Spine Biologics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 5.14 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

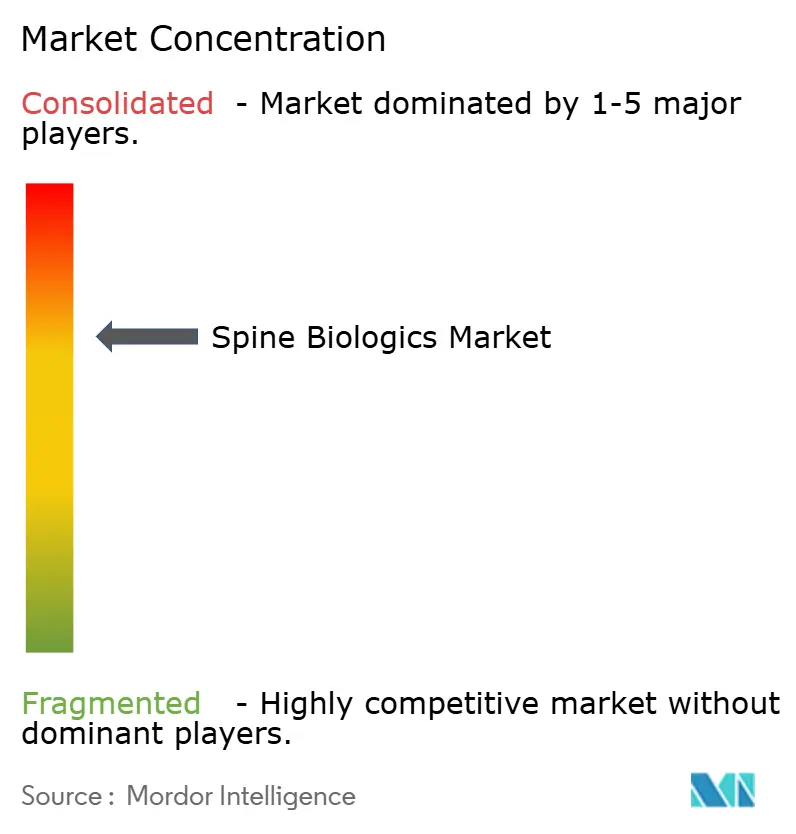

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spine Biologics Market Analysis by Mordor Intelligence

The Spine Biologics market size is expected to grow from USD 3.82 billion in 2025 to USD 4.01 billion in 2026 and is forecast to reach USD 5.14 billion by 2031 at 5.08% CAGR over 2026-2031.

Expansion reflects a clear shift away from autograft-only spine fusion toward advanced biological formulations that shorten operating times, reduce donor-site morbidity and improve fusion reliability. Population aging continues to raise the incidence of degenerative spine disease, while outpatient-friendly minimally-invasive techniques are urging surgeons to adopt fast-setting biologics that suit ambulatory surgical centers. Regional momentum differs: North America remains the revenue leader, yet Asia-Pacific grows meaningfully faster on the back of robust infrastructure upgrades and rising surgical volumes. Competitive intensity is moderate; three firms—Medtronic, Johnson & Johnson and NuVasive—control a decisive share, though ongoing mergers and new peptide-based entrants are redrawing rank order. Reimbursement scrutiny and safety alerts around certain recombinant proteins temper adoption, creating a parallel push toward synthetic peptides, 3-D printed scaffolds and rigorously screened allografts.

Key Report Takeaways

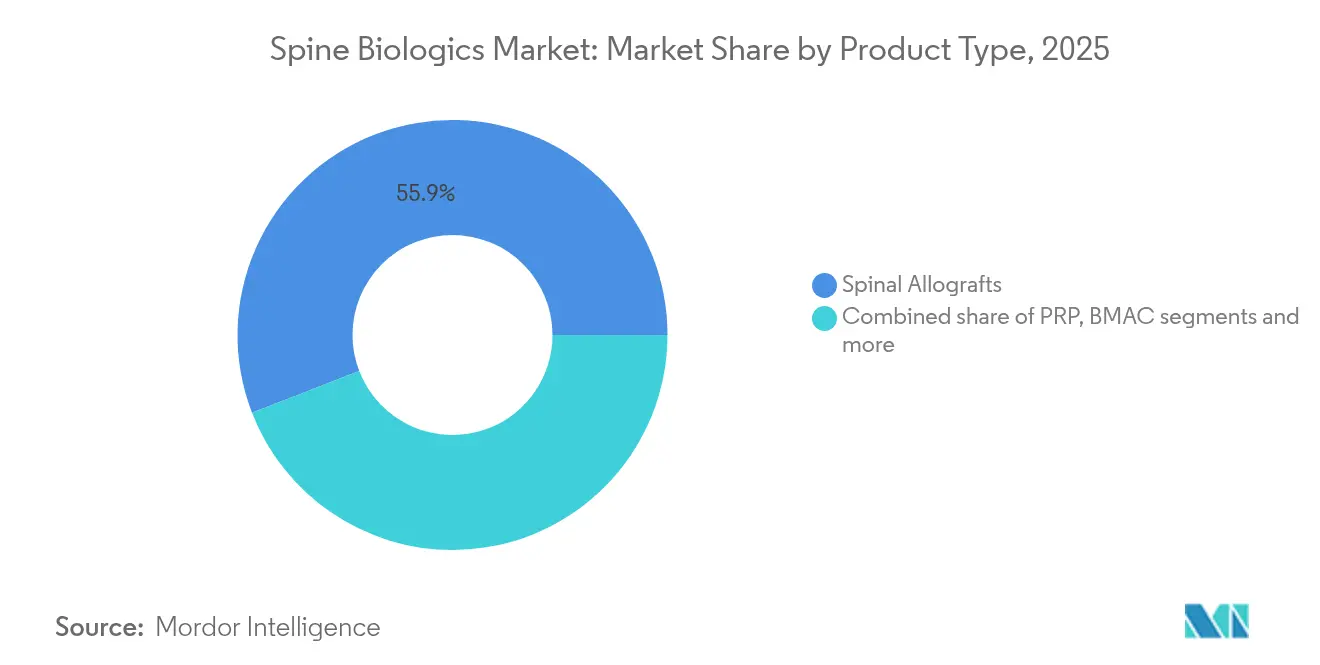

- By product type, spinal allografts led with 55.88% spine biologics market share in 2025, whereas cell-based matrices are projected to record the 6.55% CAGR through 2031.

- By surgery type, anterior cervical discectomy and fusion accounted for 34.97% of the spine biologics market size in 2025, while minimally invasive transforaminal lumbar interbody fusion shows the fastest growth, with 6.32% CAGR to 2031.

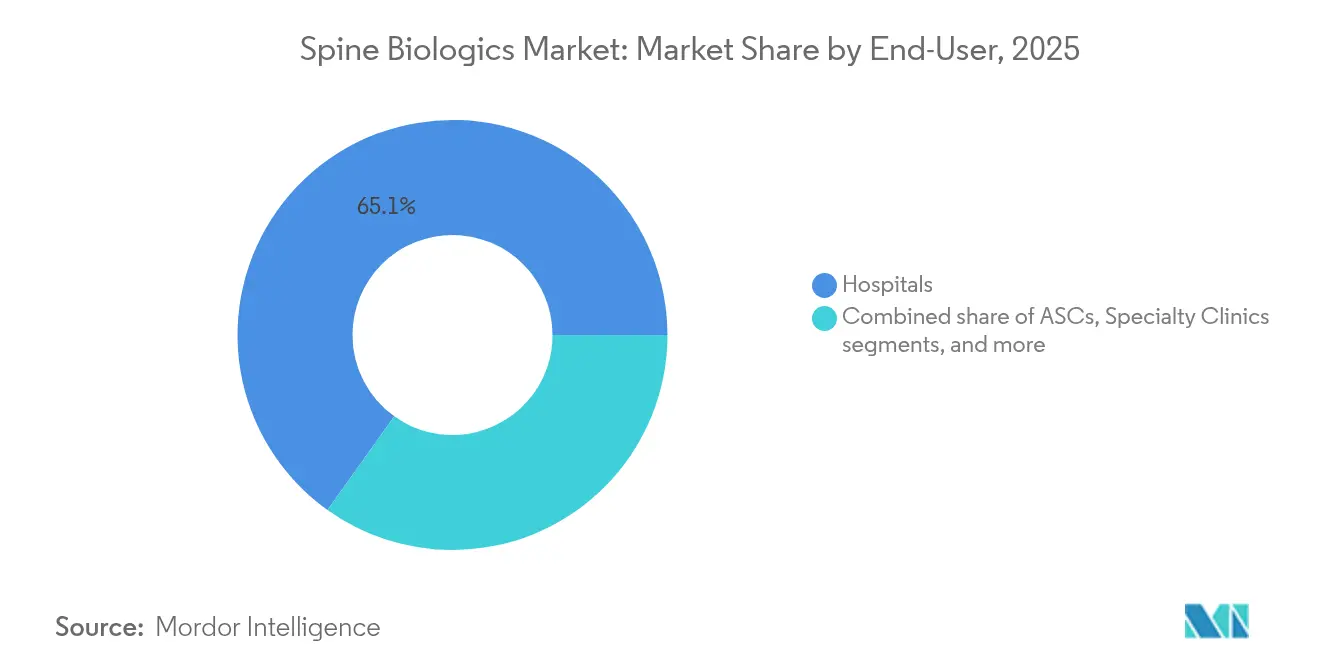

- By end-user, hospitals retained a 65.12% share in 2025; ambulatory surgical centers are expanding at 6.08% CAGR due to average USD 2,000–3,500 per-case savings.

- By region, North America remained the largest contributor with 41.98 % of the spine biologics market size in 2025, whereas Asia-Pacific is forecast to grow at a 6.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Spine Biologics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population with degenerative spine disorders | +1.8% | Global, with highest impact in Asia-Pacific and North America | Long term (≥ 4 years) |

| Surge in minimally-invasive spine procedures | +1.5% | North America & EU leading, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rising prevalence of spinal deformities & trauma | +1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Rapid ASC adoption demanding fast-setting biologics | +1.1% | North America core, emerging in EU and select Asia-Pacific markets | Short term (≤ 2 years) |

| Regulatory approvals of next-gen BMPs | +0.8% | North America & EU primary, gradual Asia-Pacific adoption | Long term (≥ 4 years) |

| 3-D bioprinted patient-specific grafts | +0.4% | North America & EU early adoption, limited Asia-Pacific penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population with Degenerative Spine Disorders

More individuals live beyond 65 and present multi-level degenerative pathology, underpinning recurrent demand across the spine biologics market. In China, annual spine surgery volumes surged 12.32% between 2003 and 2016, with mean patient age rising by almost five years. Older bone biology imposes longer healing times, so surgeons increasingly prefer recombinant proteins and cellular matrices with stronger osteoinductive cues. Osteoporosis-related complications already influence 80% of Latin American spine practices, illustrating demographic reach. Manufacturers respond with lower-dose, collagen-binding BMPs and stem-cell-enriched matrices that compensate for poor host biology. As aging intersects with lifestyle-related disc degeneration in urban Asia-Pacific, overall procedure volumes—and biologic graft consumption—remain on an upward path over the entire forecast window.

Surge in Minimally-Invasive Spine Procedures

More fusions now rely on tubular retractors and endoscopic corridors that limit graft volume and visibility. Among Medicare beneficiaries, spine cases in ambulatory surgical centers climbed 193%[1]Alex K. Miller, “Growing Utilization of Ambulatory Spine Surgery in Medicare Patients from 2010–2021,” NASS Open Access, nassopenaccess.org while hospital outpatient volumes grew 9.9% in the same period. Shorter incisions necessitate biologics that deliver rapid, predictable fusion in smaller packages, catalyzing R&D in moldable putties and ready-to-use strip formats. Cost models reinforce the trend: minimally-invasive pathways trim 9.6% from 45-day episode costs, translating to USD 2,563 in average savings. Robotic navigation further standardizes implant alignment, prompting graft makers to develop cartridges and syringes that integrate with power-assisted delivery arms. The blended effect is a durable boost to demand for premium yet workflow-friendly biologics across the spine biologics market.

Rising Prevalence of Spinal Deformities & Trauma

Rising deformity and trauma volumes stem from lifestyle changes, workplace strain and better imaging that spots conditions once missed, pushing surgeons toward biological grafts rather than traditional bone harvests. Revision operations, where earlier fusions have failed, particularly benefit from cellular bone matrices that delivered 95.3% fusion[2]Daniel K. Park, “Twenty-Four-Month Interim Results from a Prospective, Single-Arm Clinical Trial Evaluating the Performance and Safety of Cellular Bone Allograft in Patients Undergoing Lumbar Spinal Fusion,” BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com at 24 months in prospective trials, outperforming standard graft options. Modern trauma algorithms now build biologic augmentation into first-line care, shifting practice from a reactive patch to a planned regenerative strategy. The financial hit of a failed spinal fusion—each revision costs an average USD 23,702—gives hospitals a clear incentive to invest in premium biologics that cut repeat surgery risk. Younger trauma patients feel the greatest impact because they need constructs that last for decades, so clinicians increasingly favour next-generation biologics designed for durable, lifelong stability.

Regulatory Approvals of Next-Gen BMPs

After a decade of caution, the FDA has started granting breakthrough status to safer osteoinductive proteins such as Renovos’ nanoclay-bound BMP and Amphix Bio’s peptide analog. Collagen-binding domains keep proteins local, enabling half-dose protocols that slash ectopic bone risks reported in earlier formulations. Six-year follow-up data on peptide-based i-FACTOR revealed 98.6% fusion while sidestepping inflammatory complications. Regulatory harmonization in Europe speeds CE marking, letting suppliers roll out kits in multiple regions concurrently. Although reimbursement negotiations remain tough, new coding pathways for “synthetic osteoinductive peptide” solutions mark a turning point and bolster the long-term growth trajectory of the spine biologics market.

Restraints Impact Analysis of Spine Biologics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & limited reimbursement | -1.4% | Global, most severe in emerging markets | Medium term (2-4 years) |

| Safety concerns around recombinant proteins | -0.9% | North America & EU primary, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Tissue-donor supply bottlenecks | -0.7% | Global, acute in North America | Short term (≤ 2 years) |

| Surgeon learning curve for cell-based matrices | -0.5% | Global, concentrated in markets with rapid technology adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost & Limited Reimbursement

Payers increasingly demand head-to-head cost-effectiveness data before approving expensive biologics add-ons in elective spine surgery. Medicare bundling has compressed separate billing for recombinant proteins, while several private insurers list BMP-2 as “investigational” for one-level cervical fusions. In emerging economies, list prices already consume a high proportion of procedure budgets, curbing adoption outside Tier-1 hospitals. Economic modeling shows revision surgeries for failed fusions average USD 23,702, yet insurers often focus on immediate invoice totals rather than downstream savings. These dynamics restrict premium uptake and lower the achievable CAGR for the spine biologics market over the medium term.

Safety Concerns Around Recombinant Proteins

Post-marketing surveillance uncovered adverse events ranging from ectopic bone growth to inflammatory edema, leading surgeons to limit dosage or abandon recombinant proteins for specific indications. The 2023 CDC alert on tuberculosis-contaminated allografts, which affected 36 recipients in 13 centers, renewed attention on biologic safety. Although tissue banks upgraded culture protocols and BMP makers reformulated carriers, some clinicians remain cautious, particularly for cervical work, where airway swelling can be catastrophic. Publicity around 44.4% revision-rate statistic in adverse-event filings for BMP-2 maintains scrutiny. The reputational drag reduces overall utilization, thereby shaving CAGR potential from the spine biologics market in mature economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Spine Biologics Market Segment Analysis

By Product Type:

Allografts Retain Lead While Cell-Based Matrices AccelerateAllografts captured 55.88% of spine biologics market share in 2025, reflecting stable reimbursement and long clinical track records that keep surgeons loyal to demineralized bone matrix sheets and machined cortical spacers. Within this pool, processed structural grafts dominate because standard dimensions streamline instrument pairing and reduce theatre time. Manufacturers refine freeze-drying techniques that preserve osteoinductive proteins, further defending share within the spine biologics market.

Cell-based matrices, however, are posting the fastest growth, with a 6.55% CAGR to 2031. Mesenchymal stem cell-seeded putties showed 100% fusion in prospective trials, outperforming legacy grafts and drawing interest at high-miss centers managing smokers and osteoporotic patients. Peptide-enhanced synthetics such as i-FACTOR deliver 98.6% six-year fusion while bypassing recombinant protein complications, signalling a near-term pivot. Synthetic ceramics and bioactive glass, boosted by 3D printing that permits patient-specific porosity, extend options for surgeons seeking fully mineral solutions. Collectively these innovations are reshaping buying algorithms across the spine biologics market.

By Surgery Type:

ACDF Dominates but Minimally-Invasive TLIF SurgesAnterior cervical discectomy and fusion comprised 34.97% of the 2025 spine biologics market size. Its confined corridor allows surgeons to pack demineralized chips or BMP-soaked sponges with predictable radiographic union, sustaining leadership in the spine biologics market share. Demand also stems from a rising base of office workers with cervical disc herniation, which feeds patient flow into one- or two-level ACDFs.

Transforaminal lumbar interbody fusion is the fastest riser, with a 6.32% CAGR over the forecast period, thanks to expandable titanium cages that need moldable biologics to backfill graft windows. MIS-TLIF volume growth aligns with outpatient migration, sparking the usage of preloaded syringe kits that set within minutes and permit same-day discharge. Posterior lumbar interbody fusion and extreme lateral interbody fusion segments likewise pivot to faster, lower-dose proteins optimized for tubular access. Taken together, these shifts place a premium on handling and kinetics throughout the spine biologics market.

By End-User:

Hospitals Command but ASCs Gain GroundHospitals generated 65.12% of the spine biologics market size, given their capacity to manage complex, multilevel cases requiring intraoperative neuromonitoring and extensive biologic combinations. Integrated trauma centers also hold most acute burst and fracture surgeries that consume sizeable graft volumes. Hospital buying groups continue to negotiate tiered contracts that bundle plates, screws and biologics, sustaining their procurement leverage within the spine biologics market.

Ambulatory surgical centers, though smaller today, are recording the fastest growth, with a 6.08% CAGR to 2031, as they increasingly perform single-level lumbar and two-level cervical fusions. Payment models reward procedures completed under eight hours with same-day discharge, driving ASC surgeons toward fast-setting synthetics that cut anesthesia time. Specialty spine clinics blend outpatient efficiencies with boutique care, often deploying cutting-edge cellular matrices as a market differentiator. Academic institutes remain vital to first-in-human trials, shaping the next wave of spine biologics market entrants even if their direct purchasing stays modest.

Geography Analysis

North America Spine Biologics Market

North America presently generates 41.98% of the global spine biologics market share. Widespread insurance coverage for elective spine interventions, paired with robust ASC penetration, sustains high biologic use per capita. Mature reimbursement, however, slows value growth to 4.29% CAGR as cost-containment policies and safety debates restrain premium adoption.

APAC Spine Biologics Market

Asia-Pacific records the strongest 6.21% CAGR, driven by rising life expectancy, middle-class expansion, and hospital investment across China, India, and Southeast Asia. China alone experienced a 12.32% average annual rise in spine surgeries, fueling graft demand that now outpaces global averages. Japan and Australia bring sophisticated regulatory frameworks that clear advanced peptides and 3-D printed scaffolds, while emerging ASEAN countries emphasize cost-sensitive synthetics and locally processed allografts.

Europe Spine Biologics Market

Europe posts a 4.91% growth rate, balancing stringent MDR compliance costs with consistent procedure volume in Germany, France, and the United Kingdom. CE mark alignment grants suppliers access across 27 states, yet reimbursement differs by payer, nudging firms toward tiered product lines.

LATAM Spine Biologics Market

Latin America shows a 5.39% trajectory as Brazil and Argentina update trauma guidelines to include biologic augmentation, though currency volatility modulates average selling prices.

MEA Spine Biologics Market

Middle East and Africa achieve 5.73% growth through medical tourism in the Gulf and state-funded centers in South Africa, albeit from a lower starting base.

Competitive Landscape

The spine biologics market exhibits moderate consolidation. Medtronic’s large share comes from a broad BMP, allograft and synthetic ceramic portfolio that aligns with its enabling technologies. Johnson & Johnson’s Depuy Synthes contributes 16% via its ViviGen cellular matrix and FiberCel strips. NuVasive held 13% until Globus Medical disclosed a USD 615.5 million takeover that will vault the combined entity to second place by revenue.

Strategic moves center on ecosystem integration. Medtronic’s AiBLE platform couples AI planning, robotics and surface-modified implants with proprietary grafts, locking hospitals into a procedural suite that protects consumable pull-through. Stryker divested[4]Stryker Corporation, “Stryker Completes Sale of U.S. Spinal Implants Business,” Stryker, investors.stryker.com its US spine implants franchise to VB Spine, freeing capital to deepen robotics and cranial portfolios while licensing its Mako guidance know-how to the new buyer. Meanwhile, Cerapedics, Renovos and Amphix Bio leverage FDA breakthrough status to speed synthetic peptide entries and carve niches around lower-dose, high-safety constructs.

Technology frontiers include 3-D bioprinted, patient-matched scaffolds and nano-coated carriers that trigger stem-cell homing. Patent filings covering hybrid ceramic-peptide compositions rose 27% in 2024, signalling intensified R&D investment. Manufacturers increasingly sign risk-sharing contracts where biologic cost is rebated if radiographic union lags, echoing value-based care norms. Vendors that can merge clinical efficacy, procedural efficiency and documented cost savings are poised to capture incremental wallet share across the spine biologics market.

Spine Biologics Industry Leaders

Arthrex Inc.

Globus Medical

Johnson & Johnson Services, Inc.

Medtronic plc

Zimmer Biomet Holdings

- *Disclaimer: Major Players sorted in no particular order

Spine Biologics Market Companies Covered in this Report

- AlloSource

- Alphatec Holdings

- Arthrex

- B. Braun

- Baxter

- BioHorizons Vivigen

- Biosenic SA

- CoreLink Holdings, LLC

- Globus Medical

- Highridge Inc.

- Johnson & Johnson

- Kuros Biosciences

- Medtronic

- Orthofix

- RTI Surgical Holdings

- SeaSpine Holdings

- Spinal Elements, Inc.

- Spine Wave Inc.

- Stryker

- Tissue Regenix Group

- Xtant Medical Holdings

- Zimmer Biomet

Recent Industry Developments in Spine Biologics Market

- February 2025: Globus Medical announced acquisition of Nevro Corp. for USD 250 million to add spinal cord stimulation and pain management assets.

- February 2025: Medtronic purchased Nanovis nano-texture technology to enhance implant osseointegration.

- January 2025: Stryker completed the sale of its US spine implants division to Viscogliosi Brothers, forming VB Spine with exclusive access to Mako Spine and Copilot systems.

- October 2024: Amphix Bio received FDA breakthrough designation for its bone regeneration peptide product.

Spine Biologics Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the spine biologics market as the worldwide sales of bone-graft substitutes, spinal allografts, cell-based matrices, platelet-rich plasma, bone-marrow aspirate concentrates, and related biologic adjuncts that actively facilitate spinal fusion or reconstructive procedures. These products differ from traditional metal implants because they stimulate de novo bone growth and shorten recovery times.

Scope Exclusions: Orthopedic biologics used in joints other than the spine and purely mechanical fixation devices lie outside this assessment.

Segments Covered in This Report

- By Product Type

- Bone Graft Substitutes

- Bone Morphogenetic Proteins

- Synthetic Ceramics & Bioactive Glass

- Peptide-based & PTH-enhanced Grafts

- Spinal Allografts

- Machined Structural Allografts

- Demineralized Bone Matrix (DBM)

- Cellular Bone Matrices

- Cell-Based Matrices

- Platelet-Rich Plasma (PRP)

- Bone Marrow Aspirate Concentrate (BMAC)

- Others

- Bone Graft Substitutes

- By Surgery Type

- Anterior Cervical Discectomy & Fusion (ACDF)

- Transforaminal/Posterior Lumbar Interbody Fusion (TLIF/PLIF)

- Anterior/Extreme Lumbar Interbody Fusion (ALIF/XLIF)

- Minimally-Invasive Posterolateral Fusion

- Cervical Disc Replacement with Biologics Adjuncts

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed spine surgeons, biomaterial scientists, and hospital procurement managers across North America, Europe, Asia-Pacific, and Latin America; their insights validated utilization rates, discount structures, and emerging cell-based innovations. Additional surveys of ambulatory surgical-center administrators gauged the shift of fusion cases from inpatient to outpatient settings.

Desk Research

We first compiled procedure and patient volumes from public sources such as the WHO Global Health Observatory, the U.S. CDC National Spinal Cord Injury Database, and Eurostat hospital discharge records, which anchor regional demand patterns. Regulatory clearance data, notably FDA 510(k) summaries and EMEA device recalls, helped us enumerate marketed product classes and average selling prices. Trade association briefs from the International Society for the Advancement of Spine Surgery and import-export codes from UN Comtrade clarified cross-border product flows, while company filings gathered via D&B Hoovers offered revenue benchmarks. These sources, together with peer-reviewed articles in Spine Journal and Biomaterials, informed prevalence, pricing, and clinical-efficacy assumptions. The list above is illustrative rather than exhaustive.

Market-Sizing & Forecasting

A top-down model began with country-level spinal fusion procedure counts, which are then multiplied by biologic penetration ratios and calibrated against import values and reimbursement fee schedules. Supplier roll-ups and sampled ASP × volume checks provided a bottom-up sense check before results were finalized. Key variables include aging population growth, degenerative disc prevalence, ASC case-mix migration, recombinant BMP approval timelines, and median selling prices by product class. Multivariate regression (with age cohort size, procedure intensity, and ASP trend as predictors) underpins the 2025-2030 forecast, and gaps in bottom-up estimates are bridged using three-year moving averages of hospital billing data.

Data Validation & Update Cycle

Outputs undergo variance tests against historical sales, external shipment statistics, and expert comment. Senior analysts review anomalies before sign-off; the dataset refreshes annually, with interim updates triggered by major approvals or recalls, after which we rerun the whole model so clients always receive the latest viewpoint.

How Mordor Intelligence's Spine Biologics Market Size Compares to Other Published Estimates

Published numbers often diverge because firms pick different product baskets, pricing ladders, or refresh cadences, and some rely on single-source estimates that travel unchallenged.

Key Gap Drivers: certain publishers exclude platelet-rich plasma, freeze ASPs at launch-year levels, or omit ambulatory settings; others extrapolate older trends without reconciling them to the surge in minimally invasive TLIF cases. Mordor's scope includes all relevant biologic classes, adjusts prices by weighted channel mix, and applies a twelve-month refresh, producing a steadier baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.82 B (2025) | Mordor Intelligence | - |

| USD 2.30 B (2024) | Global Consultancy A | Narrower product scope, excludes cell matrices, limited Asia coverage |

| USD 3.25 B (2024) | Industry Portal B | Uses list prices, no ASC channel adjustment |

| USD 4.42 B (2024) | Market Data Publisher C | Assumes universal biologic uptake, applies aggressive currency conversion |

In sum, by combining transparent data loops, consistent scope, and timely refreshes, Mordor Intelligence delivers a balanced, decision-ready baseline that executives can trace back to clear variables and reproducible steps.

Key Questions Answered in the Report

Why are ambulatory surgical centers central to spine biologics adoption?

They favor fast-setting, ready-to-use grafts that align with cost savings and same-day discharge workflows.

How are AI and robotics shaping product requirements for spine biologics?

Integrated platforms such as Medtronic’s AiBLE pair navigation with cartridge-based graft delivery, prompting suppliers to design biologics compatible with precision guidance systems.

What steps are manufacturers taking to improve the safety profile of recombinant proteins?

Next-generation formulations use collagen-binding domains and peptide analogs that localize dosing and cut ectopic bone risks while maintaining fusion efficacy.

Which regulatory actions are accelerating innovation in spine biologics?

FDA breakthrough device designations for companies like Renovos and Amphix Bio shorten approval timelines for advanced osteoinductive peptides and nanoclay carriers.

How does population aging influence demand for spine biologics?

A growing cohort of patients over 65 presents bone-healing challenges that drive surgeon preference for biologics with enhanced osteoinductive properties.

In what way are cost pressures altering supplier strategies in this market?

Vendors increasingly bundle biologics with value-based contracts and risk-sharing guarantees that tie payment to confirmed fusion outcomes.

Page last updated on: