Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

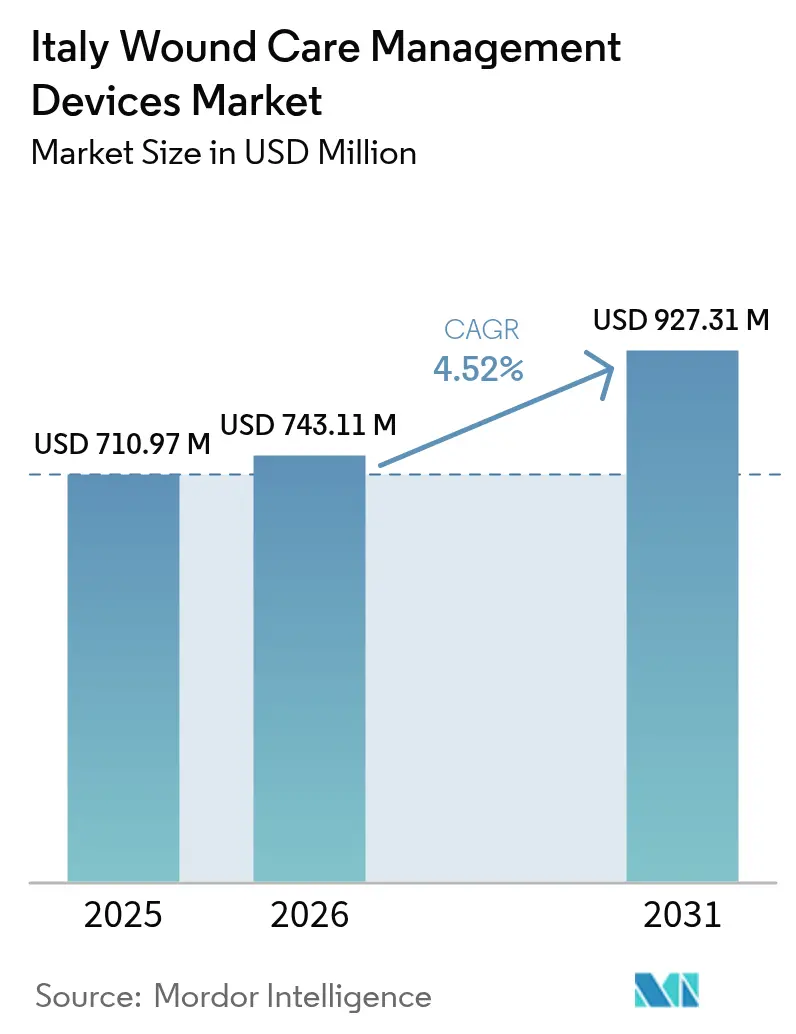

| Base Year Market Size (2025) | USD 710.97 Million |

| Market Size (2026) | USD 743.11 Million |

| Market Size (2031) | USD 927.31 Million |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

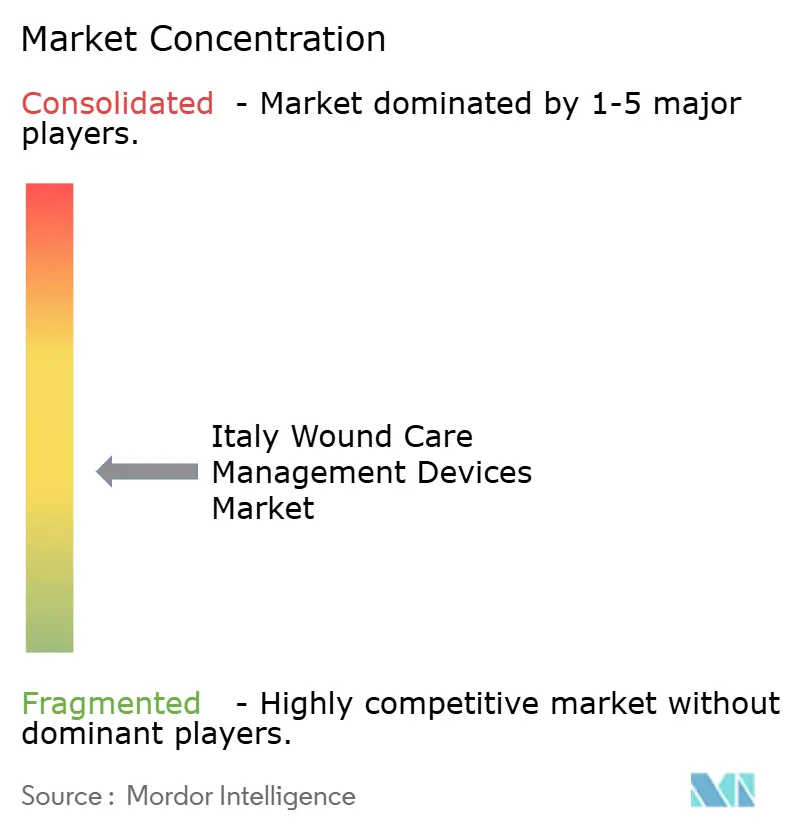

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Wound Care Management Devices Market Analysis by Mordor Intelligence

Italy wound care management devices market size in 2026 is estimated at USD 743.11 million, growing from 2025 value of USD 710.97 million with 2031 projections showing USD 927.31 million, growing at 4.52% CAGR over 2026-2031. A larger elderly population, rising diabetes incidence, and continuous digital upgrades within the national health service sustain volume growth and encourage faster adoption of advanced dressings, negative pressure wound therapy (NPWT), and bioactive materials. Hospitals remain the backbone of demand, yet home-healthcare momentum is intensifying as payers look to curb inpatient costs and patients favor convenient recovery options. Procurement reforms that standardize tenders and reward value-based purchasing stimulate competition among global brands and regional specialists [1]Ministero della Salute, “Rapporto sul Diabete in Italia,” salute.gov.it . Meanwhile, regulatory deadlines under the EU Medical Device Regulation push manufacturers toward safer, data-rich products that match Italy’s shift to outcome-driven care.

Key Report Takeaways

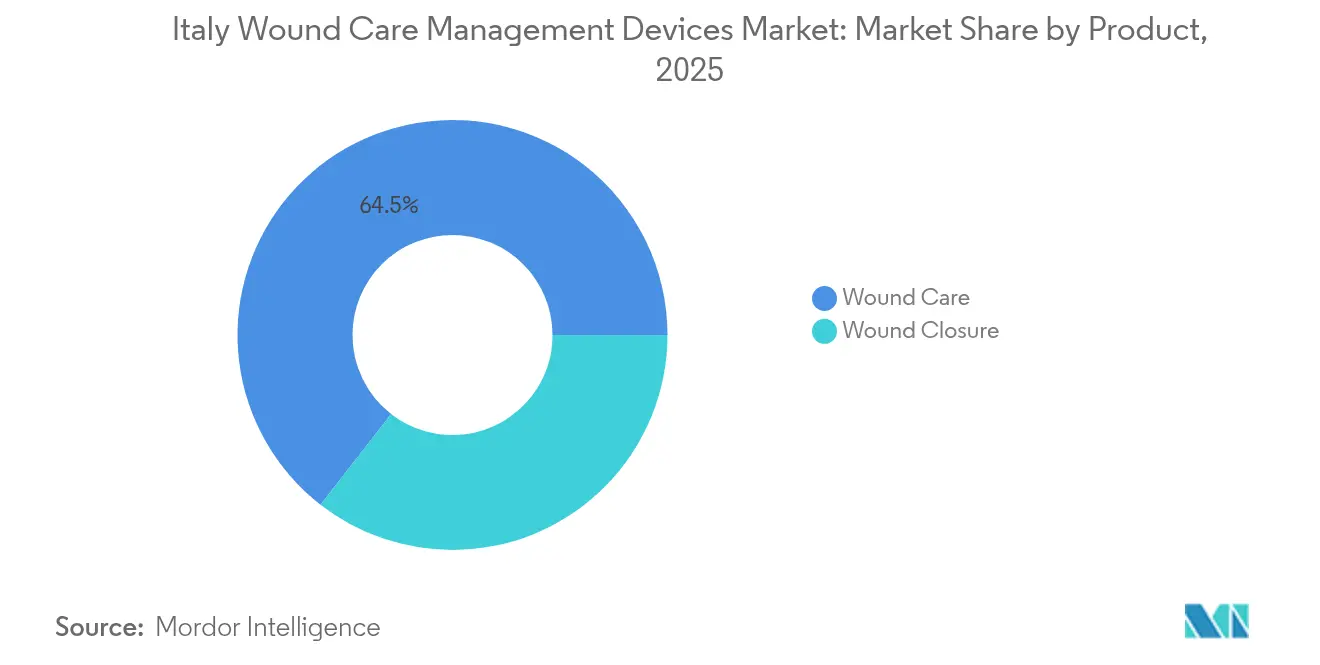

- By product category, wound care led with 64.48% of Italy wound care management devices market share in 2025; wound closure is forecast to expand at a 5.31% CAGR through 2031.

- By wound type, chronic wounds accounted for 58.10% share of the Italy wound care management devices market size in 2025, while acute wounds advance at a 5.39% CAGR between 2026-2031.

- By end user, hospitals & specialty wound clinics commanded 49.10% share of the Italy wound care management devices market size in 2025; home-healthcare settings represent the fastest segment at a 5.66% CAGR to 2031.

- By mode of purchase, institutional procurement controlled 60.72% of Italy wound care management devices market share in 2025, yet retail/OTC channels are growing at 5.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging prevalence of diabetes-linked ulcers | +1.2% | National | Long term (≥ 4 years) |

| Growing adoption of NPWT in public hospitals | +0.8% | National – North led | Medium term (2-4 years) |

| Shift to outpatient & home dressings | +0.9% | National – urban focus | Medium term (2-4 years) |

| National tender reforms for single-use NPWT | +0.6% | National | Short term (≤ 2 years) |

| EU MDR-driven collagen-HA innovation | +0.7% | EU-wide | Long term (≥ 4 years) |

| Pay-for-performance rewards for fast closure | +0.5% | Select regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Prevalence of Diabetes-Linked Chronic Ulcers

Italy’s 6% diabetes prevalence feeds continuous demand for sophisticated dressings and off-the-shelf NPWT that curb hospitalization costs averaging EUR 4,888 per diabetic foot ulcer case. Ageing amplifies this pressure because ulcer risk rises sharply after 65 years. Hospitals increasingly employ predictive analytics—machine-learning algorithms with 80% accuracy—to prioritize high-risk patients and guide early intervention. Suppliers offering integrated device portfolios, remote monitoring, and evidence-based protocols gain traction with regional health authorities seeking budget predictability [2]Roberto Da Ros, "Burden of Infected Diabetic Foot Ulcers on Hospital Admissions and Costs in a Third-Level Center," MDPI, mdpi.com.

Growing Adoption of NPWT in Italian Public Hospitals

Clinical-economic studies show NPWT shortens stays by 2.5 days and lowers readmissions, prompting procurement teams in Lombardy and Emilia-Romagna to accelerate single-use system tenders. After Europe-wide clinical standardization, nurses across Italy report smoother protocol rollouts and fewer dressing-related infections. Portable, battery-powered units designed for transfer to primary care settings now form a fast-growing sub-line that aligns with home-care expansion [3]Luc Téot, "Negative Pressure Wound Therapy An update for clinicians and outpatient care givers," EWMA, journals.cambridgemedia.com.au.

Shift to Outpatient & Home-Based Advanced Wound Dressings

The National Recovery and Resilience Plan commits EUR 15.62 billion to community care and telehealth integration, allowing clinicians to manage chronic wounds remotely with smart dressings that transmit exudate or temperature data. Patient surveys during the pandemic showed high satisfaction and reduced clinic visits when photos and data were shared via secure apps. Device makers that bundle intuitive applicators, digital platforms, and reimbursement support position strongly for this shift.

EU MDR-Driven Innovation in Bioactive Collagen-HA Dressings

Extended transition deadlines to 2027-2028 create breathing space for suppliers to launch collagen-HA composites backed by robust clinical files. Trials in Italy’s 2 million chronic-wound population confirm faster granulation and lower infection risk, driving formulary inclusion in university hospitals. Vendors with post-market surveillance infrastructure and local manufacturing partnerships build competitive edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unfavorable reimbursement for next-gen substitutes | -0.7% | National – variable by region | Long term (≥ 4 years) |

| Procurement delays in Southern Italy | -0.4% | Southern regions | Medium term (2-4 years) |

| Clinician training gap for smart monitoring | -0.3% | National – small facilities | Short term (≤ 2 years) |

| Import-dependent foam & alginate supply | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unfavorable Reimbursement for Next-Gen Skin Substitutes

AIFA’s cost-effectiveness lenses slow listing for premium cellular matrices, partly because 23% of health outlays already fall on patients. Where dossiers lack extensive Italian data, regional commissions hesitate to grant coverage, forcing clinicians to rely on conventional dressings. Companies that pair long-term outcome studies with budget impact models are improving acceptance, but widespread coverage remains a multi-year prospect.

Regional Procurement Delays in Southern Italy

Calabria, Sicilia, and Puglia report slower tender cycles and lower essential-service scores, leading many residents to travel north for complex wound care. Legislation granting full healthcare autonomy in 2024 raises the risk of deeper fragmentation, adding complexity for suppliers that must navigate 20 distinct procurement calendars. Standardization drives at the national level aim to narrow gaps, yet adoption lags and market access timelines remain uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Dressing Dominance Coupled with Closure Innovation

Wound care products held a commanding 64.48% share of the Italy wound care management devices market in 2025 as clinicians relied on advanced dressings, foams, hydrofibers, and NPWT canisters for day-to-day ulcer management. The recurring replacement cycle secures predictable revenue, and demand is reinforced by 2 million chronic wound cases that require constant exudate management. Traditional gauze usage is falling because antimicrobial dressings achieve faster epithelialization and fewer infection-related readmissions. Portable NPWT units strengthen outpatient adoption, while single-use kits lower nurse workload and cross-contamination risk.

Wound closure products expand at a 5.31% CAGR to 2031, outpacing the broader Italy wound care management devices market. Increased elective surgeries and minimally invasive procedures in major university centers stimulate uptake of absorbable staplers, tissue adhesives, and novel sealants. Surgeons in Lombardy report reduced operating time when using bioresorbable adhesives, aligning with hospital pay-for-performance metrics that reward shorter stays. Start-ups focusing on synthetic polymer glues that set in under 60 seconds attract venture funding, adding competitive pressure.

By Wound Type: Chronic Foundation Underpins Acute Momentum

Chronic wounds contributed 58.10% to the Italy wound care management devices market size in 2025, reflecting the persistence of diabetic foot, pressure, and venous ulcers. Diabetic ulcers alone generate treatment outlays of EUR 4,888 per patient and push hospitals to adopt algorithms that predict non-healing trajectories and trigger early NPWT initiation. Protein-enriched platelet-rich plasma injections achieving 52% area reduction exemplify therapies that could shift cost burdens from inpatient beds to outpatient infusion rooms.

Acute wounds grow faster, registering a 5.39% CAGR as trauma centers upgrade burn units and adopt closed-incision NPWT. Economic analyses from Italian surgery wards show EUR 166,944 savings per 100 patients when NPWT prevents surgical site infections. Burn care research institutes in Emilia-Romagna also test xenogenic dermal matrices that promise shorter grafting intervals and less hypertrophic scarring.

By End User: Hospitals Anchor Growth While Home Care Accelerates

Hospitals and specialty wound clinics delivered 49.10% of 2025 revenue, cementing their role in managing complex ulcers, post-operative wounds, and limb-threatening infections. Multidisciplinary teams integrate vascular surgeons, diabetologists, and specialized nurses to coordinate debridement, revascularization, and advanced dressing changes. Capital budgets prioritize smart NPWT consoles that synchronize with electronic health records for outcomes tracking.

Home-healthcare settings post a brisk 5.66% CAGR through 2031. Municipal nurses use mobile apps to guide dressing changes, upload images, and receive automated alerts when wounds stagnate. Patients appreciate fewer clinic visits and better sleep quality when using low-profile foam dressings. Suppliers that integrate tech support hotlines and subscription refill services into their offerings win loyalty among caregivers.

By Mode of Purchase: Institutional Muscle Faces Consumer Pull

Institutional procurement captured 60.72% of the Italy wound care management devices market share in 2025 because public hospitals bundle bulk orders that emphasize unit-cost discipline. Recent value-based tenders, however, score bidders on healing rates and reduced length of stay, shifting the focus from cheapest to most economical over the care pathway. Single-source multi-year contracts covering NPWT, advanced dressings, and staff training are gaining traction in Northern regions.

Retail and OTC channels, rising at 5.51% CAGR, mirror consumers’ willingness to address minor wounds or post-surgical incisions at home. Pharmacies stock silver hydrofiber dressings, silicone tapes, and skin barriers previously confined to hospital formularies. Tele-consult platforms link pharmacists with wound specialists who guide therapy escalation, boosting sales of premium products, especially in metropolitan areas where mobile ordering is commonplace.

Geography Analysis

Regional performance diverges sharply. Lombardy, Emilia-Romagna, and Veneto together account for close to half of total demand in the Italy wound care management devices market, driven by higher disposable incomes, better hospital infrastructure, and early adoption of EU MDR-compliant technologies. These regions integrate electronic wound registries that feed real-time data into procurement dashboards, accelerating product switches when outcomes improve.

Central Italy, led by Lazio and Tuscany, shows balanced growth as teaching hospitals test AI-enabled imaging that predicts granulation tissue progression. Procurement consortia here push suppliers to co-invest in staff education and telehealth pilots, fostering collaborative commercialization models.

Southern regions lag in adoption. Calabria and Puglia confront longer tender cycles and clinician shortages, slowing penetration of smart NPWT and bioactive dressings. Patient migration northward for advanced care illustrates the service gap and signals untapped potential once regional autonomy frameworks stabilize funding. Digital tools that eliminate travel—such as smartphone wound monitoring—could narrow disparities and unlock new volumes if reimbursement hurdles are cleared.

Regulatory Landscape

Italy regulates wound care management devices under the EU Medical Device Regulation (MDR 2017/745). The Ministero della Salute (Directorate of Medical Devices and Pharmaceutical Services) serves as the competent authority for national oversight, vigilance, and related authorizations. Legislative Decree No. 137 of 5 August 2022 is the key national measure aligning Italian law to the MDR framework, shaping compliance expectations for clinical evidence, post-market surveillance, and traceability for products sold into hospitals and community settings.

In addition to CE marking, Italy requires device registration in the national database (Banca dati nazionale dei dispositivi medici, BD/RDM). This remains an important market access step while Eudamed functionality continues to transition. Manufacturers, including extra-EU companies, must follow Italy-specific registration and validation processes when Italy is selected as the competent authority, which makes local regulatory operations and data readiness a practical requirement for maintaining listings and participating in institutional tenders.

Competitive Landscape

The Italy wound care management devices market features a moderately fragmented profile where the top five players control a significant but not overwhelming slice of revenue. Solventum, Smith+Nephew, Mölnlycke, ConvaTec, and Coloplast combine robust brand equity with large hospital networks. Smith+Nephew posted 12.2% advanced wound management growth in Q4 2024 thanks to an expanded silicone foam line. ConvaTec logged 6.7% organic growth during H1 2024 powered by Aquacel Ag+ and the InnovaMatrix range.

Product differentiation is moving beyond dressings toward integrated digital solutions. Solventum’s V.A.C. Peel & Place dressing cuts application time by 61% and extends wear to seven days, meeting hospitals’ efficiency targets. Regional manufacturers specialize in collagen-HA sheets and custom foam kits, leveraging local supply chains to counter import-related disruptions. Start-ups backed by university incubators focus on AI wound imaging and nitric-oxide topical therapies poised for launch in 2026.

Strategic alliances accelerate scale. Mölnlycke partners with logistics providers to ensure 24-hour delivery to remote clinics, while ConvaTec pilots subscription plans that bill regional health funds per healed wound episode. With value-based care on the horizon, firms that demonstrate lower total cost of treatment and provide exhaustive post-market surveillance are likely to defend or grow share.

Italy Wound Care Management Devices Industry Leaders

-

Coloplast AS

-

Convatec Inc.

-

Smith + Nephew

-

Medtronic

-

Solventum

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An evidence-led purchasing opportunity is strengthening as Italy brings the National Health Technology Assessment Programme for medical devices (PNHTA-DM) 2026-2028 into its operational phase in 2026, after unlocking EUR 13 million in funding. The programme targets 50-100 HTA assessments during 2026 for devices with high clinical, organizational, and economic impact. For wound care management devices, this raises the premium on real-world outcomes and total-cost-of-care submissions, favoring suppliers that can pair advanced dressings, NPWT, and digital monitoring with structured clinical and economic dossiers aligned to HTA requirements used across regions.

Another focus area is procurement readiness and coding alignment. The Classificazione italiana dei dispositivi medici (CID) took effect on January 1, 2026, introducing a hierarchical alphanumeric coding approach aligned with MDR and EMDN that can influence how products are specified and compared in regional tenders. Suppliers that map their portfolios quickly to CID and BD/RDM registration workflows can reduce friction in institutional uptake. Regional decision-making continues to act as a gate for market access, and HTA activity provides a concrete signal, such as Tuscany publishing rapid HTA reports in 2026, reinforcing the need for localized access strategies that combine training and service models for home and outpatient use with tender-ready clinical evidence for chronic-wound pathways.

Recent Industry Developments

- May 2026: Smith+Nephew announced the launch of ALLEVYN COMPLETE CARE Dressing and the RENASYS EDGE NPWT system at EWMA 2026 in Bremen. The releases emphasize simplified application and next-generation therapy options that support shorter, more standardized care pathways relevant to both hospital and outpatient settings. The portfolio refresh increases competitive pressure on advanced dressings and portable NPWT segments used across European markets, including Italy.

- September 2025: ConvaTec secured regulatory approval in the UK and EU for ConvaMatrix, positioning the porcine placenta-derived skin substitute for a European launch beginning in 2026. The milestone expands ConvaTec's addressable portfolio in advanced tissue and bioactive wound solutions where reimbursement and evidence thresholds are high. It also raises the bar for competitors on clinical documentation and post-market data in markets operating under EU MDR requirements.

- April 2024: Solventum expanded the capabilities of its negative pressure wound therapy offering with updates to its V.A.C. Peel and Place dressing platform, reinforcing its focus on faster application and extended wear time. The change supports hospital efficiency goals by reducing clinician time per dressing change and standardizing protocol execution. The update supports Solventum's positioning in institutional tenders where workflow savings and total-cost impact influence purchasing decisions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is measured as the revenue generated in Italy from wound care management devices used to prevent, treat, and manage acute and chronic wounds across clinical and home-care settings.

Scope exclusions: We exclude over-the-counter antiseptic solutions and purely pharmaceutical creams meant for minor cuts.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Topical Agents

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting structure of the market, so the model stays anchored to real-world wound incidence and how care is delivered in Italy. We relied on public, non-paywalled sources such as Italian health statistics releases, OECD health indicators, Istituto Superiore di Sanita publications where available, EU Medical Device Regulation guidance pages, and peer-reviewed clinical and health-economics journals covering chronic wound prevalence and care pathways.

To translate clinical need into spend, supporting reads were taken from company annual reports and investor presentations, hospital procurement notices where accessible, and reputable press on reimbursement and tender changes. In parallel, we used paid subscriptions for company financials and intelligence, and for news and financials, mainly to cross-check revenue exposure and major product launches that can shift category mix. These desk sources are not exhaustive, and many other public documents were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what part of wound care demand is actually served by devices, and how pricing and usage differ by site of care. We spoke with a mix of manufacturers, distributors, hospital procurement stakeholders, clinicians working in wound clinics, and home-care oriented channels, and then used follow-up checks to resolve gaps left by public data.

Italy-specific assumptions were stress-tested around chronic wound treatment intensity, tender-driven pricing behavior, and adoption levels of advanced therapies in hospitals versus community care, before final totals were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | |

| Mid tier: 49% | Functional/Unit leaders: 42% | |

| Smaller Players: 19% | Managers: 46% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach where wound prevalence and treated-case volumes are converted into category spending through product usage norms and average selling price ranges for key device groups. Once the totals were formed, they were corroborated with selective bottom-up approximations, including sampled price-per-unit checks, channel mix logic across hospitals and home care, and supplier revenue exposure splits, which are then used to adjust outliers.

Key inputs in the model included chronic wound prevalence signals (such as diabetic foot ulcers and pressure injuries), inpatient and outpatient procedure volumes linked to surgical wounds, adoption rates for advanced dressings and negative pressure wound therapy, public tender timing effects on price realization, and the share of care shifting toward home settings. Where volume data was incomplete for smaller channels, gaps were handled by using proxy utilization rates from clinician feedback and then applying conservative ranges for per-patient consumption.

For forecasting, scenario analysis was used, supported by short time-series smoothing on the stable components of demand (like aging-linked chronic wounds) and primary expert expectations on pricing pressure and therapy penetration. The final forecast is therefore driven by a small set of repeatable variables rather than a single growth rate assumption.

Data Validation & Update Cycle

Validation was done through cross-checking the model output against independent signals such as device adoption commentary from clinicians, public procurement patterns, and the direction of reported category growth in company disclosures. When a number moved outside expected ranges, the drivers were re-opened, and we re-contacted sources to confirm whether the change was from volume, price, or mix.

Before sign-off, the full model is reviewed in multiple steps, including consistency checks across years and a fresh read of major assumptions that materially impact the total. Reports are refreshed annually, with interim updates when major regulatory, reimbursement, or tender events can shift market behavior. Right before delivery, an analyst performs a final pass so clients receive the latest updated view.

Mordor Intelligence's Italy Wound Care Management Devices Market Size Compared Against Other Published Estimates

Published market sizes for wound care devices in Italy can differ even when the same topic label is used, since sources often choose different product inclusions, pricing logic, and the year they treat as the current baseline. Differences also show up when some studies lean more on shipment style assumptions, while others are built from treated patient demand and the therapy mix used in practice.

The main gap comes from whether over-the-counter antiseptic solutions and purely pharmaceutical creams are counted alongside device-led wound management, since Mordor Intelligence keeps the total limited to wound care management devices and related device-driven categories that are commonly procured through clinical and home-care channels.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 710.97 M (2025) | |

| Industry Publisher A | USD 692.19 M (2024) | Uses an earlier base year and does not clearly spell out exclusions, so some adjacent wound-care spending can be treated differently, especially where advanced dressings are grouped with broader supplies. |

| Market Tracker B | USD 489.22 M (2024) | Appears to apply a narrower device and product basket and may rely on a more conservative pricing and adoption mix for advanced therapies, which can compress totals versus a treated-case demand build. |

The spread across the three values is largely explained by scope and year alignment, followed by how therapy mix and price realization are handled under tender-driven procurement. By keeping assumptions tied to observable care settings and repeatable demand indicators, the estimate stays easier to reconcile when users sanity-check it against hospital utilization and category adoption trends.

Key Questions Answered in the Report

What is the current size of the Italy wound care management devices market?

The market is valued at USD 743.11 million in 2026 and is forecast to reach USD 927.31 million by 2031.

Which product category leads the Italy wound care management devices market?

Advanced wound dressings and related care products command the highest share at 64.48% in 2025.

How fast is the home-healthcare segment growing?

Home-healthcare settings are expanding at a 5.66% CAGR through 2031, the fastest among end-user segments.

What is driving the adoption of NPWT systems?

Clinical evidence of shorter hospital stays and cost savings, coupled with single-use portability, is boosting NPWT demand in Italian hospitals.

How will regional autonomy influence market access?

Greater regional control over healthcare budgets may widen North–South disparities, making supplier agility and localized strategies essential.

Which companies hold notable positions in the competitive landscape?

Solventum, Smith+Nephew, Medtronic, ConvaTec, and Coloplast are the primary multinational players leveraging broad portfolios and clinical data to maintain share.

Page last updated on: