Spinach Seeds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

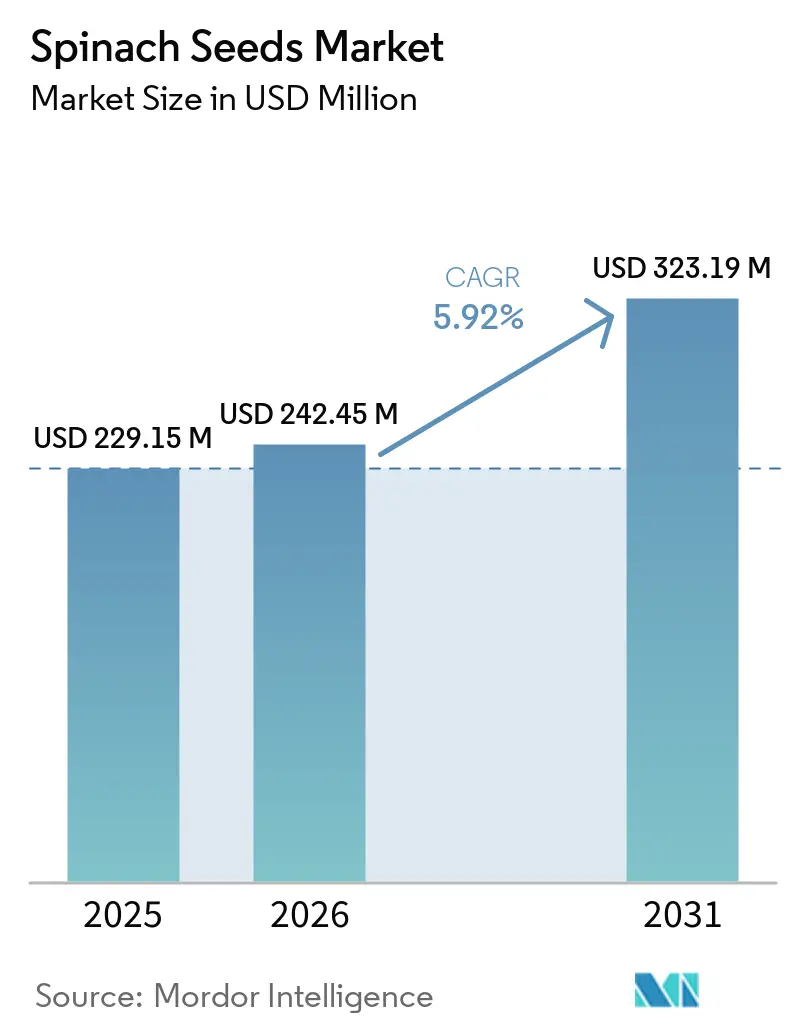

| Market Size (2026) | USD 242.45 Million |

| Market Size (2031) | USD 323.19 Million |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spinach Seeds Market Analysis by Mordor Intelligence

The spinach seeds market size was valued at USD 229.15 million in 2025 and estimated to grow from USD 242.45 million in 2026 to reach USD 323.19 million by 2031, at a CAGR of 5.92% during the forecast period (2026-2031). The spinach seeds market is being reshaped by a decisive move toward disease-resistant hybrid genetics because large commercial growers need stronger field reliability, tighter crop uniformity, and steadier retail fulfillment. That shift is tied to retail demand for year-round babyleaf supply, which has raised the commercial value of varieties that can perform consistently across seasons and production systems. The spinach seeds market also carries a clear supply-side vulnerability because Washington State University researchers confirmed in 2025 that the Pacific Northwest of the United States produces nearly one-fifth of global spinach seed supply, which means a limited number of production zones still carry outsized global importance. The same market is also drawing more investment toward treated seed, hydroponic suitability, and breeding speed, because growers now pay more for seed lots that reduce operational risk in protected systems and under strict buyer specifications.

Key Report Takeaways

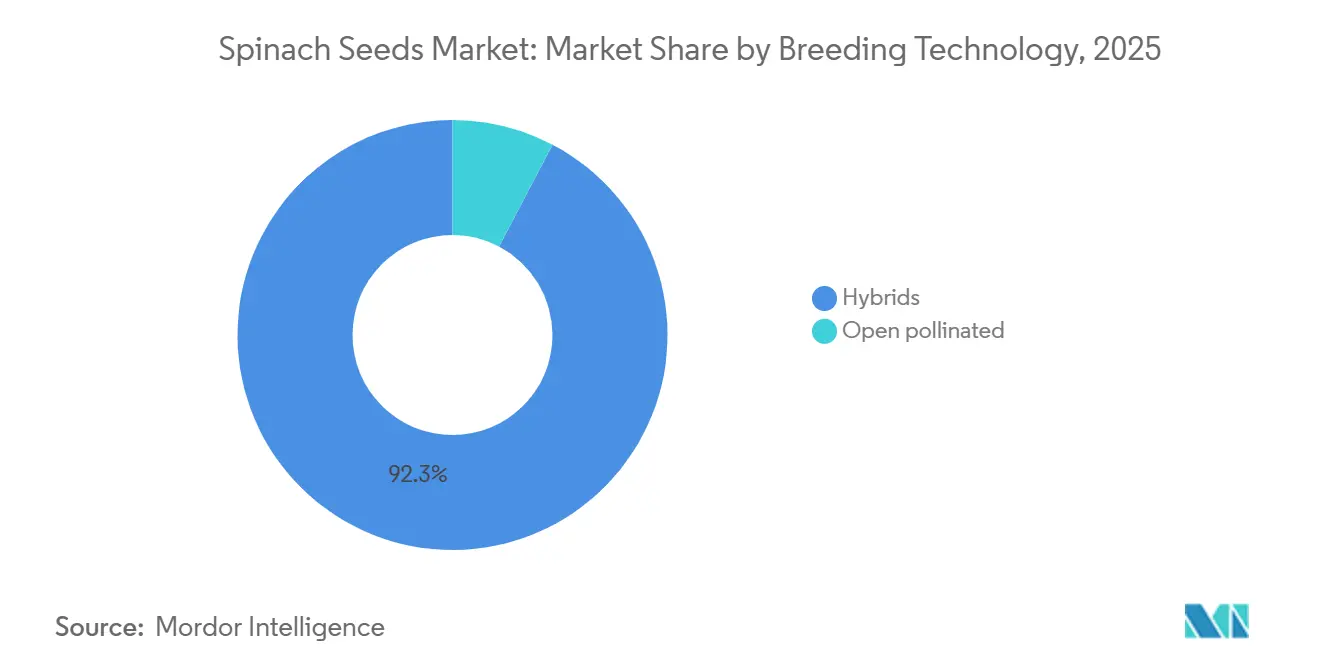

- By 2025, hybrids accounted for 92.3% of the spinach seed market and will be the fastest-growing segment, with a projected 6.0% CAGR from 2026 to 2031.

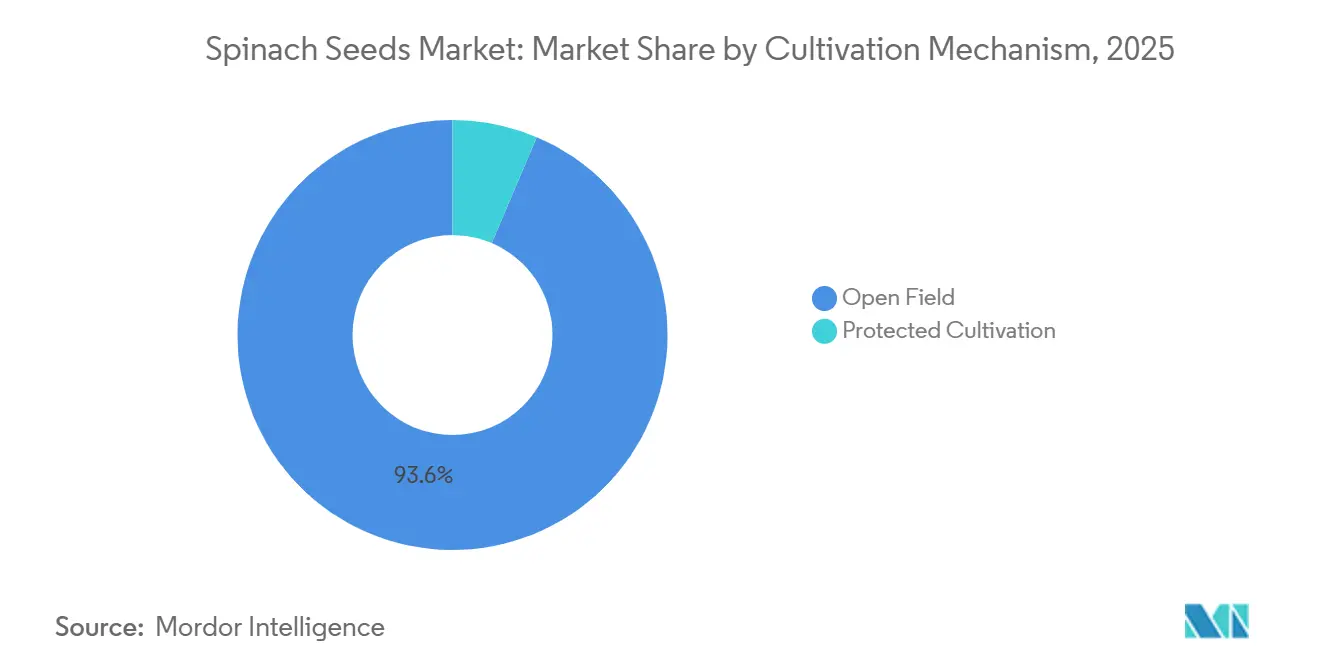

- By cultivation mechanism, open field was the largest segment, accounting for 93.6% of the spinach seed market in 2025, and protected cultivation is the fastest-growing segment, with a projected 6.8% CAGR between 2026 and 2031.

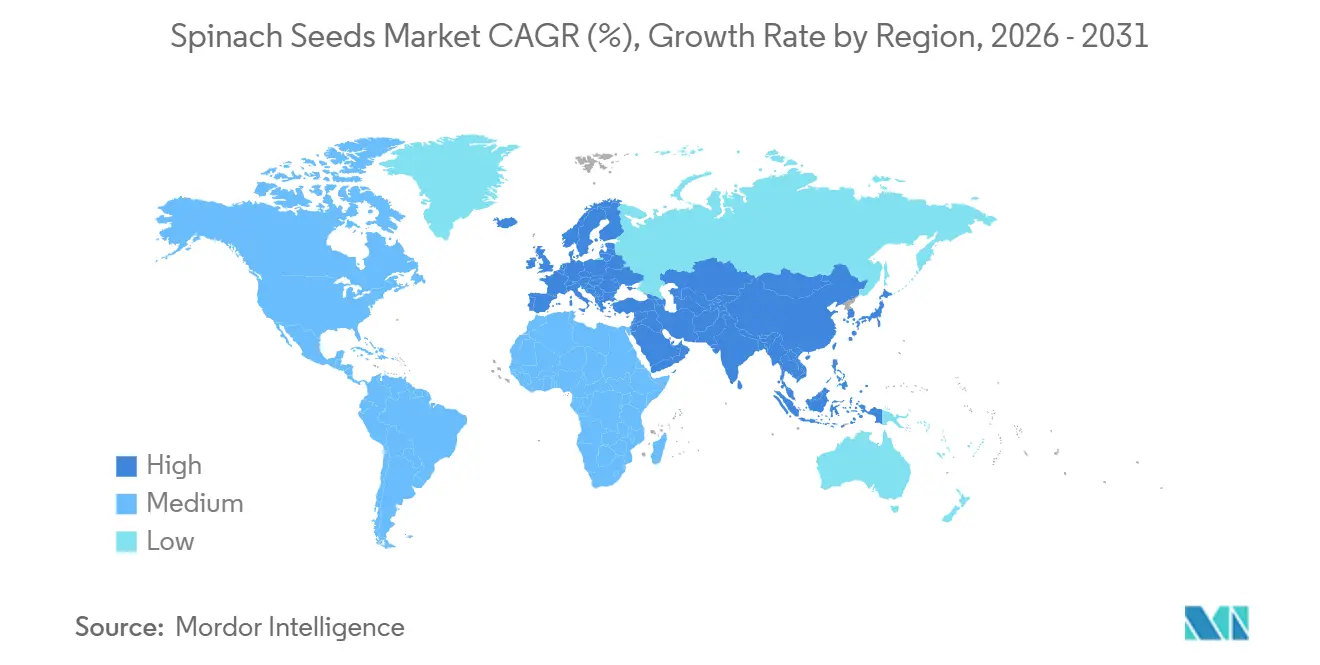

- By geography, Asia-Pacific was the largest regional segment with 42.0% revenue share in 2025, and Europe is the fastest-growing regional segment with a projected 6.9% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Spinach Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid replacement for disease resistance and uniformity | +1.8% | Global, with strongest pull in North America and Europe | Short term (≤ 2 years) |

| Year-round babyleaf retail programs | +1.0% | North America, Europe, Australia | Medium term (2-4 years) |

| Greenhouse and hydroponic spinach expansion | +0.9% | Europe, Middle East, North America | Medium term (2-4 years) |

| Organic seed demand growth | +0.6% | Europe, North America | Medium term (2-4 years) |

| Triggered resistance upgrades | +0.6% | Global, primarily Asia-Pacific core and Europe | Short term (≤ 2 years) |

| Climate-resilient breeding for weather volatility | +0.5% | Global, with early gains in Southern Europe and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid Replacement for Disease Resistance and Uniformity

The move from open-pollinated lines to hybrid spinach seed has become a commercial necessity in many production systems because disease management with chemistry alone is now harder to achieve. In open-pollinated varieties, resistance to 4 to 8 pathotypes of Peronospora effusa was generally carried, while leading commercial hybrids carried resistance to all 20 officially recognized races, creating a clear performance gap under retail and processor contracts. Nunhems Netherlands B.V. stated in 2025 that tighter restrictions on chemical seed treatments were making genetic resistance more critical for spinach growers in the United States, and that comment reflects a wider shift already visible in other major regions[1]Source: Nunhems Netherlands B.V., “Spinach Portfolio Uses Genetic Strength for Optimal Yield,” nunhems.com. In the spinach seeds market, this means hybrid replacement is not simply a yield decision, because growers without broad-spectrum resistance face a higher probability of contract failure and lower confidence in seasonal planning. It also means breeders with deeper resistance libraries can hold stronger pricing power because they are selling continuity of supply rather than only seed units. The result is that the spinach seeds market keeps generating repeat demand through replacement cycles even when headline acreage growth remains modest.

Year-Round Babyleaf Retail Programs

Retail spinach programs now expect much steadier weekly supply, and that has changed how growers choose seed portfolios across the spinach seeds market. Babyleaf buyers increasingly favor varieties that can preserve leaf quality, uniformity, and harvest timing under different sowing windows, which lifts the value of broad seed catalogues rather than single standout varieties. That shift matters because growers serving organized retail need dependable succession planting, and they are more likely to concentrate purchases with breeders that can cover multiple climates and planting slots. The commercial advantage therefore moves toward companies that can support a full annual program, from cooler months to stress periods, with consistent product standards. In the spinach seeds market, this widens the gap between breeders with deep portfolios and smaller players whose offerings do not cover the entire production calendar. It also strengthens the link between seed choice and customer retention, since a failed seasonal transition can affect grower relationships much more than a narrow price difference.

Greenhouse and Hydroponic Spinach Expansion

Protected systems are creating a distinct demand layer inside the spinach seeds market because hydroponic and greenhouse operators do not buy seed in the same way as open-field growers. These operators value seed treatment quality, synchronized emergence, compact plant habit, and clean performance under tightly managed water and light conditions. CleanGreens Solutions and GreenLife Company announced a 24,000-square-meter aeroponic greenhouse project in Kuwait in 2025 with spinach among the core crops, which shows that food security investments are directly feeding demand for specialized seed products in controlled systems[2]Source: CleanGreens Solutions, “CleanGreens Brings Its Aeroponic Expertise to the Middle East's Largest Sustainable Farming Project,” ggba.swiss. The Dutch Leafy Hydroponic Consortium launched in 2026 also includes spinach in multi-year greenhouse work, which points to a more organized effort to solve crop-specific hydroponic challenges that have historically limited adoption. In the spinach seeds market, that creates room for premium treated seed formats because operational losses in controlled systems are costly and growers will pay more for uniformity if it reduces crop risk.

Organic Seed Demand Growth

Organic spinach production is building a separate demand stream within the spinach seeds market because certified systems cannot rely on the same treated seed options used in conventional programs. That pushes breeders to develop varieties that combine acceptable vigor with stronger disease tolerance under lower-input conditions, which is not a simple extension of the standard portfolio. The commercial issue is that organic growers need compliance and performance at the same time, and seed shortages in this niche can delay planting decisions more quickly than in conventional systems. In Europe and North America, this is making organic-ready spinach genetics more strategic for companies that want to defend premium positions across the full customer base. The spinach seeds market therefore gains not only from rising organic acreage, but also from the higher technical difficulty of supplying certified seed that can still meet quality expectations. This remains one of the clearer pockets where a smaller share of volume can still have a meaningful impact on value growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-evolving downy mildew and multi-disease pressure | -0.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Seed production concentration in a few weather-sensitive regions | -0.5% | Global supply chain, particularly Pacific Northwest and Northern Europe | Medium term (2-4 years) |

| Summer germination and bolting limits in warm climates | -0.4% | Middle East, South and Southeast Asia, Southern Europe | Medium term (2-4 years) |

| Long breeding cycles and complex spinach genetics | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fast-Evolving Downy Mildew and Multi-Disease Pressure

The most immediate restraint in the spinach seeds market is the speed at which disease pressure can outdate a commercial resistance package. In 2025, researchers from the United States Department of Agriculture Agricultural Research Service reported new pathogenicity patterns and identified three additional races during screening of 70 commercial cultivars, highlighting the mutational challenges breeders face. This creates launch risk because varieties in late-stage trials may need re-evaluation when a new race emerges, which can delay commercialization after years of sunk breeding costs. It also reduces the available genetic space when breeders must stack resistance against Peronospora effusa, Stemphylium vesicarium, Fusarium wilt, and white rust in the same line. For the spinach seeds market, this means value can still grow, but breeding cost and speed become more decisive than simple scale.

Seed Production Concentration in a Few Weather-Sensitive Regions

The spinach seeds market faces a structural supply risk because seed multiplication remains concentrated in a small number of geographies with very specific agronomic conditions. The Pacific Northwest of the United States, Denmark, and New Zealand form the core of global production, and Washington State University highlighted in 2025 that the Pacific Northwest alone accounts for nearly one-fifth of world spinach seeds supply[3]Source: Washington State University, “Wild Spinach Offers Path to Breed Disease Resistance into Cultivated Varieties,” WSU Insider, news.wsu.edu. The same research also noted that Fusarium wilt remains a persistent issue for Pacific Northwest seed growers, who rely on long crop rotations and soil management practices because robust commercial resistance is still limited. That means a single weather event or disease setback in one of these regions can tighten global availability and push procurement risk downstream to growers and processors. In the spinach seeds market, this fragility matters because substitutes are limited in the short run, and seed cannot be shifted quickly from unrelated production zones. Long breeding cycles compound the issue because even when a need is visible, the industry cannot replace lost genetics or rebuild supply in one or two seasons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Anchor Commercial Spinach Production

Hybrids held 92.3% of the spinach seeds market share in 2025, making them the clear leader as commercial growers prioritized resistance, uniformity, and more dependable yields. They are also the fastest-growing segment, with a projected 6.0% CAGR from 2026 to 2031. This dominance reflects a long period of standardization around F1 seed in large fresh and processing programs, where even a modest decline in stand quality can affect harvest timing and packer acceptance. The spinach seeds market also continues to favor hybrids because new disease races force growers to replace varieties sooner than in more stable vegetable categories. Nunhems Netherlands B.V. expanded its United States commercial portfolio to more than 10 varieties with Peronospora effusa race 20 (Pe:20)-compatible resistance in 2025, demonstrating how quickly suppliers are responding to resistance pressure in a major production region. Enza Zaden Beheer B.V. has also been positioning full-race resistance genetics as a core value proposition, which supports the view that hybrid competition now revolves around durability and field confidence rather than only nominal yield.

Open pollination's smaller base still matters in parts of Asia and Africa where price sensitivity, local adaptation, and uneven access to premium seed shape buying behavior. These lines also retain relevance in organic production, where certified supply gaps can open the door to non-hybrid formats, particularly when growers need an immediate planting option. Even so, the long-term direction of the spinach seeds market still favors improved genetics in this part of the portfolio, as better resistance can narrow the performance gap without requiring a full hybrid platform. A 2025 scientific reports study by University of Arkansas, mapped a major quantitative trait locus for Fusarium wilt resistance on chromosome 6 in Spinacia turkestanica, providing breeders with a practical marker-assisted pathway to improve material beyond the top hybrid tier. That matters because the spinach seeds market can still expand access to quality in underserved regions if resistance traits move into lower-cost offerings over time.

By Cultivation Mechanism: Protected Cultivation Gains Ground on Open Fields

Open Field accounted for 93.6% of the spinach seeds market share in 2025, which kept it the largest cultivation mechanism because the economics of large-acreage spinach still favor outdoor systems in most producing regions. This base is supported by established fresh and processing supply chains in California, Europe, and Asia, where direct seeding and broad-area field management keep unit economics attractive. The California baby leaf production described the scale at which major farms sow spinach, reinforcing that large open-field programs continue to anchor baseline seed demand. In the spinach seeds market, that means open-field demand remains resilient even as newer systems expand, because field acreage still absorbs the majority of commercial seed volume. It also means breeders must continue to deliver traceable resistance packages and dependable field performance, since large buyers increasingly want documented variety characteristics before approving seed for supply programs.

Protected Cultivation accounted for a smaller share of the spinach seed market in 2025, but it is the fastest-growing cultivation mechanism, with a 6.8% CAGR through 2031. This segment is expanding because greenhouse and hydroponic operators need climate-independent production, tighter harvest planning, and more stable output for urban and premium retail channels. CleanGreens Solutions and GreenLife Company also show how protected systems are becoming a default pathway in hot-climate markets where outdoor summer production is limited. For the spinach seeds market, the importance of this segment goes beyond volume because protected growers buy for precision, and that supports premium pricing for treated seed with uniform emergence, compact growth, and cleaner crop scheduling.

Geography Analysis

Asia-Pacific accounted for 42.0% of the spinach seeds market size in 2025, which made it the largest regional block in the spinach seeds market. China remains the main anchor for this position because its overwhelming share of world spinach output creates large downstream seed demand tied to both fresh use and processing flows. Japan adds a higher-value profile within the region because growers there place greater emphasis on protected systems, uniform leaf quality, and premium retail standards. India, Indonesia, and Vietnam add a different layer of demand where hybrid adoption is still advancing, and that gives the spinach seeds market room to grow through conversion rather than only through acreage expansion.

Europe is the fastest regional segment in the spinach seeds market, with a projected 6.9% CAGR from 2026 to 2031. This regional momentum comes from a combination of controlled-environment investment, stricter seed expectations in organic channels, and the ongoing replacement cycle triggered by new downy mildew races. The Peronospora effusa race 20 (Pe:20) development had direct relevance for European growers because the new race was identified from isolates collected in both Europe and the United States, which reinforced the need for upgraded resistance packages in commercial programs. The Netherlands and Belgium are especially important in the regional story because they are pushing hydroponic spinach work further than most markets, while France and Italy remain meaningful production and consumption centers. North America remains a major commercial seed market within the global spinach seeds market because the United States continues to rely heavily on hybrid varieties across processing and babyleaf systems, and disease management needs keep replacement demand active.

The Middle East stands out in the spinach seeds market because protected cultivation is often the only dependable route for summer and year-round production in Gulf conditions. The GreenLife Company project in Kuwait and the broader rise of food security investment across the region show why greenhouse-suited seed is becoming more important in regional purchasing decisions. Africa remains led by a small set of stronger horticultural countries, but several emerging markets still have room for open pollinated to hybrid conversion where commercial spinach supply chains are becoming more organized. South America presents a mixed picture for the spinach seeds market because warm-weather bolting and germination stress narrow open-field production windows, which raises the commercial value of hybrids with better shoulder-season stability and heat tolerance.

Competitive Landscape

The spinach seeds market is moderately consolidated, with a group of European breeders holding a strong technical position in resistance breeding and babyleaf genetics. KWS Vegetables B.V., Rijk Zwaan Zaadteelt en Zaadhandel B.V., BASF SE., Syngenta AG, and Bayer AG remain important names because the spinach seeds market rewards companies that can move from pathogen monitoring to commercial release with less delay. In practical terms, the moat is built on genetics, field validation, treatment quality, and the ability to keep a grower supplied across multiple planting windows. The spinach seeds market is not determined solely by catalog size, as buyers increasingly prioritize disease resistance, regional adaptability, and a reliable plan for addressing new disease races as they emerge.

Syngenta AG made another notable move when it partnered with Tropic in 2025 to use Gene Editing-induced Gene Silencing (GEiGS) across vegetable crops to develop disease resistance, pointing to a future shift in how durable resistance could be assembled in the spinach seeds market. Rijk Zwaan Zaadteelt en Zaadhandel B.V. also reinforced its competitive position through sustained research spending, reporting EUR 204 million (USD 222 million) in research and development expenditure in fiscal year 2024/2025, which supports its ability to defend a broad and technically demanding vegetable portfolio. These moves matter because the spinach seeds market is becoming less forgiving for breeders that cannot absorb long development cycles and repeated resistance resets. They also show that speed, not only scale, is becoming a central competitive variable.

Another important signal came from Vilmorin and Cie SA, which announced in 2025 that it had entered exclusive discussions to build a strategic and financial partnership with Abu Dhabi Developmental Holding Company on vegetable seeds, including a joint research and development angle through Silal. This matters because the spinach seeds market has clear white space in desert-adapted breeding, protected-cultivation formats, and tropical-climate performance. The organic certified niche is another opportunity because supply remains tighter than demand in several commercial programs, which leaves room for specialists with cleaner resistance packages and reliable seed availability. Overall, the spinach seeds market still allows room for smaller challengers, but only where they can solve a specific production problem better than the large established breeders.

Spinach Seeds Industry Leaders

Bayer AG

Syngenta AG

KWS Vegetables B.V.

Rijk Zwaan Zaadteelt en Zaadhandel B.V.

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Rijk Zwaan Zaadteelt en Zaadhandel B.V. reported fiscal year 2024/2025 results showing net revenue growth of 9% to EUR 684 million (USD 746 million) and total research and development expenditure of EUR 204 million (USD 222 million), reinforcing its position as one of the highest research intensity competitors in the global vegetable seed sector breeding pathway for commercial seed companies to integrate Fusarium wilt resistance into hybrid lines including spinach varieties.

- July 2025: Nunhems Netherlands B.V. (BASF's vegetable seeds business under the Nunhems brand) expanded its United States commercial spinach portfolio to more than 10 varieties resistant to multiple races of Peronospora effusa, citing heightened disease pressure and reduced access to chemical seed treatments as the key market catalysts.

- May 2025: Syngenta AG and Tropic signed a strategic collaboration to deploy Tropic's Gene Editing induced Gene Silencing (GEiGS) technology across Syngenta's vegetable portfolio for disease resistance development, with spinach among the targeted crops. The agreement creates a new tool pathway for achieving durable resistance without conventional introgression, potentially compressing the time from pathogen identification to commercial variety release.

Global Spinach Seeds Market Report Scope

A spinach seed is a small, hard, tannish-brown reproductive unit produced by the mature Spinacia oleracea plant. Botanically, it is a tiny, starch-rich fruit (utricle) used exclusively to cultivate nutritious, cool-season leafy green vegetables.

The Spinach Seed Market Report is Segmented by Breeding Technology (Hybrids and Open Pollinated Varieties and Hybrid Derivatives), Cultivation Mechanism (Open Field and Protected Cultivation), and Geography (Africa, Asia-Pacific, Europe, Middle East, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

| Open Field |

| Protected Cultivation |

| Africa | By Breeding Technology | |

| By Cultivation Mechanism | ||

| By Country | Egypt | |

| Ethiopia | ||

| Ghana | ||

| Kenya | ||

| Nigeria | ||

| South Africa | ||

| Tanzania | ||

| Rest of Africa | ||

| Asia-Pacific | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Australia | ||

| Bangladesh | ||

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Myanmar | ||

| Pakistan | ||

| Philippines | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | By Breeding Technology | |

| By Cultivation Mechanism | ||

| France | ||

| Germany | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Romania | ||

| Russia | ||

| Spain | ||

| Ukraine | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Iran | ||

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| North America | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Canada | ||

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Argentina | ||

| Brazil | ||

| Rest of South America | ||

| Breeding Technology | Hybrids | ||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Cultivation Mechanism | Open Field | ||

| Protected Cultivation | |||

| Geography | Africa | By Breeding Technology | |

| By Cultivation Mechanism | |||

| By Country | Egypt | ||

| Ethiopia | |||

| Ghana | |||

| Kenya | |||

| Nigeria | |||

| South Africa | |||

| Tanzania | |||

| Rest of Africa | |||

| Asia-Pacific | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Australia | |||

| Bangladesh | |||

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Myanmar | |||

| Pakistan | |||

| Philippines | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Europe | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| France | |||

| Germany | |||

| Italy | |||

| Netherlands | |||

| Poland | |||

| Romania | |||

| Russia | |||

| Spain | |||

| Ukraine | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Iran | |||

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| North America | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Canada | |||

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Argentina | |||

| Brazil | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the spinach seeds market?

The spinach seeds market is valued at USD 242.45 million in 2026 and is projected to reach USD 323.19 million by 2031, growing at a 5.92% CAGR.

Which breeding technology leads spinach seed demand?

Hybrids lead demand, holding 92.3% share in 2025, because commercial growers increasingly need stronger disease resistance and more uniform crop performance.

Why are growers replacing spinach varieties more often now?

New downy mildew races, including Pe:20, are shortening the commercial life of varieties and pushing growers toward faster resistance upgrades.

Which cultivation system is growing the fastest for spinach seed use?

Protected cultivation is the fastest-growing system, with a projected 6.8% CAGR through 2031, because greenhouse and hydroponic operations need specialized seed performance.

Which region leads global demand for spinach seed?

Asia-Pacific led with 42.0% share in 2025, supported by China's dominant spinach production base and rising regional use of improved seed.

What is the main supply risk in spinach seed production?

Global production is concentrated in a few weather-sensitive regions, especially the Pacific Northwest of the United States, which raises supply chain risk when weather or disease affects seed crops.

Page last updated on: