Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

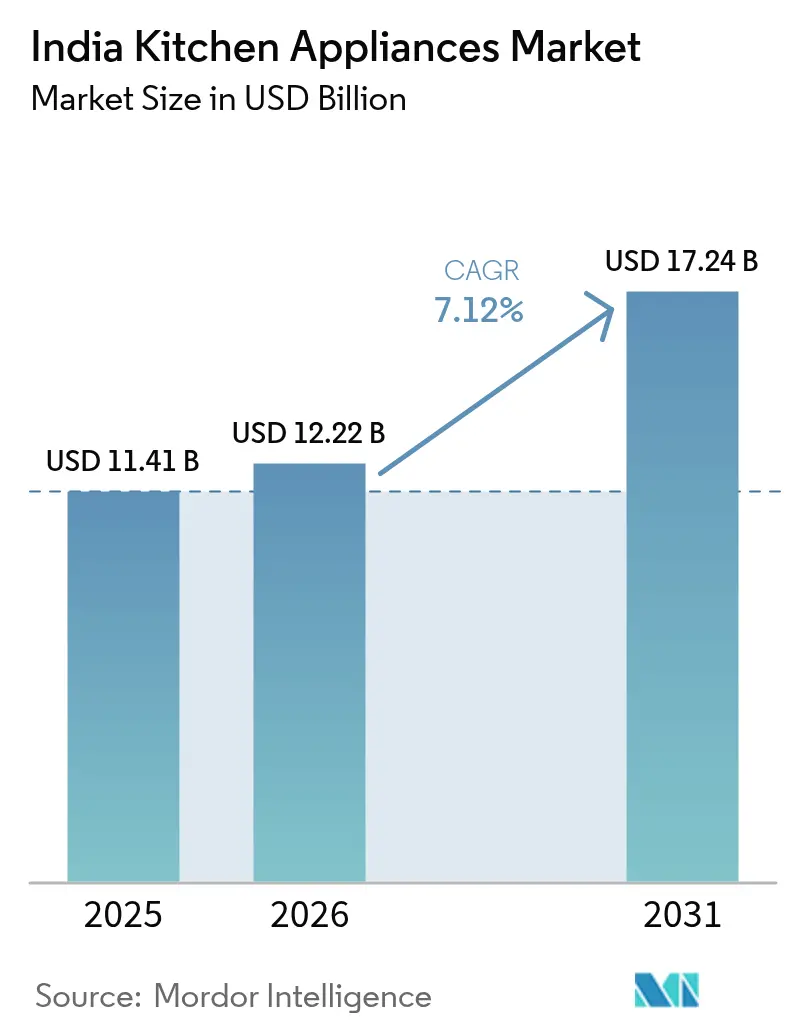

| Base Year Market Size (2025) | USD 11.41 Billion |

| Market Size (2026) | USD 12.22 Billion |

| Market Size (2031) | USD 17.24 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Kitchen Appliances Market Analysis by Mordor Intelligence

The India kitchen appliances market size was valued at USD 11.41 billion in 2025 and estimated to grow from USD 12.22 billion in 2026 to reach USD 17.24 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Rising disposable incomes, rapid urbanization, and household preferences for convenience-oriented cooking solutions underpin this growth, while government Production Linked Incentive allocations now totaling INR 444.54 crore stimulate local manufacturing of refrigerators, cooktops, and other white goods. Organized retail penetration has reached 54% of all home-appliance sales and is expected to exceed 70% by 2027, giving branded suppliers wider showroom footprints and financing options for consumers. Online marketplaces accelerate adoption by offering festival-driven flash deals, zero-cost EMIs, and doorstep installation, which together lifted digital channel volumes for large and small appliances by 25% during 2024[1]Source: India Infoline, “Organized Retail Share in Consumer Durables,” indiainfoline.com. At the same time, mandatory Bureau of Energy Efficiency star labeling continues to shorten replacement cycles by rewarding energy-savings awareness and spurring premiumization across all price tiers[2]Source: Bureau of Energy Efficiency, “Standards & Labeling Program,” beeindia.gov.in..

Key Report Takeaways

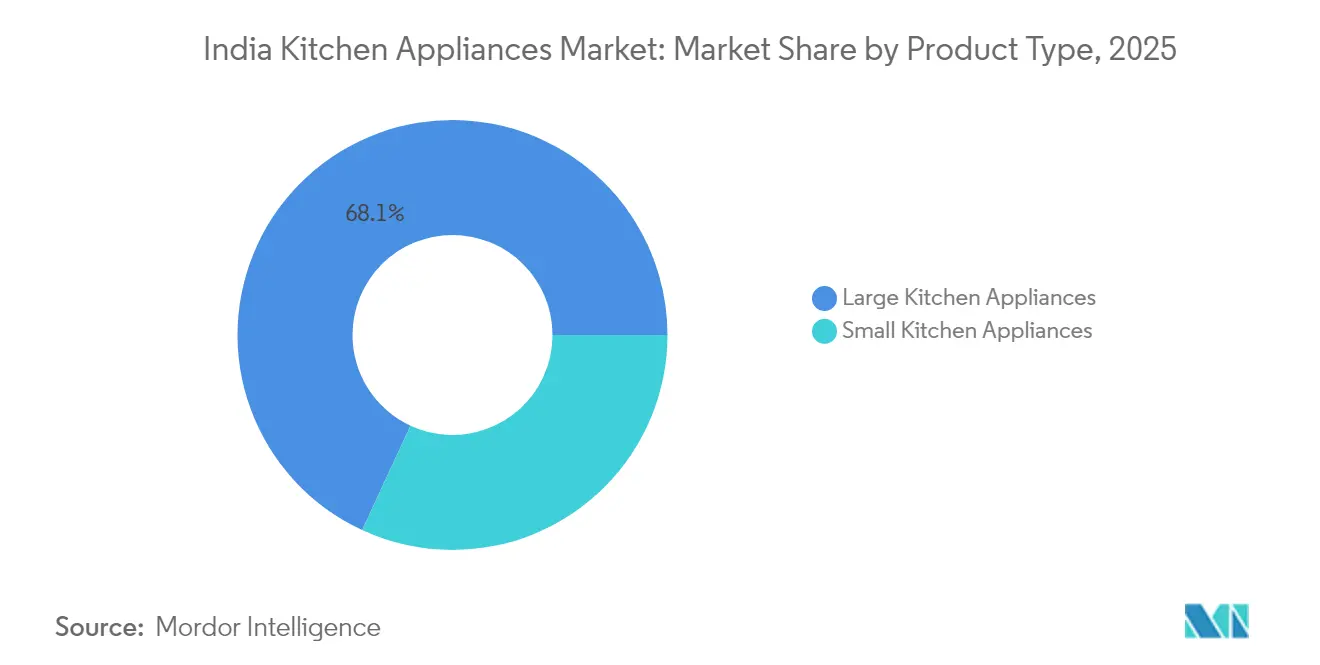

- By product type, large appliances led with 68.10% of the India kitchen appliances market share in 2025, while small appliances show the highest projected CAGR at 8.88% through 2031.

- By end user, residential applications accounted for 70.05% of the India kitchen appliances market size in 2025 and the commercial segment is poised to expand at a 7.62% CAGR between 2026-2031.

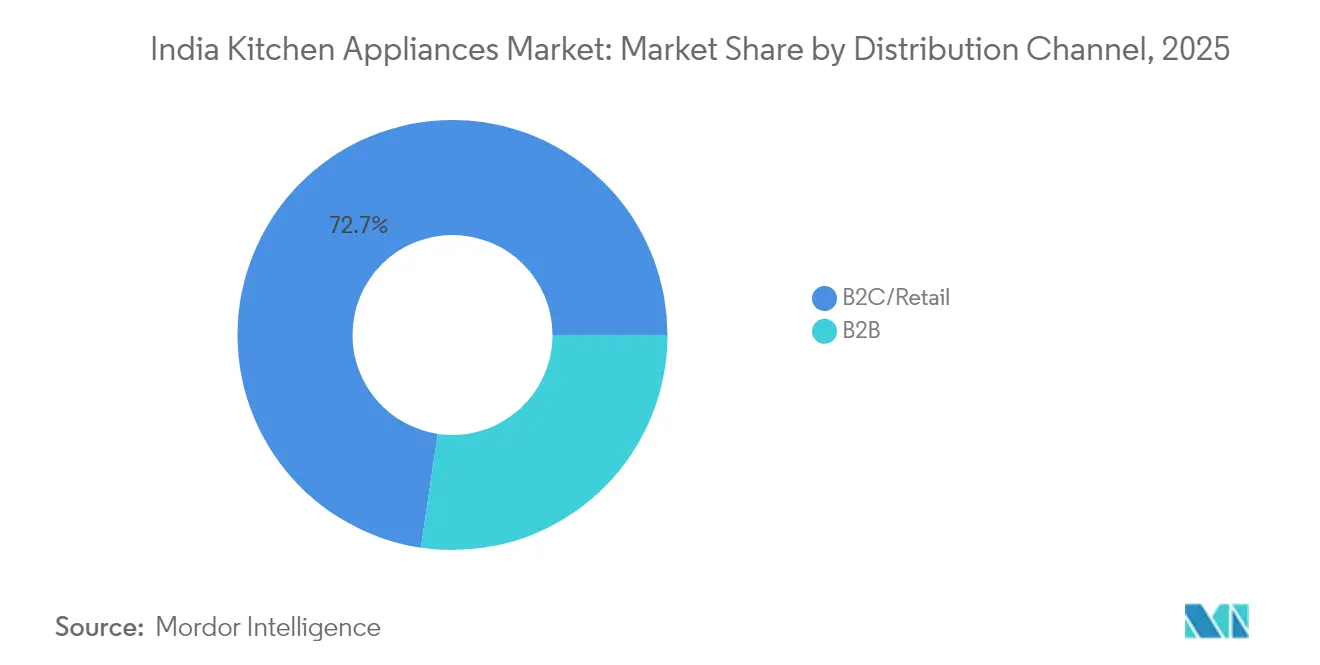

- By distribution channel, B2C/retail captured 72.65% revenue share in 2025; within this, online retail is forecast to advance at 9.92% CAGR over 2026-2031.

- By geography, South India held 33.95% of 2025 revenue, whereas East & North-East India are on track for the fastest 7.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urban middle-class disposable income | +1.8% | National, with concentration in Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Growth of e-commerce & D2C appliance brands | +1.2% | Urban India, expanding to semi-urban markets | Short term (≤ 2 years) |

| Government push for domestic manufacturing (PLI, Make in India) | +1.5% | National, with manufacturing hubs in Gujarat, Tamil Nadu, Haryana | Long term (≥ 4 years) |

| Energy-efficiency regulations driving replacements | +0.9% | National, with higher impact in metro cities | Medium term (2-4 years) |

| Surge in health-centric cooking trends | +1.1% | Urban India, with spillover to Tier-2 cities | Short term (≤ 2 years) |

| Appliance-as-a-service & rental models emerging | +0.7% | Metro cities and young professional segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Middle-Class Disposable Income

Urban household spending on consumer durables climbed 18% year-on-year during the March 2024 quarter, allowing families to move from single-function gadgets to multi-tasking smart ranges[3]Source: The Hindu Business Line, “Urban Households Outspend Rural by 60%,” thehindubusinessline.com. Average urban expenditure reached INR 49,418 per month, 1.6 times rural levels, boosting demand for premium refrigerators, dishwashers, and built-in ovens. Southern states recorded a 35% jump in grocery and home-goods outlays over two years, reinforcing the region’s appetite for energy-efficient kitchen solutions. Manufacturers now position inverter compressors and AI-assisted menus as core selling points that fit status aspirations and utility-bill savings. Organized retail expansion further enhances access to branded appliances as mall developers anchor new properties around electronics megastores.

Growth of E-commerce & D2C Appliance Brands

Digital marketplaces contributed between 9-30% of sales across major appliance categories in 2024 and logged 25% growth in Amazon’s home-and-kitchen vertical in Odisha alone. Lower entry barriers let challenger brands launch directly to consumers with online-only SKUs that undercut incumbents on price while offering app connectivity. Wonderchef’s plan to double revenue within five years rests on search-optimized listings, influencer-led recipe videos, and same-day shipping across 100 cities. Flash-sale festivals during Diwali and Republic-Day weeks routinely drive triple-digit growth for air fryers, mixer-grinders, and countertop ovens. E-commerce reliability and doorstep installation have gradually shifted even high-ticket refrigerator purchases online, signaling a permanent omnichannel rebalancing.

Government Push for Domestic Manufacturing

The Production Linked Incentive scheme raised white-goods funding to INR 444.54 crore and has cleared 84 applicant companies for investments worth INR 10,478 crore, thereby cutting import dependence for compressors, motors, and PCB assemblies. Global majors such as Haier and Godrej have earmarked USD 48.14 million and USD 25.11 million respectively for plant upgrades that localize output of direct-cool refrigerators and AI-enabled washers. Philips recently inaugurated an Ahmedabad line capable of 1.5 million air fryers annually, demonstrating how fiscal incentives improve economies of scale in specialized appliances. The policy mix extends duty rebates on key components, helping India kitchen appliance makers price competitively against Southeast-Asian imports. Technology transfer clauses embedded in PLI contracts accelerate domestic R&D for motor efficiency and IoT firmware.

Energy-Efficiency Regulations Driving Replacements

The Bureau of Energy Efficiency mandates star labels on 11 kitchen-related products, compelling shoppers to retire high-consumption models once electricity bills outpace financing costs of replacements. Even a basic one-star ceiling fan saves INR 850 annually, illustrating tangible paybacks that translate readily to refrigerators and induction cooktops. Samsung’s 2025 lineup touts AI cycle optimization that cuts power use by up to 70%, exemplifying how regulation nudges design toward inverter compressors and low-standby circuitry[4]Source: Samsung, “Bespoke AI Appliances Enter India,” samsung.com.. Rising tariffs in metro regions strengthen the case for five-star refrigerators despite their higher sticker prices. Utility companies are piloting rebate schemes for star-rated purchases, layering additional incentives on an already compelling value proposition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material & component costs | -1.3% | National, with higher impact on manufacturing hubs | Short term (≤ 2 years) |

| Wide regional price-sensitivity limiting premiums | -0.8% | Rural India and Tier-3 cities primarily | Medium term (2-4 years) |

| Slow smart-appliance uptake over data-privacy worries | -0.6% | Urban India, particularly among older demographics | Medium term (2-4 years) |

| Informal repair market prolongs product lifecycles | -0.9% | Rural and semi-urban areas, Tier-2 and Tier-3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material & Component Costs

Spot steel and aluminum prices spiked 18-22% during 2024, cutting gross margins for cooker and chimney makers by up to 250 basis points. TTK Prestige’s EBITDA margin slipped to 10.7% in Q2 FY25 despite automation investments aimed at offsetting commodity inflation. Container shortages stemming from Red Sea diversions delayed PCB shipments, forcing assemblers to carry inflated inventory that tied up working capital. Exchange-rate swings amplified exposure for firms importing compressors and semiconductors, prompting many to hedge dollar requirements or shift sourcing to Indian vendors. Local foundries are ramping induction-motor capacity, but ramp-up timelines limit short-term relief.

Wide Regional Price-Sensitivity Limiting Premiums

Rural unit volumes rose 5.8% in 2024, and average selling prices remain 23-28% lower than in metros because consumers prioritize essential features over smart functions. Manufacturers thus juggle dual roadmaps: stripped-down variants for price-conscious regions and IoT-enabled flagships for urban showrooms. This bifurcation dilutes economies of scale and complicates inventory planning across 700-plus district warehouses. Retailers in small towns hesitate to stock high-ticket models, fearing slow turnover and higher financing costs. Subsidy programs for energy-efficient units help bridge the affordability gap but have not yet reached critical mass.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Large Appliances Drive Volume, Small Appliances Accelerate Growth

Large appliances accounted for 68.10% of 2025 revenue, underscoring their anchor role in the India kitchen appliances market. Refrigerators lead the sub-segment, with AI-ready models featuring convertible freezer compartments that fit India’s penchant for bulk produce shopping. Dishwashers, once niche, are on track to cross USD 90 million by 2026 as urban households seek hygienic, labor-saving solutions [IBEF.ORG]. Built-in hobs and chimneys benefit from rapid adoption of modular kitchens in new apartment complexes, especially across Bengaluru and Pune. Government LPG subsidies also boost gas-hob replacement cycles, ensuring demand resiliency despite commodity inflation.

Small appliances exhibit a 8.88% forecast CAGR through 2031, marking them the fastest-expanding slice of the India kitchen appliances market. Air fryers dominate this surge, and Philips’ Ahmedabad plant with 1.5 million-unit capacity illustrates confidence in sustained growth. Electric kettles, toasters, and sandwich makers register holiday-season spikes, reflecting breakfast-on-the-go lifestyle shifts among millennials. Multi-cookers equipped with voice-guided recipes appeal to first-time cooks working from home, while robotic stir-fry devices introduced by Upliance.ai at INR 23,999 democratize automated cooking. Health-linked appliances such as cold-press juicers further diversify the segment, aligning with wellness priorities.

By End User: Residential Dominance with Commercial Segment Gaining Momentum

Residential buyers constituted 70.05% of 2025 shipments, validating home-cooking’s cultural centrality in shaping the India kitchen appliances market. Premium residential uptake accelerated after Samsung launched its Bespoke AI refrigerators starting at INR 36,000, bridging affordability and advanced functionality Rural households recorded faster volume growth than urban counterparts, supported by expanding electricity access and rising incomes. Energy-saving mandates incentivize households to swap legacy units for five-star-rated options, compressing payback periods to less than four years in states with higher tariffs. Voice-controlled ovens and smart hobs integrate seamlessly with broader smart-home ecosystems, driving incremental attachment sales for device makers.

Commercial kitchens are projected to grow at a 7.62% CAGR through 2031 as India’s quick-service restaurant footprint multiplies. Chain operators invest in combi-ovens, blast chillers, and high-throughput dishwashers to comply with food-safety norms and reduce labor costs. Institutional demand from corporate cafeterias, hospitals, and student hostels adds a steady replacement pipeline. International brands like Miele saw professional-grade sales rise to EUR 819 million globally in 2023, reflecting broader hospitality recovery that spills into the Indian market. Government incentives for food-processing clusters further anchor equipment demand in agro-rich states.

By Distribution Channel: Retail Channels Lead with Online Acceleration

Brick-and-mortar retail held 72.65% of 2025 sales, confirming physical inspection’s importance in the India kitchen appliances market. Big-box chains, exclusive brand outlets, and neighborhood dealers collectively drive showroom traffic via live demos, exchange offers, and zero-down-payment schemes. TTK Prestige operates 620 Prestige Xclusive stores and plans a 30% footprint expansion over four years to deepen last-mile reach. Organized retailers benefit from supply-chain financing that shortens replenishment cycles during festival rushes. In-store experiential zones showcasing connected-home ecosystems further raise average basket values.

Online retail will post a 9.92% CAGR between 2026-2031, unlocking incremental reach into Tier-2 and Tier-3 cities where premium shelf space is scarce. Amazon and Flipkart pioneered same-day delivery for select refrigerators and dishwashers, eroding a key barrier to digital conversion. D2C labels leverage social-commerce videos and live-streamed cooking tutorials to cut customer-acquisition costs. Strategic partnerships with last-mile assemblers ensure hassle-free installation, which historically favored physical stores. Hybrid “click-and-collect” models now let shoppers order online and pick up locally, marrying logistics efficiency with tactile reassurance.

Geography Analysis

South India commanded 33.95% of 2025 revenue due to higher disposable incomes, IT-sector prosperity, and early adoption of energy-efficient appliances. Tamil Nadu leads exports of processed fruits and nuts, reinforcing demand for both residential refrigerators and commercial blast freezers in food-processing hubs. Metro consumers in Bengaluru, Hyderabad, and Chennai favor AI-driven cooktops that sync with recipe apps, driving premium penetration rates above the national average. A robust manufacturing base in Chennai and Coimbatore shortens delivery times for regional dealers. Retail chains cluster large-format showrooms around tech parks, capitalizing on affluent professionals.

West India remains a major contributor with Gujarat’s Make-in-India corridors fostering OEM clusters for sheet-metal fabrication and PCB mounting. Maharashtra’s Mumbai-Pune corridor exhibits strong demand for built-in hobs and modular chimneys as apartment developers hand over ready-to-cook kitchens. The region’s extensive port infrastructure simplifies raw-material imports and finished-goods exports. Consumers across Gujarat’s tier-two towns increasingly prefer inverter refrigerators due to chronic power-quality issues that amplify operational savings. Organized retail share in the West now stands close to 60%, easing brand penetration.

East & North-East India is the fastest-growing territory, with an 7.86% forecast CAGR bolstered by rising urbanization in Kolkata, Bhubaneswar, and Guwahati. Improved highway connectivity accelerates appliance distribution into hilly terrain, and state incentives for electronics assembly nurture nascent local production. Amazon’s 25% growth in Odisha’s home-and-kitchen sales during FY24 evidences e-commerce’s catalytic role in rural outreach. Young demographics and social-media exposure cultivate aspirational purchase behavior, particularly for small appliances like air fryers and blenders. Government electrification schemes further expand addressable households, consolidating long-term upside.

Competitive Landscape

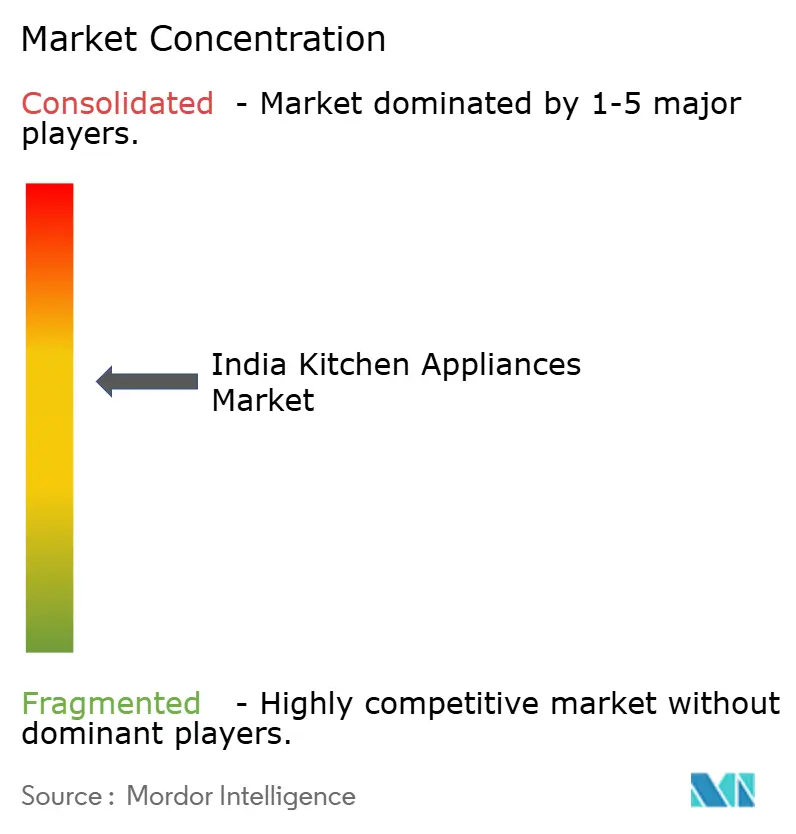

The India kitchen appliances market is moderately fragmented, with the top five companies holding major market share in 2024. Samsung, LG, and Whirlpool dominate large appliances by bundling AI diagnostics, app control, and extended warranties that reinforce brand loyalty. Domestic champion TTK Prestige targets tier-two towns through a fast-growing service-franchise network designed to double retail touchpoints by 2028. Havells entered built-in cooktops and chimneys aiming for a top-three share within three years, leveraging its electrical-appliance distribution muscle. Exclusive brand outlets serve as experiential centers where companies upsell accessory packs and AMC contracts.

Emergent disruptors capitalize on direct-to-consumer models to undercut incumbents on price while offering niche functionality. Wonderchef’s Chef Magic robotic device commands INR 49,999 and integrates 200 guided recipes, targeting tech-savvy millennials seeking hands-free cooking. Upliance.ai’s INR 23,999 stir-fry robot bundles voice control and OTA firmware updates, demonstrating rapid innovation cycles unconstrained by traditional retail margins. Subscription-based models from Rentomojo and similar platforms lock users into upgrade paths that feed future sales funnels for OEM partners. Mandatory BEE star ratings serve as both compliance hurdle and branding tool, rewarding early adopters of inverter technology and penalizing laggards.

Investment activity underscores confidence in growth prospects. Versuni, formerly Philips Domestic Appliances, selected global banks for a USD 300-350 million India IPO aimed at lifting domestic manufacturing from 70% to 90% within two years. Reliance Industries acquired Kelvinator’s India rights, signaling conglomerate interest in scaling distribution synergies across its burgeoning retail empire. Panasonic’s corporate-venture arm injected capital into Upgrid Solutions, broadening its ecosystem beyond home appliances to energy services. OEMs race to secure semiconductor allocations for smart-feature roadmaps, while commodity hedging remains a strategic imperative amid raw-material volatility. After-sales service, including on-site repair within 24 hours in metros, now represents a key differentiator as product performance converges.

India Kitchen Appliances Industry Leaders

TTK Prestige Ltd.

Philips Domestic Appliances India Ltd.

Bajaj Electricals Ltd.

Havells India Ltd.

Butterfly Gandhimathi Appliances Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Samsung debuted its 2025 Bespoke AI appliance suite in India, pricing refrigerators from INR 36,000 and introducing a combined wash-and-dry laundry combo.

- June 2025: Godrej Interio unveiled plans to open 104 new stores in FY25 to scale its premium kitchen and home-solutions portfolio.

- January 2025: Godrej Interio unveiled plans to open 104 new stores in FY25 to scale its premium kitchen and home-solutions portfolio.

- August 2024: Philips commissioned an Ahmedabad plant with 1.5 million annual air-fryer capacity under the Make-in-India initiative.

India Kitchen Appliances Market Report Scope

A complete background analysis of the India Kitchen Appliances Industry, which includes an assessment of the national accounts, economy, and emerging market trends by segments, significant changes in the market dynamics, and market overview is covered in the report.

By Product

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers and Blenders | |

| Grills and Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Countertop Ovens | |

| Other Small Kitchen Appliances |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (directly from the manufacturers) |

By Geography

| North India |

| South India |

| West India |

| East & North-East India |

| By Product | Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | ||

| Range Hoods | ||

| Cooktops | ||

| Ovens | ||

| Other Large Kitchen Appliances | ||

| Small Kitchen Appliances | Food Processors | |

| Juicers and Blenders | ||

| Grills and Roasters | ||

| Air Fryers | ||

| Coffee Makers | ||

| Electric Cookers | ||

| Toasters | ||

| Electric Kettles | ||

| Countertop Ovens | ||

| Other Small Kitchen Appliances | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (directly from the manufacturers) | ||

| By Geography | North India | |

| South India | ||

| West India | ||

| East & North-East India | ||

Key Questions Answered in the Report

How large is the India kitchen appliances market in 2026?

The India kitchen appliances market size is valued at USD 12.22 billion in 2026.

What is the expected CAGR for Indian kitchen-appliance sales to 2031?

Revenue is projected to grow at a 7.12% CAGR, reaching USD 17.24 billion by 2031.

Which product category is expanding the fastest?

Small appliances such as air fryers and multi-cookers are forecast to advance at a 8.88% CAGR.

Which region will post the strongest growth through 2031?

East & North-East India shows the highest expected CAGR at 7.86% to rising urbanization and e-commerce penetration.

How important is online retail to future sales?

Online channels are projected to register a 9.92% CAGR, driven by festival promotions, doorstep installation, and growing trust in high-value e-commerce purchases.

Page last updated on: