Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

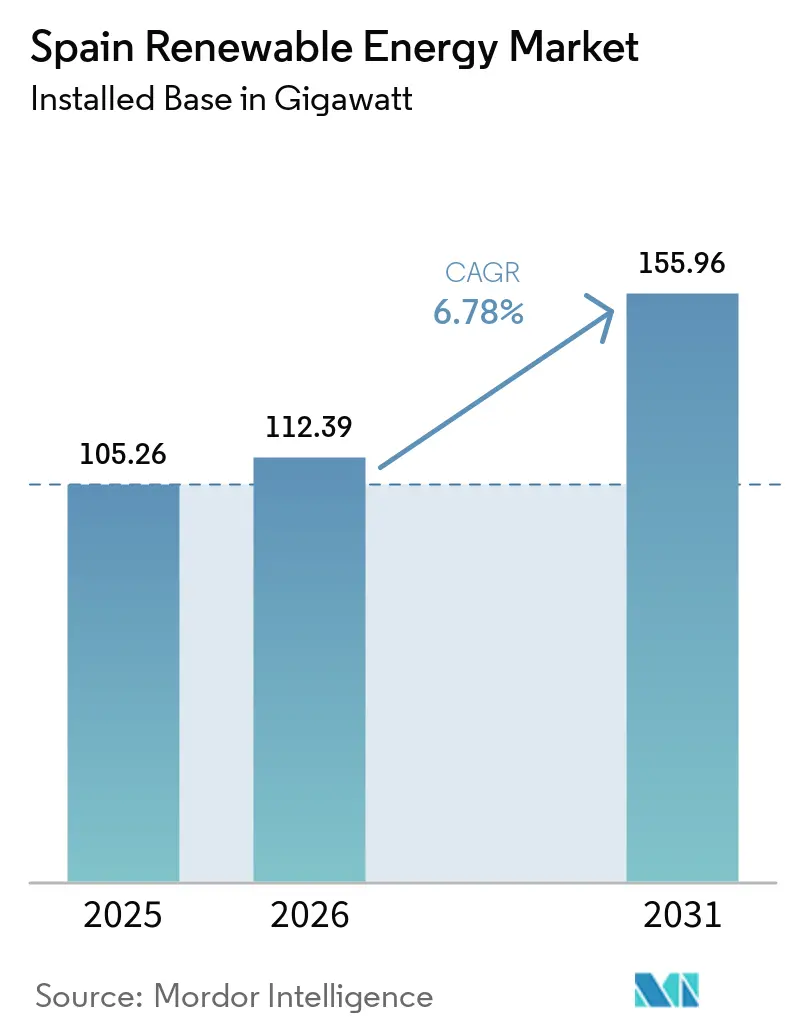

| Base Year Market Size (2025) | 105.26 gigawatt |

| Market Volume (2026) | 112.39 gigawatt |

| Market Volume (2031) | 155.96 gigawatt |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

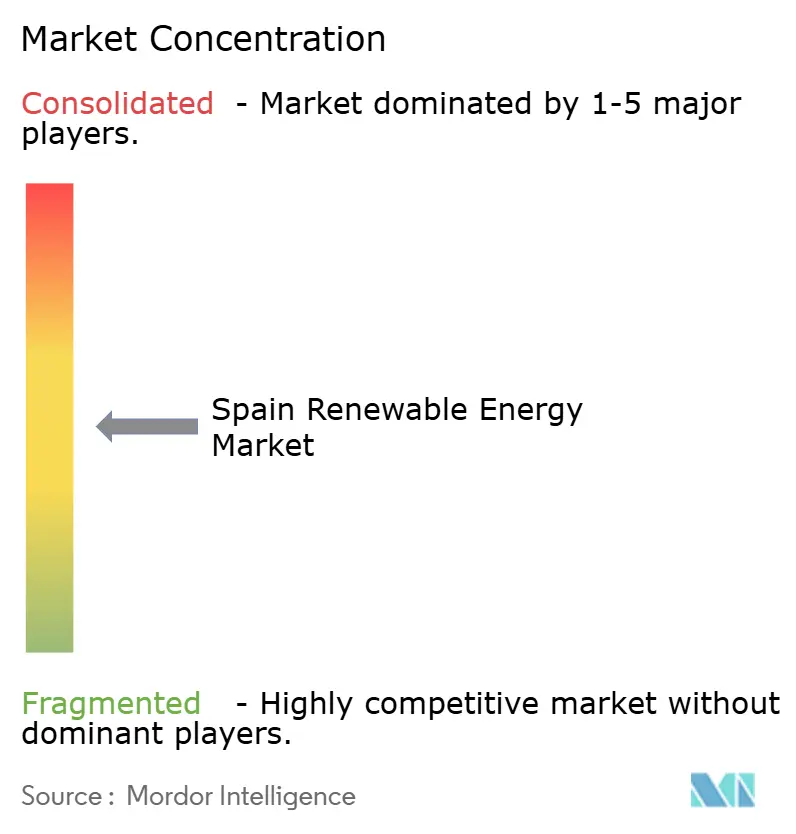

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Renewable Energy Market Analysis by Mordor Intelligence

Spain Renewable Energy Market size in 2026 is estimated at 112.39 gigawatt, growing from 2025 value of 105.26 gigawatt with 2031 projections showing 155.96 gigawatt, growing at 6.78% CAGR over 2026-2031.

Growth springs from clear decarbonization mandates, lower technology costs, and a policy mix that aligns tightly with the EU Fit-for-55 package. In 2024, renewables supplied 56.8% of Spanish electricity, a 10.3% annual jump, cementing investor confidence and drawing sizable cross-border capital. Solar PV and onshore wind dominate new builds, yet offshore wind, green hydrogen, and hybrid storage projects add momentum and diversify the technology base. Grid upgrades, interconnector expansion, and rising corporate power-purchase agreements (PPAs) further widen opportunity sets, but network congestion and slow permitting temper near-term deployment. Overall, Spain's renewable energy market continues to convert policy ambition into commercial scale at a pace that reshapes Iberian power flows.

Key Report Takeaways

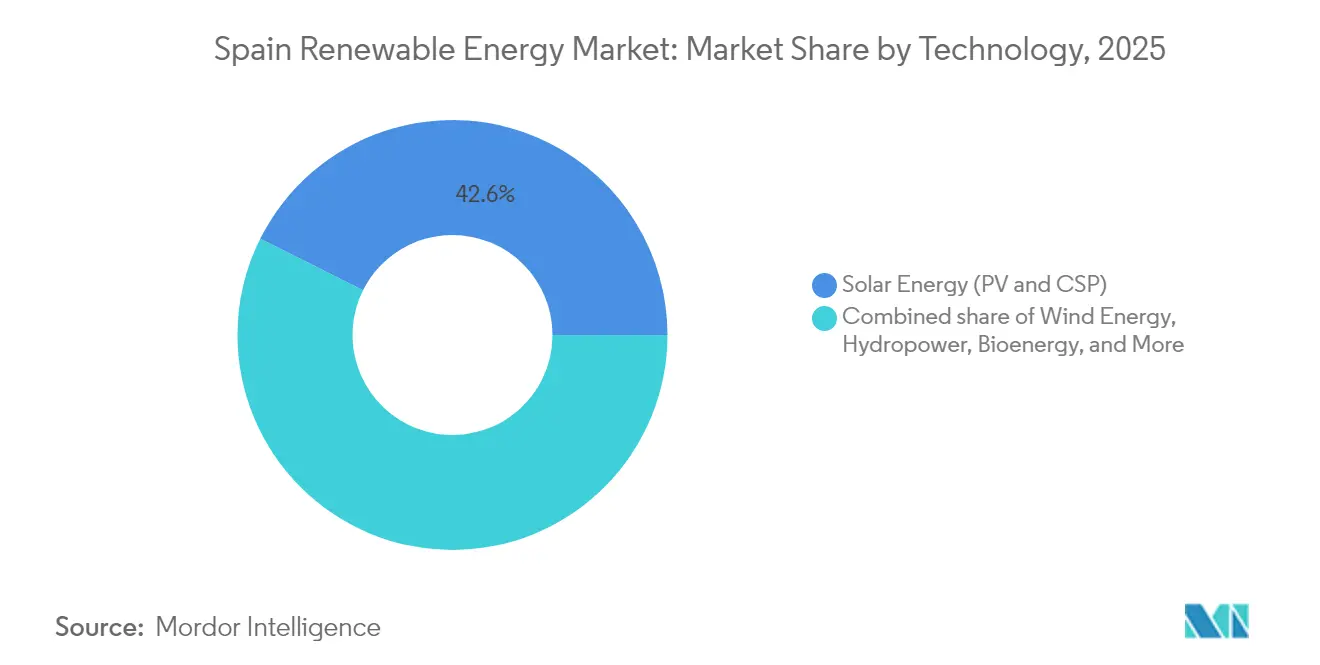

- By technology, solar energy held 42.62% of Spain's renewable energy market share in 2025 and is advancing at a 10.09% CAGR to 2031, the fastest pace across all generation types.

- By end-user, utilities accounted for 69.90% of Spain's renewable energy market size in 2025, while the commercial and industrial segment is projected to register the highest CAGR of 12.21% through 2031.

- Iberdrola, Acciona Energía, Endesa, Naturgy, and EDPR collectively controlled approximately 55% of the installed capacity in 2024, confirming a moderately concentrated landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining levelized cost of solar PV | +1.8% | Andalusia, Extremadura, Castilla-La Mancha | Short term (≤ 2 years) |

| Rapid build-out of onshore wind capacity | +1.5% | Castilla-La Mancha, Aragon, Galicia | Medium term (2-4 years) |

| EU Fit-for-55 and PNIEC 2023 targets | +1.2% | Nationwide | Long term (≥ 4 years) |

| Corporate PPAs from energy-intensive users | +1.0% | Catalonia, Basque Country, Valencia | Medium term (2-4 years) |

| Green-hydrogen export hub initiatives | +0.9% | Andalusia, Asturias, Aragon | Long term (≥ 4 years) |

| Cross-border interconnectors with neighbors | +0.7% | Bay of Biscay, Western border regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining Levelized Cost of Solar PV

Utility-scale solar delivered an average LCOE of EUR 29 per MWh in 2024, undercutting combined-cycle gas generation in every major node.(1)Fraunhofer ISE, “Levelized Cost of Electricity Update 2024,” ISE.FRAUNHOFER.DE The cost advantage reflects widespread adoption of bifacial modules and single-axis tracking that lifts yields by up to 20%, as well as aggressive EPC pricing from new Chinese entrants. Collective self-consumption rules have translated the same economics into urban rooftops, where installations expanded by 30% during 2024. Lower wholesale prices, expected from accelerated solar additions, threaten thermal margins and hasten coal retirements; however, anti-dumping probes on Asian module imports could disrupt the downward cost curve. Even so, the investment shift toward merchant or PPA-backed projects reduces dependence on government auctions and signals rising confidence in the long-term competitiveness of solar energy.

Rapid Build-Out of Onshore Wind Capacity

The repowering of early-2000s turbines using 15 MW platforms has increased capacity factors by approximately 40%, while alleviating land-use tensions in saturated regions.(2)Vestas Wind Systems, “V236-15 MW Platform Overview,” VESTAS.COM Developers secure sub-4% debt through long-tenor PPAs with data-center and steel offtakers, transferring volumetric risk downstream. Nonetheless, limited greenfield sites and avian-protection zones push activity toward floating offshore pilots off Galicia and the Canary Islands, where 3 GW is slated for commissioning late in the decade. Streamlined environmental reviews remain essential if Spain is to achieve an average of 5 GW of net wind additions each year and stay aligned with its 2030 target of 62 GW.

EU Fit-for-55 and PNIEC 2023 Targets

Spain’s mandate to reach 81% renewable power by 2030 requires 50 GW of incremental capacity, backed by Red Eléctrica de España’s EUR 6.9 billion grid upgrade plan.(3)Red Eléctrica de España, “Electricity System Report 2025,” REE.ES Compliance reviews and potential penalties under EU law amplify execution urgency. Extended assessment timelines from 12 to 18 months, however, slowed 3.8 GW of 2024-scheduled projects, illustrating the tension between ambition and local permitting realities. Carbon-border adjustment rules, starting in 2026, may reshape supply chains in favor of domestic equipment, yet complicate sourcing for developers reliant on Asian turbines.

Corporate PPAs from Energy-Intensive Industries

Spain topped the European PPA league for a fifth year, signing 4.67 GW in 2023 at an average of EUR 38.5 per MWh, a 15% discount to the spot benchmark. Virtual structures dominate, enabling buyers in congested load pockets to hedge without a direct grid connection. A government proposal to cap tenors at 10 years stalled several gigawatt-scale deals, since project lenders typically require 15-year visibility. Some industrials have begun taking equity in generation assets to internalize margins and comply with Scope 2 targets, further blurring the distinction between end-users and producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion and curtailment risk | -0.8% | Andalusia, Extremadura, Castilla-La Mancha | Short term (≤ 2 years) |

| Lengthy environmental and permitting lead-times | -0.6% | Nationwide, acute in protected zones | Medium term (2-4 years) |

| Balancing-market revenue volatility post-2025 | -0.4% | National | Short term (≤ 2 years) |

| Battery-grade lithium supply uncertainty | -0.3% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion and Curtailment Risk

Curtailment events tripled year-over-year in 2023 and forced 1.2 GW of solar and wind capacity offline during midday peaks in 2024, erasing EUR 180 million in revenue. REE’s expansion plan encompasses 2,500 kilometers of new lines and 15 substations; however, land acquisition lags behind capacity additions, resulting in constraints through 2027. Co-located battery projects partly offset lost output; however, round-trip efficiency and cost hurdles limit their uptake. A pilot dispatch regime now prioritizes hybrid assets, signaling tougher economics ahead for standalone solar.

Lengthy Environmental and Permitting Lead-Times

Impact assessments were extended to 18 months in 2024 amid tighter rules for avian and landscape protection. A 2023 auction under-subscribed by 33% and many 2021 awards still await final clearance, fraying investor confidence. One-stop digital platforms launched in 2024 aim to streamline reviews; however, fragmented authority layers and local moratoria curtail momentum, especially for offshore wind, whose inaugural auction has been moved to 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar Dominance Reshapes Generation Mix

Spain Solar energy accounted for 42.62% of installed capacity in 2025, confirming its leadership within the Spanish renewable energy market. Utility-scale projects in Andalusia and Extremadura, where irradiance exceeds 2,000 kWh / m², underpin the segment's 10.09% CAGR outlook through 2031. The Spain renewable energy market size for solar is forecast to add roughly 35 GW by the decade's close, reflecting the lowest LCOE across competing resources. Wind follows as the second-largest pillar; onshore parks in Castilla-La Mancha and Aragon deliver capacity factors of 28-32%, while a 3 GW floating portfolio off Galicia and the Canary Islands seeks final permits. Hydropower supplies 20 GW, with 5.3 GW of pumped storage acting as a flexibility backbone, yet it is vulnerable to drought-driven inflow variability.

Cost competitiveness drives investor preference toward solar and wind, but technological diversification remains essential. CSP plants provide thermal storage and extend dispatch into evening peaks, mitigating price cannibalization. Bioenergy, geothermal, and ocean energy collectively contribute less than 2 GW, primarily due to limited feedstock availability, resource quality, and the nascent stage of technology readiness. Nevertheless, pumped storage expansions and battery hybrids signal a trend toward integrated resource portfolios that balance intermittency and bolster system reliability.

By End-User: Utilities Lead, Yet C&I Segment Accelerates

Utilities held 69.90% of Spain's renewable energy market share in 2025, a position underpinned by scale economics, investment-grade balance sheets, and access to cheap debt. The Spain renewable energy market size attributable to utilities is projected to climb from 73.57 GW in 2025 to 107.25 GW by 2031, tracking system-level additions. The commercial and industrial segment records a 12.21% CAGR, thanks to rooftop solar and on-site wind, leveraging the provisions of Royal Decree 244/2019 that shorten the payback period to 5-7 years.

Industrial offtakers secure PPAs at EUR 38-40 per MWh, well below average spot rates, locking in cost predictability. Data-center operators cluster near renewable energy hubs to integrate generation, storage, and compute load, driving investments in microgrids. Residential uptake increased by 30% in 2024, driven by tax credits and simplified net-metering, although its absolute footprint remains modest. Overall, end-user diversification suggests a gradual decentralization of Spain's renewable energy architecture, with utilities still steering bulk capacity while commercial and industrial (C&I) adopters capture incremental, high-margin niches.

Geography Analysis

Andalusia hosts approximately 15 GW of solar and 5 GW of wind, accounting for roughly 19.65% of the national renewable capacity, and is projected to grow at an annual rate of 8.12% through 2031. High irradiance, land availability, and the Andalusian Hydrogen Valley draw substantial capital but also intensify curtailment, prompting prioritized grid reinforcement. Castilla-La Mancha and Extremadura together represent 40% of the development pipeline; Extremadura’s co-located 200 MW battery project illustrates a model for mitigating intermittency while unlocking ancillary services.

Aragon’s onshore wind fleet navigates site saturation, making repowering the primary growth lever, whereas Galicia leverages superior wind speeds and port infrastructure to champion Spain’s floating-offshore aspirations. Catalonia and the Basque Country lead distributed generation, aided by regional subsidies that cover up to 35% of rooftop solar costs, and high industrial density that favors self-consumption PPAs.

The Canary Islands, aiming to achieve 70% renewable electricity by 2030, up from 18% in 2024, are piloting hybrid microgrids that combine wind, solar, and storage to displace diesel imports. Regional disparities in permitting and infrastructure create a two-speed landscape: sun-rich southern provinces attract utility-scale capital, while industrialized or island regions prioritize smaller, flexible assets that circumvent grid bottlenecks.

Competitive Landscape

The top five operators, Iberdrola, Acciona Energía, Endesa, Naturgy, and EDPR, controlled about 55% of the Spanish renewable energy market share in 2024, illustrating moderate concentration.(4)Iberdrola, “Strategic Plan Spain 2024-2026,” IBERDROLA.COM Incumbents exploit vertical integration across generation, storage, and retail, and maintain sub-3.5% financing that underwrites large, multi-technology portfolios. Mid-tier challengers such as Grenergy, Capital Energy, and Solaria grow through agile greenfield development and corporate PPAs that bypass utility intermediation, narrowing incumbent dominance.

Strategically, incumbents expand into storage and hydrogen to capture emerging value pools. Iberdrola has earmarked EUR 5 billion for 2.5 GW of new capacity, plus 500 MW of storage, between 2024 and 2026. Grenergy partnered with TotalEnergies to co-develop 1 GW of solar and 200 MW of battery storage, exemplifying a partnership-driven approach to scale. Offshore floating wind remains relatively uncontested, offering whitespace for new consortia.

Technology differentiation intensifies as Siemens Gamesa pilots 14 MW offshore turbines that yield 40% higher capacity factors, and Acciona tests iron-air batteries targeting long-duration storage. Financial sponsors acquire de-risked assets; Blackstone and Macquarie acquired 2.3 GW of operating solar in 2024, signaling a shift toward infrastructure fund ownership. ESG disclosure requirements under the EU taxonomy favor listed players, potentially widening the cost-of-capital gap versus private developers.

Spain Renewable Energy Industry Leaders

Iberdrola SA

Siemens Gamesa Renewable Energy SA

Acciona SA

Red Electrica Corporacion SA

Cobra Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Spain awards EUR 1.223 billion to seven hydrogen-valley projects, adding 2,292.8 MW of electrolysis capacity and mobilizing EUR 5.821 billion of investment.

- May 2025: PLOCAN begins construction of the first offshore renewable-hydrogen plant in the Canary Islands, under the H2VERDE project, with an annual output of 15,000 kg.

- April 2025: Enagás launches public consultation for a 2,600-km hydrogen pipeline network spanning 13 regions, backed by €75 million in EU funding.

- March 2025: Masdar expands its Endesa partnership through a EUR 368 million asset acquisition, while Amazon finalizes 870 MW of PPAs, underscoring the strong corporate commitment.

Spain Renewable Energy Market Report Scope

The Spain renewable energy market report includes:

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How large is the Spain renewable energy market in 2026 and where is it headed by 2031?

Installed capacity reached 112.39 GW in 2026 and is projected to climb to 155.96 GW by 2031, equal to a 6.78% CAGR.

Which technology is growing the fastest in Spain's clean-power mix?

Solar photovoltaics lead, expanding at a 10.09% CAGR and already holding 42.62% of 2025 installed capacity.

What role do corporate PPAs play in new project financing?

Spain signed 4.67 GW of PPAs in 2023, allowing developers to secure sub-4% debt and hedge revenue under long agreements.

How will nodal pricing affect merchant renewable projects after 2025?

Locational marginal pricing will expose assets in congested nodes to discounts up to 30%, making long-term PPAs or CfDs vital for bankability.

Where are the main geographic hotspots for new capacity?

Andalusia, Extremadura, and Castilla-La Mancha dominate utility-scale solar, while Galicia is the focal point for floating offshore wind.

Who are the market leaders and how concentrated is the landscape?

Iberdrola, Acciona Energía, Endesa, Naturgy, and EDPR hold about 55% of capacity, resulting in a moderate concentration score of 6.

Page last updated on: