Duchenne Muscular Dystrophy Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

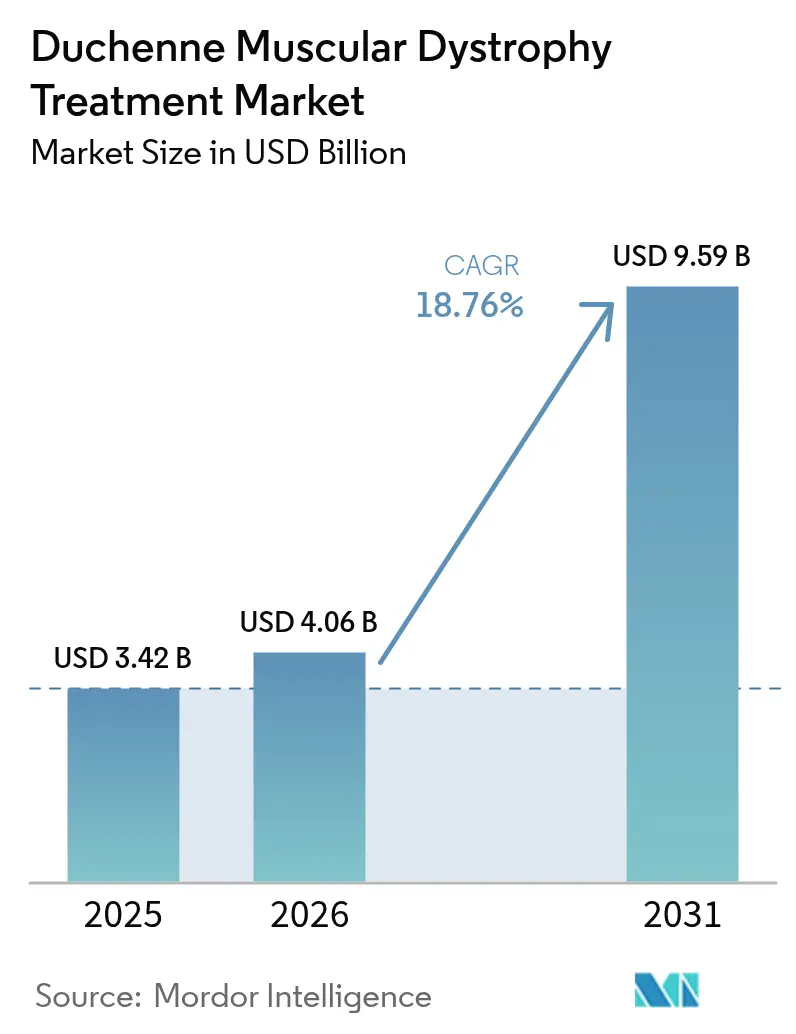

| Market Size (2026) | USD 4.06 Billion |

| Market Size (2031) | USD 9.59 Billion |

| Growth Rate (2026 - 2031) | 18.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Duchenne Muscular Dystrophy Treatment Market Analysis by Mordor Intelligence

Duchenne muscular dystrophy treatment market size in 2026 is estimated at USD 4.06 billion, growing from 2025 value of USD 3.42 billion with 2031 projections showing USD 9.59 billion, growing at 18.76% CAGR over 2026-2031. Breakthrough gene therapies, regulatory acceleration, and sustained venture investment are redefining therapeutic standards, shifting care from palliative regimens toward durable disease-modifying interventions. The FDA’s broadened approval of delandistrogene moxeparvovec for children aged 4 and older, the first-in-class non-steroidal agent givinostat, and the corticosteroid alternative vamorolone together underpin a multimodal ecosystem where molecular approaches dominate [1]U.S. Food and Drug Administration, “FDA Approves Expanded Indication for Gene Therapy in Duchenne Muscular Dystrophy,” fda.gov . Investor appetite remains robust as platform technologies mature, illustrated by record capital raises for oligonucleotide and CRISPR innovators. Competitive realignment, sparked by program discontinuations among larger firms, has opened white-space opportunities for emerging players while intensifying focus on scalable vector manufacturing. Geographic momentum centers on Asia-Pacific, where regulators in Japan and China have accelerated reviews, positioning the region for above-average revenue growth and diversified clinical trial activity.

Key Report Takeaways

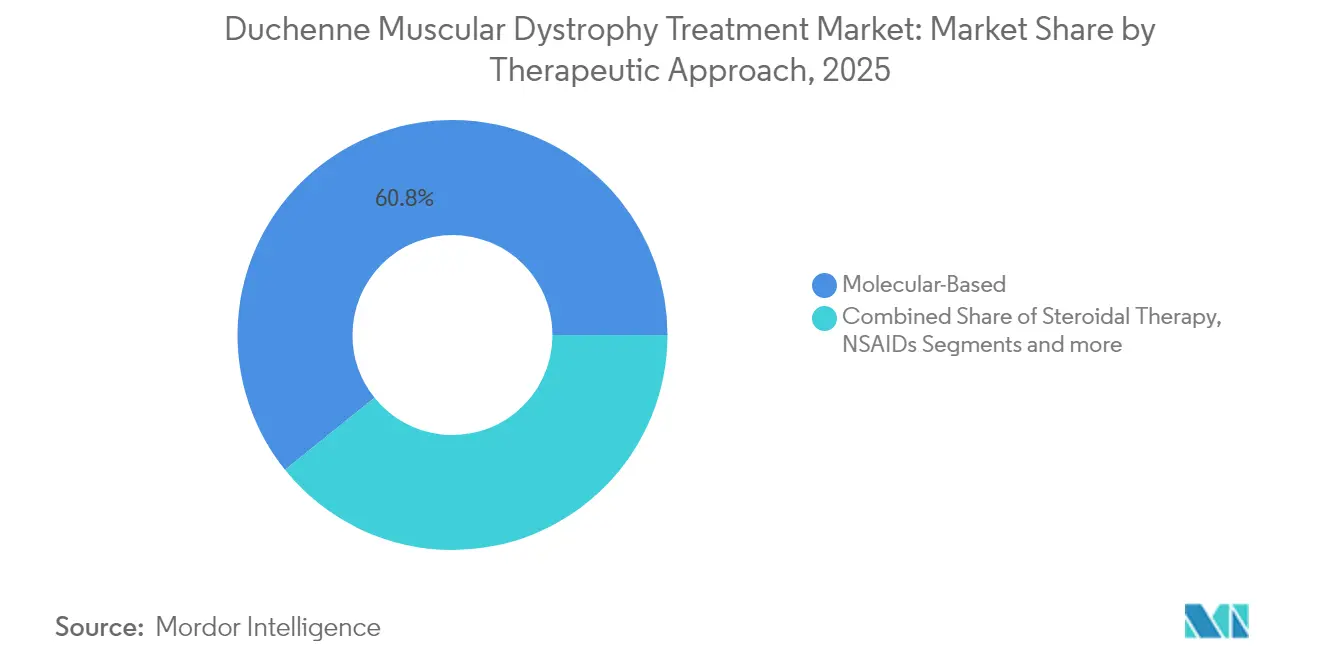

- By therapeutic approach, molecular-based products held 60.78% of Duchenne muscular dystrophy treatment market share in 2025, while they are forecast to post a 19.42% CAGR through 2031.

- By route of administration, the intravenous segment accounted for 51.68% of the Duchenne muscular dystrophy treatment market size in 2025; the subcutaneous segment is projected to advance at 19.37% CAGR to 2031.

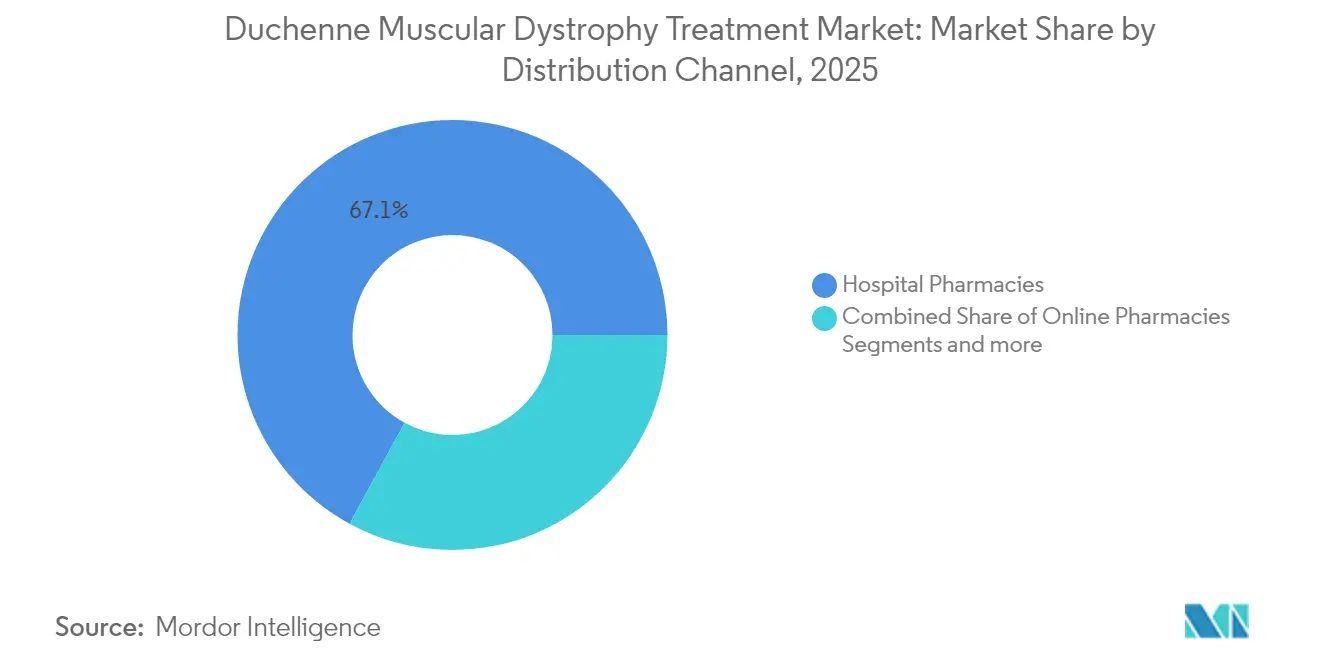

- By distribution channel, hospital pharmacies commanded 67.05% of Duchenne muscular dystrophy treatment market share in 2025, whereas online pharmacies will likely record the fastest 19.55% CAGR through 2031.

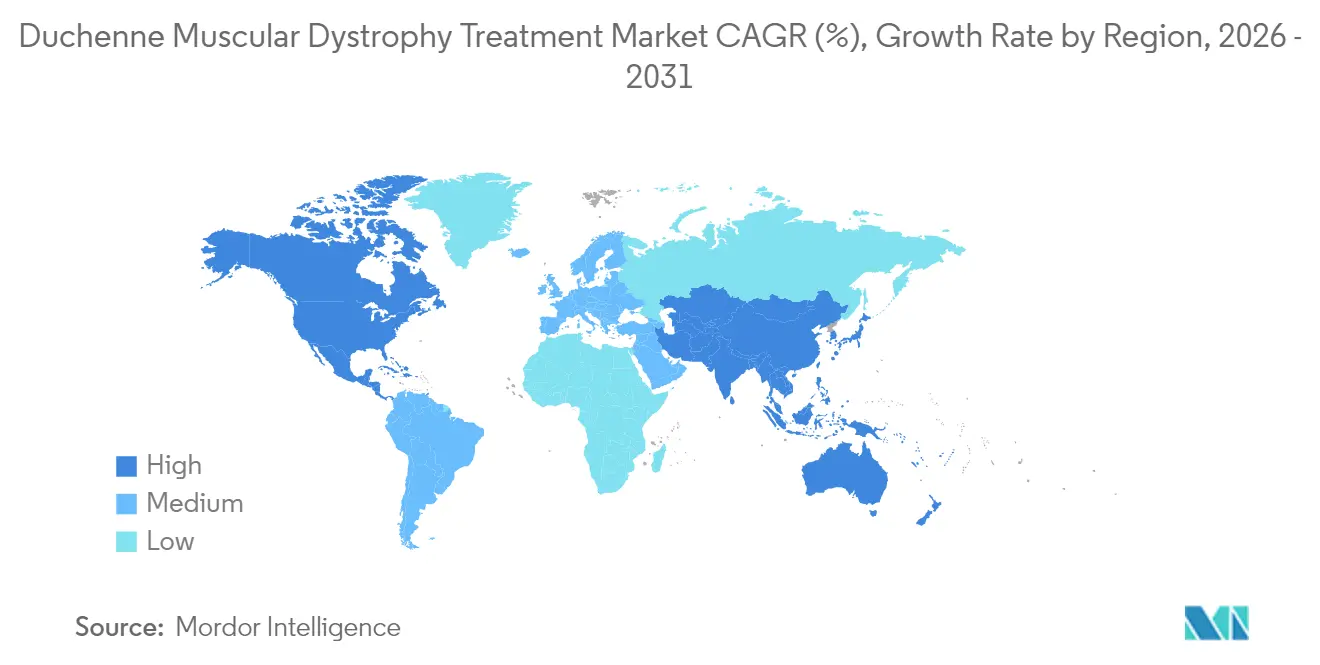

- By geography, North America led with 41.11% revenue share in 2025, while Asia-Pacific is on track for the highest 19.61% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Duchenne Muscular Dystrophy Treatment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disease burden of DMD | +3.2% | Global | Long term (≥ 4 years) |

| Increasing investments in novel therapies | +4.1% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Approval momentum for antisense exon-skipping drugs | +2.8% | Global, with early gains in US, EU, Japan | Short term (≤ 2 years) |

| Orphan-drug incentives & priority review vouchers | +2.3% | North America & EU core | Medium term (2-4 years) |

| CRISPR platform deals accelerating gene-editing pipelines | +3.5% | Global, concentrated in US, China | Long term (≥ 4 years) |

| Decentralised trials improving patient recruitment | +1.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disease Burden of DMD

Growing recognition that 1 in 3,500-6,000 male births are affected has prompted national registries and newborn screening programs that enlarge trial-eligible populations and encourage earlier therapeutic intervention [2]Ulrike Schara-Schmidt, “Epidemiology and Survival in Duchenne Muscular Dystrophy,” Springer, springer.com . Point prevalence studies in England now cite 3.23 cases per 100,000, while direct medical costs rise nearly three-fold as patients transition from ambulatory to ventilator-assisted stages. Life expectancy improvements—from 18.2 years for those born before 1970 to 24 years for the 1990-1999 cohort—extend treatment duration and amplify market demand.

Increasing Investments in Novel Therapies

Venture and strategic capital continue to flow; CureDuchenne has catalyzed over USD 3 billion in follow-on funding since 2014, and Dyne Therapeutics secured USD 300 million in a single 2024 raise. Collaborations such as Sarepta-Arrowhead for siRNA and Sanofi-Fulcrum on epigenetic modulation illustrate big-pharma commitment to rare-disease portfolios, while philanthropic venture arms remain vital to early discovery [3]Sarepta Therapeutics, “Launch of Gene Editing Innovation Center,” sarepta.com .

Approval Momentum for Antisense Exon-Skipping Drugs

Four exon-skipping agents are already on the US market, and additional candidates are nearing submissions. Wave Life Sciences plans an accelerated filing for WVE-N531 after 48-week data showed sustained dystrophin expression with a 61-day tissue half-life. The FDA and EMA now accept dystrophin expression as a surrogate biomarker, enabling compressed timelines and lower development risk relative to historical standards.

Orphan-Drug Incentives & Priority Review Vouchers

The Rare Pediatric Disease voucher attached to givinostat in 2024 fetched secondary-market valuations in the hundreds of millions, creating a self-reinforcing capital loop where voucher proceeds finance additional pipeline assets. Seven-year exclusivity and clear guidance issued in 2025 underpin sponsor willingness to advance high-risk programs.

Restraints Impact Analysis of Duchenne Muscular Dystrophy Treatment Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of standardised clinical efficacy endpoints | -2.1% | Global | Medium term (2-4 years) |

| High therapy cost & reimbursement hurdles | -3.4% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Manufacturing bottlenecks for high-dose AAV vectors | -2.8% | Global, concentrated in US & EU production hubs | Short term (≤ 2 years) |

| Regulatory uncertainty on off-target gene editing | -1.9% | Global, most pronounced in US & China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardised Clinical Efficacy Endpoints

Variability in biomarkers such as creatine kinase complicates cross-study comparisons, prompting validation efforts for alternatives like urinary N-terminal titin, which correlates more closely with microdystrophin expression. Divergent FDA and EMA guidance adds planning complexity, while updated pediatric gait classifications expose gaps between historical outcome measures and contemporary standards.

High Therapy Cost & Reimbursement Hurdles

One-time gene therapies priced above USD 3 million strain payer budgets, and prior-authorization criteria frequently confine coverage to narrow subgroups. Value-based agreements and installment models are emerging, yet logistical challenges in post-market data capture have slowed adoption, limiting access especially across middle-income nations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Duchenne Muscular Dystrophy Treatment Market Segment Analysis

By Therapeutic Approach:

Molecular Strategies Sustain OutperformanceMolecular-based interventions generated the largest contribution to 2025 revenue, representing 60.78% of the Duchenne muscular dystrophy treatment market. That segment is projected to expand at 19.42% CAGR to 2031 on the back of first-to-market gene therapies, increasingly efficient exon-skipping chemistries, and emerging read-through agents. The Duchenne muscular dystrophy treatment market size for molecular categories is poised to reach USD 5.93 billion by 2031, reflecting sustained reimbursement for delandistrogene moxeparvovec and pipeline maturation among CRISPR constructs. Mutational-suppressing approaches continue to benefit from expanded labeling, while dystrophin-expressing chimeric cells are progressing through early trials without reliance on viral vectors.

Competitive dynamics within molecular modalities hinge on differentiated dystrophin expression; DYNE-251 delivered 3.71% expression versus 0.3% from legacy eteplirsen in head-to-head assessments. Manufacturing innovation remains a gating factor, yet recent optimizations in poly-A sequencing and transgene cassette architecture are lifting functional yields per liter of bioreactor capacity. Steroidal and non-steroidal anti-inflammatories retain a complementary role, particularly where gene therapy access is delayed, preserving revenue baselines for chronic care protocols and underpinning combination-therapy investigation.

By Route of Administration:

Convenience Shifts Toward SubcutaneousIntravenous infusions dominated with 51.68% share in 2025, reflecting hospital-based delivery of high-dose viral vectors central to current standards. While IV remains indispensable for full-length or micro-dystrophin constructs, the subcutaneous channel is projected to post a 19.37% CAGR as self-injectable oligonucleotides and antibody-fragment carriers gain regulatory traction. The Duchenne muscular dystrophy treatment market size for subcutaneous formulations could surpass USD 2.22 billion by 2031, unlocking outpatient care pathways that alleviate facility congestion and improve adherence.

Drug-device combination innovations—ranging from wearable autoinjectors to depot-forming polymers—are expanding candidate compatibility with subcutaneous routes. Oral agents, catalyzed by the 2024 approval of givinostat, maintain relevance for adjunctive therapy and early-stage intervention; ongoing research into skeletal-muscle-selective inhibitors aims to delay functional decline without the immunogenicity concerns attributable to viral vectors.

By Distribution Channel:

Digital Platforms Accelerate Rare-Disease AccessHospital pharmacies retained 67.05% share in 2025, justified by stringent handling protocols, companion diagnostics, and complex reimbursement workflows. Nonetheless, online specialty networks are expected to grow 19.55% annually as integrated patient-support portals streamline prior authorization, cold-chain logistics, and remote monitoring. The Duchenne muscular dystrophy treatment market share held by digital pharmacies may double by 2031, supported by insurer acceptance of mail-order gene therapies packaged with telehealth oversight.

SareptAssist and analogous programs illustrate how manufacturers are re-engineering distribution into full-service ecosystems encompassing genetic counseling, virtual physical therapy, and financial navigation. Retail pharmacies continue to service corticosteroid refills but face ceiling effects absent scope expansion into advanced therapy stewardship.

Geography Analysis

North America Duchenne Muscular Dystrophy Treatment Market

North America led with 41.11% revenue contribution in 2025, buoyed by an established orphan-drug framework, broad private insurance coverage, and venture funding depth. The Duchenne muscular dystrophy treatment market size in the region surpassed USD 1.41 billion, and steady rollout of newborn screening mandates is expected to enlarge the treated population base. Canada and Mexico are adopting harmonized labeling, promoting cross-border treatment continuity while forging local pathways for gene-therapy reimbursement.

APAC Duchenne Muscular Dystrophy Treatment Market

Asia-Pacific is forecast to be the fastest-advancing territory at 19.61% CAGR through 2031. Japan approved delandistrogene moxeparvovec under its regenerative medicine pathway in May 2025, granting seven-year conditional marketing rights. China’s priority review of vamorolone positions the mainland for first-wave uptake once manufacturing transfers conclude, and state-supported CRISPR initiatives are drawing global sponsors into joint ventures for localized production capacity. India, South Korea, and Australia are scaling investigator networks and rare-disease registries, collectively widening clinical trial participation.

Europe Duchenne Muscular Dystrophy Treatment Market

Europe maintains a pivotal role through coordinated regulatory accelerators and dense academic-medical networks. Conditional approval of givinostat in April 2025 underscored the EMA’s willingness to accept surrogate endpoints while stipulating robust post-marketing commitments. Germany and France remain early adopters, backed by statutory insurance schemes that reimburse high-cost therapies under outcomes-based contracts. Eastern European nations are gradually introducing pilot reimbursement projects, anticipating price negotiations once additional therapeutic alternatives reach market.

Competitive Landscape

The Duchenne muscular dystrophy treatment market exhibits moderate consolidation. Sarepta Therapeutics generated more than USD 1 billion in 2025 from its ELEVIDYS franchise, securing early-mover entrenchment and leveraging a network of 60 centers of excellence across three continents. PTC Therapeutics preserves a sizable annuity stream from Emflaza and Translarna, collectively yielding USD 547 million in 2025 revenue and providing a hedge against single-asset risk. Pfizer’s exit from the mini-dystrophin race in late 2024 redistributed investor focus toward mid-cap specialists and unlocked vector capacity for licensors.

Emerging platforms prioritize superior dystrophin expression and patient convenience. Dyne Therapeutics achieved a 3.71% expression benchmark and is preparing a registrational cohort that could underpin filing by early 2026. Edgewise Therapeutics pursues an oral fast skeletal myosin inhibitor targeting muscle-preservation pathways, appealing to steroid-intolerant cohorts. Capricor concentrates on cardiac comorbidity with a cell-derived exosome therapy, addressing an under-served mortality driver even as it confronts regulatory setbacks.

Partnering activity remains brisk as incumbents seek modality diversification; Sarepta licensed Arrowhead’s siRNA portfolio to complement gene replacement, and Sanofi committed USD 80 million upfront to co-develop Fulcrum Therapeutics’ epigenetic regulator. Competitive advantage now turns on manufacturing scalability, tissue specificity, and the ability to bundle patient services that fortify brand loyalty beyond initial infusion.

Duchenne Muscular Dystrophy Treatment Industry Leaders

NIPPON SHINYAKU CO., LTD. (NS Pharma Inc.)

ITALFARMACO S.p.A.

PTC Therapeutics

Santhera Pharmaceuticals

Sarepta Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Duchenne Muscular Dystrophy Treatment Market Companies Covered in this Report

- Sarepta Therapeutics

- PTC Therapeutics

- Nippon Shinyaku (NS Pharma)

- Pfizer

- Italfarmaco

- Santhera Pharmaceuticals

- FibroGen

- BioMarin

- Roche / Genentech

- Wave Life Sciences

- Solid Biosciences

- Dyne Therapeutics

- Edgewise Therapeutics

- Regenxbio

- Alexion (AstraZeneca Rare Disease)

- Genethon

- Eli Lilly and Company

- Dystrogen Therapeutics

- Entrada Therapeutics

Recent Industry Developments in Duchenne Muscular Dystrophy Treatment Market

- May 2025: Sarepta Therapeutics gained Japanese approval for ELEVIDYS in children aged 3-7, its first gene-therapy clearance in the country and delivered through a co-promotion alliance with Chugai.

- April 2025: The European Medicines Agency issued a positive opinion for Duvyzat (givinostat), the first HDAC inhibitor for ambulatory DMD patients aged ≥ 6 years.

- March 2025: Wave Life Sciences confirmed intent to seek accelerated US approval of WVE-N531 after 48-week Phase 2 data showed durable exon-skipping efficacy.

- January 2025: Dyne Therapeutics announced initiation of an expansion cohort for DYNE-251 aimed at supporting an early-2026 accelerated-approval submission.

Global Duchenne Muscular Dystrophy Treatment Market Report Scope

As per the scope of this report, Duchenne muscular dystrophy is a rare genetic disease that causes gradual muscle wasting and weakness, brought on by the X-linked recessive pattern, which causes muscle deterioration. However, it could also be a recent mutation or a parent-passed genetic characteristic. The Duchenne muscular dystrophy treatment market is segmented by therapeutic approaches and geography. By therapeutic approaches, the market is further segmented into molecule-based therapies, steroid therapy, and other therapeutic approaches. The report also covers the market sizes and forecasts for major countries across different regions. The market size is provided for each segment in terms of value (USD).

Segmentation Overview

| Molecular-Based | Mutation Suppressing |

| Exon Skipping | |

| Steroidal Therapy | |

| NSAIDs | |

| Others |

| Intravenous |

| Sub-cutaneous |

| Oral |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapeutic Approach | Molecular-Based | Mutation Suppressing |

| Exon Skipping | ||

| Steroidal Therapy | ||

| NSAIDs | ||

| Others | ||

| By Route of Administration | Intravenous | |

| Sub-cutaneous | ||

| Oral | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Duchenne muscular dystrophy treatment market by 2031?

The market is expected to reach USD 9.59 billion by 2031, growing at a 18.76% CAGR.

Which therapeutic approach currently dominates?

Molecular-based therapies hold 60.78% market share and will likely remain the leading category as gene-replacement and exon-skipping advances mature.

Why is Asia-Pacific the fastest-growing region?

Accelerated approvals in Japan and priority reviews in China, combined with expanding clinical infrastructure, are driving a projected 19.61% CAGR through 2031.

How are reimbursement challenges being addressed?

Payers are piloting value-based contracts, installment payments, and real-world evidence collection to balance high upfront costs with long-term outcomes.

What makes subcutaneous delivery attractive?

Self-administration reduces hospital visits, improves adherence, and is backed by pipeline agents designed for depot or autoinjector platforms, supporting a 19.37% CAGR for this route.

Which companies are emerging challengers to market leaders?

Dyne Therapeutics, Edgewise Therapeutics, and Capricor are leveraging novel mechanisms such as optimized oligonucleotides, muscle-preservation small molecules, and cardiac-targeted exosomes to differentiate from established gene-therapy incumbents.

Page last updated on: