Spain Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

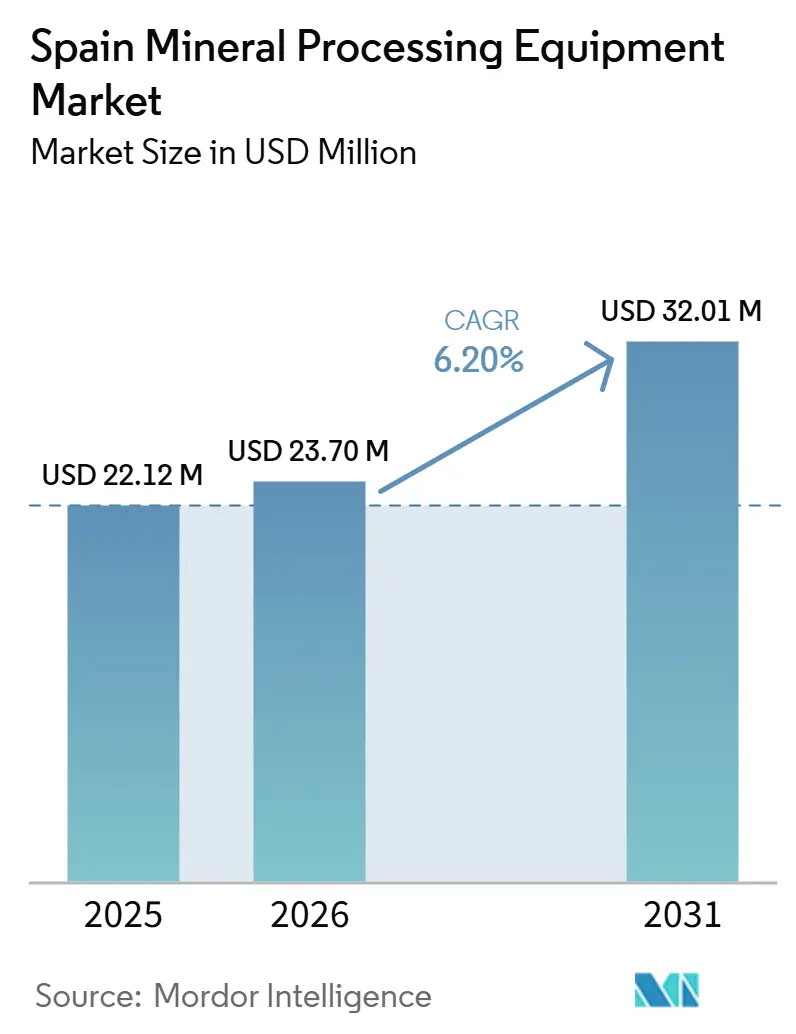

| Base Year Market Size (2025) | USD 22.12 Million |

| Market Size (2026) | USD 23.70 Million |

| Market Size (2031) | USD 32.01 Million |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Spanish mineral processing equipment market size was valued at USD 22.12 million in 2025 and estimated to grow from USD 23.70 million in 2026 to reach USD 32.01 million by 2031, at a CAGR of 6.20% during the forecast period (2026-2031). Strong policy support under the EU Critical Raw Materials Act and Madrid’s EUR 414 million (~USD 481 million) National Mineral Raw Materials Action Plan is reinvigorating a sector that had contracted for two decades, encouraging operators to embed automation and circular-economy requirements in both greenfield and brownfield investments. Several projects—focused on lithium in Extremadura and Galicia, tungsten in Badajoz and Ciudad Real, and copper in Sevilla—have achieved strategic status. This designation has expedited permitting processes and secured financing from the European Investment Bank, effectively streamlining procurement cycles for systems related to crushing, conveying, and hydrometallurgy [1]“Strategic Projects under the Critical Raw Materials Act,” European Commission, europa.eu . As demand pivots from iron-centric flowsheets to battery minerals, lithium equipment is witnessing significant growth, outpacing the broader trajectory of Spain's mineral processing equipment market. However, challenges persist: water scarcity, fluctuations in electricity prices, and a persistent lack of automation technicians are influencing capital decisions. As a result, buyers are leaning towards energy-efficient crushers, closed-loop water treatment systems, and remote operating centers hosted by vendors.

Key Report Takeaways

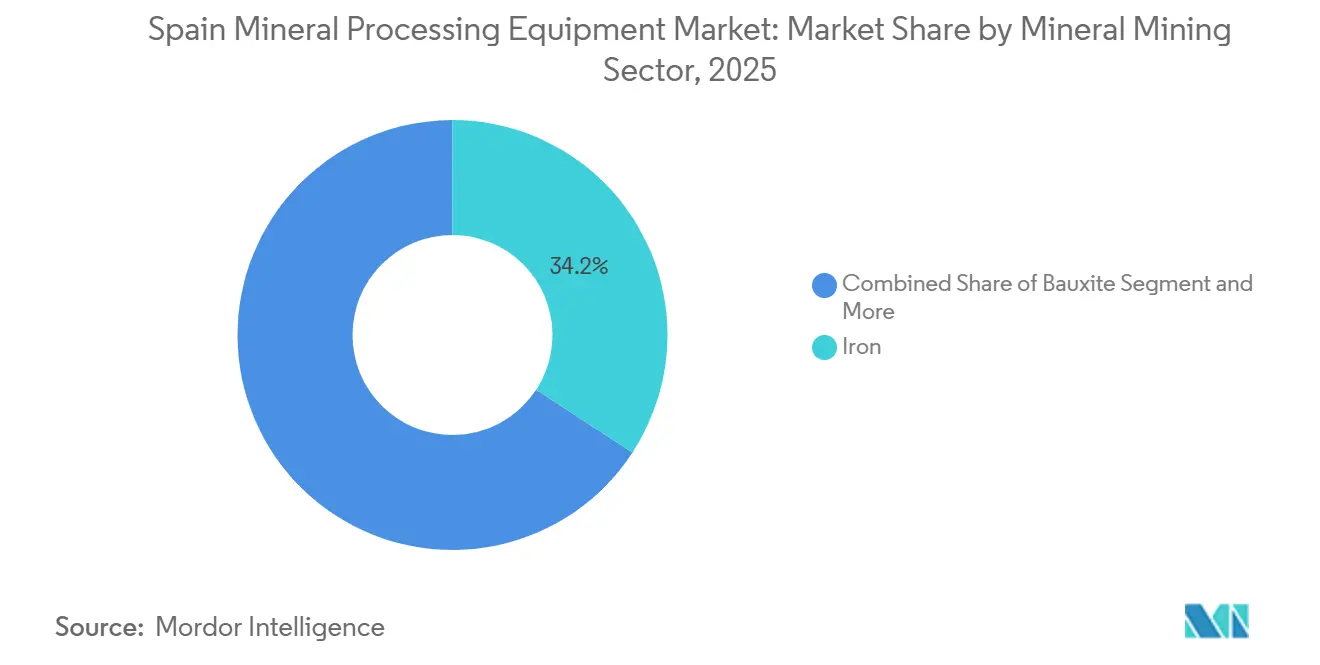

- By mineral mining sector, iron led with 34.18% of the Spanish mineral processing equipment market share in 2025, while lithium is poised to expand at a 6.95% CAGR through 2031.

- By equipment type, crushers commanded 28.33% share of the Spanish mineral processing equipment market size in 2025, and conveyors are projected to register the fastest 7.03% CAGR over 2026-2031.

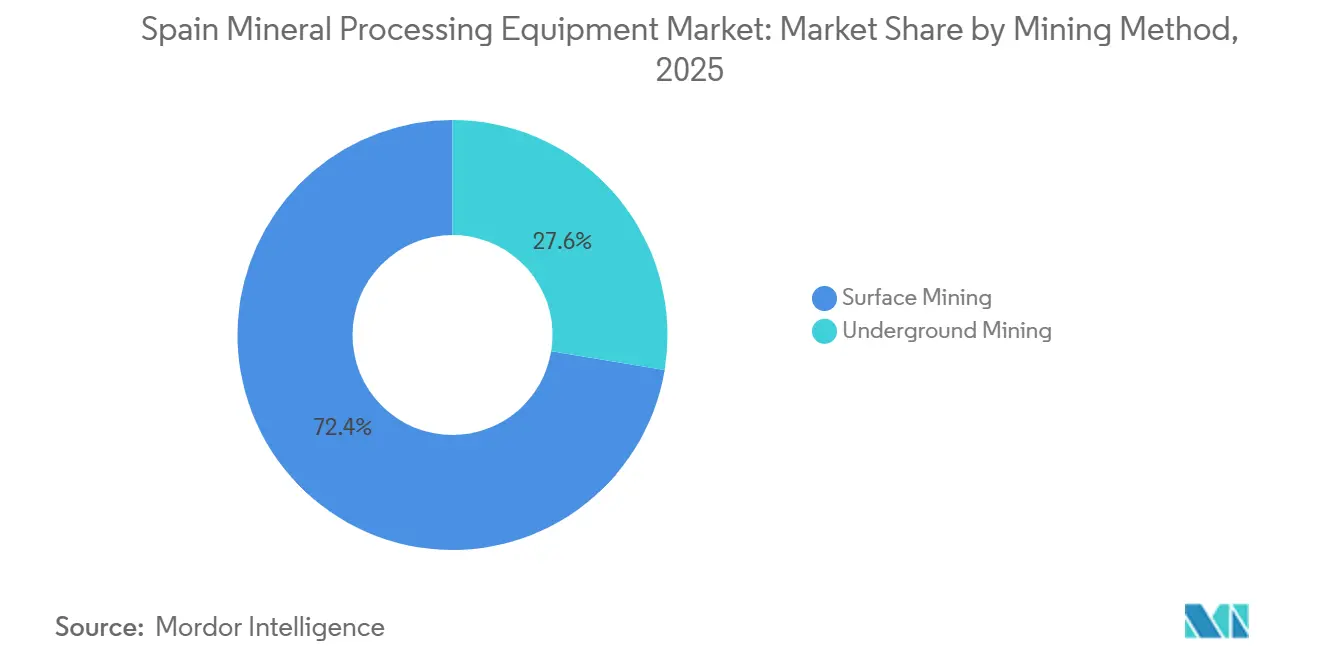

- By mining method, surface operations accounted for 72.41% of the Spanish mineral processing equipment market size in 2025, yet underground solutions are advancing at a 6.72% CAGR to 2031.

- By automation level, semi-automated platforms held 47.36% share in 2025, and fully autonomous systems are forecast to grow at a 7.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide industry scale is not derived from any single country or region but from the combination of national and regional inputs. The mineral processing equipment market size of Mordor Intelligence integrates these into one global valuation.

Spain Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Critical Battery Minerals | +1.8% | Extremadura, Galicia, Castilla y León | Medium term (2-4 years) |

| Net-Zero Localization Incentives | +1.5% | National; spillover to Portugal | Long term (≥ 4 years) |

| Surge in Brown-field Plant Retrofits | +1.2% | Andalusia, Huelva | Short term (≤ 2 years) |

| Government Support for the Mining Sector | +1.0% | Western corridor | Medium term (2-4 years) |

| Mandates on Mine Waste Valorization | +0.9% | Andalusia, Huelva, Asturias | Long term (≥ 4 years) |

| Low-carbon Equipment Financing | +0.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Demand for Critical Battery Minerals

Spain’s Mineral Raw Materials Action Plan (2026-2030) is the nation’s first systematic exploration program since the 1970s and targets lithium, cobalt, graphite, and rare earths across the western corridor from Galicia to Andalusia [2]“National Mineral Raw Materials Action Plan 2026-2030,” Ministry for Ecological Transition, esmining.gob.es. Strategic status under the Critical Raw Materials Act grants streamlined permitting and EIB financing, which is already accelerating equipment orders for flotation cells, autoclaves, and ion-exchange circuits designed for spodumene and lepidolite ores. In Spain, two lithium hubs are aligning with the construction of gigafactories in Valencia and Navarra. This synchronization establishes a crucial offtake anchor, mitigating upfront capital expenditure risks for processing plants. As a result, the growth of lithium equipment in Spain outpaces the overall growth of the country's mineral processing equipment market. Furthermore, the Pedersen electrolysis, validated by universities, significantly reduces water usage compared to the traditional Bayer process, offering domestic OEMs a notable environmental edge. These strategic moves collectively position Spain as the leading contender in the EU for battery-grade mineral conversion capacity.

EU Net-Zero Industry Act Localization Incentives

The Net-Zero Industry Act mandates that 40% of annually deployed strategic technologies be made inside the bloc by 2030, effectively favoring EU-sourced mineral processing equipment. Spain’s joint Iberian Pyrite Belt work with Portugal harmonizes standards and allows OEMs to scale R&D across two national markets, cutting per-unit capex for modular crushing and conveying lines. Fiscal measures adopted in 2025 include accelerated depreciation and tax credits for new lithium hydroxide refineries, driving incremental orders for pressure-oxidation autoclaves and solvent-extraction mixers. Strategic project designations compress permitting to around 24-27 months, so suppliers with off-the-shelf modules gain share at the expense of bespoke fabricators. ESG compliance now acts as a gateway for public co-funding, pushing vendors to integrate real-time emissions and water analytics as standard features.

Surge in Brown-field Plant Digital Retrofits

At Sandfire's MATSA mine, RCT's ControlMaster and Epiroc's ABC Total platforms have significantly advanced underground fleet autonomy while reducing operator exposure in sulfide zones. The Horizon Europe MASTERMINE initiative is now applying these insights across multiple sites, establishing a reference architecture that smaller operators in Spain can implement, even without dedicated data-science expertise. As miners prioritize maximizing existing assets over new greenfield projects, digital retrofits are driving growth in Spain's mineral processing equipment market. Metso's modular FIT conveyor lines streamline installation processes and address a persistent labor shortage. Sandvik's rigs, equipped with predictive analytics, have enhanced component lifespan, underscoring the value of sensor-rich hardware.

Growing Government Support for the Mining Sector

Under its exploration program, Madrid invests in extensive core re-logging, conducts new geophysical surveys, and utilizes remote sensing. Additionally, it has established a significant co-investment facility aimed at projects that integrate land rehabilitation with resource recovery. The CSIC has identified that roasted pyrite waste in the Odiel Basin holds valuable resources such as cobalt, antimony, and tungsten. This finding has spurred interest in technologies like bio-leach reactors and electro-separation skids, which combine reclamation efforts with metal extraction. Thanks to the establishment of single-window permitting offices in every autonomous community and the strategic labels from CRMA, the typical permitting timelines have been significantly reduced. These strategic moves have boosted the growth of Spain's mineral processing equipment market, facilitating less risky exploration and a quicker rollout of pilot plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy Environmental Permitting Timelines | -1.3% | Andalusia, Galicia | Long term (≥ 4 years) |

| Tight Water-use Restrictions | -0.9% | Andalusia, Extremadura | Medium term (2-4 years) |

| Shortage of Skilled Technicians | -0.8% | Rural mining belts | Medium term (2-4 years) |

| Electricity Prices Impacting OPEX | -0.7% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy Environmental Permitting Timelines

Andalusia's demand for additional impact studies pushed back Aznalcóllar’s copper-zinc restart from a 2025 target to 2027. This delay underscores how multi-layer reviews can extend timelines by up to three years, even for sites deemed strategic. Meanwhile, Galicia’s Mina Muga tungsten project has been ensnared in a 12-year review, primarily due to Natura 2000 concerns. These concerns have not only frozen equipment orders but also dissuaded OEMs from allocating engineering resources. While CRMA status can potentially shorten these timelines to around 26 months, by early 2026, only seven ventures in Spain had achieved this status. As a result, the majority of applicants remain bound by the older, more protracted regime. Such delays have tangible repercussions: Spain's mineral processing equipment market growth sees a notable dip. Notably, large crushers and overland conveyors are feeling the brunt, as operators postpone purchases, awaiting final permits.

Tight Water-use Restrictions in Drought-prone Mining Regions

In 2024, Emerita Resources sought a significant amount of water annually in Huelva, facing backlash from farmers after the Andévalo reservoir's capacity dropped significantly. This scarcity compelled redesigns, pivoting towards closed-loop circuits and dry-stacking. While mandatory closed-loop systems increase capital expenditures, they simultaneously boost the demand for paste-backfill plants, thickeners, and pressure filters. At Aznalcóllar, REECOVERY achieved high water recycling efficiency, but scaling up to larger volumes remains a challenge, necessitating further R&D. Consequently, water scarcity curtails growth and steers preference towards dry magnetic separators and sensor-based sorters that operate without process water.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Lithium Drives Equipment Innovation

Iron-focused operations generated 34.18% of Spain's mineral processing equipment market demand in 2025, anchored by Minas de Alquife’s 4.5 Mt/y magnetite circuit that relies on hydrocyclones and dry gravimetric sorting. Lithium, although starting from a smaller installed base, is expanding at a 6.95% CAGR, reflecting two EC-backed projects in Extremadura and Galicia that require dense-media separators, roasting kilns, and containerized flotation lines.

As battery minerals gain prominence, there's a surge in demand for hydrometallurgical autoclaves and ion-exchange columns. Concurrently, iron producers are turning to energy-efficient HPGRs and air classifiers to reduce energy consumption. Government grants, which tie land rehabilitation to resource recovery, are boosting the demand for bio-leach reactors. These reactors are now pivotal in extracting cobalt, antimony, and germanium from tailings. Consequently, by 2029, the Spanish market for lithium mineral processing equipment is set to outpace that of bauxite. This shift is prompting vendors to recalibrate their R&D focus towards low-water flowsheets and enhanced digital traceability.

By Equipment Type: Modular Conveyors Gain Traction

Crushers retained the largest 28.33% slice of 2025 spending, but modular-design conveyors are advancing at a 7.03% CAGR thanks to Metso’s FIT and Foresight lines that shorten on-site assembly by 15%. Sandvik’s CH442 and CH662 cone crushers, introduced in March 2026, remove elastomer liners and extend maintenance intervals to a full year, illustrating how materials science is improving uptime.

Variable-frequency-drive belts allow throughput modulation during price peaks, improving grid-integrated solar economics. Autonomous drills and breakers extend rig life by 40% through predictive wear algorithms, supporting the broader shift from preventive to condition-based maintenance. Closed-loop water mandates are simultaneously elevating orders for pressure filters and paste-backfill plants that fall under the “Others” category. Altogether, these dynamics reinforce a procurement tilt toward modularity and automation across the Spanish mineral processing equipment market.

By Mining Method: Underground Automation Accelerates

Surface operations still captured 72.41% of 2025 equipment demand, yet underground solutions are growing at 6.72% CAGR as lithium, tungsten, and polymetallic projects advance in Extremadura and Castilla y León. RCT's autonomous LHDs at MATSA have reduced haulage cycle times and cut diesel consumption. These efficiencies highlight swift paybacks, even with higher sticker prices than conventional options.

In the Iberian Pyrite Belt, dense ore bodies favor underground mining. Here, considerations like ventilation, geotechnical monitoring, and fleet automation are paramount from the outset. While surface fleets dominate, they grapple with automating large trucks on variable ramps. Yet, pilot programs suggest a significant leap in autonomy by 2030. As subsurface automation gains traction, the Spanish mineral processing equipment market for underground hardware is projected to grow significantly by 2031. This surge intensifies competition between global OEMs and local specialists.

By Automation Level: Fully Autonomous Systems Gain Share

Semi-automated assets represented 47.36% of 2025 outlays, but fully autonomous systems are climbing at a 7.54% CAGR, driven by safety mandates that credit automation with fewer injuries. Sandvik’s AutoMine suite achieves 24/7 operation in sulfide zones where manual shifts were capped at eight hours, and bundled remote-operating-center packages let mines outsource scarce data-science skills.

While small slate and ornamental-stone quarries still rely on manual units, tele-operated drill rigs are beginning to gain traction. Horizon Europe's Mine.io project aims to make digital twins more accessible, potentially paving the way for wider adoption among SMEs. This shift highlights the convergence of labor shortages and ESG metrics, driving a push towards greater autonomy in Spain's mineral processing equipment market.

Geography Analysis

Activity is clustered along a west-to-south corridor from Galicia through Castilla y León and Extremadura to Andalusia, reflecting both geological prospectivity and the focus of Spain’s new exploration program. Andalusia’s Iberian Pyrite Belt hosts Sandfire’s MATSA complex, Cobre Las Cruces, and the Aznalcóllar restart, anchoring orders for underground loaders, hydrometallurgical reactors, and tailings-valorization skids. In Extremadura and Galicia, EC-designated lithium hubs unlock rapid approvals and EIB loans, spurring procurement of dense-media separators and roasting kilns. Huelva province, meanwhile, is emerging as a circular-economy center, with Atlantic Copper’s CirCular smelter targeting WEEE feed.

Infrastructure and water availability shape technology choices. Coastal Andalusia benefits from deep-water ports that handle large gyratory crushers, while landlocked Extremadura prefers containerized units that can be trucked. Chronic drought pushes Andalusia and Extremadura toward dry-stacking and sensor-based sorting that eliminates process water, even at a capex premium. Galicia, with higher rainfall and abundant hydropower, remains attractive for energy-intensive flotation, but still struggles with protracted permitting such as the 12-year delay at Mina Muga.

Castilla y León’s tungsten and tantalum assets appeal to defense and aerospace supply chains, spurring gravity-concentrator sales. Regional one-stop permit offices trim legal costs, giving domestic OEMs like Sotecma and Talleres Alquézar a service-response advantage over global rivals whose nearest hubs sit in Germany or France. Overall, geographic concentration allows vendors to localize parts inventories and win on total cost of ownership, reinforcing Spain’s distinct regional patterns within the wider Spanish mineral processing equipment market.

Mordor Intelligence tracks the mineral processing equipment market with additional country-level coverage spanning Italy, Germany, Japan, Mexico, Oman, Egypt, Morocco, South Africa, and Brazil, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Spanish mineral processing equipment market is moderately fragmented. Global majors—Metso, Sandvik, FLSmidth, Weir, Komatsu—vie with domestic specialists Sotecma, Talleres Alquézar, and Eriez Iberica. Recent moves skew toward digital bundling: Metso’s 2026 tie-up with Loesche on vertical roller mills folds digital twins into grinding circuits, while Sandvik’s CH442/CH662 cone crushers launch embedded analytics that notify operators of liner wear before shutdowns [3]“Digital Milling Collaboration with Loesche,” Atlantic Copper, atlanticcopper.es. Modular pre-engineered platforms such as Metso’s FIT conveyors shave project timelines by a quarter, a critical edge amid labor shortages and cautious capital budgets.

In the evolving landscape of Spain's mineral processing equipment market, circular-economy capabilities emerge as a pivotal arena. Leitat's patents for MOF-based adsorbents, set for 2026, empower Spanish vendors with licensing rights across Europe. Meanwhile, CSIC's advancements in Pedersen electrolysis are carving out a niche in low-water alumina circuits. Despite Spain boasting Europe's richest hard-rock resources, it finds itself without domestic refining in lithium hydroxide conversion. However, OEMs that can provide pressure-oxidation autoclaves and calcination kilns are poised to seize first-mover advantages as construction kicks off in 2027-2028.

In this market, technology has taken precedence over price in shaping procurement decisions. RCT's autonomous LHD package, deployed at MATSA, achieved significant improvements in operational efficiency. Furthermore, ESG compliance has become the linchpin for securing public co-funding. Suppliers boasting ISO 14001 certifications and alignment with the EU Taxonomy enjoy a distinct advantage. Collectively, these dynamics intensify competition and foster a continuous influx of innovative features and service models in Spain's mineral processing equipment sector.

Spain Mineral Processing Equipment Industry Leaders

FLSmidth A/S

Metso Corporation

Sandvik AB

The Weir Group PLC

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Eurobattery Minerals appointed Minepro Solutions to deliver final engineering and metallurgical reconfirmation for the San Juan tungsten plant in Ourense, setting the stage for a Q1 2027 construction start.

- March 2026: Sandvik unveiled CH442 and CH662 cone crushers, enhancing component strength, simplifying maintenance, and adding smart-automation functions for deeper production visibility.

Spain Mineral Processing Equipment Market Report Scope

The scope includes segmentation by mineral mining sector (bauxite, iron, and more), equipment type (crushers, conveyors, drills and breakers, feeders, and others), mining method (surface mining and underground mining), and automation level (manual, semi-automated, and fully automated). Market size and growth forecasts are presented by value in USD and by volume in units.

| Bauxite |

| Iron |

| Lithium |

| Others |

| Crushers |

| Conveyors |

| Drills and Breakers |

| Feeders |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Others | |

| By Equipment Type | Crushers |

| Conveyors | |

| Drills and Breakers | |

| Feeders | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

How large is Spain’s mineral-processing equipment demand today?

The Spain mineral processing equipment market size reached USD 23.70 million in 2026 and is expected to hit USD 32.01 million by 2031.

Which segment grows fastest through 2031?

Lithium-focused processing lines exhibit the highest 6.95% CAGR as two EC-backed projects advance toward construction.

Where are most new plants located?

A west-south corridor covering Galicia, Castilla y León, Extremadura, and Andalusia hosts the bulk of upcoming lithium, copper, and tungsten projects.

Which technology trend dominates procurement agendas?

Fully autonomous crushers, drills, and loaders that integrate digital twins and predictive analytics are gaining share thanks to 25-35% lifecycle cost savings.

Page last updated on: