Germany Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

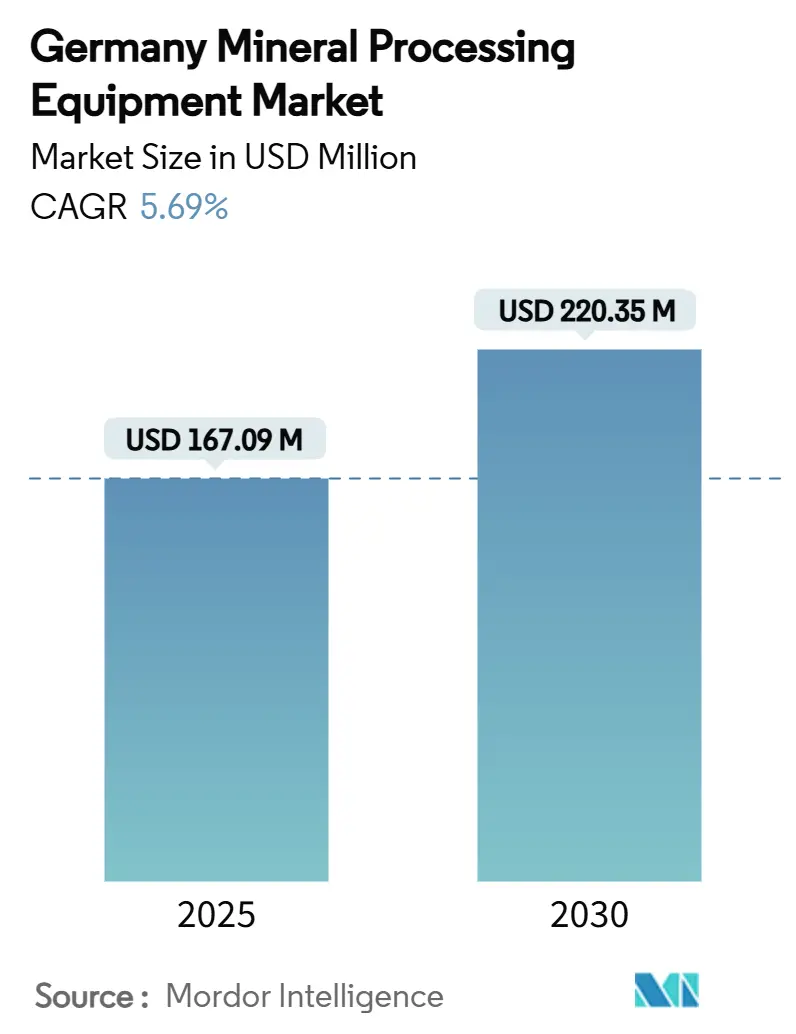

| Market Size (2025) | USD 167.09 Million |

| Market Size (2030) | USD 220.35 Million |

| Growth Rate (2025 - 2030) | 5.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Mineral Processing Equipment Market Analysis by Mordor Intelligence

The German Mineral Processing Equipment Market size is estimated at USD 167.09 million in 2025, and is expected to reach USD 220.35 million by 2030, at a CAGR of 5.69% during the forecast period (2025-2030). Growing investor confidence springs from Germany’s EUR One Billion Raw Materials Fund and the European Critical Raw Materials Act, which funnel capital into domestic extraction, processing, and recycling facilities. Policy-backed funding converges with a nationwide coal phase-out that steers operators toward renewable-powered plants equipped with energy-efficient crushers, conveyors, and digital control systems. Surging demand for lithium, rare earths, and secondary raw materials is elevating order backlogs for automated separation, grinding, and sorting solutions. At the same time, high industrial energy prices and an aging technical workforce compel buyers to favor fully automated, low-maintenance equipment packages that shrink lifetime operating costs. Competitive intensity is moderate, with global machinery majors and mid-sized German specialists racing to embed Industrie 4.0 connectivity and circular-economy functionality into next-generation product lines.

Key Report Takeaways

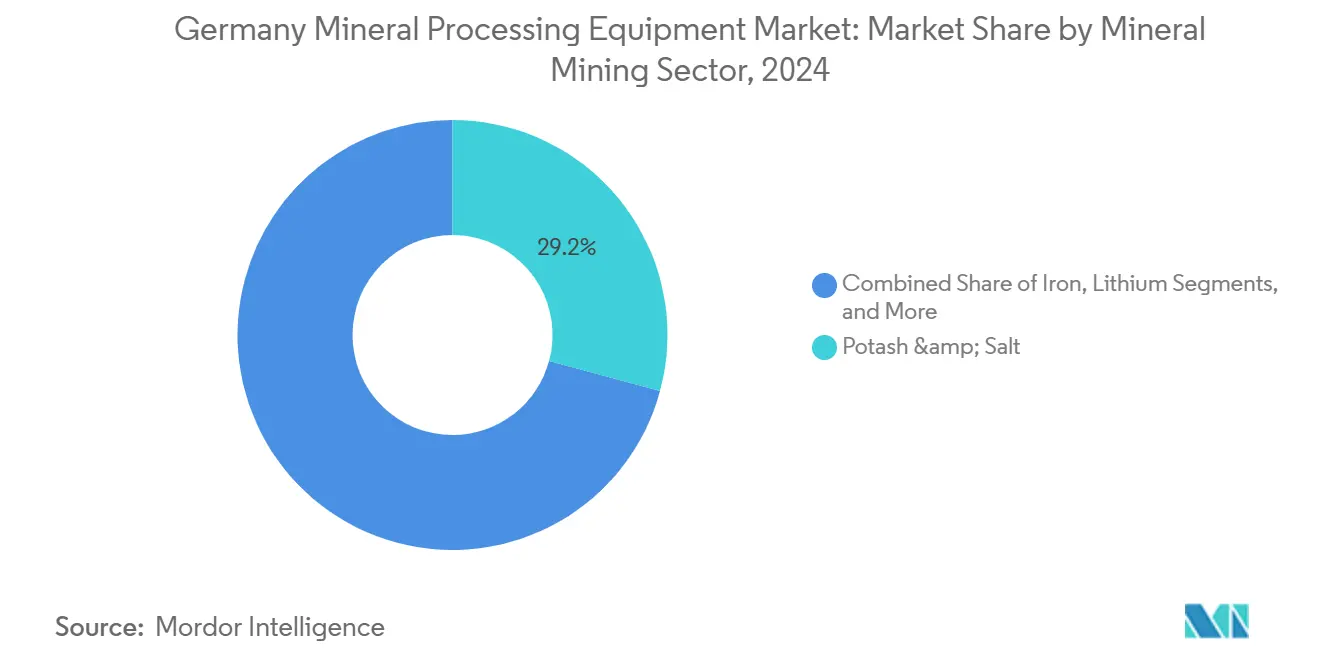

- By mineral mining sector, potash & salt processing led with 29.15% of Germany's mineral processing equipment market share in 2024, whereas lithium processing is projected to expand at a 5.71% CAGR through 2030.

- By equipment type, crushers captured 25.47% revenue share of the German mineral processing equipment market in 2024; conveyors exhibit the highest growth potential at a 5.75% CAGR to 2030.

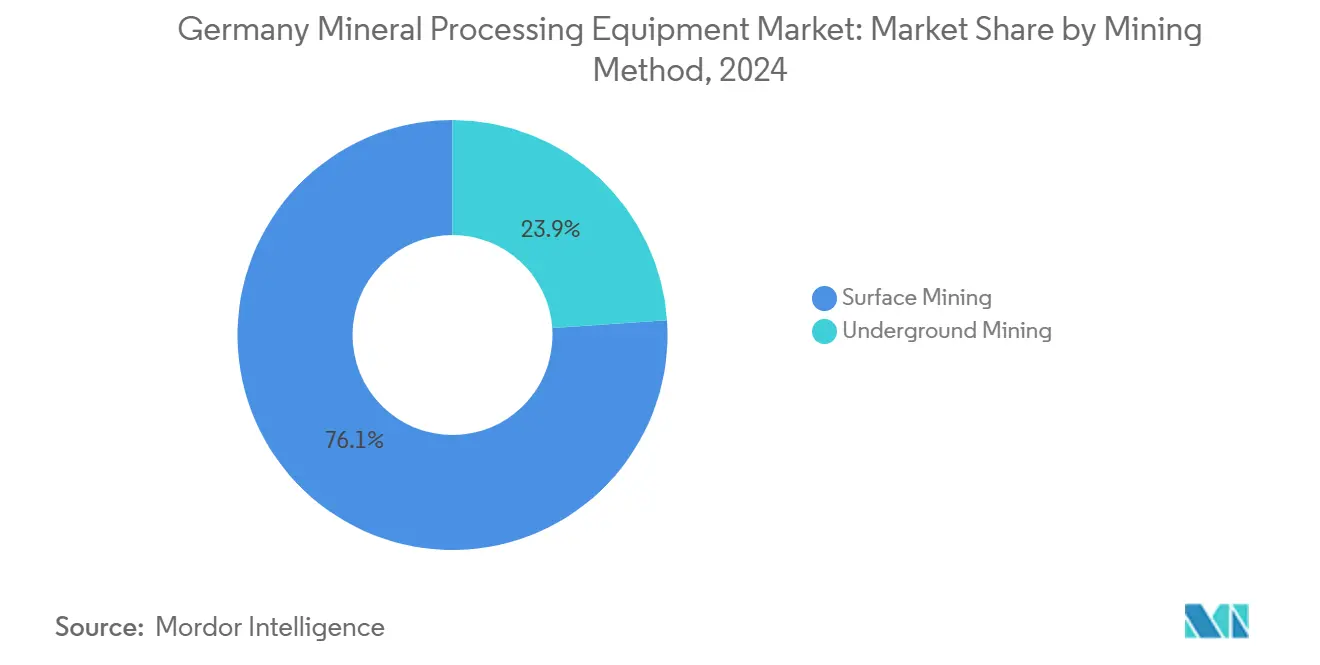

- By mining method, surface mining accounted for 76.13% of the German mineral processing equipment market size in 2024, while underground mining is advancing at a 5.84% CAGR to 2030.

- By automation level, semi-automated systems held 48.17% of Germany's mineral processing equipment market share in 2024; fully automated solutions are forecast to grow at a 5.88% CAGR through 2030.

Dynamics observed within Germany present a country level view when set against the broader international context. The mineral processing equipment market analysis by Mordor Intelligence provides that expanded global perspective.

Germany Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Support | +1.2% | National, with EU coordination | Long term (≥ 4 years) |

| European Critical Raw Materials Act Fast-Tracks Funding | +1.1% | EU-wide, Germany priority regions | Long term (≥ 4 years) |

| Circular-Economy Push | +0.9% | National, urban concentration | Medium term (2-4 years) |

| Increasing Mineral Production | +0.8% | National, concentrated in Saxony and Thuringia | Medium term (2-4 years) |

| Digitally Integrated Plants Enabled | +0.7% | National, industrial clusters | Medium term (2-4 years) |

| Accelerated Brownfield Mine Expansions | +0.6% | Regional, eastern Germany focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Support via German Raw Materials Strategy 2024

KfW’s EUR 1 billion Raw Materials Fund accepts proposals of EUR 50 million – EUR 150 million for mining, processing, and recycling projects involving cobalt, copper, lithium, and rare earths. The program replaces earlier, fragmented grant schemes with a single window that shortens application cycles and guarantees long-term offtake contracts to qualifying lenders. Project sponsors in France and Italy align investment terms with KfW to build a trilateral pipeline of critical-material supply anchors processing capacity inside Europe. Equipment vendors supplying crushers, autoclaves, and solvent extraction circuits report faster order conversion because government guarantees reduce counterparty risk. The German Mineral Resources Agency now tracks 34 critical materials and publishes quarterly price alerts, giving operators early signals to adjust procurement timetables and hedge exposure.

European Critical Raw Materials Act 2024 Fast-tracks Funding

The European Commission has granted “Strategic Project” status to 47 ventures, including German lithium refineries in Saxony and rare-earth recycling hubs near Leipzig. Projects reaching financial close receive permit approvals in months instead of years, a shift accelerating procurement of high-capacity flotation cells, magnetic separators, and AI-enabled sorters. To hit EU targets of 10% domestic extraction, 40% processing, and 25% recycling by 2030, German operators partner with Scandinavian and Iberian miners, routing unrefined concentrates to German plants equipped with low-carbon electricity and hydrogen. Because single-country sourcing must not exceed 65% of any strategic raw material, processors diversify feedstock channels, raising demand for modular equipment that can switch between ores without lengthy refurbishments. Vendors offering plug-and-play drives, variable-frequency screens, and digital twins position themselves to capture early-mover contracts under the Act’s public-interest designation.

Circular-economy Push Driving Secondary-raw-material Processing

An annual target of construction and demolition waste spurs mobile crushers sales with power-optimized jaws and on-board optical sorters. AI-guided disassembly lines separate printed circuit boards, unlocking critical metals whose spot prices often outstrip virgin-ore equivalents. Studies by Agora Energiewende show that maximizing recycling could shave 26% off Germany’s total energy-transition cost by 2050, giving policymakers fiscal headroom to raise investment subsidies for waste-to-resource plants. Equipment builders respond with electrodynamic fragmentation systems that liberate embedded metals at sub-millimeter precision while consuming 30% less electricity than legacy hammer mills. Operators view circular-economy compliance as an insurance policy against feedstock volatility, steering capex toward versatile crushers, shredders, and sensor-based separators compatible with heterogeneous waste streams.

Digitally Integrated Plants Enabled by Industrie 4.0 Adoption

Mining companies embed Industrial IoT sensors across crushers, conveyors, and grinding circuits to capture vibration, temperature, and power-draw data every second[1]“REWO-SORT: AI-Enhanced Mineral Sorting,” Fraunhofer Institute, fraunhofer.de. Cloud dashboards detect performance drift and trigger predictive maintenance well before mechanical failure, cutting unplanned downtime by up to 18%. Digital twins replicate entire processing lines, allowing engineers to model throughput impacts of ore-grade fluctuations without halting production. AI-driven sorters like those trialed in the REWO-SORT project combine laser-induced plasma spectroscopy with multi-energy X-ray imaging to boost rare-earth recovery rates above 95% while trimming reagent consumption. As labor shortages deepen, plant managers favor software interfaces that integrate with existing ERP suites and permit remote control from centralized operation centers. Vendors that bundle equipment with cybersecurity-hardened gateways and open-standard communication protocols win share because buyers fear vendor lock-in on proprietary platforms and escalating integration costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Costs | -1.3% | National, industrial regions | Short term (≤ 2 years) |

| Stringent EU Environmental and Permitting Regulations | -0.9% | EU-wide, Germany compliance focus | Long term (≥ 4 years) |

| Skilled Labor Shortages | -0.8% | National, manufacturing clusters | Medium term (2-4 years) |

| Raw-Material Price Volatility | -0.7% | Global impact, Germany exposure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy Costs Following Coal-Power Phase-out

Forty percent of German industrial firms weighed production cuts or relocation amid the 2022 energy-price spike, and many have not reversed those plans despite recent market stabilization[2]“Energy Data: National and International Development,” Federal Ministry for Economic Affairs and Climate Action, bmwk.de. The mandatory closure of all coal-fired plants by 2038 imposes transition costs estimated at EUR 69 billion – EUR 93 billion on affected regions. Energy-intensive mineral processors face compound headwinds: electricity tariffs remain around one-fifths above the EU average, and hydrogen supplies are still scarce outside pilot clusters. Operators prioritize energy-efficient comminution circuits and variable-speed drives, accepting higher upfront prices for life-cycle savings. Vendors that certify mill liners, screens, and pumps for low-specific-energy consumption gain competitive ground, while those reliant on high-carbon power struggle to justify operating expenditure projections in tender evaluations.

Skilled Labor Shortages in Mechanical & Mechatronic Trades

Roughly three lakh machinery-sector employees will retire by 2034, leaving a decent vacancies that Germany’s current education pipeline cannot fill. The Federal Employment Agency already lists 183 occupations with acute shortages, notably in process engineering, industrial IT, and construction planning. Mineral processing plants, many located in rural areas, find it difficult to lure young technicians who prefer urban technology jobs. Maintenance backlogs lengthen, forcing operators to extend service intervals and accept higher breakdown risk. Some firms rehire retirees part-time or lobby for relaxed immigration rules, yet administrative barriers slow foreign credential recognition. Equipment builders react by integrating augmented-reality service modules and self-diagnosing control firmware that reduce the need for on-site specialists. Fully automated packages that arrive pre-calibrated and require only remote software updates are marketed as “future-proof” solutions to the labor crunch, commanding price premiums of up to 12%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Critical-Material Processing Redefines Portfolio

Potash & salt processing generated the largest share of Germany's mineral processing equipment market revenue at 29.15% in 2024, underpinned by fertilizer demand from Lower Saxony and Saxony-Anhalt. Lithium operations, however, are pacing the market with a 5.71% CAGR, reflecting ramp-ups at the Zinnwald and Bitterfeld plants that will jointly yield thousand of tons of lithium hydroxide annually by 2030. Therefore, the German mineral processing equipment market size for lithium is expected to widen considerably as geothermal brines in northern Germany unlock recoverable lithium, enough to supply battery cell factories in Thuringia and Brandenburg. Iron processing retains baseline demand tied to green steel investments, while interest in rare-earth separation grows under EU supply-diversification mandates. Secondary-bauxite projects concentrate on alumina recovery from red-mud stocks and recycled scrap, consistent with Germany’s circular-economy trajectory.

Operators allocate capex toward modular autoclaves, rotary kilns, and solvent-extraction circuits that can handle virgin ores and secondary feeds without lengthy retooling. Vendors bundle calcining furnaces for lithium with off-gas scrubbers to capture HF emissions and meet EU chemical safety norms. Potash processors upgrade crystallizers with heat-recovery loops, lowering steam consumption by up to 22%. Rare-earth refiners test ion-exchange resins tuned for dysprosium and neodymium separation, reducing acid consumption and wastewater volumes. Equipment suppliers that deliver turnkey packages, including design, installation, and guaranteed uptimes, are favored as mine developers race to meet project deadlines tied to EU milestone funding tranches.

By Equipment Type: Automation Upscales Material Handling

Crushers held 25.47% of Germany's mineral processing equipment market share in 2024 as urban demolition projects generated million of tons of rubble needing size reduction. The Germany mineral processing equipment market size for conveyors is expanding fastest at a 5.75% CAGR, propelled by demand for high-speed, low-energy belt and pipe systems equipped with predictive-maintenance sensors. Next-generation conveyor drives use synchronous reluctance motors that trim power draw by 8% versus induction equivalents, prized in a high-electricity-price environment. Screens & separators integrate high-frequency decks and ultrasonic de-blinding modules, elevating throughput of fine products such as battery-grade lithium hydroxide. Grinding-mill vendors shift toward vertical-roller designs that cut specific energy by 15%, a deciding factor for plant operators under pressure to offset escalating utility bills.

Battery-electric drills and breakers are gaining traction as mine operators chase zero-emission targets. Sandvik’s DD422iE electric jumbo, already trialed in Finland, is now marketed to German underground lithium developers with claims of 56% lower ventilation costs. In the “Others” category, electrodynamic fragmentation units offer new revenue streams by recovering precious metals from ceramic substrates, a niche previously served only by chemical leaching. Equipment integrators bundle SCADA interfaces that plug into cloud analytics suites. This creates a data loop calibrating crusher gap settings or conveyor speeds based on real-time ore hardness and moisture inputs.

By Mining Method: Underground Projects Stage a Comeback

Surface operations contributed 76.13% of Germany's mineral processing equipment market activity in 2024, a legacy of open-pit lignite mines in the Rhenish and Lusatian basins. Underground mining, however, registers the briskest expansion at a 5.84% CAGR as deep-lithium and polymetallic ore bodies in Saxony and Thuringia become financially viable. The German mineral processing equipment market size for underground methods gains tailwinds from stricter surface-disturbance rules that make subsurface extraction politically preferable. Battery-electric LHDs and autonomous drilling rigs reduce diesel particulate emissions, addressing resident concerns about air quality and mine-ventilation cost.

Digital-twin software maps geotechnical conditions at centimeter resolution, allowing engineers to pinpoint stope dimensions and equipment deployment sequences that optimize ore recovery. Real-time positioning systems guide haulers through narrow tunnels, shrinking cycle times, and cutting maintenance induced by operator error. Processing circuits installed beside portals pre-concentrate ore, minimizing waste transport to surface stockpiles. Vendors that customize compact crushers, modular thickeners, and stackable tailings filters for underground commissioning gain an edge as project sponsors prioritize tight footprints and rapid relocatability.

By Automation Level: Fully Autonomous Lines Surge Ahead

Semi-automated configurations accounted for 48.17% of Germany's mineral processing equipment market share in 2024, reflecting operators’ reliance on skilled technicians to oversee critical settings while leveraging PLC-controlled drives for routine tasks. Fully automated plants show the steepest growth, clocking a 5.88% CAGR through 2030, as demographic pressures and safety mandates converge. Manual plants retain niche roles in pilot testing and artisanal operations but face obsolescence in large-scale projects tied to EU financing that conditions approval on digital-monitoring capabilities.

Manufacturers integrate edge-computing modules that allow equipment to execute critical safety functions offline if network links fail. Remote-update architectures ensure cybersecurity patching without halting production, an attribute prized by utilities whose insurers now audit OT security compliance annually. Liebherr’s record deal to supply 360 battery-electric trucks and 55 electric excavators to Fortescue underscores the market’s pivot toward autonomous, emission-free fleets that dovetail with fully digital process plants. Equipment warranties increasingly bundle software-as-a-service clauses, creating recurring revenue streams for vendors and simplifying upgrade paths for operators.

Geography Analysis

Germany absorbs more than three-fifths of mineral processing equipment shipped into the EU, making it a self-contained demand center shaped by regional industrial profiles. Eastern states, notably Saxony and Thuringia, anchor new critical-material hubs in coal-transition funds, turning former lignite towns into lithium-refining strongholds. The Lusatia region’s “Net Zero Valley” plan attracts vendors of hydrogen-compatible pelletizers and low-carbon calcining kilns, anticipating renewable-powered grids supporting high-temperature processes. North Rhine-Westphalia maintains its status as a steel-processing powerhouse; ThyssenKrupp’s direct-reduction plant in Duisburg will need tailor-made equipment for hot-briquetted iron handling and smelter off-gas recycling.

Lower Saxony and Saxony-Anhalt continue to underpin demand for crushers and brine-evaporation systems through mature potash & salt operations. Lithium-rich brines near Hanover amplify orders for geothermal-well pumps and crystallizers adaptable to varying brine chemistries. Bavaria and Baden-Württemberg host clusters of control-system developers and precision gear-box makers, fostering region-specific upgrades in smart drives and IoT sensors. Their universities supply R&D collaboration that accelerates the commercialization of AI-enhanced sorters and laser-induced breakdown analyzers.

Cross-border cooperation with Poland and Czechia under the EU Critical Raw Materials corridors creates scope for shared processing infrastructures. Concentrates mined in Lower Silesia traverse short rail links to German plants where clean electricity levels CO₂ footprints below EU taxonomy thresholds, an advantage in green-bond financing. Equipment suppliers gain from harmonized CE-marking rules that reduce certification costs for multi-country deployments. However, tight environmental permitting in Germany incentivizes some junior miners to pre-process ore abroad, exporting semi-finished products for final refining in German facilities that already meet stringent wastewater and emission norms.

Coverage of the mineral processing equipment market by Mordor Intelligence spans a wide geographic footprint, with detailed country-level intelligence for Spain, Turkey, South Korea, Argentina, Japan, Mexico, Oman, Egypt, and Morocco, each shaped by local operating conditions.

Competitive Landscape

Market concentration is mid-range as global OEMs such as Metso, FLSmidth, and Sandvik vie with German stalwarts like ThyssenKrupp Polysius and RHEWUM. Leading players combine complete equipment portfolios with local service centers, which is crucial in a market where unplanned downtime can breach EU emission permits and trigger stiff fines. Technology partnerships proliferate: Metso teams with Siemens to integrate variable-speed drives into high-pressure grinding rolls, while Sandvik licenses machine-learning software from a Berlin startup to optimize bit wear in underground drills. Circular-economy specialization spawns new entrants—AI-sorter companies and electrodynamic fragmentation providers—who carve out niches by solving processing challenges unique to secondary feeds.

Acquisition activity intensifies as incumbents seek digital competencies. In 2024, a prominent German sensor firm acquired a mid-sized crusher maker to embed vision analytics directly onto primary crushers, reducing downstream screening loads. Service contracts shift toward outcome-based models where vendors guarantee throughput levels or energy savings; failure to meet KPIs triggers fee rebates. Skilled-labor shortages elevate the value of plug-and-play modular plants that arrive pre-wired and pre-tested, reducing on-site commissioning timelines. OEMs with robust training portals and augmented-reality troubleshooting apps gain loyalty from operators struggling to recruit millwrights and electricians.

Enhanced after-sales support becomes a competitive lever. Predictive-maintenance algorithms that slash bearing failure incidents by two-fifths become standard in tender documents. Vendors unable to offer digital twins and emissions-tracking dashboards risk exclusion from EU-funded projects whose environmental-social-governance metrics require real-time data feeds. As regulatory deadlines loom, buyers converge on suppliers whose roadmaps align with zero-emission mining and full traceability of input materials.

Germany Mineral Processing Equipment Industry Leaders

Metso Outotec

Sandvik AB

FLSmidth A/S

Weir Group PLC

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The European Commission confirmed 47 Critical Raw Material Strategic Projects, allocating EUR 22.5 billion and granting several German lithium, rare-earth, and recycling ventures accelerated permitting.

- November 2024: Thyssenkrupp Steel unveiled a plan to cut steel output to 8.7-9 million t while committing to carbon-neutral production by 2030, signaling demand for low-carbon pelletizing and smelting equipment.

- September 2024: Liebherr and Fortescue expanded their zero-emission partnership, covering 475 battery-electric haul trucks and excavators—the largest deal in Liebherr’s history.

Germany Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Potash & Salt |

| Rare Earths |

| Crushers |

| Feeders |

| Conveyors |

| Drills & Breakers |

| Screens & Separators |

| Grinding Mills |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Potash & Salt | |

| Rare Earths | |

| By Equipment Type | Crushers |

| Feeders | |

| Conveyors | |

| Drills & Breakers | |

| Screens & Separators | |

| Grinding Mills | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

What is the current value of the German mineral processing equipment market?

The market stands at USD 167.09 million in 2025 and is forecast to reach USD 220.35 million by 2030.

Which mineral segment is expanding fastest in Germany?

Lithium processing is clocking a 5.71% CAGR through 2030 thanks to new projects in Saxony and Bitterfeld.

How are high energy prices influencing equipment purchases?

Operators favor energy-efficient crushers, conveyors, and vertical-roller mills that lower electricity consumption across plant lifecycles.

What role does automation play in new mineral processing plants?

Fully automated lines featuring AI-driven control loops are growing at a 5.88% CAGR as companies tackle labor shortages and safety standards.

Which regions within Germany are seeing the most new mineral processing investment?

Saxony, Thuringia, and the Lusatia coal-transition area attract capital for lithium, rare-earth, and recycling facilities.

How is the EU Critical Raw Materials Act affecting equipment demand?

Strategic Project status accelerates permitting and guarantees offtake, driving early procurement of modular, digitally integrated processing equipment.

Page last updated on: