Isomalt Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

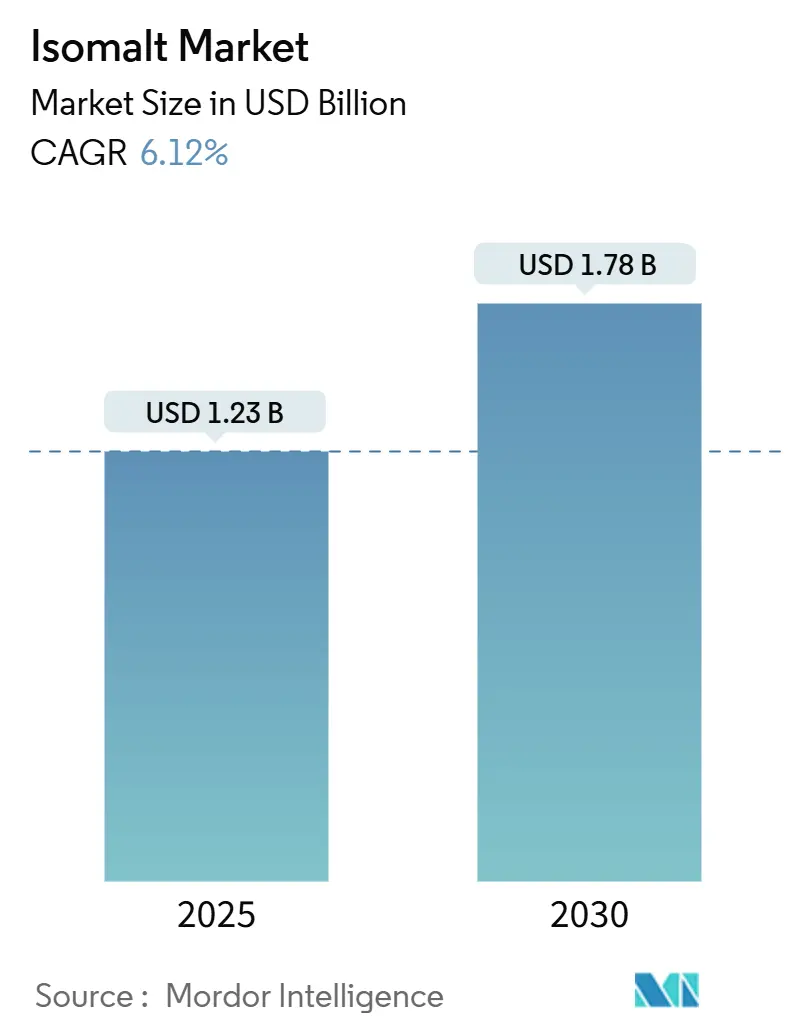

| Market Size (2025) | USD 1.23 Billion |

| Market Size (2030) | USD 1.78 Billion |

| Growth Rate (2025 - 2030) | 6.12% CAGR |

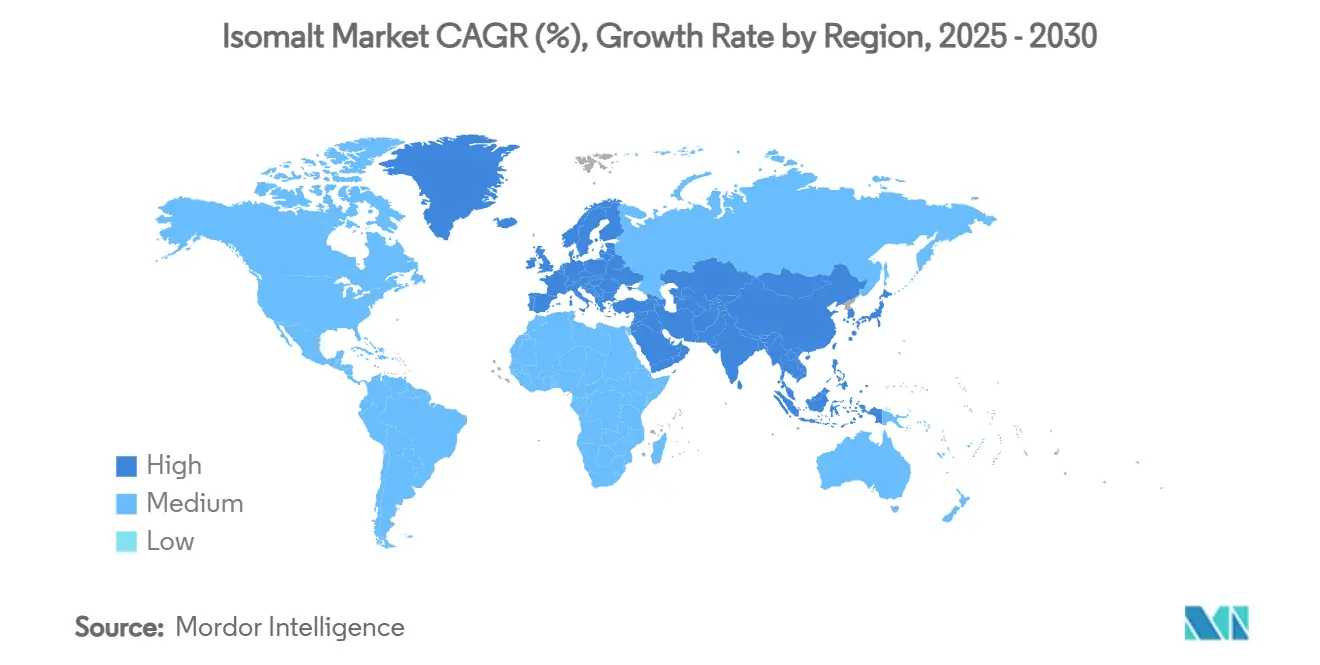

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

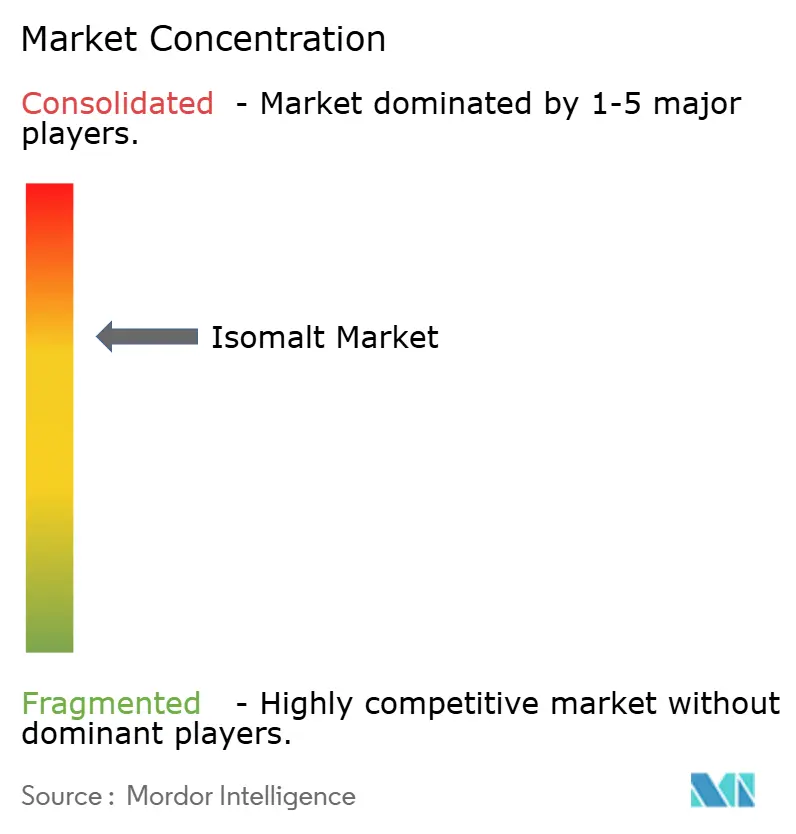

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Isomalt Market Analysis by Mordor Intelligence

In 2025, the global isomalt market size was valued at USD 1.23 billion. Forecasts suggest it will grow to USD 1.78 billion by 2030, registering a CAGR of 6.12%. The demand is steadily increasing due to consistent regulatory approvals, a rising consumer focus on sugar reduction, and advancements in food processing technology. Europe leads in sales, supported by four decades of industrial expertise and regular E-number authorizations. In contrast, the Asia Pacific region is experiencing the fastest growth, driven by a growing diabetic and pre-diabetic population. Product developers increasingly prefer isomalt for its heat stability, clean sweetness, and anticaries properties, which are driving its use in bakery, confectionery, and oral-care products. While European beet-sugar output has traditionally influenced supply-side dynamics, diversification into cane-based sources in Asia and Latin America is reducing raw-material risks. The competitive landscape is moderately intense. Key players leverage integrated agribusiness networks and formulation support teams to maintain margins, even as emerging sugars like allulose raise the bar for innovation.

Key Report Takeaways

- By form, powder/crystalline held 47.12% of the 2024 isomalt market share and will grow at a 6.80% CAGR through 2030, while liquid grades outpace on-processing convenience.

- By application, confectionery captured 55.67% market share in 2024, whereas oral-care products are forecast to advance at a 7.67% CAGR to 2030.

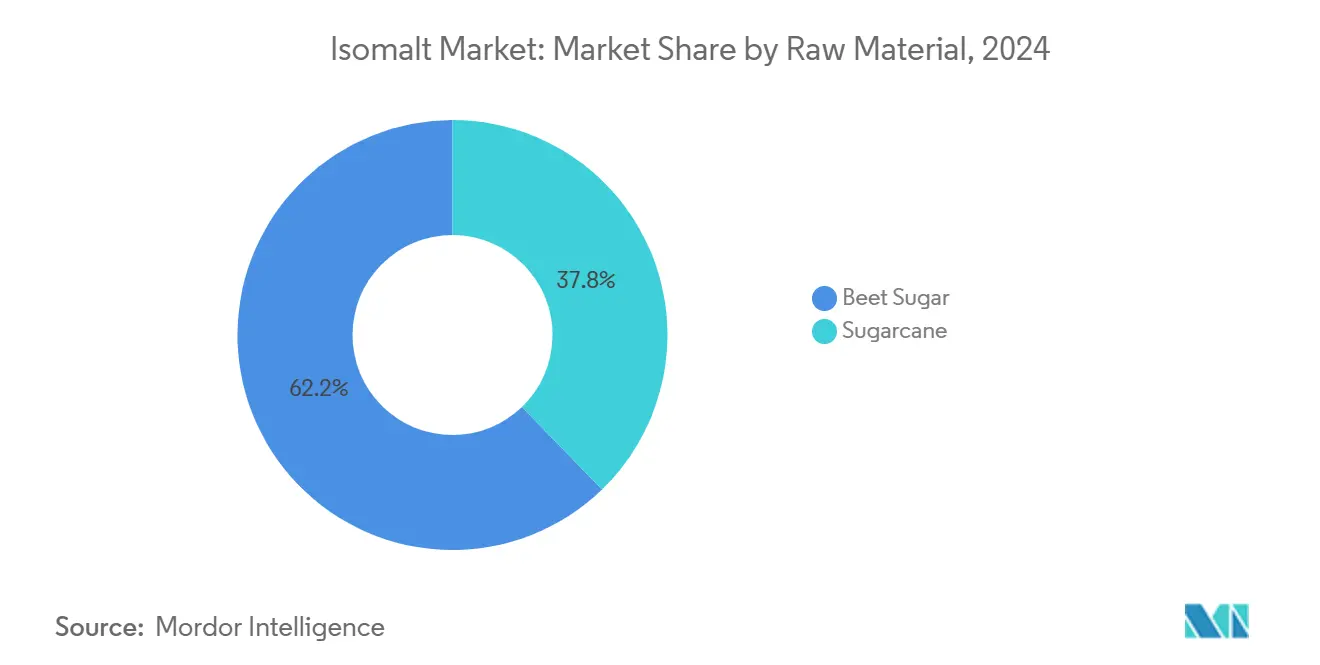

- By raw material, beet-sugar routes contributed 62.23% of the 2024 isomalt market share, and sugarcane-derived output is projected to expand at a 7.34% CAGR during 2025-2030.

- By geography, Europe led with a 33.24% share in 2024, yet Asia Pacific is on track for the quickest regional CAGR of 8.01% through 2030.

Global Isomalt Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for sugar-free confectionery | +1.1% | Global, with strongest growth in North America and Europe | Medium term (2-4 years) |

| Rising diabetic and pre-diabetic population | +0.8% | Global, with highest impact in Asia Pacific and North America | Long term (≥ 4 years) |

| Favorable global approvals for polyols (E953, GRAS) | +0.9% | Global, with recent expansions in emerging markets | Short term (≤ 2 years) |

| Heat-stable functionality boosts bakery adoption | +0.7% | Europe and North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Pharma shift to isomalt for direct-compression tablets | +0.6% | Global, with concentration in developed pharmaceutical markets | Long term (≥ 4 years) |

| 3-D food printing and decorative sugar-arts applications | +0.4% | North America and Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sugar-Free Confectionery

As consumers increasingly prioritize health, confectionery manufacturers are reformulating products, opting for sugar alternatives that preserve taste and texture. Isomalt stands out as a preferred bulk sweetener for premium sugar-free applications, offering 50% fewer calories than sugar and a clean, sucrose-like taste, as highlighted by Cargill. Research from MDPI underscores isomalt's advantage: it notably lessens blood glucose and insulin responses when compared to sugar, making it a prime choice for diabetic-friendly products. Furthermore, the FDA recognizes isomalt's non-cariogenic properties, enabling manufacturers to tout dental health benefits, thus enhancing product appeal beyond mere calorie reduction. For over 40 years, European regulatory frameworks have championed this trend, solidifying isomalt's dominance as the go-to bulk sweetener for sugar-free candies in the region. This blend of regulatory endorsement and rising consumer demand fuels a self-reinforcing cycle, propelling market growth in this key segment.

Rising Diabetic and Pre-Diabetic Population

The global diabetes epidemic is driving significant changes in food industry dynamics, fueling a growing demand for low-glycemic ingredients. World Health Organization[1]Source: World Health Organization, “Urgent action needed as global diabetes cases increase four-fold over past decades,” who.int data indicates that diabetes cases have increased fourfold since 1990, with over 800 million adults currently affected. This trend extends beyond diagnosed diabetics, as health-conscious consumers increasingly adopt preventive dietary measures. Isomalt, known for its low glycemic index and minimal impact on blood glucose levels, is particularly effective for diabetic dietary management. Research shows it has negligible effects on insulin response compared to traditional sugars. The UN's 2025 meeting on diabetes management is expected to introduce global health policies that could further boost the demand for approved sugar alternatives. Products with established safety profiles and regulatory approvals are gaining favor among healthcare providers, giving isomalt a competitive edge over newer alternatives.

Favorable Global Approvals for Polyols (E953, GRAS)

Regulatory momentum is building for polyol sweeteners. Isomalt, in particular, is reaping the rewards of its established GRAS status in the U.S. and the E953 approval in Europe. In 2024, the FDA processed 57 GRAS notifications, approving 13 substances. This showcases the FDA's openness to food ingredient innovations, all while upholding stringent safety standards. Meanwhile, the European Food Safety Authority's recent nod to isomaltulose syrup as a novel food under Regulation (EU) 2015/2283 hints at a broader acceptance of sugar alcohol applications[2]Source: European Food Safety Authority, “Safety of Isomaltulose Syrup as a Novel Food,” efsa.onlinelibrary.wiley.com. This could pave the way for expanded uses of isomalt. Additionally, the Joint Expert Committee on Food Additives (JECFA) has cleared isomalt for consumption, notably without setting an acceptable daily intake limit. This offers manufacturers greater flexibility in their formulations. Such regulatory endorsements not only facilitate market expansion into new regions and application categories but also ease compliance challenges for manufacturers.

Heat-Stable Functionality Boosts Bakery Adoption

Isomalt's thermal stability makes it a valuable ingredient in high-temperature food processing applications, where traditional sugar alcohols often fail to perform effectively. It retains its structural integrity and sweetening properties during baking processes, making it an excellent choice for products such as breads, pastries, and other baked goods that require prolonged exposure to heat. Unlike alternative sweeteners that may degrade or lose functionality under heat stress, isomalt maintains its bulk properties and contributes to texture development, addressing both sweetening and functional requirements in baked products. This dual-purpose functionality not only simplifies ingredient formulations for manufacturers but also ensures that the final product meets the high-quality standards demanded by consumers. The growing adoption of isomalt in the bakery sector reflects a broader industry movement toward clean-label formulations, which focus on reducing ingredient complexity while delivering consistent functional performance across various processing conditions. This trend highlights the increasing consumer preference for transparent and simplified ingredient lists without compromising on product quality or performance.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gastro-intestinal tolerance limits & labelling rules | -0.5% | Global, with strictest enforcement in North America and Europe | Short term (≤ 2 years) |

| Volatility in beet-sugar feedstock prices | -0.3% | Europe primarily, with spillover effects globally | Medium term (2-4 years) |

| Supply-chain concentration in Europe creates risk | -0.4% | Global supply chains, with highest impact in non-European markets | Medium term (2-4 years) |

| Emerging competition from rare sugars (e.g., allulose) | -0.2% | North America and Asia-Pacific, expanding to Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gastro-Intestinal Tolerance Limits & Labelling Rules

Digestive tolerance warnings, mandated by regulatory bodies, pose marketing hurdles that hinder product positioning and acceptance among key demographics. The FDA requires products with over 15 grams of polydextrose per serving to carry warning labels, citing potential laxative effects. This mandate extends to other polyols, like isomalt. Such labeling not only induces consumer hesitation but also restricts portion sizes in food applications. This limitation curtails market growth in sectors where higher sweetener concentrations could be advantageous. Echoing the FDA's stance, the European Union also mandates warnings for potential mild gastrointestinal side effects. Cargill states that customers are responsible for complying with laws governing usage levels. Given that tolerance thresholds differ from person to person, there's an element of unpredictability in consumer experiences. If mishandled, especially in formulation and labeling, it could tarnish a brand's reputation. Manufacturers face the challenge of optimizing sweetening potency while ensuring digestive comfort. This often leads to intricate formulation methods, driving up production costs and making it tough to compete with traditional sugar applications.

Volatility in Beet-Sugar Feedstock Prices

Fluctuations in the European beet sugar market are creating cost pressures on isomalt production chains, impacting pricing strategies and profit margins across the value network. Since October 2024, EU sugar prices have significantly declined, driven by increased imports from Ukraine and broader geopolitical factors reshaping agricultural trade. United States Department of Agriculture forecasts indicate that beet sugar production in the EU27 for the 2024/25 period will grow by 4%, reaching approximately 15.4 million metric tons[3]Source: U.S. Department of Agriculture, “European Union: Sugar Semi-annual,” fas.usda.gov. However, with consumption remaining stable at 16.5 million metric tons, this imbalance between supply and demand is contributing to price volatility. The geographic concentration of beet sugar production in Europe increases susceptibility to weather changes, shifts in agricultural policies, and trade disruptions, which can quickly affect feedstock availability and pricing. These cost fluctuations are driving isomalt producers to adopt flexible pricing strategies, potentially reducing their competitiveness against alternative sweeteners with more stable cost structures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominates While Liquid Gains Processing Advantages

In 2024, powder/crystalline isomalt accounts for 47.12% of the market share, highlighting its established role in confectionery manufacturing, where solid forms are valued for their excellent handling and storage stability. Liquid/syrup formulations are experiencing growth at a 6.80% CAGR through 2030, primarily due to their ability to enhance processing efficiencies in industrial food production by integrating seamlessly into automated mixing systems. Granular forms occupy a middle ground, offering a balance between handling convenience and effective dissolution properties.

The growth of the liquid segment reflects a broader industry shift towards automation, with manufacturers increasingly adopting ingredients that simplify processing and reduce labor demands. Cargill, a prominent player, supplies both crystalline and liquid grades of isomalt, ensuring consistent quality and reliable supply for various application needs. Powder forms remain advantageous in applications requiring precise dosing and extended shelf life, particularly in consumer-facing products where packaging and storage considerations favor solid ingredients. Form segmentation is increasingly aligning with manufacturing scale, as large industrial producers prefer liquid systems, while smaller specialty manufacturers opt for powder formulations due to their flexibility and ease of inventory management.

By Application: Confectionery Leadership Faces Oral Care Disruption

Oral care products are poised to be the fastest-growing segment, with a projected 7.67% CAGR through 2030, driven by isomalt's FDA-approved anticaries properties. Confectionery retains its leading position with a 55.67% market share in 2024, supported by its four-decade history in sugar-free candy applications. Isomalt serves as an excipient in direct-compression tablet manufacturing for pharmaceuticals and dietary supplements, while dairy products and processed foods offer emerging growth opportunities.

Clinical studies underscore isomalt's effectiveness in mouthrinse formulations. Combinations of isomalt, fluoride, and cetylpyridinium chloride have proven significantly more effective than fluoride-only formulations in preventing tooth demineralization. In the bakery segment, isomalt's heat-stable functionality enables its use in high-temperature processing, where other sweeteners may degrade. Pharmaceutical applications capitalize on isomalt's compressibility and stability, making it ideal for direct-compression tablet manufacturing, where consistent flow characteristics are critical. This diversification across segments reduces market concentration risks while creating multiple growth opportunities to counterbalance cyclical variations in specific categories.

By Raw Material: Beet Sugar Dominance Faces Sugarcane Competition

In 2024, beet sugar-derived isomalt holds a 62.23% market share, highlighting Europe's well-established production infrastructure and decades of processing expertise. Meanwhile, sugarcane-based production is growing at a 7.34% CAGR through 2030, driven by geographic diversification efforts and cost optimization measures in regions with abundant sugarcane resources. The segmentation of raw materials increasingly emphasizes regional agricultural strengths and supply chain efficiency rather than differences in the functionality of end products.

European beet sugar producers face challenges from rising Ukrainian imports and price volatility. According to USDA data, EU27 beet sugar production is projected at 15.4 million metric tons for the 2024/25 period, while consumption remains stable at 16.5 million metric tons. In contrast, sugarcane-derived production offers advantages in geographic diversification and potentially lower feedstock costs in tropical regions, where year-round sugarcane harvesting is possible. The production process remains consistent across raw material sources, involving the enzymatic conversion of sucrose to isomaltulose, followed by hydrogenation to produce isomalt. Market dynamics increasingly favor suppliers capable of sourcing from multiple raw material streams, enabling cost optimization and reducing supply chain risks associated with reliance on a single source.

Geography Analysis

In 2024, Europe holds its leading position with a 33.24% market share, supported by more than four decades of robust production infrastructure and regulatory frameworks that have facilitated isomalt adoption. The region excels in sugar alcohol processing, with key players like BENEO and Südzucker utilizing local beet sugar resources in their integrated production facilities. However, the region faces challenges from Ukrainian sugar imports and price volatility, as reflected in Südzucker's preliminary revenue decline to EUR 9.7 billion in 2024/25, compared to EUR 10.3 billion in the previous year. To address these challenges, European manufacturers are focusing on improving operational efficiencies and pursuing geographic diversification to maintain competitiveness. Europe's regulatory leadership in polyol approvals continues to drive market development, exemplified by EFSA's recent approval of isomaltulose syrup, which highlights ongoing regulatory support for sugar alcohol innovations.

Asia Pacific is the fastest-growing region, with an 8.01% CAGR projected through 2030. This growth is driven by a rising diabetic population and rapid modernization of the food industry in major economies. China's approval of isomalt as a new resource food, with usage permitted across various categories (excluding infant foods), has established a critical regulatory foundation for market growth. The region is experiencing increased health awareness among middle-class consumers and a growing preference for Western-style processed foods that incorporate sugar alternatives. Beyond traditional confectionery applications, Japan's advanced food technology sector and India's expanding pharmaceutical industry provide additional growth opportunities. With cost-effective manufacturing and proximity to growing consumer markets, Asia Pacific is well-positioned for sustained market share growth throughout the forecast period.

North America, though a mature market, remains stable and benefits from its established GRAS regulatory status and advanced food processing industries that value isomalt's functional properties. The region's high diabetes prevalence, as reported by WHO, sustains demand for low-glycemic sweeteners across various applications. U.S. manufacturers are increasingly targeting premium applications where isomalt's superior taste and functional benefits justify higher prices compared to alternative sweeteners. The region's strong pharmaceutical sector drives demand for isomalt as an excipient in tablet production, while its expanding oral care applications leverage FDA-approved anticaries claims. Although South America and the Middle East & Africa are smaller markets, they offer significant long-term growth potential as regulatory frameworks advance and consumer awareness improves.

Competitive Landscape

The isomalt market exhibits moderate concentration, reflecting established players who have built significant production capabilities and regulatory expertise over decades of commercial operation. Market leaders leverage integrated supply chains that span from raw material sourcing through final product distribution, creating barriers to entry for new competitors while enabling cost optimization and quality control.

Strategic patterns emphasize vertical integration, with major players controlling beet sugar or sugarcane feedstock sources alongside processing facilities to manage input cost volatility and ensure supply security. Technology deployment focuses on process optimization and product differentiation, with companies investing in enzymatic conversion efficiency improvements and purification technologies that enhance product quality while reducing manufacturing costs. Ingredion's acquisition of Mannitab Pharma Specialties demonstrates the strategic importance of pharmaceutical applications, where specialized expertise in excipient manufacturing creates defensible market positions.

White-space opportunities exist in emerging applications such as 3D food printing and decorative sugar arts, where isomalt's unique crystallization properties provide functional advantages that traditional sweeteners cannot match. The competitive landscape increasingly rewards companies that can navigate complex regulatory environments while maintaining operational flexibility to serve diverse application requirements across multiple geographic markets.

Isomalt Industry Leaders

IHC - I.H. Chempharm GmbH i.L.

Cargill Incorporated

Foodchem International Corporation

Merck Group

FREUND Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BENEO GmbH has inaugurated a state-of-the-art pulse processing plant at its site in Obrigheim, Germany, marking a significant expansion of its production capabilities. This new facility, developed with an investment of approximately €50 million by the Südzucker Group, focuses on processing locally grown faba beans into high-quality, plant-based ingredients for food and feed applications.

- July 2024: Covestro (India) opened a new Polyol Tank Farm in Kandla, Gujarat's Kutch district. The facility enhances supply chain efficiency and addresses increasing customer demand. The tank farm stores polyols, essential materials for Covestro's Performance Material Business.

- June 2024: Tate & Lyle announced its acquisition of CP Kelco for USD 1.8 billion, creating a leading global specialty food and beverage solutions business with enhanced capabilities in hydrocolloids, including pectin and specialty gums. The merger aims for revenue growth of 4-6% per annum and cost synergies of at least USD 50 million by the second full financial year following completion.

Global Isomalt Market Report Scope

| Crystalline/Powder |

| Granular |

| Liquid/Syrup |

| Food and Beverges | Confectionery |

| Bakery Products | |

| Dairy Products | |

| Others(Processed Foods, Beverages) | |

| Pharmaceuticals and Dietary Supplements | |

| Oral Care Products | |

| Others(Cosmetics, Homecare) |

| Beet Sugar |

| Sugarcane-derived |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Netherlands | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South africa | |

| Rest of Middle East and Africa |

| By Form | Crystalline/Powder | |

| Granular | ||

| Liquid/Syrup | ||

| By Application | Food and Beverges | Confectionery |

| Bakery Products | ||

| Dairy Products | ||

| Others(Processed Foods, Beverages) | ||

| Pharmaceuticals and Dietary Supplements | ||

| Oral Care Products | ||

| Others(Cosmetics, Homecare) | ||

| By Raw Material Type | Beet Sugar | |

| Sugarcane-derived | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Netherlands | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the isomalt market by 2030?

Forecasts place the isomalt market at USD 1.78 billion by 2030, up from USD 1.23 billion in 2025.

Which region is expected to expand fastest in isomalt demand?

Asia-Pacific is forecast to log an 8.01% CAGR between 2025 and 2030, outpacing all other regions.

Why do confectionery makers prefer isomalt over other polyols?

Isomalt mimics sucrose taste, resists crystallization, and cuts calories by 50%, preserving texture in sugar-free candies.

How does isomalt benefit oral-care products?

Its non-cariogenic profile and FDA-recognized anticaries claims allow formulators to market enamel-friendly mouthwashes and toothpaste.

Page last updated on: