Recreation Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

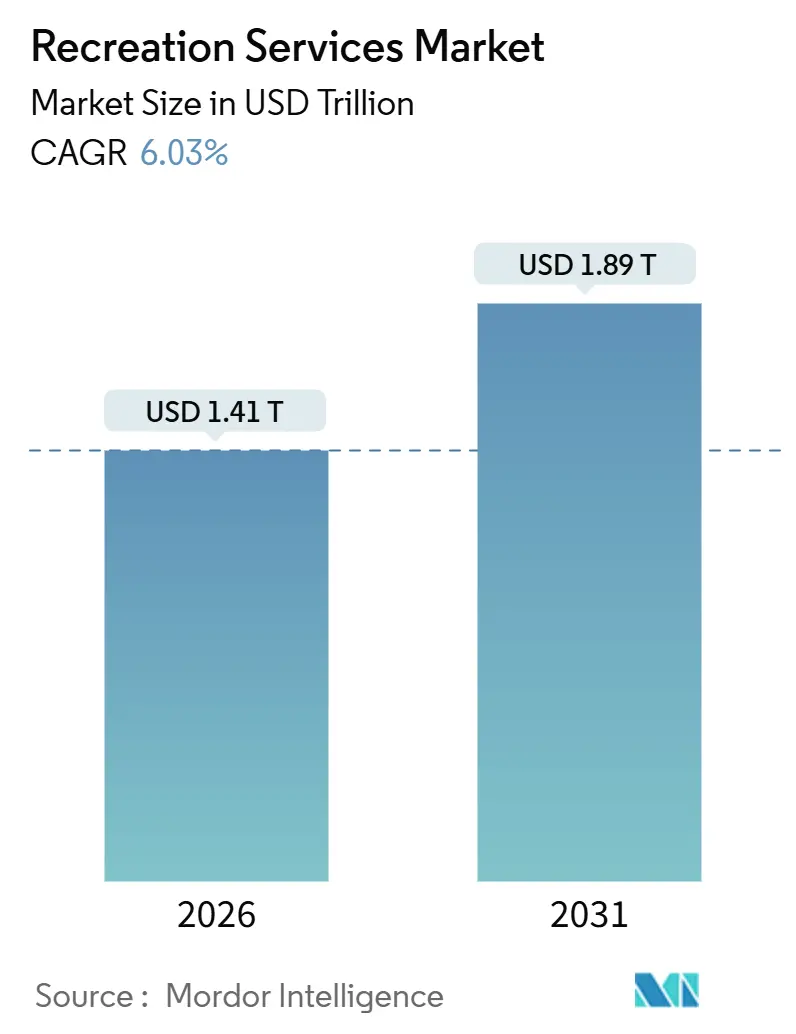

| Market Size (2026) | USD 1.41 Trillion |

| Market Size (2031) | USD 1.89 Trillion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

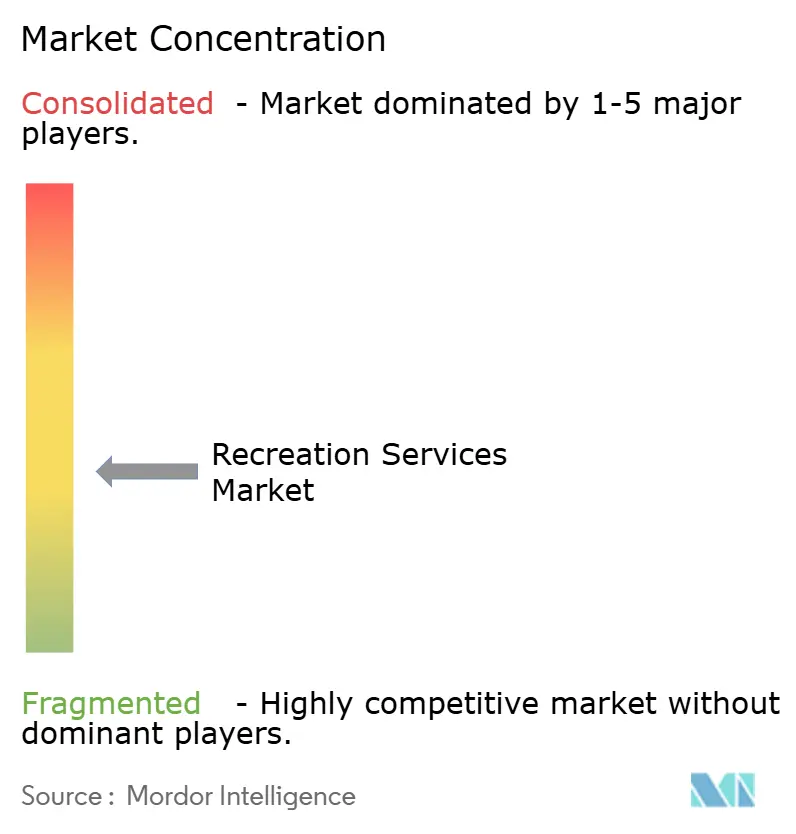

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recreation Services Market Analysis by Mordor Intelligence

The global recreation services market size reached USD 1.41 trillion in 2026 and is projected to climb to USD 1.89 trillion by 2031, registering a 6.03% CAGR during the forecast period. This expansion reflects a decisive move away from passive leisure toward immersive, intellectual-property-anchored venues that command higher per-capita outlays. Operators that integrate physical infrastructure with digital overlays are extracting larger margins, while brands eager for captive audiences are accelerating sponsorship demand. North America remains the single-largest region, yet Asia-Pacific is advancing the fastest on the back of a wealthier middle class and government tourism investments. Competitive intensity is rising as media conglomerates vertically integrate, capital costs escalate, and technology reshapes visitor engagement.

Key Report Takeaways

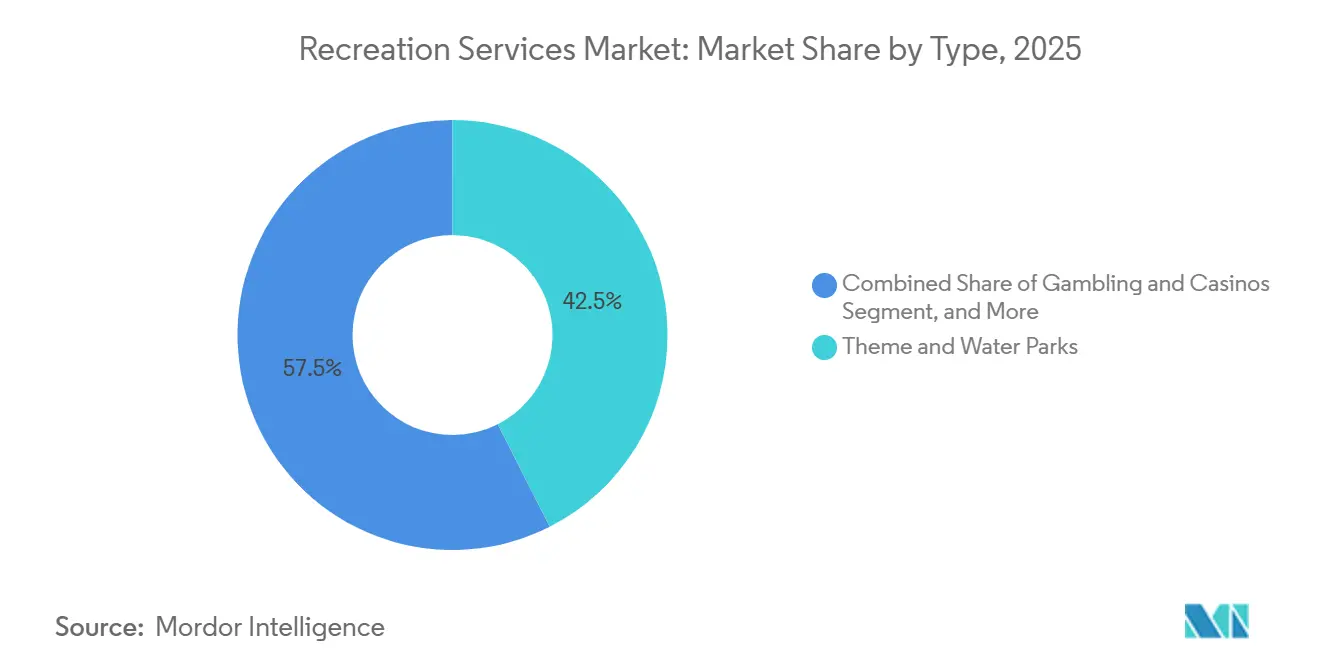

- By type, theme and water parks led with 42.53% of recreation services market share in 2025, while online and virtual experiences are forecast to expand at a 6.92% CAGR to 2031.

- By revenue stream, admission and ticket sales accounted for 48.27% of the recreation services market size in 2025, whereas sponsorship and advertising is the fastest-growing stream at a 6.71% CAGR through 2031.

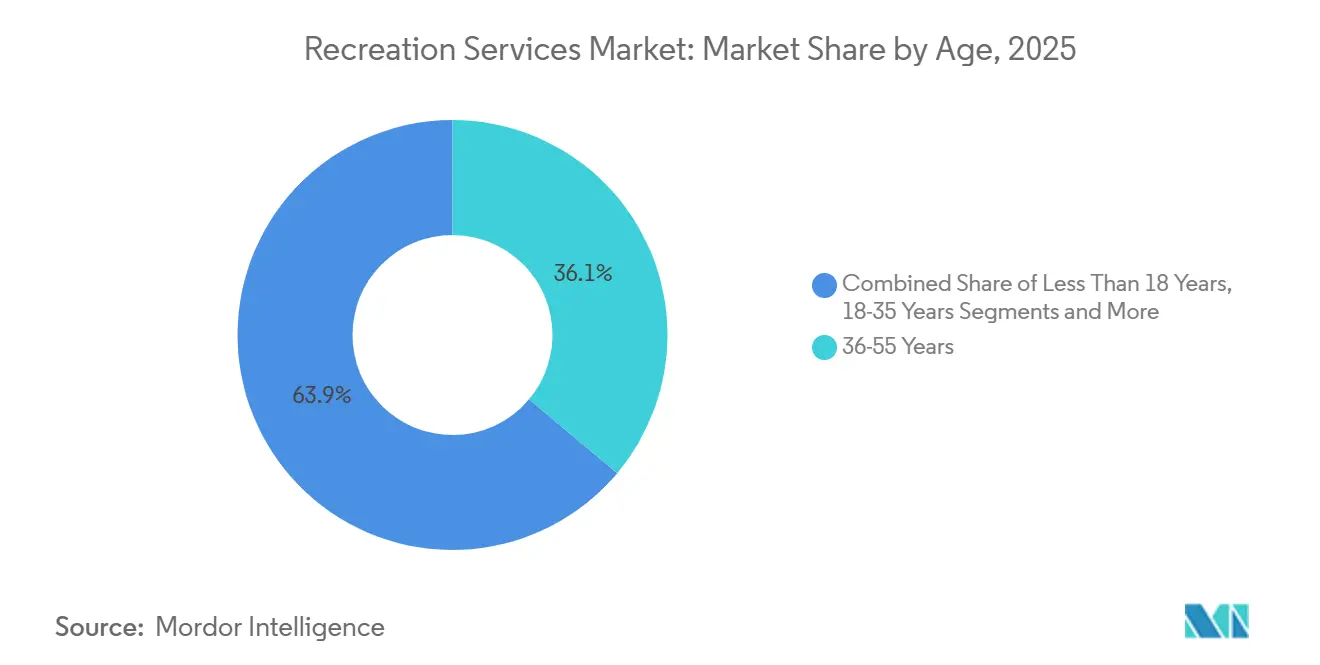

- By age group, millennials contributed 36.11% of 2025 revenue, but Generation Z is poised for a 6.47% CAGR through 2031, reflecting its appetite for shareable experiences.

- By mode, on-site physical visits dominated with an 88.07% share in 2025, yet virtual and online formats are expanding at a 6.92% CAGR, underscoring the need for hybrid propositions.

- By geography, North America commanded 35.49% of revenue in 2025, while Asia-Pacific is projected to post a 6.54% CAGR through 2031 on surging discretionary incomes and tourism infrastructure.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recreation Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer-led shift toward experiential leisure travel in Asia-Pacific | +1.2% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Surge of IP-based theme parks tied to global media franchises | +1.4% | Global, highest in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Casino-integrated resorts driving non-gaming revenue diversification in North America | +0.9% | North America, Macau, Singapore | Medium term (2-4 years) |

| Government urban-revitalization programs spurring cultural attractions in Europe | +0.7% | Europe, early gains in France, Germany, United Kingdom | Long term (≥ 4 years) |

| Sports-tourism campaigns ahead of 2028 Los Angeles and 2032 Brisbane Olympics | +0.8% | North America, Australia | Short term (≤ 2 years) |

| Rapid adoption of AR/VR attractions to boost per-capita spend in GCC | +1.0% | Middle East (UAE, Saudi Arabia, Qatar) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer-Led Shift Toward Experiential Leisure Travel in Asia-Pacific

China’s domestic tourism bill hit CNY 5.8 trillion (USD 820 billion) in 2025, with 22% flowing to theme parks and cultural venues, up four percentage points since 2023.[1]China National Tourism Administration, “Domestic Tourism Expenditure Report 2025,” cnta.gov.cn Parallel spending pivots are visible in India, where outbound travel jumped 34% year-over-year in 2025, yet domestic venues captured a bigger slice as operators expanded capacity. Younger visitors prize photogenic, interactive installations, prompting operators to prioritize set design and mobile-ready experiences. Governments from Thailand to Vietnam now market experiential attractions as anchors for economic diversification, reinforcing the region’s 6.54% CAGR outlook.

Surge of IP-Based Theme Parks Tied to Global Media Franchises

Intellectual property is the chief price premium driver, raising per-capita spending by as much as 40% relative to generic rides. Universal’s Epic Universe, opened in 2025 after a USD 5 billion build-out, charges USD 150-200 entry by bundling Nintendo, Harry Potter, and How to Train Your Dragon lands. Disney answered with a USD 2.2 billion Shanghai Resort expansion announced in December 2025. Independent parks lacking franchise access face a squeeze, often pivoting to culturally rooted themes or selling to larger platforms.

Casino-Integrated Resorts Driving Non-Gaming Revenue Diversification in North America

MGM Resorts derived 58% of Q3 2025 revenue from entertainment, dining, and retail as traditional table-game propensity wanes among younger patrons.[2]MGM Resorts Investor Relations, “Q3 2025 Earnings Report,” mgmresorts.com Las Vegas Sands’ Macau resorts generated 61% from non-gaming streams in the same quarter, while Wynn Resorts earmarked USD 1.1 billion for a Las Vegas theater and immersive dining upgrade. The pivot shields earnings from regulatory caps on gaming tables and aligns with Generation Z demand for diversified leisure.

Government Urban-Revitalization Programs Spurring Cultural Attractions in Europe

France allocated EUR 850 million (USD 920 million) in 2025 to regional museums, and Germany committed EUR 1.3 billion for digitized heritage upgrades through 2027. The United Kingdom increased regional gallery funding by 28% in 2025. Publicly financed venues now pull visitor traffic away from private parks, particularly older travelers favoring educational content.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front CAPEX for Large-Scale Experiential Venues (More than USD 500 million) | -0.8% | Global, with acute impact in emerging markets | Long term (≥ 4 years) |

| Rising Liability-Insurance Premiums for High-Thrill Attractions | -0.6% | North America, Europe, Australia | Short term (≤ 2 years) |

| Talent Shortages in Specialised Live-Event Operations Post-COVID | -0.5% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Intensifying ESG Scrutiny on Animal-Based Entertainment | -0.4% | North America, Europe, with emerging pressure in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front CAPEX for Large-Scale Experiential Venues

Universal’s latest park consumed USD 5 billion over five years, a threshold unattainable for most independents. Interest-rate hikes added 200-300 basis points to emerging-market borrowing costs in 2024-2025, delaying project timelines and nudging smaller operators toward asset-light licensing arrangements.

Rising Liability-Insurance Premiums for High-Thrill Attractions

Insurance costs for roller coasters and water slides climbed 18-22% across North America and Europe in 2025. Cedar Fair said premiums now consume 4-5% of revenue, almost double 2022 levels.[3]Cedar Fair, “Form 10-K 2024,” sec.gov European regulators shortened inspection intervals, magnifying compliance spending and pressuring margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type - Virtual Add-Ons Amplify IP-Driven Park Economics

Theme and water parks captured 42.53% of 2025 revenue thanks to multi-day visit potential, premium quick-queue passes, and on-site hotels that elevate recreation services market size. Yet virtual experiences, though only 11.93% of revenue in 2025, are forecast for a 6.92% CAGR, the highest in the recreation services market. IP-anchored mega-resorts continue to justify USD 5 billion budgets, whereas mid-market operators such as Merlin Entertainments avoid head-to-head competition by emphasizing city-center attractions. Gambling venues, integrating luxury dining and live shows, reduce gaming dependency as regulators tighten oversight. Cultural sites, boosted by urban-renewal grants, meet the accessibility preferences of older segments yet must address ESG pressure on animal exhibits.

Second-order dynamics revolve around data-driven personalization. RFID wristbands and mobile apps at Epic Universe and Six Flags transform visitor flow management and coax incremental spending, supporting recreation services market share gains for operators that can fund such systems. Asset-light strategies are proliferating: smaller park chains license IP or sell to larger groups to sidestep CAPEX barriers.

By Revenue Stream - Sponsorship Scales Beyond Static Signage

Admission fees remained the backbone at 48.27% of 2025 turnover, but brands are accelerating into immersive collaborations that yield the 6.71% CAGR in sponsorship and advertising. Food and beverage receipts outpace headline attendance growth as celebrity chef partnerships lift average checks to USD 80-120. Merchandise now skews toward personalized items enabled by RFID and mobile checkout, while premium fast-pass products and after-hours events embed dynamic pricing. MGM Resorts extracted 42% of Q3 2025 turnover from food and beverage, illustrating how premiumization counters ticket-price sensitivity.

Operators increasingly bundle experiences: Coca-Cola’s interactive tasting lab at Disney Springs and Samsung’s VR zones at Six Flags recast sponsorship as an attraction in itself, enhancing the recreation services market size without overcrowding price-conscious admission lines. The strategy also decreases revenue cyclicality by aligning brand budgets with off-peak periods.

By Age Group - Social-First Design Captures Generation Z Wallets

Operators that segment offerings with VIP tours for millennials and sensory-inclusive experiences for seniors balance per-capita upside with inclusivity mandates.

By Mode - Hybrid Visitation Extends Lifetime Customer Value

On-site visits still anchor the recreation services market, but virtual modes expand reach to international or mobility-constrained audiences. Disney’s late-2025 VR park lets users roam Magic Kingdom remotely, purchase merchandise, and bank loyalty points redeemable on future physical trips. Universal deploys VR pre-shows that feed narrative context before guests join physical queues, cutting perceived wait time and supporting higher recreation services market share. Hybrid passes coupling physical tickets with exclusive digital content encourage annual renewals and minimize seasonality.

Geography Analysis

North America maintained a 35.49% hold on the recreation services market in 2025, anchored by mature clusters in Florida, California, and Nevada. Growth is moderating in absolute attendance; hence, operators emphasize premiumization through VIP tours, backstage events, and dynamic pricing to boost per-capita spend. Liability insurance inflation and talent shortages temper expansion, although large chains leverage economies of scale to maintain margins.

Asia-Pacific is on a 6.54% CAGR trajectory to 2031, powered by expanding middle-class households and government-backed tourism corridors. China’s 2025 domestic tourism bill of CNY 5.8 trillion (USD 820 billion) channeled 22% to parks and cultural venues, while India’s theme park footfall rose 28% and operators pushed into tier-2 cities. Japan’s Universal Studios Osaka logged record attendance in fiscal 2025 on the magnetism of Super Nintendo World. Rapid AR/VR adoption bolsters per-capita spend in Gulf Cooperation Council states, with Saudi Arabia’s Qiddiya aiming for 17 million annual visitors by 2030.

Europe benefits from cultural-site subsidies, yet tepid macro conditions in Germany and France restrain disposable income. Urban renewal programs channel visitors to secondary cities, easing congestion in legacy hubs like Paris and London. The Middle East and South America are earlier-stage but assertive: Dubai Parks and Resorts added a Bollywood zone in 2025 to capture South Asian travelers. Africa’s growth potential hinges on infrastructure investment; operators eye clusters in Egypt, South Africa, and Kenya for long-term positioning.

Regulatory Landscape

Regulation is tightening around the digital layers that increasingly run alongside physical recreation, including online and virtual experiences, ticketing apps, and media-delivered leisure content. In the United Kingdom, secondary legislation implementing the Media Act 2024 expanded Ofcom oversight for Tier 1 video-on-demand services, adding clearer content standards and accessibility obligations for large services (500,000+ UK users). For recreation operators that distribute branded experiences via connected TV and streaming platforms, this creates additional compliance constraints across content and access.

Elsewhere, governments are formalizing age-gating and verification requirements that affect online recreation and interactive entertainment. At the EU level, Commission Recommendation (EU) 2026/1035 (adopted 29 April 2026) set a timetable for member states to implement privacy-enhancing age-verification solutions by 31 December 2026, raising expectations for platforms that blend virtual experiences with commerce and loyalty. In India, the Promotion and Regulation of Online Gaming Rules, 2026 came into force on 1 May 2026 and created the Online Gaming Authority of India, increasing oversight for online money games and adjacent e-sports ecosystems that overlap with online and virtual recreation offerings.

Competitive Landscape

The recreation services market registers moderate concentration: the top 10 players account for roughly 35-40% of global revenue. Disney, Universal, Merlin Entertainments, Las Vegas Sands, and MGM Resorts anchor this cohort, each leveraging IP, real estate scale, and data analytics to widen moats. Capital requirements north of USD 500 million for marquee assets deter new entrants, though asset-light licensing provides a bridge for regional players.

Technological differentiation is accelerating. Universal’s Epic Universe adopted biometric entry and predictive analytics to steer visitor flow and optimize staffing, demonstrating cost deflation and elevated guest spending. Disney’s 2025 augmented-reality patents foreshadow customizable storylines delivered through personal devices, lifting dwell time and merchandise sales. Data-centric upstarts like Dreamscape and Sandbox VR offer location-based VR attractions with lighter CAPEX, siphoning urban consumers seeking novel night-out options.

Consolidation is set to intensify as smaller parks battle insurance inflation and labor scarcities. Larger groups can absorb these costs, standardize training, and negotiate enterprise-wide sponsorship deals, further uplifting their recreation services market share. IP gatekeepers also wield leverage: holders that once licensed brands now prefer vertical integration, tilting bargaining power away from stand-alone operators.

Recreation Services Industry Leaders

The Walt Disney Company

Universal Destinations & Experiences

Las Vegas Sands Corp.

Merlin Entertainments Group

MGM Resorts International

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hybrid recreation propositions are creating additional whitespace as jurisdictions formalize age assurance and platform oversight, with compliance-ready digital experiences becoming a more tangible differentiator for operators that can run robust data governance. The EU requirement for privacy-enhancing age verification by 31 December 2026 and the United Kingdom's Ofcom regime for large video-on-demand services under the Media Act 2024 increase demand for trusted identity, accessibility, and content controls across virtual layers used for remote park access, AR/VR overlays, and loyalty programs. For operators already linking on-site visits (88.07% share in 2025) with digital add-ons, these compliance investments can support higher-value sponsorship formats that function more like attractions than static placements.

Commercially, advertising and identity infrastructure is shifting toward data-driven activation, which gives recreation venues ways to monetize captive attention without pushing gate prices. In May 2026, Publicis agreed to acquire LiveRamp for USD 2.2 billion to strengthen data, identity, and agentic media buying capabilities, supporting measurable sponsorship and advertising tied to personalized targeting. In July 2026, Fox Corporation named Amazon Web Services its preferred AI cloud provider to power the FOX One direct-to-consumer platform, and Warner Bros. Discovery announced agentic AI-powered advertising technology built on AWS, highlighting how AI tooling can be adapted by IP owners and venue operators for targeted promotion, dynamic offers, and integrated media-to-venue engagement.

Recent Industry Developments

- July 2026: Universal Destinations and Experiences officially opened Universal Kids Resort in Frisco, Texas, expanding its footprint beyond destination mega-parks into a family-focused regional format. The opening adds a new mix of revenue sources and strengthens repeat-visit potential in a large metro catchment, while increasing competitive pressure on regional amusement and themed entertainment operators.

- December 2025: The Walt Disney Company committed USD 2.2 billion to expand Shanghai Disney Resort, adding major IP-led lands (including Zootopia and Frozen) scheduled to open in 2028. The investment reinforces how franchised intellectual property supports premium ticketing, merchandising, and multi-day visitation in Asia-Pacific.

- October 2024: MGM Resorts partnered with Live Nation on a USD 1.5 billion Las Vegas entertainment district project. This deepens casino-integrated resort strategies that emphasize non-gaming recreation, including live events and venue-driven food and beverage, to broaden spend per visitor.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the recreation services market is the value of paid experiences and facilities that people use during leisure time, including amusements, sports and event participation, cultural visits, and selected digital recreation where the core purpose is entertainment or wellness.

Scope exclusions: We exclude lodging, passenger transport, packaged travel products, and standalone sales of recreation equipment or apparel.

Segmentation Overview

- By Type

- Amusements

- Theme and Water Parks

- Gambling and Casinos

- Cultural and Heritage Attractions (Museums, Galleries, Zoos)

- Sports Facilities and Events

- By Revenue Stream

- Admission / Ticket Sales

- Food and Beverage

- Merchandise and Licensing

- Sponsorship and Advertising

- By Age Group

- Less Than 18 Years

- 18-35 Years

- 36-55 Years

- 55+ Years

- By Mode

- On-Site / Physical

- Online and Virtual Experiences

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia

- Middle East and Africa

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping which activities are treated as recreation services and how spending is commonly recorded across countries. We relied on public statistical series and definitions from sources such as the US Bureau of Economic Analysis and US Bureau of Labor Statistics, Eurostat, the UN World Tourism Organization, and World Bank macro indicators to anchor income, inflation, and consumer outlays.

To keep the model workable, we also reviewed materials that show operating revenue patterns and participation signals, such as company annual reports, investor presentations, filings, and reputable press coverage of attendance and ticketing trends. Where gaps existed in the public record, we used paid subscriptions for company financials and intelligence, broad news and financials, patent lookups for experience formats, and selected trade and shipment databases when import exposure mattered for facility inputs. These desk sources are illustrative and not exhaustive, and many other public and paid references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually counted as paid recreation service revenue, and how pricing moves through the year. We spoke with operators, distributors and partners, venue managers, and industry advisors across APAC, EMEA, and the Americas to confirm demand drivers, utilization swings, and common revenue streams (tickets, memberships, food and beverage attach rates, and digital add-ons).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 43% |

| Mid tier: 59% | Functional/Unit leaders: 32% | EMEA: 37% |

| Smaller Players: 14% | Managers: 55% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where consumer leisure spend and service revenue pools are reconstructed by region and then filtered into recreation-only services using activity participation, venue capacity, and tourism intensity indicators. Once the regional totals were formed, we corroborated them with selective bottom-up checks, such as sampled venue revenue per visitor, membership counts multiplied by average fees, and a small set of supplier and channel checks that helped keep the totals realistic.

Key model inputs included inbound and domestic tourism volumes, household discretionary spending and inflation, venue attendance and utilization patterns (seasonality matters in parks and outdoor formats), ticket and membership price moves, and the mix shift between on-site and online or virtual offerings. Where bottom-up signals were missing for smaller formats, we used proxies such as capacity counts, typical revenue per seat or per visit, and the share of paid participation confirmed through interviews, then adjusted using regional consistency tests.

For forecasting, scenario analysis was used with a simple set of demand and pricing drivers that are easy to track year to year, and assumptions were aligned to expert views on price pass-through, occupancy and attendance recovery, and travel normalization. The forecast was then converted into USD using consistent currency timing so regional growth is not overstated by short-term exchange-rate swings.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals such as tourism receipts, recreation-related consumer spend trends, and reported admissions or member growth where available. Large variances triggered a second pass on the underlying drivers, and when a swing could not be explained by demand or price, respondents were re-contacted to confirm whether the issue was scope, timing, or a one-off event.

Before sign-off, assumptions and calculations go through multi-step analyst reviews, including checks for year-over-year continuity and regional sanity. Reports are refreshed annually, and interim updates are made when material events change pricing, capacity, or participation behavior. Right before delivery, a final update sweep is completed so clients receive the latest view.

Mordor Intelligence's Recreation Services Market Estimate Compared With Other Published Estimates

Published market sizes for recreation services can look far apart even when the topic label is similar, because the included activities, revenue streams, and currency treatment are not consistent. Differences usually come from whether gambling, digital experiences, and on-site add-on revenues are included, and from whether the number is built from consumer spend pools or from operator revenue roll-ups.

Refresh cadence and currency timing also matter because ticket prices, memberships, and travel-linked attendance can shift within a year, which changes the effective average selling price used in the model. When exchange rates, inflation pass-through, and validation checks against participation and capacity signals are refreshed on a clear cadence, the final USD value tends to be more stable across updates, which is the refresh-led logic applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.41 T (2026) | |

| Trade Publisher A | USD 1.32 T (2024) | Uses an earlier base year and a different cut of the demand pool, and the estimate is more sensitive to near-term pricing and exchange-rate timing when rolling forward to later years. |

| Industry Report B | USD 1.72 T (2025) | Broader recreation definition can pull in adjacent categories and may include more bundled goods value within service revenue, which can lift the total versus a tighter recreation-services-only boundary. |

The table shows that most of the spread is explained by year selection and by how far the scope extends into adjacent recreation activities and bundled value. By keeping the scope tied to paid recreation service experiences and by checking price and attendance style inputs before converting to USD, the estimate stays traceable to a repeatable set of drivers rather than a one-time spend snapshot.

Key Questions Answered in the Report

How large is the recreation services market in 2026?

The recreation services market size reached USD 1.41 trillion in 2026.

What is the expected CAGR through 2031?

Market value is projected to rise at a 6.03% CAGR from 2026 to 2031.

Which segment is growing the fastest?

Online and virtual experiences lead with a forecast 6.92% CAGR.

Why are sponsorship revenues rising?

Brands seek captive audiences, making sponsorship the fastest-growing revenue stream at 6.71% CAGR.

Which region shows the strongest growth outlook?

Asia-Pacific is expected to advance at a 6.54% CAGR through 2031, supported by a growing middle class and tourism infrastructure.

How are operators responding to high CAPEX barriers?

Smaller parks adopt asset-light licensing or sell to larger groups, while major players leverage diversified cash flows to self-finance expansions.

Page last updated on: