]Hannah J. Brooks et al., “Economic Impact of Marine Protected Areas on Tourism,” Scientific Reports, nature.com Marine-protected areas are also unlocking USD 2 billion in additional tourism receipts, prompting local operators to invest in rental fleets that familiarize novice visitors with premium wrist computers before ownership consideration. Manufacturers benefit from this exposure effect, as divers often transition to air-integrated devices once certified and financially able. Indonesia’s liveaboard sector illustrates the pattern: rental inventories use mid-range units that showcase intuitive menus, creating future demand for feature-rich personal purchases. The virtuous cycle widens the overall wrist dive computer market by grooming a pipeline of equipment-savvy buyers.

Shift from console gauges to compact wrist computers

Replacing hose-linked consoles with palm-sized computers reduces task loading and improves streamlining, especially in currents common to Caribbean drift sites. Affordable models such as the Shearwater Peregrine combine a 2.2-inch LCD and 30-hour battery at USD 575 while integrating Bühlmann GF algorithms that previously required desktop planning.[2]Shearwater Research, “Peregrine Dive Computer Specifications,” shearwater.com Sapphire faces and 120 m depth ratings now eclipse the durability of traditional brass-and-glass consoles. Technical divers gain additional upside: up to five gas transmitters simplify bailout management during multi-stage decompression, a feature highlighted in the Mares Quad Ci release. These advantages are accelerating global console-to-wrist migration.

Increasing adoption of air-integrated and wireless transmitters

Modern air-integration moves beyond SPG replacement to algorithmic gas forecasting that accounts for diver respiratory rate. Shearwater’s Swift Transmitter, launched March 2024, introduced collision-avoidance signaling so multiple units can coexist on a single wreck dive without data drop-outs.[3]Shearwater Research, “Swift Transmitter Technical Sheet,” shearwater.com Eliminating HP hoses cuts drag and snag risk during cave penetrations, while allowing instructors to monitor student gas reserves remotely through paired consoles. The reliability gains have led leading training agencies to accept air-integrated computers as primary gauges in advanced trimix curricula, a milestone that quickens adoption within the wrist dive computer market.

Growing popularity of technical and rebreather diving courses

Trimix, CCR and extended-range certifications posted double-digit enrollment growth in 2024, expanding the addressable premium-device base. Products such as the heads-up Shearwater NERD 2 (USD 1,775) overlay PO₂ and CNS exposure on a rebreather mouthpiece so divers no longer lower their gaze during deco-critical moments. Semi-closed rebreathers are expected to filter into advanced recreational syllabi, extending multi-gas requirements to a broader user tier and lifting ASPs within the wrist dive computer market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High market concentration and

premium pricing pressures

High market concentration and

premium pricing pressures

| -1.3% | Global, sharper in price-sensitive regions | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-1.3%

|

Geographic Relevance

:

Global, sharper in price-sensitive

regions

|

Impact Timeline

:

Medium term (2-4 years)

|

Supply-chain exposure to specialty

pressure sensors and chips

Supply-chain exposure to specialty

pressure sensors and chips

| -0.8% | Asia-Pacific manufacturing hubs | Short term (≤ 2 years) | |||

Equipment rental culture in emerging

dive destinations

Equipment rental culture in emerging

dive destinations

| -0.9% | Southeast Asia, Caribbean | Long term (≥ 4 years) | |||

Stricter e-waste regulations raising

end-of-life cost

Stricter e-waste regulations raising

end-of-life cost

| -0.6% | Europe, North America, Developed Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High market concentration and premium pricing pressures

A handful of legacy brands control algorithm IP and dealer networks, permitting MSRP ranges of USD 1,000–2,000 for flagship units. Devices like the Shearwater Teric list at USD 1,195, pricing out many newly certified divers. Apple’s USD 800 Watch Ultra illustrates how cross-subsidized consumer-electronics players can undercut incumbents while matching core functionality, forcing downward price pressure across the wrist dive computer market. The margin squeeze complicates RandD funding for smaller specialists.

Supply-chain exposure to specialty pressure sensors and chips

Although post-2023 silicon availability has improved, niche piezo-resistive pressure sensors still come from a handful of Taiwanese fabs. Any geopolitical or logistics disruption could delay production cycles by quarters, as seen during the 2021 shortages that deferred multiple launch roadmaps. Brands are therefore dual-sourcing components, adding overhead that trickles into ASPs.

By Display Type: AMOLED performance rewrites on-hand visibility

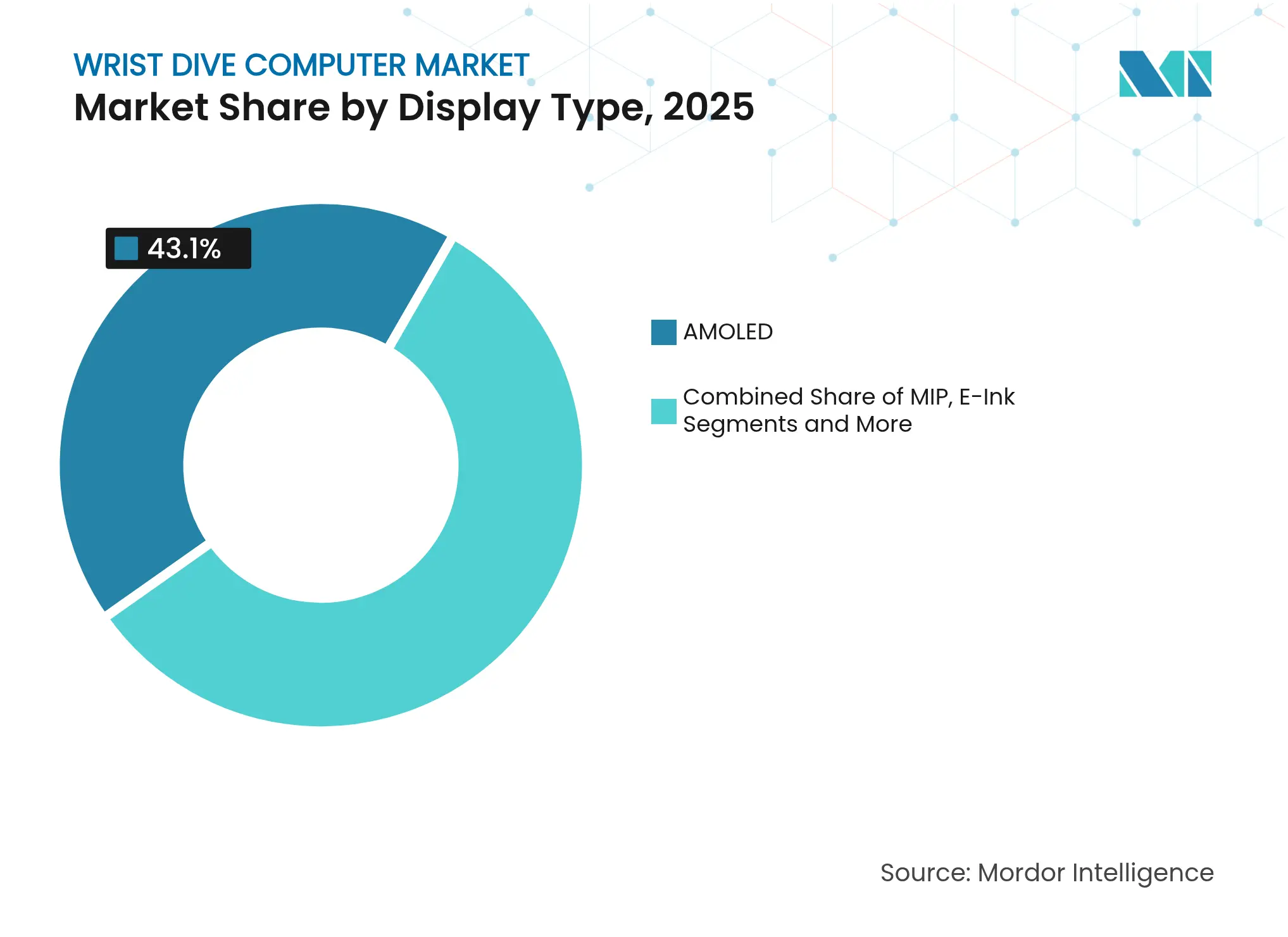

The AMOLED segment generated 43.10% of 2025 revenue and is projected to post a 8.95% CAGR, lifting its share of the wrist dive computer market size through 2031. Superior contrast, intrinsic illumination, and improved battery efficiency jointly overcome the readability gaps that long challenged LCD models at depth.

Manufacturers harness smartphone supply chains to secure thinner panels and vibrant 1000-nit peaks, evident in Garmin’s Descent G2 priced at GBP 589.99 (USD 662 million). MIP and e-ink retain niches for expedition divers chasing multi-week autonomy, but hybrid dual-layer experiments remain cost-weighted for now. As yields climb and price gaps narrow, AMOLED will cement leadership, pushing suppliers of legacy displays toward value tiers within the wrist dive computer market.

Note: Segment shares of all individual segments available upon report purchase

By Connectivity: Wireless data shapes post-dive coaching

Bluetooth-enabled units dominated 45.25% of 2025 sales, and air-integrated transmitters are expanding at 9.32% CAGR, signifying rising appetite for real-time gas analytics within the wrist dive computer market size. Instant log uploads satisfy certification agencies that now accept cloud portfolios in lieu of paper books.

Shearwater’s Swift collision-avoidance protocol permits up to five parallel transmitters, making multi-stage dives safer. Entry-level stand-alone models persist for budget travelers, but once divers cross 50-dive experience thresholds they typically migrate to transmitter bundles for consolidated telemetry. Collision-safe radio stacks therefore represent a defensible moat for premium SKUs in the wrist dive computer market.

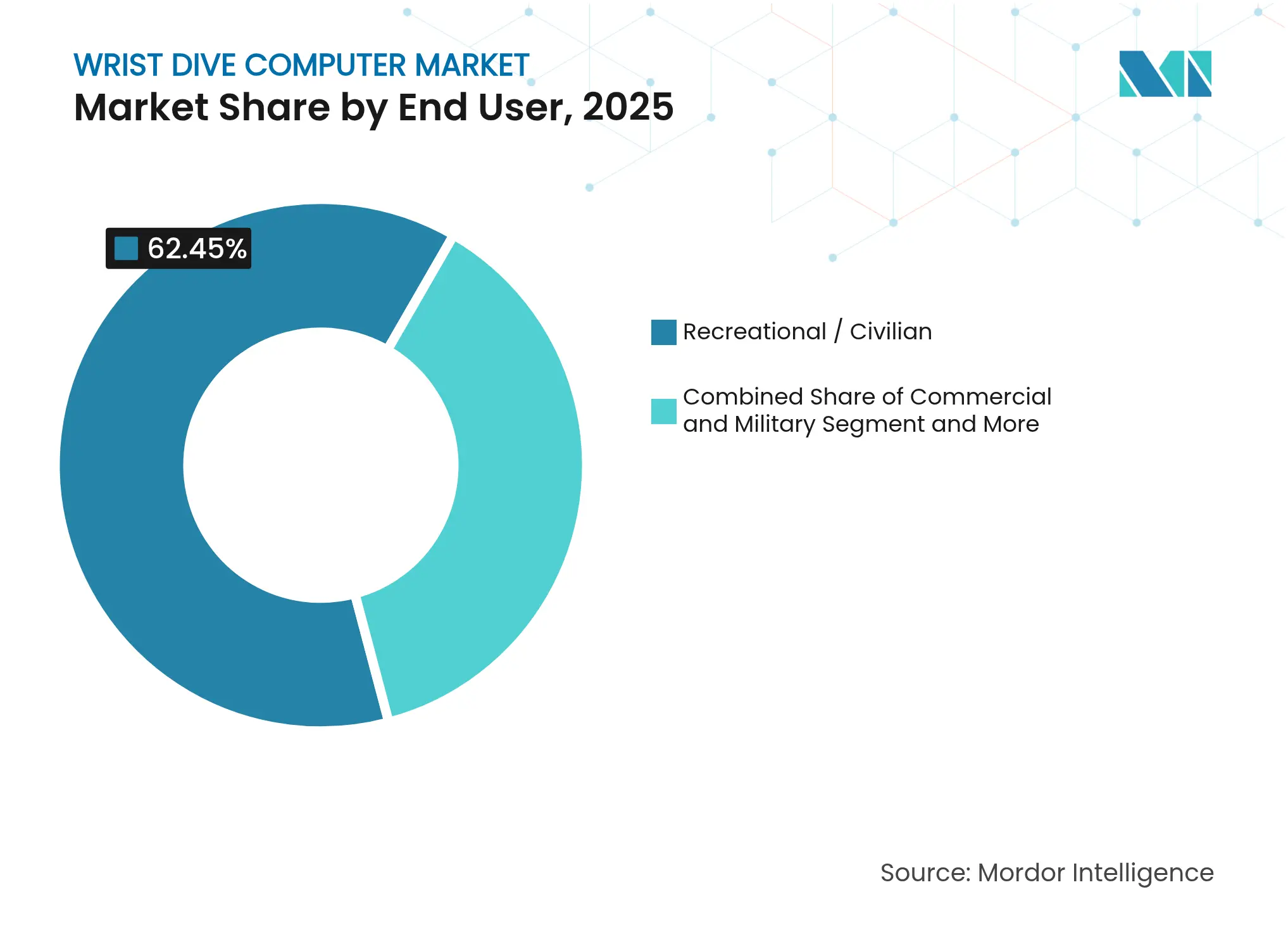

By End User: Technical demand fuels top-line price resilience

Recreational divers captured 62.45% of 2025 unit demand, yet technical/professional categories are outpacing at 8.54% CAGR and commanding higher ASPs, thereby enlarging revenue contribution to the wrist dive computer market share. Advanced curricula require multi-gas control, helium-mix planning, and redundant displays.

Heads-up solutions such as NERD 2 permit continuous PO₂ oversight during deco stops, a safety upgrade revered in rebreather circles. Commercial and military divers drive bespoke variants integrating surface telemetry, but volume remains low. The technical segment’s affinity for frequent firmware upgrades and accessory transmitters secures a recurring revenue flywheel for vendors inside the wrist dive computer market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: E-commerce scales availability, shops pivot to service

Offline stores accounted for 56.60% of 2025 turnover, but digital retail is growing 8.16% annually as shoppers compare global prices before resort departures. The trend echoes broader sporting-goods migration yet retains unique nuances: pre-trip dry fits and pressure-test services still favor brick-and-mortar convenience.

Dive centers are repurposing retail footprints into demo pools, sensor calibration stations, and instructor clinics that build loyalty beyond product margin. Hybrid buy-online-pick-up-in-store models reduce inventory risk while preserving expertise advantages. Brands responding with unified serial-number activation portals now foster omnichannel data visibility to reinforce warranty adherence in the wrist dive computer market.

North America commanded 32.60% of 2025 revenue owing to entrenched certification networks, cold-water tech communities, and affluent consumer bases that tolerate USD 1,000+ ticketed gear. United States Gulf and Pacific coasts anchor demand through charter operations, while Canada’s ice-diving specialism favors high-contrast AMOLED legibility at low ambient light. Mexico’s Riviera Maya, with its cenote circuit, stimulates rental fleets that convert to personal sales when divers repatriate and seek customizable firmware.

Asia-Pacific leads growth at a 7.78% CAGR, underpinned by Indonesia, Philippines, and Maldives tourism corridors that register surging open-water graduations. China’s coastal cities now host PADI five-star facilities catering to a growing middle class that embraces wearable tech, yet equipment tariffs still modulate adoption velocity. Japan and Australia maintain sophisticated mixed-gas communities that adopt multi-transmitter configurations early, reinforcing the premium tier of the wrist dive computer market.

Market Concentration

The market remains moderately concentrated; the top five players hold roughly 65% combined revenue, a structure that rewards scale while allowing room for specialist upstarts. Garmin, Suunto, and Shearwater Research anchor the premium tier through proprietary decompression models, AMOLED leadership, and extensive transmitter ecosystems. Suunto’s April 2025 Ocean hybrid signals multidiscipline convergence by merging dive profiles with marathon metrics, broadening brand reach.

Consumer-electronics entrants inject fresh rivalry. Apple leverages an immense installed watch base and periodic software updates to iterate dive capabilities without dedicated hardware releases, challenging purpose-built models on value perception. Garmin pre-emptively diversified into large-format architectures with the Descent X50i, accepting that wrist real estate may face smartwatch commoditization. Traditional dive-gear conglomerates such as Mares and Scubapro counter via bundled regulator-computer packages that incent ecosystem lock-in.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The wrist dive computer measures depth and time, then uses the algorithm to determine decompression requirements or estimate remaining no-stop times at the current depth.

The wrist dive computer market is segmented by display type (AMOLED display, MIP display), by distribution channel (online, offline), by end-users (civilian, military, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.