Lettuce Seeds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

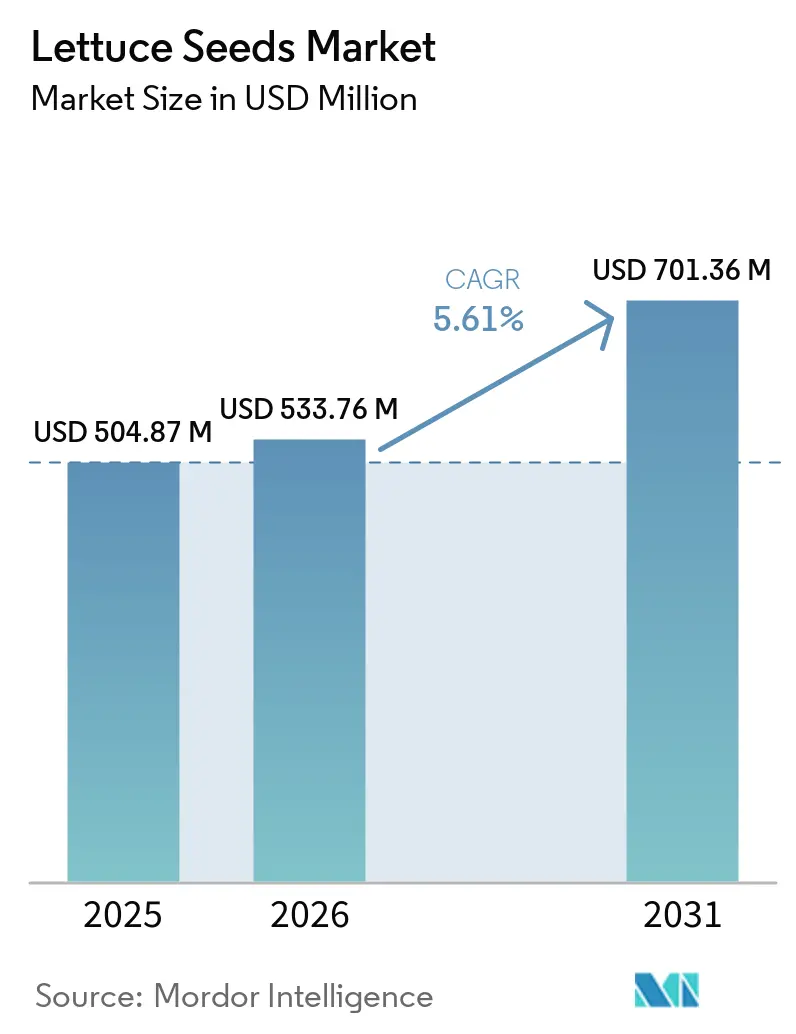

| Market Size (2026) | USD 533.76 Million |

| Market Size (2031) | USD 701.36 Million |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lettuce Seeds Market Analysis by Mordor Intelligence

The lettuce seeds market size is projected to increase from USD 504.87 million in 2025 to USD 533.76 million in 2026 and reach USD 701.36 million by 2031, growing at a CAGR of 5.61% over 2026-2031. The lettuce seeds market is being shaped by a clear shift in fresh produce supply chains, where processed salad packs and ready-to-eat formats are creating steady demand for varieties with uniform texture, stable shelf life, and lower post-harvest browning. The lettuce seeds market is also benefiting from the spread of greenhouse and hydroponic production, especially in North America, Europe, and urban parts of Asia, because these systems depend on genetics that perform well under controlled conditions. Procurement standards from processors and retailers are becoming stricter, which is pushing seed developers to focus on fewer but stronger commercial platforms with dependable field and packing results. Climate stress, disease pressure, and tighter compliance requirements are raising the commercial value of advanced breeding pipelines in the lettuce seeds market. These conditions continue to favor companies that can combine resistance, uniformity, and system-specific performance in a single variety portfolio.

Key Report Takeaways

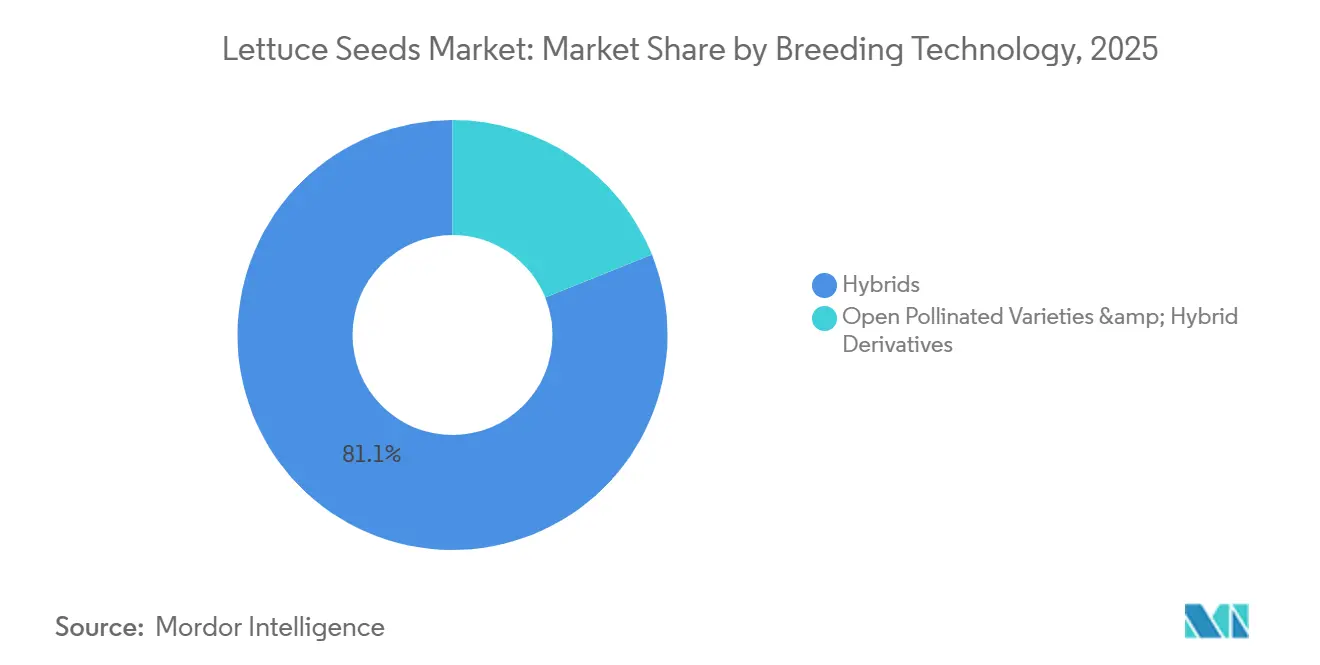

- By breeding technology, hybrids were the largest segment, with 81.1% of the lettuce seed market share in 2025, and are also the fastest-growing segment, with a projected 5.6% CAGR through 2031.

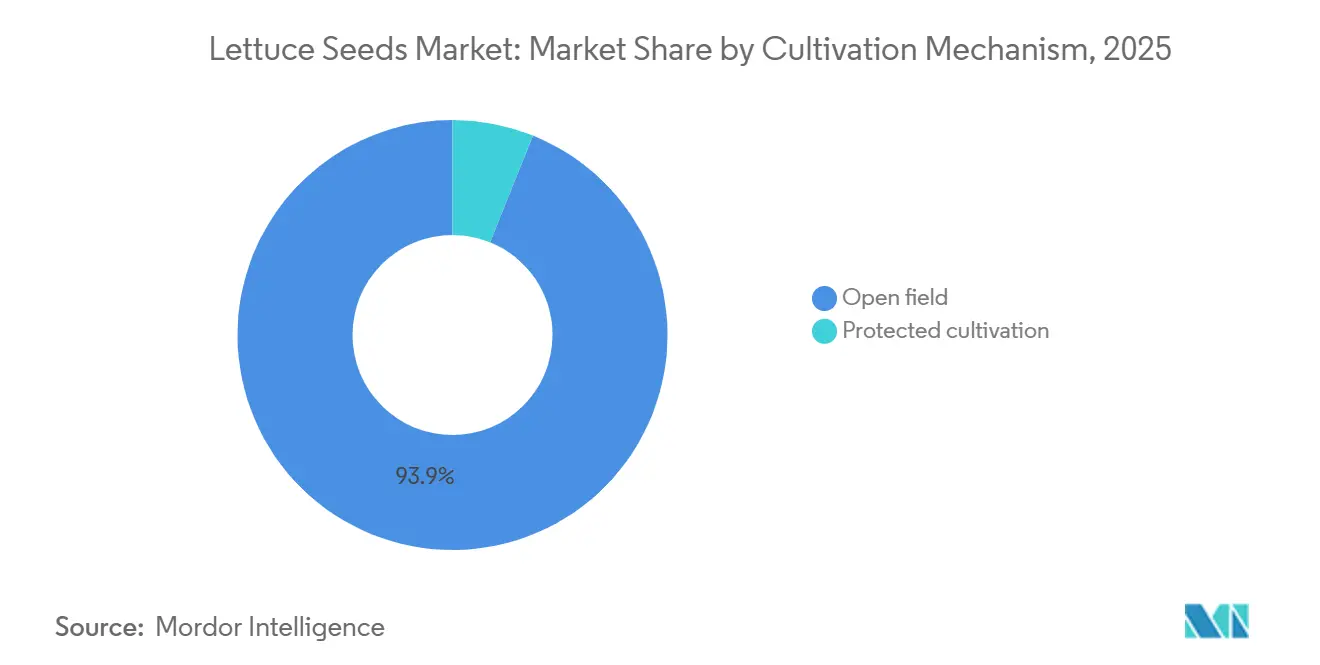

- By cultivation mechanism, open field was the largest segment and accounted 93.9% of the lettuce seed market in 2025, while protected cultivation was the fastest-growing segment and is anticipated to grow at an 8.6% CAGR through 2031.

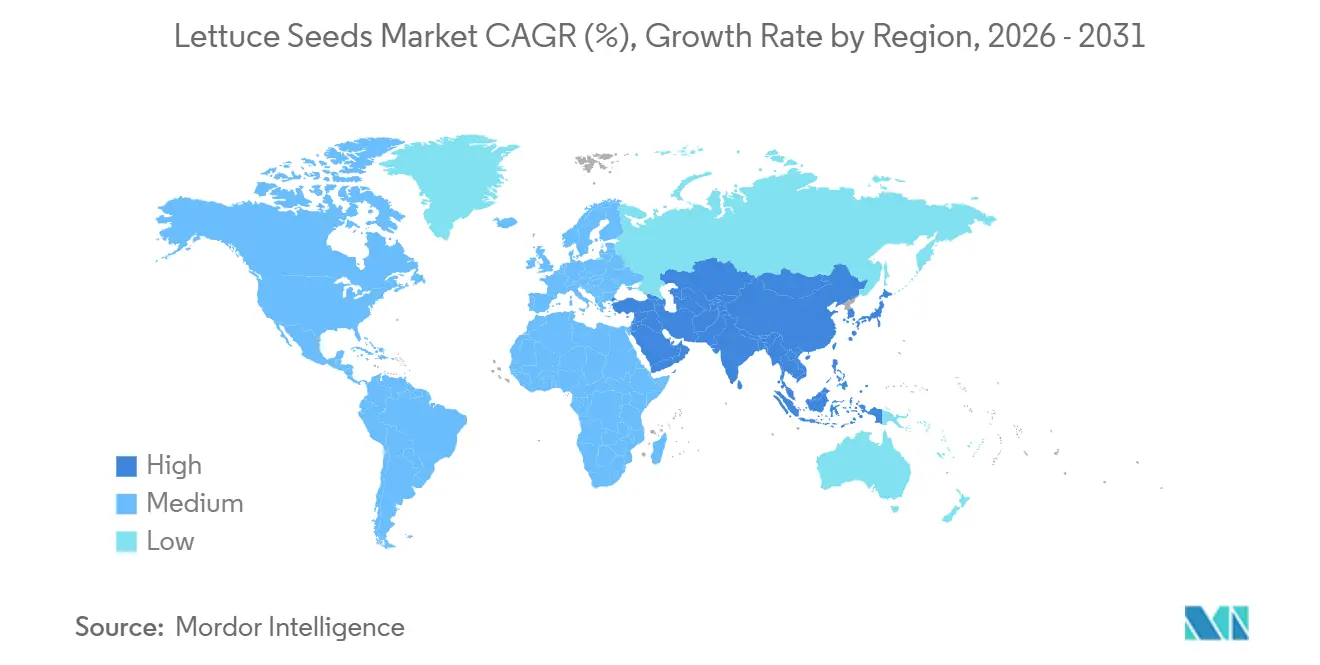

- By geography, Asia-Pacific was the largest segment with 43.7% of the market in 2025 and was also the fastest-growing region, anticipated to post a 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lettuce Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising salad and fresh-cut lettuce consumption | +1.5% | Global, with commercial concentration in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of greenhouse and hydroponic lettuce acreage | +1.2% | North America and Europe core, with spillover to Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Demand for disease-resistant and climate-resilient genetics | +1.0% | Global | Medium term (2-4 years) |

| Organic lettuce acreage expanding seed demand | +0.8% | North America and Europe, with early gains in South America | Medium term (2-4 years) |

| Processor demand for low-pinking and longer-shelf-life traits | +0.7% | North America and Europe, with emerging gains in Asia-Pacific | Short term (≤ 2 years) |

| Automation-ready and digitally phenotyped lettuce varieties | +0.6% | North America, Europe, and Japan, with early adoption in South Korea and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Salad and Fresh-Cut Lettuce Consumption

Fresh-cut salads and packaged lettuce formats remain the most immediate volume driver for the lettuce seeds market because foodservice chains, institutional buyers, and meal-kit operators need stable supply through the year. These buyers prefer growers that can meet strict standards on uniform head size, maturity timing, and post-harvest performance, which gives hybrids a clear advantage over conventional seed formats. In practical terms, processor approval now acts as an early filter for commercial seed success, because a variety that works well in the packing line can win volume before wider farm-level testing is complete. The Food and Agriculture Organization of the United Nations (FAO) reported that global lettuce and chicory production reached 28.2 million metric tons in 2024, which shows that the production base supporting this channel remains large and active[1]Source: Food and Agriculture Organization of the United Nations, “FAOSTAT Crops and Livestock Products,” fao.org. As more of that production is tied to value-added fresh produce formats, the lettuce seeds market is moving toward tighter alignment between breeding priorities and processor requirements. This is strengthening the commercial position of companies that already hold processor-validated hybrid portfolios.

Expansion of Greenhouse and Hydroponic Lettuce Acreage

Controlled environment agriculture (CEA) is expanding the range of places where lettuce can be produced at commercial scale, and that is creating a distinct growth layer inside the lettuce seeds market. Seed performance in greenhouse and hydroponic systems is judged on different criteria from open-field systems, including response to artificial light, dense planting, and recirculating nutrient delivery. This is raising demand for genetics tested under specific indoor conditions instead of broad outdoor trial performance alone. In April 2025, Vegpro International inaugurated a 5.2-hectare greenhouse in Sherrington, Quebec, through a CAD 135 million (USD 97 million) investment, showing the level of capital being directed into controlled lettuce production[2]Source: Harnois Greenhouses and Vegpro International, “Vermax Glass Greenhouse, 5.2-Hectare Breakthrough Project,” harnoisgreenhouse.com. Facilities like these also replant more often than field farms, which creates more regular purchase cycles for seed suppliers. That recurring demand pattern makes the lettuce seeds market more attractive for breeders that can prove consistent CEA performance.

Demand for Disease-Resistant and Climate-Resilient Genetics

Disease resistance and climate tolerance have moved from premium features to baseline requirements across a wide part of the lettuce seeds market. New races of Bremia lactucae and evolving pest pressure are shortening the useful life of existing resistance packages, while warmer conditions are increasing concern around Fusarium crown rot, bacterial leaf spot, bolting, and tipburn. This is pushing growers and seed companies to place more value on varieties that can maintain performance under variable field stress and under tighter chemical use limits. A 2025 study in Theoretical and Applied Genetics identified a major and stable quantitative trait locus linked to resistance against Impatiens Necrotic Spot Virus in lettuce, which shows how technically intensive durable resistance work has become. The research burden behind these programs is widening the gap between large R&D-led breeders and smaller competitors. As a result, the lettuce seeds market is rewarding companies that can update resistance platforms quickly without sacrificing agronomic uniformity.

Organic Lettuce Acreage Expanding Seed Demand

Organic production is opening a premium but compliance-driven layer of demand in the lettuce seeds market. Certified growers in North America and Europe are projected to source organically produced seed when commercial supply is available, which makes seed choice part of certification discipline rather than a simple price decision. That creates a more stable premium channel for breeders that have invested in certified seed multiplication and traceable supply. It also matters that organic producers still face the same pressure on disease control, shelf life, and field uniformity as conventional growers, especially when they sell into large retail programs. Because of this, the most valuable opportunity is not organic seed alone, but organic seed that also carries strong resistance and dependable field performance. The lettuce seeds market therefore gains incremental value when breeders align certification, resistance, and commercial handling traits in the same offering.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid pathogen evolution versus long breeding cycles | -0.8% | Global | Long term (≥ 4 years) |

| Tightening treated-seed and phytosanitary compliance | -0.6% | North America and Europe, with spillover to Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Heat stress, bolting, and tipburn risk across seasons | -0.5% | Asia-Pacific, Middle East and North Africa, and southern North America | Medium term (2-4 years) |

| Fragmented trait needs by channel and growing system | -0.4% | Global, particularly in emerging markets and smallholder systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Pathogen Evolution Versus Long Breeding Cycles

One of the clearest restraints on the lettuce seeds market is the mismatch between how fast pathogens evolve and how slowly new commercial varieties are developed. A new disease race can weaken an established resistance package within a few planting cycles, while a marketable lettuce cultivar usually needs 7 to 8 years from early crossing to commercial seed production. That gap forces breeders to invest in complex stacking programs and forward-looking resistance strategies that may still lose relevance before full commercialization. Research published through the United States Department of Energy Office of Scientific and Technical Information in 2025 identified key resistance loci linked to Sclerotinia minor resistance and bolting control, which shows the scientific depth now required even for targeted trait improvement[3]Source: United States Department of Energy Office of Scientific and Technical Information, “Integrative Path Modeling and QTL Mapping Identify Maturity, Stem Strength, and Cell Wall Composition Driving Lettuce Resistance to Sclerotinia minor,” osti.gov. The pace of climate variation adds another layer of difficulty because shifting seasons can alter disease pressure in ways that are harder to predict with conventional trial calendars. This leaves the lettuce seeds market exposed to periodic resets in commercial variety value.

Tightening Treated-Seed and Phytosanitary Compliance

Compliance costs are becoming a stronger gatekeeper in the lettuce seeds market, especially for companies moving seed lots across borders. In April 2025, the United States Department of Agriculture Animal and Plant Health Inspection Service (USDA APHIS) Plant Protection and Quarantine expanded its risk-based sampling program at ports of entry to cover all major lettuce variety types arriving from Mexico, including iceberg, romaine, butterhead, and leaf. At the same time, the International Seed Federation (ISF) published technical guidelines in June 2025 for the validation of seed health methods, which supports trade harmonization but also raises the need for testing capability and documentation systems. These requirements are easier for large exporters to absorb than for regional or niche seed companies. The result is that compliance now acts as both a quality filter and a structural entry barrier. This is one reason the lettuce seeds market continues to favor larger suppliers with established certification and traceability systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrid Varieties Define Commercial Positioning

Hybrids held 81.1% of lettuce seeds market share in 2025, making them the largest breeding technology segment and the commercial standard across iceberg, romaine, butterhead, and baby-leaf production, and hybrids are also the fastest segment with a projected 5.6% CAGR through 2031. Their leadership comes from strong uniformity, dependable resistance packages, and stable head formation under mechanized harvest systems, all of which matter to processors and large retail programs. The lettuce seeds market has reached a point where these traits are treated as minimum requirements in mainstream channels rather than premium extras. Hybrid adoption continues to deepen wherever professionalized production and formal input distribution are already established. Open-Pollinated Varieties and Hybrid Derivatives still play a role in smallholder systems where farm-saved seed practices remain economically sensible and certified distribution networks are less developed.

The breeding technology segment market size remains centered on hybrids because multi-trait platforms can now support both open-field production and controlled environment agriculture with the same genetic base. In the lettuce seeds industry, this type of research supports stacking programs that combine disease resistance, harvest consistency, and stress tolerance in one commercial platform. That direction raises the competitive threshold because advanced hybrid programs require long cycles, reliable parent-line control, and sustained selection budgets. The lettuce seeds market therefore continues to reward breeders with deep proprietary germplasm and disciplined commercialization pipelines.

By Cultivation Mechanism: Protected Systems Gain Value While Open Field Leads Volume

Open field cultivation had 93.9% market share in 2025, making it the largest cultivation mechanism in the lettuce seeds market, while protected cultivation is the fastest segment with an 8.5% CAGR through 2031. The large open-field base still reflects the scale of established production belts across China, Spain, and the United States, where field-grown lettuce supports both fresh and processing channels. Even so, volume share alone does not tell the full commercial story because protected systems often carry higher value per seed unit. Growers operating greenhouses and hydroponic sites pay more for varieties that are validated under artificial light, dense spacing, and system-specific disease pressure. The lettuce seeds market is seeing a gradual shift in value concentration even while field acreage remains dominant.

The cultivation mechanism segment market size is gaining added support from research and investment tied to both greenhouse and field performance. In March 2026, the University of Florida Institute of Food and Agricultural Sciences received a USD 500,000 federal grant from the United States Department of Agriculture National Institute of Food and Agriculture to develop multi-disease-resistant lettuce varieties for open-field and greenhouse systems in Florida, California, and Arizona. In April 2025, Vegpro International also opened a major greenhouse project in Quebec, which reflects the commercial pull of year-round lettuce production. In the lettuce seeds industry, these developments show that cultivation systems are no longer being treated as separate breeding worlds. The lettuce seeds market is instead moving toward dual-system variety validation, where a broader set of growers expects reliable performance across more than one production setting.

Geography Analysis

Asia-Pacific held 43.7% of lettuce seeds market share in 2025, making it the largest regional segment in the lettuce seeds market, and it is also the fastest region with a 6.8% CAGR through 2031. China remains the central anchor because its scale in lettuce and chicory production means that even modest changes in hybrid penetration create meaningful seed demand at the aggregate level. According to the Food and Agriculture Organization of the United Nations, China accounts for more than half of global lettuce and chicory production, giving the region an unusually strong base for commercial seed production. India, Vietnam, Japan, and the Philippines add a second layer of demand as urban retail channels and fresh produce handling systems improve. The lettuce seeds market in Asia-Pacific also includes technologically advanced niches where greenhouse and indoor operators require varieties suited to defined light and temperature regimes.

Europe and North America represent a mature yet innovation-focused segment of the lettuce seeds market. In Europe, stricter pesticide regulations and higher residue standards are driving growers to adopt seeds with enhanced genetic resistance. Additionally, the region's emphasis on sustainable agricultural practices and the increasing adoption of organic farming methods are further influencing seed selection. Meanwhile, consistent demand from both field and greenhouse production channels sustains ongoing variety development, ensuring adaptability to evolving consumer preferences and environmental conditions. In North America, California continues to be the primary hub for commercial demand, as the production of processor-grade romaine and iceberg lettuce remains concentrated in the region. The state's favorable climate, established infrastructure, and proximity to processing facilities contribute to its dominance in the lettuce seeds market.

Regulatory discipline is influencing regional competition in North America, as fully documented seed lots now offer a significant commercial advantage. Growth in this region is driven by urban food demand, increasing retail penetration, and the gradual formalization of seed systems. The demand for high-quality seeds is further supported by the growing awareness among farmers regarding the benefits of improved seed varieties, including higher yields and better resistance to pests and diseases. While open-pollinated varieties and hybrid derivatives remain more prevalent than advanced commercial channels, the long-term potential for hybrids is evident as cold chain infrastructure, retail standards, and formal distribution networks continue to improve. Additionally, government initiatives aimed at enhancing agricultural productivity and ensuring food security are expected to further boost the adoption of hybrid seeds in the region.

Competitive Landscape

The lettuce seeds market is moderately consolidated, with Syngenta AG (Syngenta Group Co., Ltd.), BASF SE, Rijk Zwaan Zaadteelt en Zaadhandel B.V. (Rijk Zwaan Holding B.V.), Enza Zaden Beheer B.V., and East-West Seed International Limited (East-West Seed Group) holding broad commercial portfolios across major lettuce types in 2025. Competition centers on companies that can combine resistance, uniformity, harvest fit, and post-harvest performance in fewer, stronger variety platforms. The processor channel has increased that pressure because buyers prefer validated varieties that reduce risk in washing, cutting, and packing operations. This favors companies with deep germplasm libraries and long trial networks. It also leaves smaller breeders with narrower room to compete unless they target a specific white space, such as heat adaptation, organic seed, or CEA suitability.

The lettuce seeds market is also being shaped by strategic moves that strengthen regional reach and technical capability. In June 2025, Vilmorin & Cie SA entered exclusive discussions with Abu Dhabi Developmental Holding Company to build a partnership focused on vegetable seeds and desert-adapted genetics, underscoring how major breeders are positioning for arid-climate demand. In September 2025, Sakata Vegetables Europe announced the acquisition of Allium Seeds’ onion and shallot business, expanding the operating scale of Sakata Seed Corporation in Europe beyond lettuce-specific lines. These moves matter because broader platform scale can support stronger breeding budgets, deeper distribution, and broader regulatory coverage.

A third competitive pattern is the rising importance of shared technical infrastructure around seed health and research. The International Seed Federation published updated validation guidance for seed health methods in 2025, which supports more consistent testing expectations across trading regions. Public research is also feeding the pipeline, as shown by the University of Florida breeding program that is testing disease-resistant materials in both greenhouse and open-field settings. The lettuce seeds market, therefore, remains open to innovation, but the path to scale is harder than it looks because technical, compliance, and customer validation demands are all rising together. Incumbent breeders still hold a durable moat in the global lettuce seeds market.

Lettuce Seeds Industry Leaders

BASF SE

East-West Seed International Limited

Rijk Zwaan Zaadteelt en Zaadhandel B.V. (Rijk Zwaan Holding B.V.)

Syngenta AG (Syngenta Group Co., Ltd.)

East-West Seed International Limited (East-West Seed Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Enza Zaden Beheer B.V. announced that commercial seed volumes of its new iceberg lettuce varieties, featuring intermediate resistance to Nasonovia ribisnigri Nr:1 along with HR Nr:0, IR Nr:1, and full Bremia resistance (Bl:29-41), will be available starting mid-2026. Sowing is anticipated to begin in June, targeting European fresh-market growers.

- May 2026: Syngenta AG introduced 'Renegade,' a romaine lettuce variety designed with high resistance to Impatiens Necrotic Spot Virus (INSV) and bolting tolerance. This variety was specifically developed for the growing conditions of Salinas Valley, California, and is intended for both fresh-market and processing applications.

- April 2025: Vegpro International inaugurated a 5.2-hectare greenhouse in Sherrington, Quebec, representing a CAD 135 million (USD 97 million) investment in controlled-environment lettuce production, illustrating the capital scale being deployed in this channel across North America.

Global Lettuce Seeds Market Report Scope

A lettuce seed is a tiny, elongated, greyish-brown or white achene produced by the mature Lactuca sativa plant. Botanically, it is a single-seeded dry fruit containing an oil-rich embryo used exclusively to cultivate diverse crisp, leafy salad greens. The Lettuce Seed Market Report is Segmented by Breeding Technology (Hybrids and Open Pollinated Varieties and Hybrid Derivatives), by Cultivation Mechanism (Open Field and Protected Cultivation), and by Geography (Africa, Asia-Pacific, Europe, Middle East, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

| Open Field |

| Protected Cultivation |

| Africa | By Breeding Technology | |

| By Cultivation Mechanism | ||

| By Country | Egypt | |

| Ethiopia | ||

| Ghana | ||

| Kenya | ||

| Nigeria | ||

| South Africa | ||

| Tanzania | ||

| Rest of Africa | ||

| Asia-Pacific | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Australia | ||

| Bangladesh | ||

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Myanmar | ||

| Pakistan | ||

| Philippines | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | By Breeding Technology | |

| By Cultivation Mechanism | ||

| France | ||

| Germany | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Romania | ||

| Russia | ||

| Spain | ||

| Ukraine | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Iran | ||

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| North America | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Canada | ||

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Breeding Technology | |

| By Cultivation Mechanism | ||

| Argentina | ||

| Brazil | ||

| Rest of South America | ||

| Breeding Technology | Hybrids | ||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| Cultivation Mechanism | Open Field | ||

| Protected Cultivation | |||

| Geography | Africa | By Breeding Technology | |

| By Cultivation Mechanism | |||

| By Country | Egypt | ||

| Ethiopia | |||

| Ghana | |||

| Kenya | |||

| Nigeria | |||

| South Africa | |||

| Tanzania | |||

| Rest of Africa | |||

| Asia-Pacific | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Australia | |||

| Bangladesh | |||

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Myanmar | |||

| Pakistan | |||

| Philippines | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Europe | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| France | |||

| Germany | |||

| Italy | |||

| Netherlands | |||

| Poland | |||

| Romania | |||

| Russia | |||

| Spain | |||

| Ukraine | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Iran | |||

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| North America | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Canada | |||

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | By Breeding Technology | ||

| By Cultivation Mechanism | |||

| Argentina | |||

| Brazil | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is driving growth in lettuce seeds demand through 2031?

Growth is being supported by packaged salad consumption, wider use of controlled environment agriculture, and stronger demand for disease-resistant and climate-resilient genetics. The sector is projected to grow from USD 533.76 million in 2026 to USD 701.36 million by 2031 at a 5.61% CAGR.

Why are hybrids leading commercial adoption in lettuce planting material?

Hybrids led with 81.1% share in 2025 because they offer better uniformity, resistance, and post-harvest consistency, which matter to processors, retailers, and mechanized growers.

Which cultivation system is expanding fastest for lettuce seed demand?

Protected cultivation is expanding fastest at an 8.6% CAGR through 2031, even though open field remained the largest system with 93.9% share in 2025.

Which region offers the strongest near-term growth opportunity?

Asia-Pacific is the largest regional base and the fastest-growing one, with 43.7% share in 2025 and a 6.8% CAGR through 2031, supported by China's scale and wider hybrid adoption in other Asian countries.

What are the biggest operational risks for seed companies in this space?

The main risks are rapid pathogen evolution, long breeding cycles, stricter phytosanitary rules, and rising heat stress that can weaken commercial performance and shorten the life of resistance packages.

How concentrated is competition among lettuce seed suppliers?

Competition is moderate rather than extreme. Large breeders such as Syngenta AG, Rijk Zwaan Zaadteelt en Zaadhandel B.V., Enza Zaden Beheer B.V., HM. CLAUSE, Inc., and Vilmorin & Cie SA have strong positions, but the field is not controlled by only a few players.

Page last updated on: