Fruits and Vegetables Seeds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

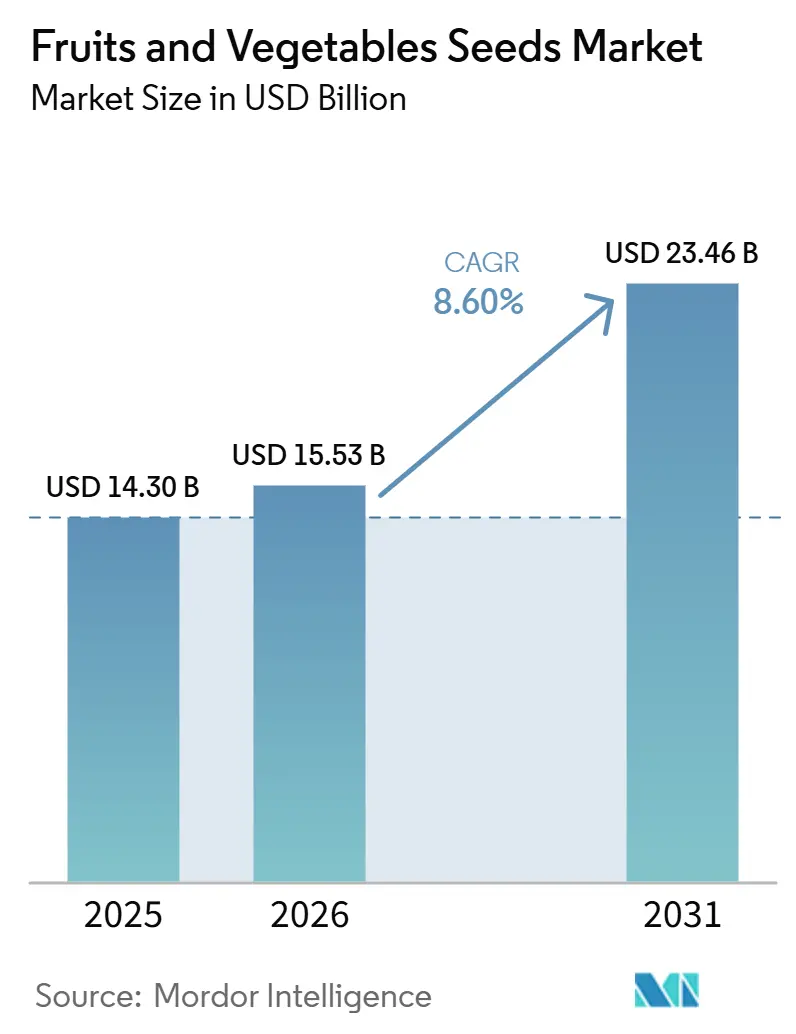

| Market Size (2026) | USD 15.53 Billion |

| Market Size (2031) | USD 23.46 Billion |

| Growth Rate (2026 - 2031) | 8.60% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fruits and Vegetables Seeds Market Analysis by Mordor Intelligence

The fruits and vegetables seeds market was valued at USD 11.09 billion in 2025 and is projected to grow from USD 11.68 billion in 2026 to USD 15.12 billion by 2031, registering a CAGR of 5.30% during the forecast period from 2026 to 2031. Growth in this market is driven by increasing global consumption of fresh produce, expanding commercial horticulture activities, and a shift from farm-saved seeds to purchased seeds that offer more consistent performance. This transition remains significant in countries such as India, Egypt, and parts of Sub-Saharan Africa, where seed replacement rates are still lower in several farming systems. Additionally, rising disease pressure is encouraging growers to replace older seed varieties more frequently, particularly in high-value crops such as tomatoes, where resistance traits are becoming a critical factor in purchasing decisions. The expansion of greenhouse cultivation across Europe, West Asia, and other controlled growing regions is further boosting demand for seeds specifically bred for protected environments rather than open-field conditions. The market is also experiencing ongoing consolidation among large multinational breeders, while regional players are expanding their presence by offering locally adapted genetics in rapidly growing emerging markets.

Key Report Takeaways

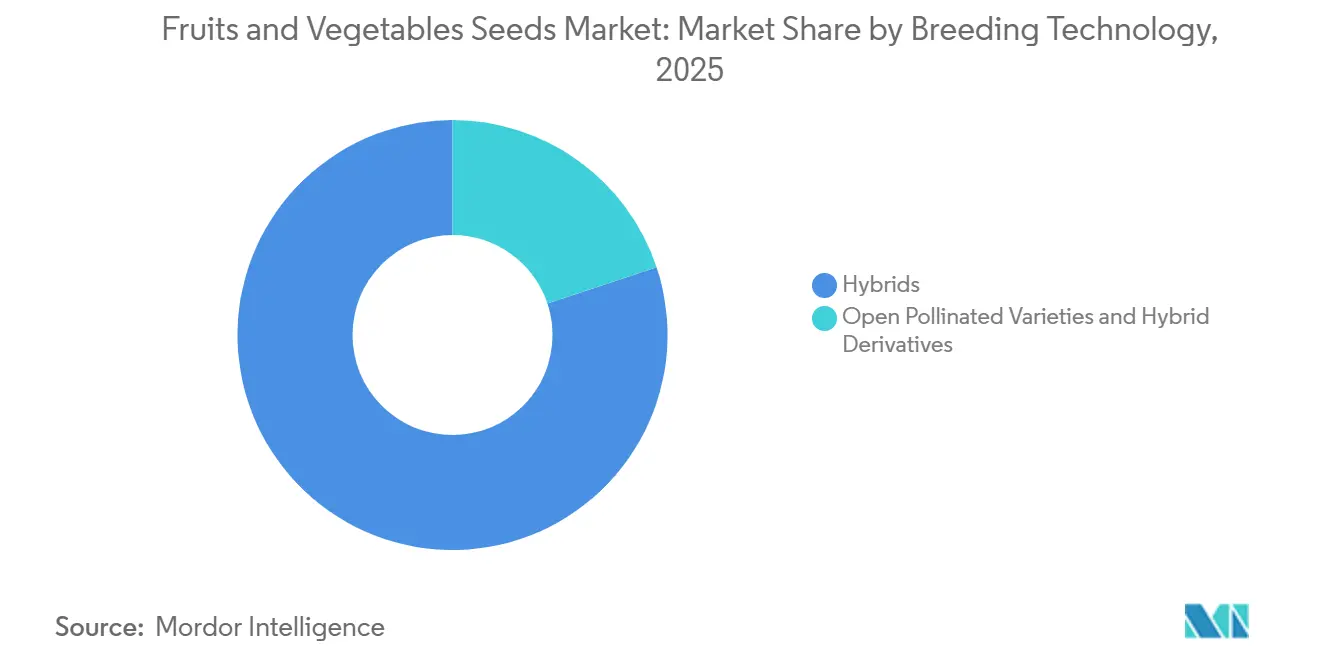

- By breeding technology, the fruits and vegetables seeds market share for hybrids held the largest 80.1% share in 2025, and it is also forecast to grow fastest at a CAGR of 5.7% from 2026 to 2031.

- By cultivation mechanism, open-field cultivation accounted for the largest 69.4% share in 2025, and the fruits and vegetables seeds market size for protected cultivation is projected to grow at the fastest CAGR of 7.4% from 2026 to 2031.

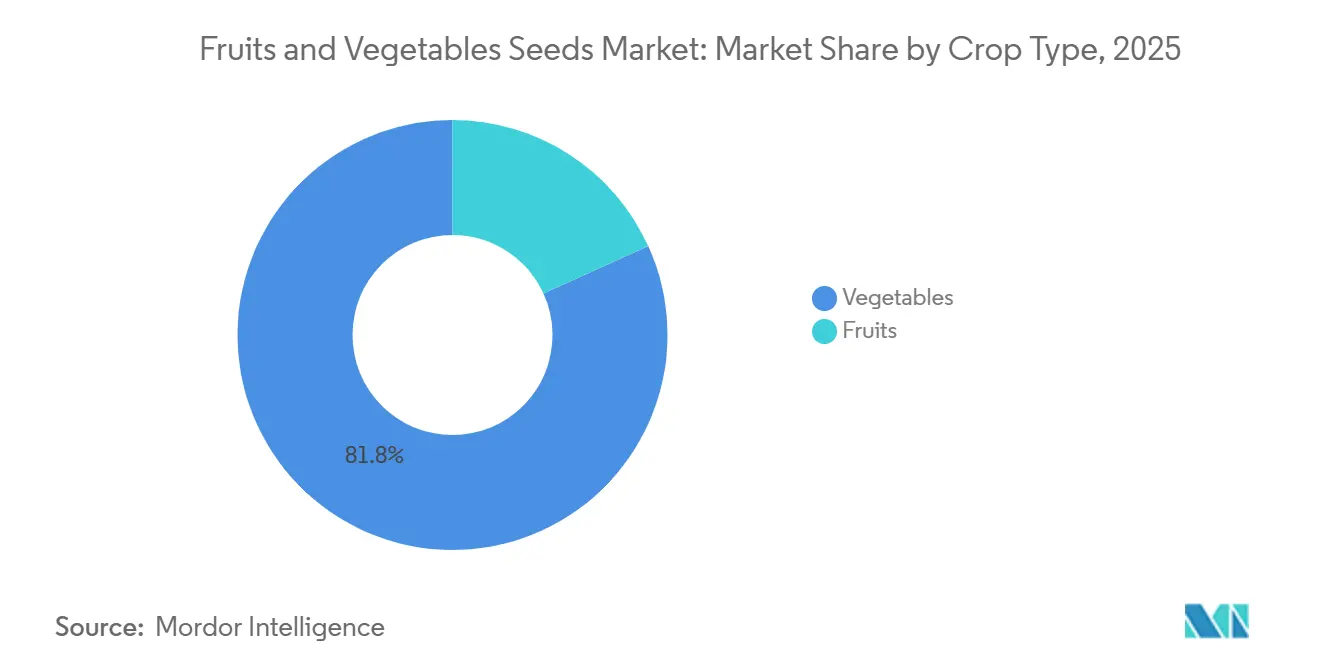

- By crop type, vegetables held the largest 81.8% share in 2025, while fruits are forecast to grow at the fastest CAGR of 9.2% from 2026 to 2031.

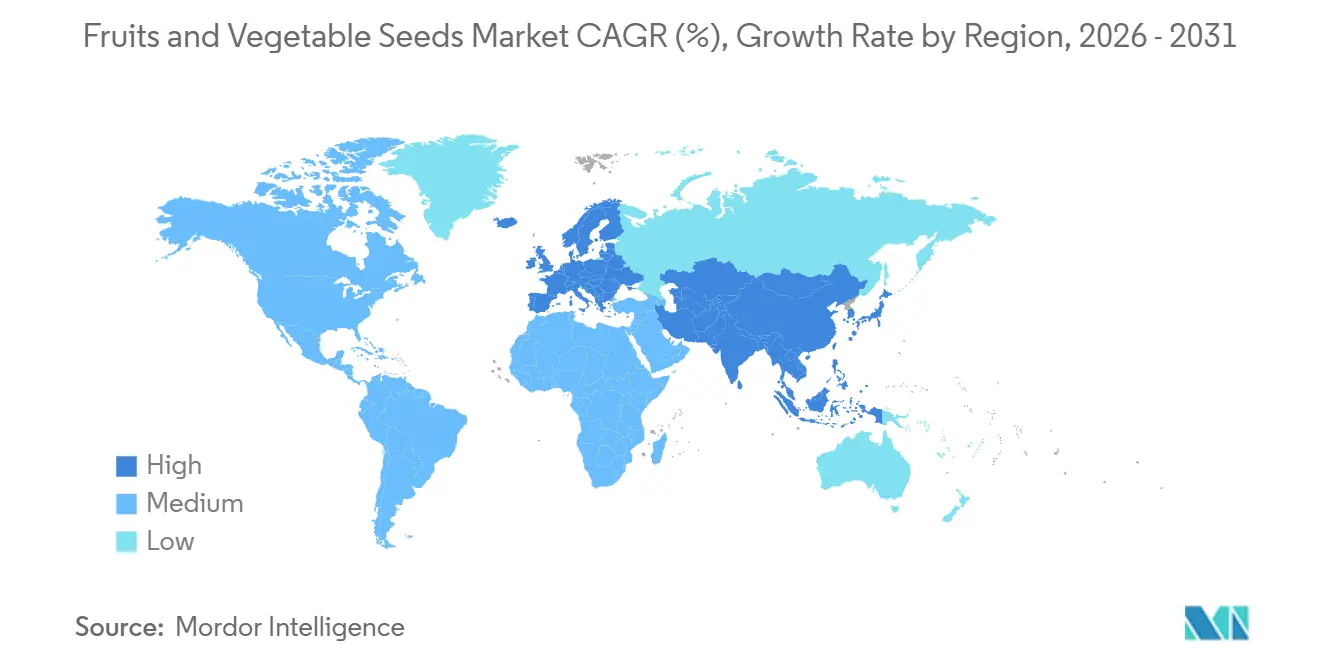

- By geography, Europe led with the largest 31.6% share in 2025, while Asia-Pacific is projected to expand fastest at a CAGR of 6.1% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fruits and Vegetables Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of hybrid and disease-resistant seeds | +1.4% | Global, with strongest density in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Expansion of protected cultivation and controlled environment agriculture | +0.9% | Asia-Pacific, Middle East, and Europe | Medium term (2-4 years) |

| Higher demand for high-yield seed genetics in commercial horticulture | +0.7% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Shift toward organic and non-GMO produce supply chains | +0.5% | North America, Europe, with spillover into Asia-Pacific | Long term (≥ 4 years) |

| Seed traceability and quality standardization requirements in export markets | +0.4% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Climate volatility accelerating demand for trait-improved varieties | +0.8% | Global, most acute in South Asia, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Hybrid and Disease-Resistant Seeds

The increasing need to safeguard crop yields from emerging diseases is driving the adoption of hybrid and disease-resistant seeds in commercial fruits and vegetables production. Farmers are progressively replacing conventional seed varieties with advanced hybrids that provide enhanced resistance traits and more consistent performance under disease pressure. This shift is particularly pronounced in tomato cultivation, where disease outbreaks can lead to substantial economic losses. According to the UK Department for Environment, Food and Rural Affairs (DEFRA, 2024), in its Tomato Brown Rugose Fruit Virus (ToBRFV) Policy Review, ToBRFV has the potential to infect up to 100% of a crop, causing yield losses ranging from 25% to 70%[1]Source: UK Department for Environment, Food & Rural Affairs (DEFRA), “Tomato Brown Rugose Fruit Virus (ToBRFV) Policy Review,” planthealthportal.defra.gov.uk. These risks are prompting seed companies to intensify their resistance-breeding initiatives, positioning hybrid and disease-resistant seeds as a significant growth driver in the fruits and vegetables seeds market.

Expansion of Protected Cultivation and Controlled Environment Agriculture

The growth of protected cultivation and controlled environment agriculture is driving significant demand for specialized fruit and vegetable seeds tailored for greenhouse and polyhouse production. These systems require seed varieties with characteristics such as uniform growth, extended harvest periods, and high performance under intensive management practices. As greenhouse cultivation continues to expand, growers are increasingly prioritizing premium seeds with enhanced productivity and disease resistance. For instance, the Rivenhall Greenhouse project, which received planning approval from Essex County Council in April 2026, is projected to produce up to 30,000 metric tons of tomatoes annually at full capacity. This highlights the scale of new controlled-environment production initiatives being developed in Europe. Such investments are bolstering the demand for high-value seed varieties, contributing to the growth of the fruits and vegetables seeds market.

Higher Demand for High-Yield Seed Genetics in Commercial Horticulture

The growing commercialization of horticulture is increasing demand for high-yield seed genetics that ensure consistent performance, uniformity, and quality throughout the production cycle. Stakeholders, including growers, retailers, and processors, are prioritizing seed traits that enhance productivity, disease resistance, and reliable marketable yields. This trend is driving investments in advanced breeding programs and improved seed technologies. In line with this development, the United States Department of Agriculture (USDA), through its Agricultural Marketing Service (AMS), announced USD 72.9 million in grant funding for 2025 under the Specialty Crop Block Grant Program[2]Source: U.S. Department of Agriculture (USDA) Agricultural Marketing Service (AMS), “USDA Announces $72.9 Million in Grant Funding Available through Specialty Crop Block Grant Program,” ams.usda.gov.. This funding aims to enhance the competitiveness of fruits, vegetables, tree nuts, horticulture, and nursery crops. Such initiatives highlight the critical role of high-performance seed genetics in modern horticultural production, fostering growth in the fruits and vegetables seeds market.

Shift Toward Organic and Non-GMO Produce Supply Chains

The growing focus on organic and non-GMO produce supply chains is driving demand for certified, traceable seed varieties in the fruits and vegetables seed market. Retailers and exporters are tightening sourcing standards, encouraging growers to adopt certified organic production systems and compliant seed varieties. According to the Research Institute of Organic Agriculture (FiBL) and IFOAM Organics International (2026), global organic vegetable cultivation covered approximately 536,418 hectares, while organic fruit cultivation reached around 660,260 hectares in 2024. The large areas of dedicated certified organic horticultural production are increasing demand for organic and non-GMO fruit and vegetable seeds that meet certification and traceability requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High royalty and trait licensing costs increase seed prices | -0.7% | Global, most acute in South America and South Asia | Medium term (2-4 years) |

| Long breeding cycles delay commercial launches | -0.5% | Global | Long term (≥ 4 years) |

| Tight phytosanitary and genetic purity compliance burden | -0.4% | Global, strongest in Europe and North America | Short term (≤ 2 years) |

| Grower price sensitivity in smallholder and emerging markets | -0.6% | Africa, South Asia, and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long Breeding Cycles Delay Commercial Launches

Long breeding and commercialization cycles continue to be a significant restraint for the fruits and vegetables seeds market, limiting the pace at which improved varieties become available to growers. The development of new seed varieties involves extensive processes, including breeding, trait selection, and multi-location validation, to ensure consistent performance across diverse growing conditions. Despite advancements in breeding technologies, commercial launches often require decades to complete. For instance, according to Cornell AgriTech (2025), the Northstar broccoli hybrid, released in September 2025 in collaboration with Bejo Zaden, took over 24 years from initial line development to its commercial release[3]Source: Cornell University, “Public-Private Partnership Results in New Broccoli Hybrid, ‘Northstar’,” news.cornell.edu.. These prolonged development timelines delay the introduction of improved disease-resistant and high-yield varieties, hindering the market's ability to adapt swiftly to evolving production challenges and changing grower needs.

Tight Phytosanitary and Genetic Purity Compliance Burden

Stringent phytosanitary and genetic purity requirements are driving up compliance costs and increasing operational complexity in the fruits and vegetables seeds market. Seed companies are required to implement extensive documentation, traceability systems, and quality-control procedures to meet international trade standards, adding significant challenges for exporters. Smaller seed producers face greater difficulties, as the investments needed for compliance can restrict their access to global markets. Highlighting this development, the International Plant Protection Convention (IPPC, 2024) mandates ISPM 38 for the International Movement of Seeds, which requires a systems-based approach. This approach includes traceability, pest-risk management, and documented phytosanitary measures throughout the seed supply chain. These regulatory requirements result in higher testing, certification, and administrative costs, hindering supplier expansion and reducing broader participation in the fruits and vegetables seeds market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrid Penetration Near Saturation in Core Crops

Hybrids held the largest 80.1% share in 2025. Hybrid varieties maintain their dominant position due to their advantages in yield consistency, crop uniformity, vigor, and resistance management. Commercial growers increasingly prioritize reliable field performance and predictable product quality, making hybrids the preferred choice across various fruit and vegetable crops. Their ability to integrate multiple desirable traits within a single variety further supports their adoption in intensive production systems. Consequently, hybrids remain the primary revenue-generating segment within modern seed portfolios.

Fruits and vegetables seeds market size for hybrids is also forecast to grow fastest at a CAGR of 5.7% from 2026 to 2031. This growth is driven by the expansion of commercial cultivation, the rise of protected agriculture, and increasing demand for improved crop performance. While open-pollinated varieties continue to hold relevance in specific crops and farming systems where seed saving or lower input costs are priorities, breeding innovation across the industry remains predominantly focused on hybrid development. This focus is attributed to hybrids' ability to deliver differentiated value to growers. The sustained emphasis on hybrid breeding is projected to solidify their position as the leading breeding technology throughout the forecast period.

By Cultivation Mechanism: Protected Cultivation Defines the Premium Seed Tier

Open-field cultivation accounted for the largest 69.4% share in 2025, so it remained the largest cultivation mechanism in the fruits and vegetables seeds market. This dominance is attributed to the extensive acreage dedicated to outdoor fruit and vegetable production in major agricultural regions. Open-field systems cater to a wide range of commercial, semi-commercial, and smallholder operations, driving significant demand for seeds across various crop categories. The segment benefits from its scale and widespread adoption, particularly in areas with limited greenhouse infrastructure. As a result, open-field cultivation continues to provide the largest volume base for seed suppliers in global agricultural markets.

The protected cultivation is projected to expand at the fastest CAGR of 7.4% from 2026 to 2031. This growth is driven by the increasing adoption of greenhouse and polyhouse systems, which require specialized seed varieties with specific performance characteristics. Controlled growing environments emphasize uniformity, productivity, disease resistance, and quality consistency, leading to strong demand for premium genetics. These systems also promote faster varietal replacement and higher-value seed purchases. As protected agriculture expands across various regions, it is projected to remain a key area for product development and value creation within the industry.

By Crop Type: Vegetables Sustain Scale Dominance as Fruit Seed Genetics Accelerate

Vegetables accounted for the largest share of 81.8% in 2025, maintaining their dominant position in the fruits and vegetables seeds market. This is supported by extensive commercial cultivation, frequent varietal replacement, and continuous investments in breeding programs targeting higher yields, disease resistance, and improved quality traits. Hybrid seed adoption remains particularly strong across major vegetable crops due to their superior productivity and uniformity. Seed companies are increasingly developing varieties adapted to changing climatic conditions, while growers continue replacing conventional cultivars with improved hybrids to enhance production efficiency, crop resilience, and marketable quality across both domestic and export-oriented vegetable production.

Fruits are forecast to grow at the fastest CAGR of 9.2% from 2026 to 2031, supported by increasing demand for premium fruit varieties and improved planting material. Breeding activities are increasingly focused on enhancing fruit quality, disease resistance, shelf life, and climate adaptability to meet evolving consumer and commercial production requirements. Hybrid watermelon and melon varieties continue to gain popularity due to their consistent performance and superior fruit characteristics, while protected cultivation is accelerating innovation in crops such as strawberries. Ongoing improvements in rootstock genetics and specialized breeding programs are further supporting long-term growth across the fruit seed segment.

Geography Analysis

Europe led with the largest 31.6% share in 2025. The region's leadership is attributed to its well-established vegetable breeding and seed production companies. Countries such as the Netherlands, France, Germany, and Italy benefit from advanced breeding infrastructure, robust intellectual property protection, and highly developed greenhouse cultivation systems. Additionally, Europe serves as a global hub for seed research, processing, and export activities. These factors collectively reinforce Europe's dominance in the development and distribution of commercial fruit and vegetable seeds.

Asia-Pacific is projected to expand fastest at a CAGR of 6.1% from 2026 to 2031. This growth is driven by increasing vegetable consumption, the expansion of protected cultivation practices, and the rising adoption of hybrid seed technologies. China and India play a pivotal role in the region's growth due to their extensive agricultural sectors and ongoing investments in seed improvement programs. Rapid urbanization and evolving dietary preferences are further driving the need for enhanced production efficiency and quality improvements in horticultural crops. These trends are boosting demand for advanced seed varieties, positioning Asia-Pacific as a key driver of future market growth.

The strong commercial value of North America's horticulture sector continues to drive sustained demand for high-performance fruit and vegetable seed varieties. The region is characterized by high hybrid adoption, advanced breeding technologies, and strong investment in productivity, disease resistance, and premium quality traits. According to the United States Department of Agriculture National Agricultural Statistics Service (2025), the United States tomato crop was valued at USD 1.97 billion in 2024, reflecting the economic importance of commercial vegetable production. This large-scale, high-value production encourages growers to invest in improved hybrid seeds with superior yield, resilience, and quality attributes, supporting continuous innovation and long-term growth in the fruits and vegetables seeds market.

Competitive Landscape

The fruits and vegetables seeds market is moderately consolidated, with a few large multinational companies accounting for a significant share of global commercial seed sales. Major players in the market include Bayer AG, Syngenta Group, BASF SE, Groupe Limagrain Holding, and Sakata Seed Corporation. These companies maintain their strong market positions through extensive breeding programs, global distribution networks, and diversified product portfolios. Competition is particularly pronounced in vegetable crops, where continuous varietal development and frequent product replacement cycles drive innovation and market differentiation.

Leading companies are reinforcing their market positions by investing in breeding capabilities, production infrastructure, and strategic partnerships. Product development efforts are increasingly focused on traits such as disease resistance, yield stability, quality improvements, and adaptability to protected cultivation systems. Additionally, companies are expanding research into advanced breeding technologies to accelerate varietal improvement and reduce development timelines. Meanwhile, regional suppliers play a critical role by catering to local production systems and addressing crop-specific needs that may not be prioritized by larger multinational firms.

Competition in the market is further shaped by access to proprietary genetics, production infrastructure, and regional breeding capabilities. For instance, Bayer AG inaugurated its Khon Kaen Vegetable Seeds Production Center in Thailand in February 2026, following an investment of THB 310 million (USD 8.7 million). This facility aims to strengthen seed production and supply for the Asia-Pacific region and international markets. The investment underscores the importance of dedicated seed production capacity in ensuring supply reliability and supporting the commercialization of advanced seed varieties. Consequently, companies with robust production networks and strong breeding resources maintain a competitive edge in expanding their market presence and meeting the needs of global growers.

Fruits and Vegetables Seeds Industry Leaders

Bayer AG

Syngenta Group

BASF SE

Groupe Limagrain Holding

Sakata Seed Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: BASF SE has completed the acquisition of Noble Seeds Pvt. Ltd. in India. This acquisition enhances its vegetable seed portfolio by adding cauliflower and radish genetics, while also expanding its breeding capabilities and market presence within the Indian fruits and vegetables seeds market.

- February 2026: Bayer AG has opened its Vegetable Seeds Production Center in Khon Kaen, Thailand, following an investment of THB 310 million (approximately USD 8.7 million). This initiative enhances the production capacity of export-grade vegetable seeds for the Asia-Pacific region and global markets.

- September 2025: Cornell AgriTech, in partnership with Bejo Zaden B.V., introduced the Northstar broccoli hybrid, a climate-resilient variety developed over 24 years to enhance performance in warmer growing conditions across the Northeastern United States and Canada.

Global Fruits and Vegetables Seeds Market Report Scope

Fruit and vegetable seeds serve as planting materials for cultivating horticultural crops. These seeds are developed to enhance yield, quality, disease resistance, climate adaptability, and overall crop performance in both commercial and protected farming systems. The Fruits and Vegetables Seeds Market Report is Segmented by Breeding Technology (Hybrids and Open Pollinated Varieties and Hybrid Derivatives), by Cultivation Mechanism (Open Field and Protected Cultivation), by Crop Type (Fruits and Vegetables), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | |

| Insect Resistant Hybrids | ||

| Other Traits | ||

| Open Pollinated Varieties and Hybrid Derivatives | ||

| Open Field |

| Protected Cultivation |

| Fruits | Watermelon |

| Melon | |

| Strawberry | |

| Citrus | |

| Apple | |

| Banana | |

| Other Fruits | |

| Vegetables | Onion |

| Lettuce | |

| Carrot | |

| Cabbage | |

| Cauliflower | |

| Broccol | |

| Other Vegetables |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Netherlands | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide Tolerant Hybrids | ||

| Insect Resistant Hybrids | |||

| Other Traits | |||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| By Cultivation Mechanism | Open Field | ||

| Protected Cultivation | |||

| By Crop Type | Fruits | Watermelon | |

| Melon | |||

| Strawberry | |||

| Citrus | |||

| Apple | |||

| Banana | |||

| Other Fruits | |||

| Vegetables | Onion | ||

| Lettuce | |||

| Carrot | |||

| Cabbage | |||

| Cauliflower | |||

| Broccol | |||

| Other Vegetables | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Netherlands | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East | Turkey | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the fruits and vegetables seeds market?

The fruits and vegetable seeds current market size valued at USD 15.53 billion in 2026.

Which seed type leads revenue in fruit and vegetable seeds?

Vegetable seeds lead the market with the largest 81.8% share in 2025.

Why are hybrids so important in this sector?

Hybrids held the largest 80.1% share in 2025 and are also the fastest-growing breeding technology at 5.7% CAGR from 2026 to 2031 because growers value yield, uniformity, and disease resistance.

Which cultivation method is growing fastest?e in 2025 and are also the fastest-growing breeding technology at 5.7% CAGR from 2026 to 2031 because growers value yield, uniformity, and disease resistance.

Protected cultivation is the fastest-growing cultivation mechanism with a 7.4% CAGR from 2026 to 2031.

Page last updated on: