Spinal Muscular Atrophy Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

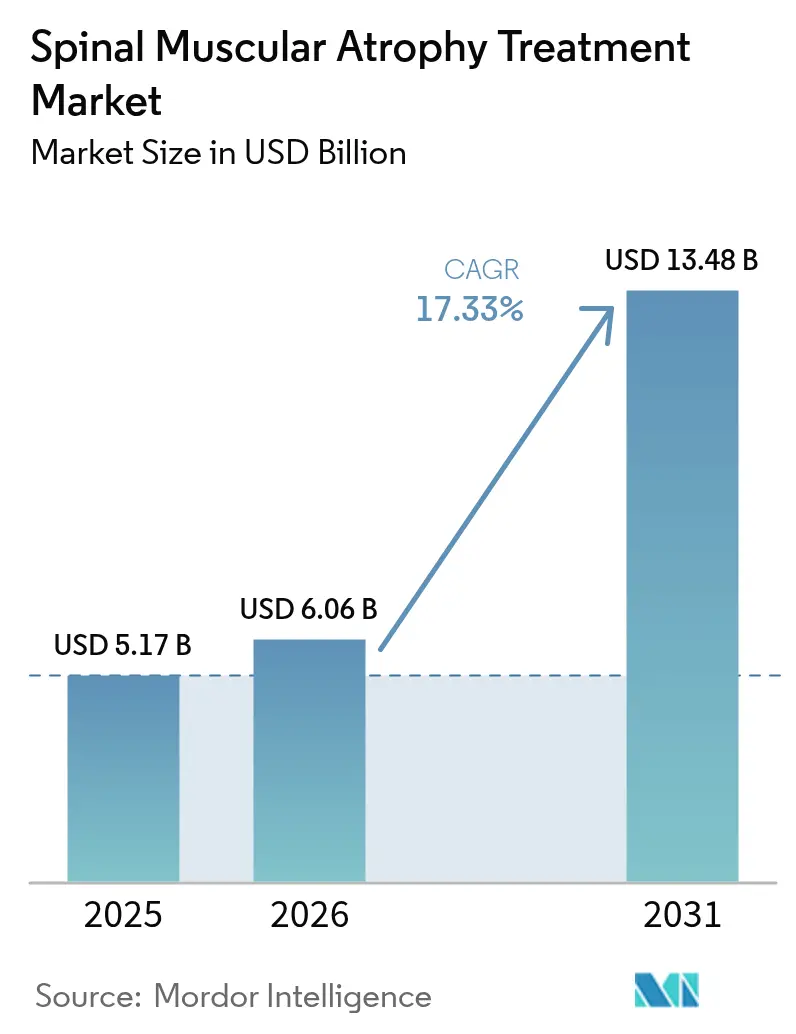

| Market Size (2026) | USD 6.06 Billion |

| Market Size (2031) | USD 13.48 Billion |

| Growth Rate (2026 - 2031) | 17.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spinal Muscular Atrophy Treatment Market Analysis by Mordor Intelligence

spinal muscular atrophy treatment market size in 2026 is estimated at USD 6.06 billion, growing from 2025 value of USD 5.17 billion with 2031 projections showing USD 13.48 billion, growing at 17.33% CAGR over 2026-2031. A mature newborn-screening infrastructure, rapid uptake of gene therapies, and supportive reimbursement policies combine to create the highest growth trajectory ever recorded for this rare-disease space. Early diagnostic confirmation drives presymptomatic treatment starts, while multiple SMN-targeting mechanisms expand clinical choice, reduce unmet need, and lift the overall spending ceiling. Pharmaceutical revenues further benefit from precision dosing strategies, combination-regimen trials, and steady geographic rollouts that add new payer budgets every year. At the same time, high-value outcomes data, particularly five-year survival gains, sustain premium prices even as additional entrants reach the market. Collectively these factors ensure the spinal muscular atrophy treatment market continues to outpace broader neurological drug segments through 2030.

Key Report Takeaways

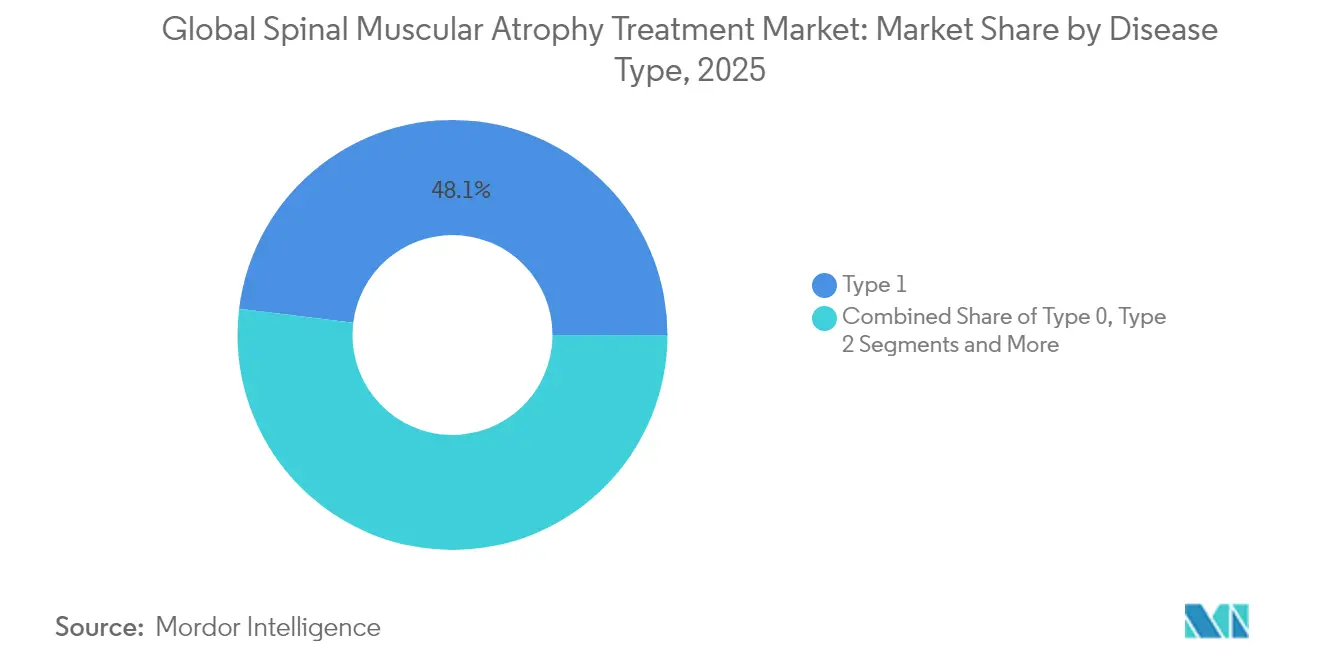

- By disease type, Type 1 SMA held 48.05% of the spinal muscular atrophy treatment market share in 2025; Type 0 is projected to expand at an 18.02% CAGR to 2031.

- By treatment modality, SMN2 splicing modifiers led with 42.35% revenue share in 2025; gene replacement therapy is on track for an 18.41% CAGR through 2031.

- By route of administration, intrathecal therapies accounted for 51.05% share of the spinal muscular atrophy treatment market size in 2025, while oral regimens advance at an 18.22% CAGR to 2031.

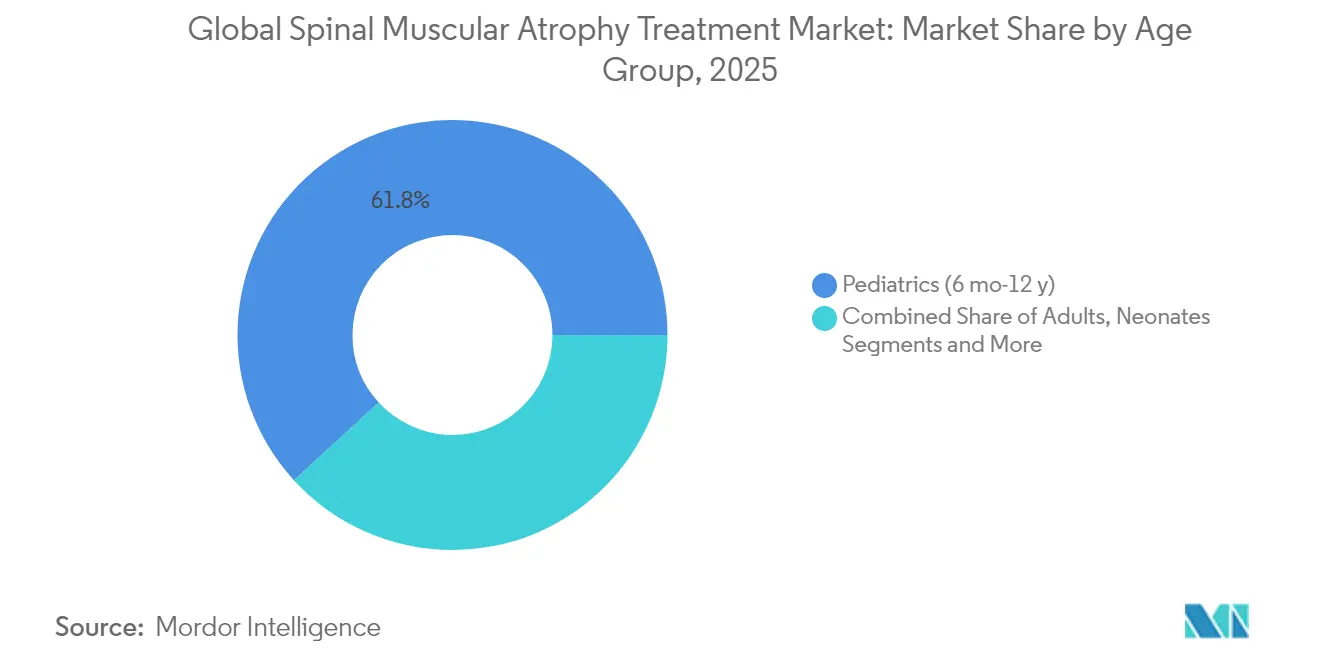

- By age group, pediatric patients captured 61.80% of the spinal muscular atrophy treatment market size in 2025; neonates record the fastest 18.05% growth through 2031.

- By distribution channel, hospital pharmacies controlled 46.85% revenue in 2025; online and retail outlets grow at 18.92% CAGR into 2031.

- By geography, North America dominated with 42.30% share in 2025, while Asia-Pacific is forecast to rise at a 18.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spinal Muscular Atrophy Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Newborn Screening Mandates Expand Treatable Patient Pool | +3.2% | Global, with early gains in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Rapid Uptake Of SMN-Targeting Gene Therapies In High-Income Markets | +4.1% | North America & EU, spillover to APAC core markets | Medium term (2-4 years) |

| Global Payer Acceptance Of High-Value Rare-Disease Drugs | +2.8% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Rising Advocacy-Group Funding For Early-Stage Trials | +1.9% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Pipeline Combination Regimens Targeting SMN & Myostatin | +3.5% | Global, initial deployment in high-income markets | Long term (≥ 4 years) |

| Home-Based Digital Adherence Platforms Boost Chronic Dosing | +1.8% | Developed markets initially, expanding to emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Newborn Screening Mandates Expand Treatable Patient Pool

Nationwide screening now active across all US states since January 2024 identifies SMA at a presymptomatic stage, enabling optimal timing for high-impact therapies. Taiwan, Hungary, and Serbia followed similar rollouts and collectively screened more than 650,000 infants, highlighting scalability across varied health systems [1]Audrey M. Nijhof, “Five-Year Newborn Screening Outcomes in Taiwan,” Orphanet Journal of Rare Diseases, ojrd.biomedcentral.com. Screening detects roughly 1 in 14,694 newborns, generating a predictable annual cohort that sustains therapy demand. Early detection translates into markedly improved motor outcomes, reinforcing payer willingness to reimburse expensive treatments. The practice also supplies essential epidemiological data that refine capacity planning for infusion centers and specialty pharmacies.

Rapid Uptake of SMN-Targeting Gene Therapies in High-Income Markets

SMN-targeting therapeutics now span antisense oligonucleotides, gene replacement vectors, and small-molecule splicing modifiers, offering clinicians multiple paths to restore SMN protein levels. Nusinersen dose-escalation showed a 94% reduction in plasma neurofilament light chain, supporting the clinical rationale for higher loading doses. Roche’s February 2025 tablet approval further lowers treatment burden without compromising exposure. Novartis achieved a 2.39-point HFMSE gain in older children using intrathecal onasemnogene abeparvovec, broadening gene-therapy eligibility. Together, these advances shorten the adoption curve and amplify the revenue base of the spinal muscular atrophy treatment market.

Global Payer Acceptance of High-Value Rare-Disease Drugs

Cost-effectiveness ratios for nusinersen often exceed USD 210,000 per QALY, yet nationwide SMA coverage persists across most US and major EU payers because early intervention averts lifelong ventilatory and orthopedic costs. Orphan-drug incentives, real-world evidence, and outcome-based contracts continue to reinforce reimbursability. The European SMA access tracker confirms an upward trend in favourable reimbursement decisions each year. Payer endorsement translates into steady revenue visibility and underpins multi-year investment in next-generation assets.

Rising Advocacy-Group Funding for Early-Stage Trials

Non-profit organisations such as Cure SMA, Muscular Dystrophy UK, and SMA Foundation direct grants toward exploratory approaches, including RNA editing and neuro-protective small molecules. Their involvement accelerates proof-of-concept phases, de-risks technology platforms, and attracts venture capital follow-on funding. Resulting trial networks shorten enrolment timelines, widen geographic reach, and maintain the innovation pipeline that sustains growth momentum for the spinal muscular atrophy treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Million-dollar price tags and uncertain long-term reimbursement | -2.9% | Global; strongest in emerging markets | Medium term (2-4 years) |

| Intrathecal delivery complexities and capacity constraints at infusion centers | -1.8% | Global; acute where specialist density is low | Short term (≤ 2 years) |

| Shortage of pediatric neuromuscular specialists in emerging economies | -2.1% | Latin America, South Asia, Africa | Long term (≥ 4 years) |

| Viral-vector manufacturing bottlenecks for AAV supplies | -1.6% | Global; impacts gene-therapy rollouts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Million-Dollar Price Tags and Uncertain Long-Term Reimbursement

Zolgensma’s multi-million-dollar cost and a lifetime efficacy horizon strain payer budgets, especially in middle-income countries. Incremental cost-effectiveness ratios remain above traditional thresholds, prompting risk-sharing arrangements that delay uptake. Where coverage is approved, reimbursement often includes outcomes-based milestones, adding administrative complexity and revenue deferral for manufacturers. This drag limits penetration potential despite compelling clinical benefit.

Intrathecal Delivery Complexities and Capacity Constraints at Infusion Centers

Intrathecal dosing requires lumbar-puncture expertise and fluoroscopy equipment unavailable in many regional hospitals. Scheduling backlogs now reach several weeks at some US and EU centers, delaying therapy start within the critical presymptomatic window [2]Giuseppe M. Geraci, “Safety of Lumbar Puncture in SMA Children,” European Journal of Paediatric Neurology, sciencedirect.com. Pediatric spinal deformities increase procedural risk and lengthen appointment slots, further squeezing capacity. These bottlenecks cap the near-term growth pace of the spinal muscular atrophy treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Type 1 Severity Drives Market Concentration

Type 1 SMA retained 48.05% share of the spinal muscular atrophy treatment market in 2025. Its life-threatening nature prompts immediate therapy initiation and supports premium pricing. Universal newborn screening has shifted diagnoses into the presymptomatic stage, improving ventilatory-free survival and reinforcing clinical consensus for early gene therapy use. Type 0, historically excluded from trials, now logs an 18.02% CAGR as regulatory guidance broadens eligibility criteria and compassionate-use precedents confirm safety. Types 2 and 3 generate steady, recurring revenue because lifelong maintenance dosing remains standard practice. Type 4 adult-onset cases remain a niche today but grow as awareness climbs.

Presymptomatic treatment markedly improves motor milestones for Type 1 patients, evidenced by Taiwanese screen-and-treat cohorts achieving independent sitting in 100% of gene-therapy recipients. Later-onset groups experience slower but durable gains, supporting chronic therapy continuation. Variations in disease severity influence modality choice: gene replacement is favored in Type 1, while SMN2 splicing modifiers and antisense oligonucleotides dominate Types 2-4 due to flexible dosing and straightforward logistics.

By Treatment Modality: SMN2 Splicing Dominance Faces Gene-Therapy Challenge

SMN2 splicing modifiers commanded 42.35% of the spinal muscular atrophy treatment market share in 2025. Competitive advantages include pan-phenotype eligibility, oral or intrathecal options, and favorable safety records. Gene-replacement therapy shows the fastest 18.41% CAGR as manufacturing yields improve and intrathecal formulations remove weight caps for older children. Antisense oligonucleotides hold steady with dose-escalation protocols, boosting neurofilament clearance metrics.

Muscle-directed agents such as apitegromab promise synergistic benefits when layered onto SMN-restoring backbones. Supportive therapies—ventilation aids, nutritional support, orthopedics—still feature in multidisciplinary care but shrink in revenue share as disease-modifying agents delay or prevent complications. An emerging pipeline of RNA-editing tools could eventually converge with existing modalities, sustaining innovation depth for the spinal muscular atrophy treatment market.

By Route of Administration: Intrathecal Infrastructure Enables Oral Growth

Intrathecal delivery held 51.05% share of the spinal muscular atrophy treatment market size in 2025. Long-standing lumbar-puncture protocols and infusion suites create entrenched practice patterns. However, oral risdiplam and the newly approved Evrysdi tablet grow at 18.22% CAGR thanks to at-home dosing convenience and comparable CNS exposure. Intravenous gene-therapy infusions remain important for infants under 13.5 kg but face expansion limits due to AAV manufacturing capacity.

Patient-centric flexibility now guides administration decisions. Families living far from infusion centers often prefer oral routes, whereas infants screened presymptomatically may receive single-dose gene therapy followed by periodic laboratory monitoring. Intrathecal capacity investments—additional fluoroscopy suites, nurse-practitioner training—continue, yet they also raise fixed costs that hospitals aim to amortize through high treatment throughput, further anchoring intrathecal share even as oral uptake accelerates.

By Age Group: Pediatric Concentration Reflects Early-Intervention Focus

The pediatric cohort aged 6 months to 12 years captured 61.80% of the spinal muscular atrophy treatment market size in 2025. Neurologists prefer aggressive therapy before irreversible motor-unit loss, making this segment the primary revenue engine. Neonatal prescriptions rise 18.05% annually, fueled by presymptomatic screen-and-treat programs. Adolescents and adults account for a smaller but rising share as diagnostic algorithms catch late-onset cases, and payers recognize quality-of-life gains even in established disability.

Early-treated infants now reach normative developmental percentiles, forcing regulators to revise functional endpoints that once relied on motor-score increments. Adult-onset SMA brings separate needs: managing fatigue, scoliosis, and metabolic demands. Tailored dosing and rehabilitation adjuncts expand total addressable spend per patient, maintaining growth momentum for the sspinal muscular atrophy treatment market.

By Distribution Channel: Hospital Pharmacies Anchor Specialist Care Networks

Hospital pharmacies dispensed 46.85% of therapies in 2025. Complex logistics—cold chain, inventory of gene-therapy vectors, emergency response readiness—justify their central role. Specialty clinics coordinate dosing schedules, collect real-world data, and interface with payers on outcomes-based contracts. Online and retail pharmacies grow at 18.92% CAGR, powered by direct-to-home delivery of oral formulations and remote adherence monitoring tools.

Hybrid hub models now link hospital-based infusion services with community pharmacists who oversee refill timeliness, nutritional consults, and telemedicine check-ins. Such integration reduces caregiver burden and supports lifelong adherence, thereby protecting pharmacotherapy revenue streams within the spinal muscular atrophy treatment market.

Geography Analysis

North America retained 42.30% of global revenue in 2025, underpinned by exhaustive newborn screening coverage, dense neuromuscular-specialist networks, and mature payer mechanisms that accommodate six- to seven-figure price tags. The US CMS infant-screening mandate guarantees near-universal early detection, while private insurers and Medicaid programs negotiate milestone-based contracts that secure wide access. Canada’s single-payer system funds risdiplam and nusinersen nationwide, yet gene-therapy reimbursement remains provincial in scope, leading to cross-border treatment outflow from western provinces to US centers. Europe shows steady incremental gains as EMA centralized approvals streamline label harmonization, but individual country negotiators stagger market entry times. Germany and France implement compulsory sickness-fund coverage for all approved SMA therapies, preserving high uptake. Conversely, Italy and Spain apply age or weight caps to gene-therapy funding, directing older children toward splicing modifiers instead. Eastern Europe accelerates newborn-screening adoption, with Serbia screening 54,000 infants within twelve months of program launch .

Asia-Pacific records the fastest 18.96% CAGR through 2031 thanks to rising health-insurance penetration, expanding molecular-diagnostics capacity, and government rare-disease lists that waive import tariffs. Japan leads on per-capita spend, screening every newborn since 2023 and funding all three SMN-targeted classes. China approved nusinersen in 2024 and included it in the NRDL formulary at a negotiated discount that accelerates provincial uptake. India’s Union Health Ministry pilots state-funded screening in Kerala and Maharashtra, laying groundwork for broader scale. Australia and South Korea complete the region’s high-income cluster, leveraging robust genomic labs and telehealth to reach rural patients. Collectively, these expansions add tens of thousands of eligible patients to the spinal muscular atrophy treatment market each year.

Competitive Landscape

The spinal muscular atrophy treatment market remains top-heavy, with Biogen, Novartis, and Roche together controlling well above two-thirds of global revenue. Each firm occupies a distinct mechanism niche—antisense, gene therapy, and oral splicing modulation—minimizing direct substitution and allowing parallel prescribing in many treatment algorithms. Defensive strategies include lifecycle management (higher-dose nusinersen, intrathecal gene vectors) and geographic expansion into emerging regions where reimbursement is still evolving.

Pipeline disruptors target complementary biology rather than head-on competition. Scholar Rock’s apitegromab, an anti-myostatin antibody, delivered 30.4% responder rates on top of background SMN therapy, positioning it as the first add-on muscle-build option. Roche started a Phase II/III combo study pairing risdiplam with RO7204239, aiming to quantify dual-pathway benefit. Manufacturing innovation also reshapes competitive moats: Novartis doubled AAV vector yield in 2025 by integrating suspension HEK293 systems, reducing per-dose cost, and mitigating supply constraints.

Strategic alliances expand global footprint. Biogen renewed its logistic partnership with UPS Healthcare to enhance cold-chain reliability into Latin America, while Roche licensed a Chinese CDMO to handle regional fill-finish and accelerate NRDL-linked supply timeline. M&A interest focuses on platform enrichment; myostatin and neuro-protective small-molecule startups report increased term-sheet activity. Overall, competition centers on combination versatility, supply security, and payer-linked patient-support infrastructure rather than price discounting, sustaining healthy margins across the spinal muscular atrophy treatment market.

Spinal Muscular Atrophy Treatment Industry Leaders

Biogen

F. Hoffmann - La Roche Ltd

Cytokinetics, Inc.,

Novartis AG

Catalyst Pharmaceutical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Scholar Rock received FDA priority review for apitegromab BLA with a PDUFA date of Sep 22 2025.

- February 2025: Roche secured FDA approval for Evrysdi 5 mg tablets, the first solid-dose formulation for SMA.

- January 2025: Novartis announced positive Phase III STEER data for intrathecal onasemnogene abeparvovec, posting a 2.39-point HFMSE improvement.

- September 2024: Biogen reported DEVOTE study results showing superior efficacy for higher-dose nusinersen with a 94% neurofilament reduction.

Global Spinal Muscular Atrophy Treatment Market Report Scope

Spinal muscular atrophy linked to chromosome 5q (SMA) is a recessive, progressive, neuromuscular disorder caused by bi-allelic mutations in the SMN1 gene, resulting in motor neuron degeneration and variable presentation in relation to onset and severity. The spinal muscular atrophy treatment market is segmented by type (type I, type II, type III, and type IV), procedure (gene replacement therapy and drug therapy), route of administration (oral and intrathecal), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The report offers the value (in USD million) for the above segments. The report offers the value (in USD million) for the above segments.

| Type 0 |

| Type 1 |

| Type 2 |

| Type 3 |

| Type 4 |

| Gene Replacement Therapy |

| SMN2 Splicing Modifiers |

| Antisense-Oligonucleotide Therapy |

| Muscle-Directed / Myostatin Inhibitors |

| Supportive & Assistive Therapies |

| Oral |

| Intrathecal |

| Intravenous |

| Neonates (0–6 mo) |

| Pediatrics (6 mo–12 y) |

| Adolescents (12–18 y) |

| Adults (>18 y) |

| Hospital Pharmacies |

| Specialty Clinics |

| Online & Retail Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Type 0 | |

| Type 1 | ||

| Type 2 | ||

| Type 3 | ||

| Type 4 | ||

| By Treatment Modality | Gene Replacement Therapy | |

| SMN2 Splicing Modifiers | ||

| Antisense-Oligonucleotide Therapy | ||

| Muscle-Directed / Myostatin Inhibitors | ||

| Supportive & Assistive Therapies | ||

| By Route of Administration | Oral | |

| Intrathecal | ||

| Intravenous | ||

| By Age Group | Neonates (0–6 mo) | |

| Pediatrics (6 mo–12 y) | ||

| Adolescents (12–18 y) | ||

| Adults (>18 y) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Clinics | ||

| Online & Retail Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Global Spinal Muscular Atrophy Treatment Market size?

The spinal muscular atrophy therapeutics market is projected to rise from USD 6.06 billion in 2026 to USD 13.48 billion by 2031, delivering a 17.33% CAGR over the period.

Who are the key players in Global Spinal Muscular Atrophy Treatment Market?

Biogen, F. Hoffmann - La Roche Ltd, Cytokinetics, Inc.,, Novartis AG and Catalyst Pharmaceutical are the major companies operating in the Global Spinal Muscular Atrophy Treatment Market.

Why does Asia-Pacific show the fastest growth?

Rising health-insurance coverage, expanding molecular-diagnostic capacity, and government incentives for rare-disease drugs drive a 18.96% CAGR for Asia-Pacific through 2031.

Which therapy class currently holds the largest revenue share?

SMN2 splicing modifiers led with 42.35% market share in 2025, supported by established safety profiles and applicability across all SMA types.

Page last updated on: