Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.34 Billion |

| Market Size (2026) | USD 5.61 Billion |

| Market Size (2031) | USD 7.19 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Malt Ingredient Market Analysis by Mordor Intelligence

Asia-Pacific malt ingredients market size in 2026 is estimated at USD 5.61 billion, growing from 2025 value of USD 5.34 billion with 2031 projections showing USD 7.19 billion, growing at 5.08% CAGR over 2026-2031. The upward curve reflects robust premiumization across alcoholic and non-alcoholic beverages, steady functional food uptake, and wider urban middle-class adoption. Craft brewers, large distillers, and food processors increasingly specify specialty malts, pressuring suppliers to scale differentiated portfolios while embracing water- and energy-efficient technologies. Volatile grain prices have shifted procurement toward multi-grain strategies, yet rice, sorghum, and lentil malting remain early-stage niches. Region-wide regulatory convergence, notably clearer labeling and halal requirements, raises compliance costs but strengthen consumer trust in supply chains.

Key Report Takeaways

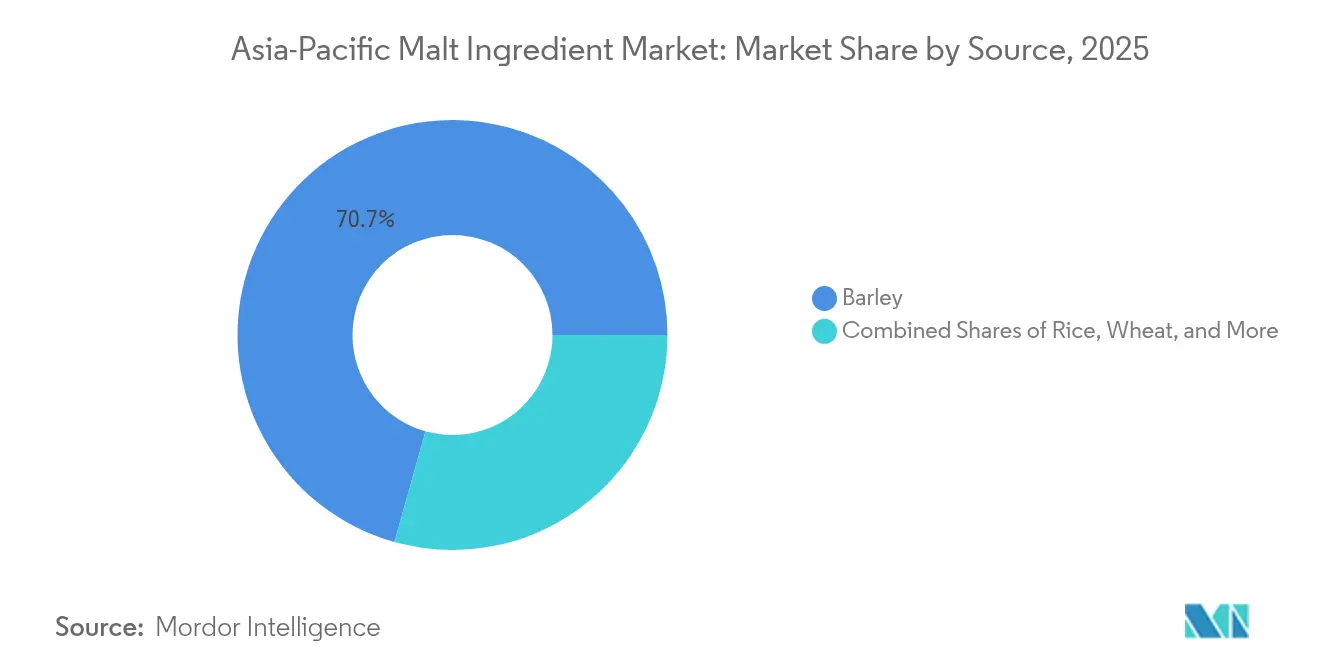

- By source, barley led with 70.65% of the Asia-Pacific malt ingredients market share in 2025, whereas rice is set to register a 6.12% CAGR through 2031.

- By form, liquid extract held 64.72% share of the Asia-Pacific malt ingredients market size in 2025; malt flour is projected to climb at 6.66% CAGR to 2031.

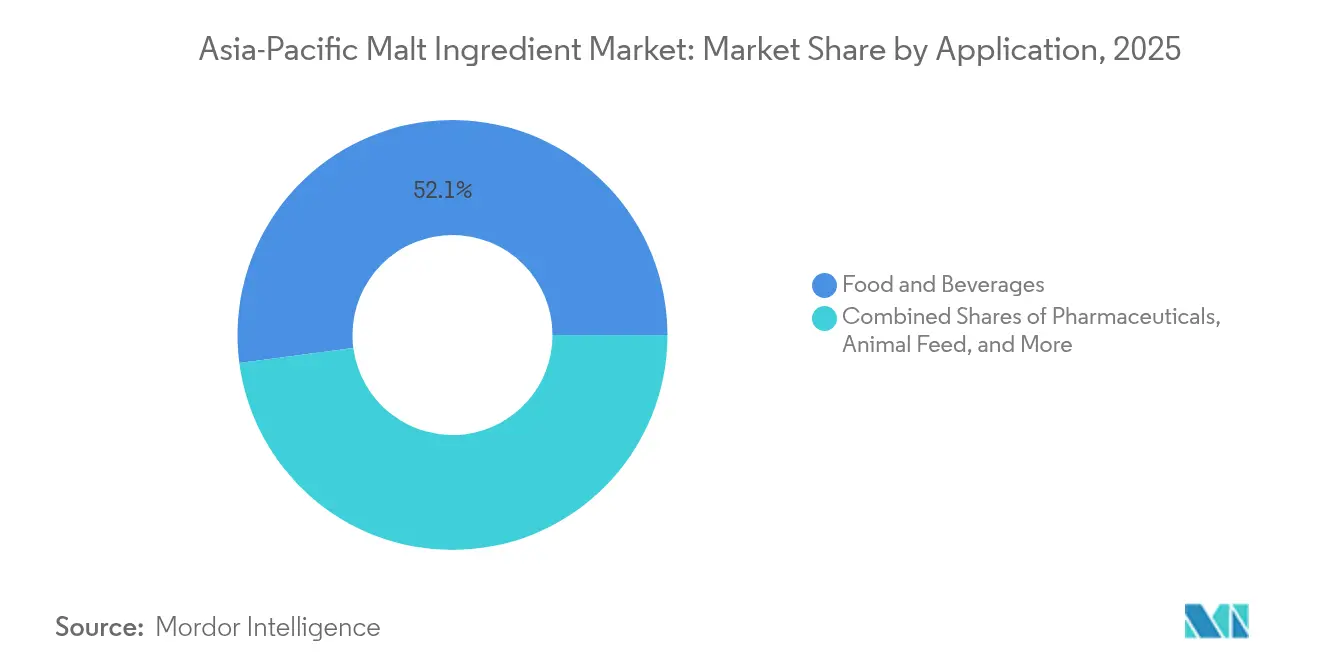

- By application, food and beverages accounted for 52.08% of the Asia-Pacific malt ingredients market size in 2025, and pharmaceuticals are advancing at a 6.23% CAGR through 2031.

- By geography, China contributed 45.21% revenue share in 2025, while Japan is on track for a 6.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Malt Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for malt in the booming craft brewing industry | +1.2% | Japan, Australia, Thailand, South Korea | Medium term (2-4 years) |

| Growing usage of malt in bakery, confectionery, and processed foods | +0.8% | China, India, Indonesia, Philippines | Long term (≥ 4 years) |

| Increased use of malt extracts in nutritional and functional foods | +0.9% | Japan, Australia, South Korea, Singapore | Medium term (2-4 years) |

| Growing Adoption of Malt Ingredients | +0.7% | APAC core, spill-over to emerging markets | Long term (≥ 4 years) |

| Development of tailored malt products | +0.6% | Japan, Australia, China urban centers | Medium term (2-4 years) |

| Rising Demand for Malt Ingredients in Animal Feed | +0.5% | China, Indonesia, Vietnam, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Malt in the Booming Craft Brewing Industry

The craft brewing boom across the Asia-Pacific region is transforming malt demand, expanding its applications beyond traditional brewing. In 2023, Japan's craft beer market displayed notable growth, with tax-exempt shipments increasing by 1.8%, sales rising by 7.2%, and the market share reaching 1.72%. In Thailand, the Community Liquor Bill has removed minimum production requirements for microbreweries, fostering local craft beer production and driving demand for specialized malts. At the same time, major Japanese breweries, including Asahi, Kirin, and Sapporo, are focusing on international markets and diversifying their product portfolios to capitalize on premiumization opportunities. The growing craft brewing sector is fueling demand for specialty malts with unique flavor profiles, encouraging advancements in malting techniques and the use of alternative grains. In Karnataka, regulatory changes have reduced the minimum space requirement for microbreweries from 10,000 to 6,500 square feet, highlighting a policy environment conducive to craft brewing growth.

Growing Usage of Malt in Bakery, Confectionery, and Processed Foods

Malt extract, traditionally associated with brewing, has carved out essential roles in baking, confectionery, and breakfast cereals. It not only enhances flavor complexity and texture but also extends shelf life. Beyond its flavoring prowess, malt extract boosts dough rise, aids in crust development, and imparts natural sweetness, all while upholding a clean label appeal. The Asia-Pacific region, particularly Indonesia, is witnessing a surge in demand for premium processed foods with malt ingredients, driven by its burgeoning middle class, set to hit 135 million by 2030, as highlighted by the Food Export Organization[1]Food Export Organization, "Country Market Profile: Indonesia", www.foodexport.org. Food manufacturers are tapping into malt extract's 6% protein content and rich vitamin profile, bolstering their nutritional positioning and elevating sensory experiences. Once viewed primarily as a health component, malt extract is now pivoting towards functional applications, acting as a natural enzyme source for yeast activation and flavor enhancement. With Indonesia's food processing industry importing 65% of its raw materials, there's a golden opportunity for malt ingredient suppliers, especially in the bakery and confectionery sectors.

Increased Use of Malt Extracts in Nutritional and Functional Foods

Health-conscious consumers in Asia-Pacific are increasingly opting for meal replacements and health-focused products, boosting the use of malt extract. With its fermentable sugars and robust nutritional profile, malt extract is becoming a key ingredient in multigrain beverages that combine diverse food sources to enhance nutritional value. Asahi Group's expansion into health and wellness, marked by the launch of 'Like Milk' – a dairy alternative made from yeast extract powder – highlights the industry's focus on functional ingredient innovation. Likewise, Kirin's partnership with Blackmores to roll out LC-Plasma powder in Taiwan demonstrates the integration of brewing expertise with nutraceuticals to meet the rising demand for gut health products. The growing trend of veganism and dietary restrictions is creating opportunities for malt-based products that address specific nutritional needs while ensuring taste and functional performance.

Development of Tailored Malt Products

Innovators in alternative grain malting are developing distinctive products that meet specific brewing needs and dietary requirements while lowering production costs. Research underscores the potential of green lentil malt for producing gluten-free beers. Although challenges exist in achieving complete saccharification during mashing, this creates opportunities for new beer styles targeting consumers with gluten sensitivities. Rice malt, despite being approximately 20% more expensive than barley malt, delivers higher yields and superior malting qualities, making it a sustainable option for breweries in regions reliant on barley imports. Malting legume seeds, such as chickpeas, lentils, peas, and vetch, increases phenolic compounds and antioxidant activity, though external enzymes are required to enhance their technological properties. Over the past 25 years, innovations like the Optisteep system have reduced water consumption by 40% and cut kilning energy usage by 20-35%, reflecting the industry's commitment to efficiency, as reported by the Journal of the Institute of Brewing[2]Journal of the Institute of Brewing, “Malting – a history of innovation and the quest for efficiency,” www.jib.org. To strengthen innovation in tailored malt product development, Bühler Group has acquired Esau & Hueber, enhancing capabilities in hygienic processes and fermentation technology.

Restraints Impact Analysis*

| Restraints | )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating barley and wheat prices | -0.9% | Global, particularly China and Australia | Short term (≤ 2 years) |

| Competition from substitute ingredients | -0.6% | APAC core markets, urban centers | Medium term (2-4 years) |

| Stringent food safety, quality control, and labeling regulations | -0.4% | China, Japan, Australia, New Zealand | Long term (≥ 4 years) |

| Seasonality of raw material supplies | -0.3% | Agricultural regions across APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fluctuating Barley and Wheat Prices

In the Asia-Pacific region, malt producers grapple with significant margin pressures due to commodity price volatility, which also shapes their sourcing strategies and production planning. As reported by India's Department of Economic Affairs[3]Department of Economic Affairs (India), "Procurement price of barley across India", www.dea.gov.in, global wholesale prices for barley malt in India rose from USD 19.91 to USD 21.23 per quintal. In April 2025, China's grain import dynamics showcased notable fluctuations: corn imports fell to 183,000 metric tons, and wheat imports stood at 740,000 metric tons, both figures markedly below the previous year's levels, as highlighted by Dimsums. Anheuser-Busch's 2024 negotiations with farmers, marked by multiple contract changes, underscore the prevailing demand uncertainty. Initial contract prices for malting barley were set at approximately USD 6.25 per bushel, a dip from prior years, according to Agweek. Additionally, the surplus barley from earlier harvests is casting a shadow on 2024 contracts, compelling farmers to rethink their crop selections and possibly curtailing their malting barley production capacity.

Stringent Food Safety, Quality Control, and Labeling Regulations

Regulatory complexities across Asia-Pacific markets place significant compliance burdens on smaller producers, driving them toward consolidation with larger, better-resourced companies. China's proposed pre-packaged labeling standards require clearer ingredient and origin disclosures. While this initiative enhances market transparency, it is likely to increase operational costs for malt ingredient suppliers. In Malaysia, public consultations on amendments to the 1985 Food Regulations began in February 2025, reflecting a regulatory landscape in constant evolution that necessitates ongoing compliance monitoring. Indonesia's mandatory halal certification, effective October 2024, introduces additional compliance costs and may exclude non-certified suppliers from the market serving the world's largest Muslim population. The March 2025 update to the Australia New Zealand Food Standards Code highlights the dynamic nature of regulatory frameworks, requiring continuous adaptation. Vietnam's Decree 8/2010/ND-CP governs feed production and imports, promoting local production while enforcing stringent quality controls, which impact malt ingredient suppliers targeting animal feed applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Barley Dominance Faces Rice Innovation

Barley generated 70.65% of 2025 revenue, yet rice is forecast to outpace all other sources at a 6.12% CAGR through 2031. The Asia-Pacific malt ingredients market size for rice-based malts is projected to expand as breweries look for locally abundant, climate-resilient grains. University of Arkansas research indicates rice malt slashes beer production costs by up to 12%, helping margin-constrained craft brewers compete [PHYS.ORG]. Wheat remains a steady second choice, while sorghum and rye cater to niche brews. Rice’s gluten-free attribute also feeds rising better-for-you beer categories, which command premium shelf pricing in markets such as Australia and Singapore.

Growth in rice malt aligns with sustainability agendas. Rice requires less irrigation than barley under tropical farming systems, reducing the embodied water footprint per ton of malt. Pilot malt houses in Thailand report up to 15% energy savings during drying because of rice’s lower moisture content at harvest. Barley nonetheless retains processing efficiency advantages, with higher enzyme potential that supports shorter mash cycles. Continuous process improvements, including staged germination control, allow maltsters to extract more fermentable sugars from non-barley grains, narrowing quality gaps and encouraging brand experimentation.

By Form: Liquid Extract Leadership Amid Flour Innovation

In 2025, liquid extract commands a dominant 64.72% market share, thanks to its established ties in the brewing industry and efficient processing methods. Meanwhile, malt flour is on a growth spree, boasting a 6.66% CAGR, driven by its rising use in functional foods and baking. Dry malt extract holds steady, catering to home brewers and specialty markets, capitalizing on its longer shelf life and storage ease. The segmentation by form mirrors industry-wide shifts towards convenience and functionality. Liquid extracts cater to the immediate needs of large-scale brewers, while flour forms offer precise dosing benefits in food manufacturing.

Malt flour's rapid ascent is attributed to its adaptability in bakeries, confectioneries, and breakfast cereals. It not only elevates flavor profiles but also aids in dough development due to its natural enzyme activity. With a protein content of 6% and a robust vitamin profile, malt flour champions the clean label movement. Beyond its flavor and functional benefits, it also extends shelf life and enhances texture. While liquid extracts continue to lead in brewing, bolstered by strong supply chain ties and processing efficiencies, they grapple with sustainability pressures. These initiatives advocate for reduced water usage and heightened energy efficiency in malting operations.

By Application: Food and Beverages Lead Pharmaceutical Growth

In 2025, food and beverage applications hold a leading 52.08% market share, covering alcoholic beverages, functional foods, and bakery products. At the same time, the pharmaceutical sector emerges as the fastest-growing segment, with a projected 6.23% CAGR through 2031. Malt extract's natural enzyme activity and high nutritional value enhance its application in dietary supplements and functional medicine formulations. Cosmetics and personal care sectors, though niche, utilize malt's antioxidant properties and natural origins to develop premium product formulations. The animal feed sector experiences consistent growth, driven by the expanding livestock industry and a growing focus on feed quality and nutritional optimization.

Research highlighting malt extract's functional benefits in health-oriented formulations drives its growth in pharmaceuticals. Kirin Holdings' introduction of LC-Plasma powder in Taiwan demonstrates the integration of brewing expertise with nutraceuticals, targeting the gut health market with scientifically supported ingredients. Asahi's expansion into health and wellness, marked by the development of proprietary postbiotic Lactobacillus gasseri CP2305, reflects the commitment of major beverage companies to innovate with functional ingredients. In aquaculture, studies emphasize barley malt's role in improving fish quality, enhancing texture, and optimizing n-6 polyunsaturated fatty acids, all while maintaining cost efficiency.

Geography Analysis

China delivered 45.21% of regional revenue in 2025, reflecting its massive beverage base and maturing food-processing sector. Premium beer and whisky launches elevate malt inclusion rates per hectoliter, offsetting declining mainstream beer volume. China’s proposed labeling reforms and erratic grain import patterns prompt brewers to lock in domestic malt contracts to secure supply continuity. Large-scale distillery investments such as Pernod Ricard’s new 13 million-liter malt facility in Nagpur underscore confidence in long-term Asian demand.

Japan emerges as the fastest-growing node at a 6.31% CAGR through 2031, underpinned by craft beer resilience, expanding whisky capacity, and surging non-alcoholic malt beverage consumption. Over 100 distilleries operate nationwide, each specifying tailored roast and moisture specifications, thus enlarging the specialty-malt opportunity. Government support for regional breweries fuels experiential tourism, further amplifying malt demand.

India, Australia, Indonesia, and South Korea complete the next tier. India’s burgeoning middle class and brewer investment in micro-malt houses reduce import reliance. Australia remains a strategic barley supplier and benefits from domestic craft-brew expansion, complemented by Malteurop’s 200,000-ton capacity extension. Indonesia’s halal rule intensifies certification spend yet also drives value-added halal malt exports. South Korea focuses on functional malt drinks, leveraging its strong convenience-store network to trial product innovations quickly.

Competitive Landscape

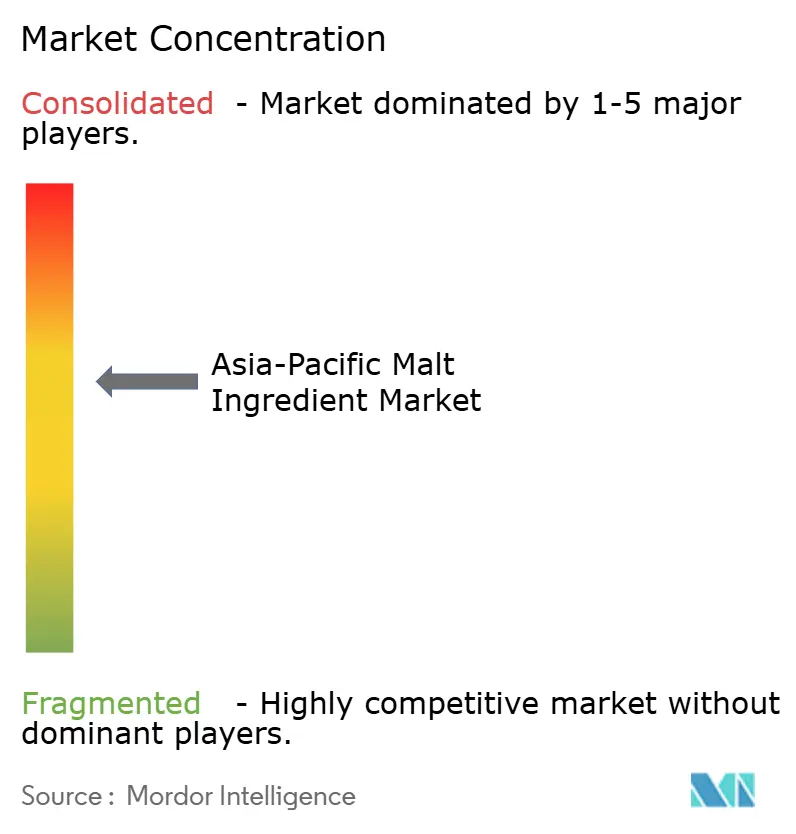

In the Asia-Pacific malt ingredients market, a moderate concentration score of 6 out of 10 highlights a tug-of-war between global consolidation and regional fragmentation. Major acquisitions, such as Soufflet Malt's takeover of United Malt Group, which now boasts a leading capacity of 3.7 million tonnes across 41 global plants, and Boortmalt's purchase of Cargill Malt, adding another 3 million tonnes to its portfolio, have significantly reshaped the industry's landscape. These consolidations not only enhance operational efficiencies but also heighten competition for regional market dominance, especially in burgeoning sectors like craft brewing and functional foods.

Companies are increasingly turning to technology as a differentiator; for instance, investments in water reduction systems, such as Optisteep, have led to a 40% cut in water usage and a 20-35% boost in kilning energy efficiency. There's a burgeoning interest in alternative grain malting and sustainability-driven applications. Companies like Malteurop and Boortmalt are innovating with rice and legume malting and championing carbon reduction efforts. Meanwhile, regional players are emerging as disruptors, harnessing local grain varieties and unique processing methods.

In Thailand, for instance, regulatory liberalization is empowering smaller producers to carve out a niche. Brewing companies are forging strategic alliances with ingredient suppliers, creating a seamless value chain. Notable examples include Kirin's health science foray, bolstered by its collaboration with Blackmores and Asahi's initiatives in developing functional ingredients. The competitive arena is increasingly skewed in favor of firms boasting strong sustainability credentials. Major players like Asahi are setting ambitious targets, aiming for 100% sustainable barley procurement by 2030, while Sapporo is charting a course towards net-zero emissions by 2050.

Asia-Pacific Malt Ingredient Industry Leaders

-

Puremalt Products Ltd.

-

Muntons PLC

-

GrainCorp Group

-

Rahr Corporation

-

Grain Processing Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Grains Australia released new malt performance summaries for the barley varieties Cyclops and Laperouse. These summaries support market development and evaluation by domestic processors, highlighting the growing acceptance and adoption of these varieties in the malting barley sector.

- May 2025: Joe White Maltings, a leading Australian malting supplier, and India’s The Catalysts Group collaborated to bring Australia's premium malting barley to India. Facilitated by the Australia-India Economic Cooperation and Trade Agreement (AIECTA), this deal provided Indian craft brewers access to high-quality Australian barley,

Asia-Pacific Malt Ingredient Market Report Scope

Malt is a grain product added to foods and beverages to add flavor and nutrients and serves as a base for fermentation. Malt is prepared from cereal grain by allowing partial germination to modify the grain's natural food substances. Although any cereal grain may be converted to malt, barley is chiefly used. Rye, wheat, rice, and corn are used much less frequently.

The Asia-Pacific malt ingredient market is segmented by source, application, and country. By source, the market is segmented into barley, wheat, and other sources of malt. Others sources include rye, rice, and sorghum. By application, the market is segmented into food, beverages, pharmaceuticals, and animal feed. Beverages are further categorized as alcoholic beverages and non-alcoholic beverages. By country, the market is segmented into China, India, Japan, Australia, and Rest of Asia-Pacific. For each segment, market sizing and forecasts have been done based on values in USD million.

Source

| Barley |

| Wheat |

| Rice |

| Rye |

| Sorghum |

Form

| Liquid Extract |

| Dry Malt Extract |

| Malt Flour |

Application

| Food and Beverages | Alcoholic and Non Alcoholic Beverages |

| Funtional Foods | |

| Bakery and Confectionery | |

| Others | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Animal Feed |

By Geography

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Rest of Asia-Pacific |

| Source | Barley | |

| Wheat | ||

| Rice | ||

| Rye | ||

| Sorghum | ||

| Form | Liquid Extract | |

| Dry Malt Extract | ||

| Malt Flour | ||

| Application | Food and Beverages | Alcoholic and Non Alcoholic Beverages |

| Funtional Foods | ||

| Bakery and Confectionery | ||

| Others | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Animal Feed | ||

| By Geography | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the Asia-Pacific malt ingredients market?

It reached USD 5.61 billion in 2026 and is forecast to hit USD 7.19 billion by 2031.

Which country leads regional demand for malt ingredients?

China held 45.21% of 2025 revenue due to its large beverage and food-processing sectors.

Which grain source is growing fastest for malt production?

Rice is projected at a 6.12% CAGR through 2031 as brewers pursue local, gluten-free options.

Why is malt flour gaining popularity in food manufacturing?

It delivers natural enzymes for dough improvement, supports clean-label claims, and is forecast at a 6.66% CAGR.

Page last updated on: