Brazil Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

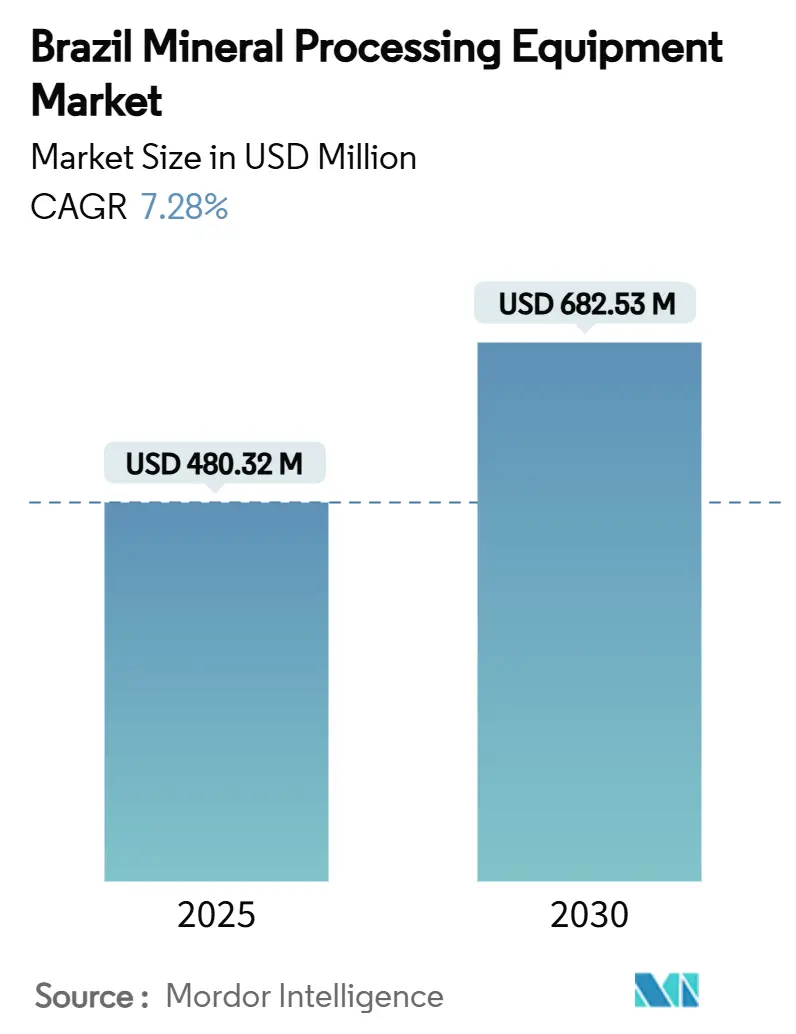

| Market Size (2025) | USD 480.32 Million |

| Market Size (2030) | USD 682.53 Million |

| Growth Rate (2025 - 2030) | 7.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Brazil mineral processing equipment market stood at USD 480.32 million in 2025 and is projected to reach USD 682.53 million by 2030, translating into a 7.28% CAGR through the forecast period. Accelerated investment under the government’s Nova Indústria Brasil financing window, a steep rise in iron-ore export volumes, and the rapid build-out of lithium conversion projects collectively underpin solid medium-term demand for comminution, classification, and concentration systems. Automation retrofits that lift throughput and cut maintenance downtime, plus ESG-linked credit that lowers the cost of capital for “green” plants, are widening the addressable base of buyers across both tier-one and mid-tier miners. Competitive positioning favors suppliers that can pair high-capacity surface-mining equipment with digital-twin control platforms. At the same time, a shortage of OT-cyber talent restrains smaller operators from moving beyond manual or semi-automated modes. Delivery lead times remain volatile because inland logistics depend heavily on road freight, yet proactive localization by leading manufacturers is easing parts availability and field-service response.

Key Report Takeaways

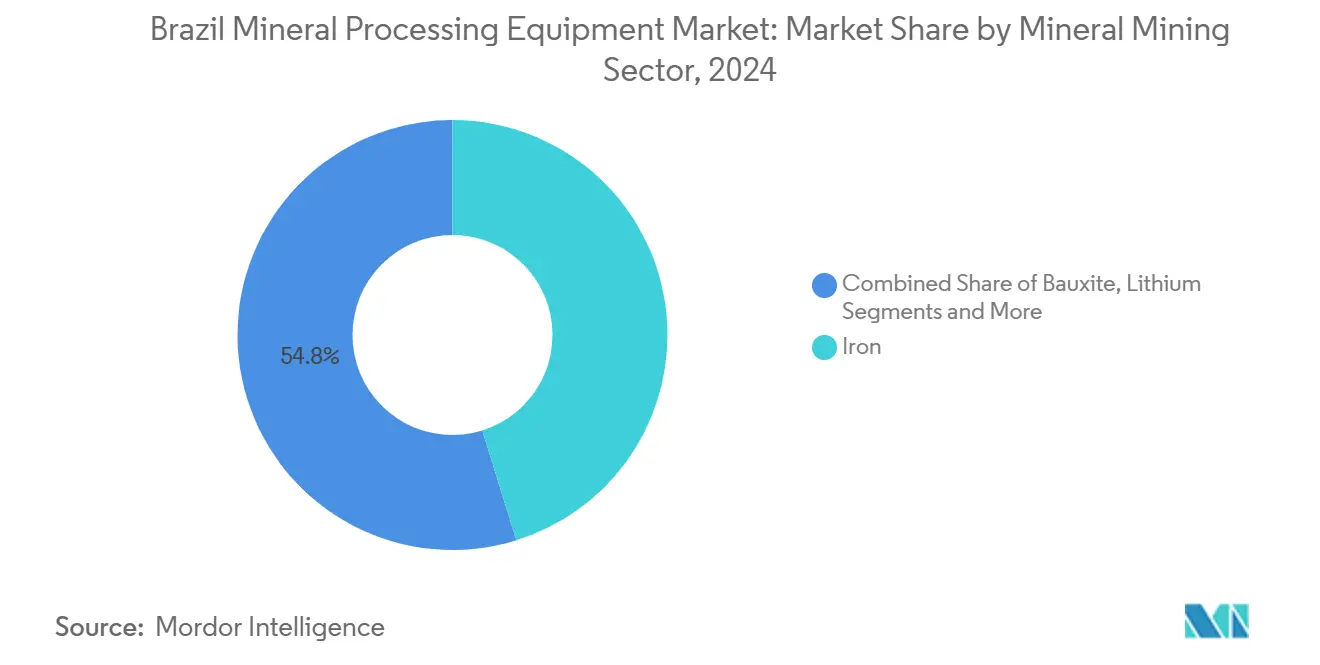

- By mineral mining sector, iron-ore retained 45.19% of Brazil mineral processing equipment market share in 2024, whereas lithium processing equipment is advancing at a 12.26% CAGR to 2030.

- By equipment type, crushers led with 25.38% revenue share in 2024; flotation cells are forecast to post the fastest 9.23% CAGR through 2030.

- By mining method, surface operations commanded 74.26% of the Brazil mineral processing equipment market size in 2024, while underground equipment is expanding at an 11.28% CAGR between 2025-2030.

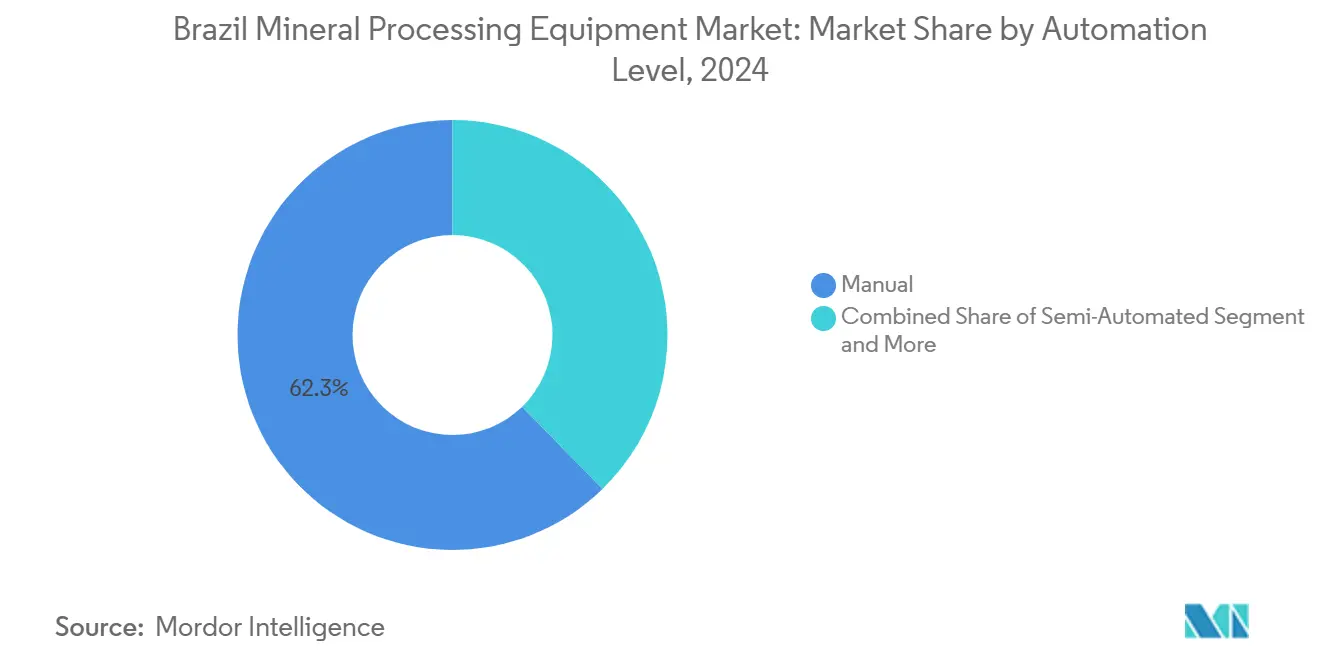

- By automation level, manual systems still held 62.28% share of the Brazil mineral processing equipment market size in 2024, yet fully automated plants are set to grow at 11.72% CAGR to 2030.

- By geography, the Southeast region accounted for 41.19% share of the Brazil mineral processing equipment market in 2024; the North is projected to grow the fastest at an 8.84% CAGR over 2025-2030

National developments in Brazil connect differently with activity unfolding across other parts of the world. In the global mineral processing equipment market coverage, Mordor Intelligence integrates these into a single analytical framework.

Brazil Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mineral output surge | +2.1% | Southeast, North, Center-West | Medium term (2-4 years) |

| Fast-track incentives | +1.8% | National, early gains in Minas Gerais & Pará | Short term (≤ 2 years) |

| Critical-mineral demand | +1.5% | Global spill-over to Southeast & North | Long term (≥ 4 years) |

| Automation OPEX cuts | +1.2% | Southeast core, expansion to North | Medium term (2-4 years) |

| ESG finance boost | +0.9% | National, concentration in Southeast | Long term (≥ 4 years) |

| Tailings-safety rules | +0.7% | National priority in Southeast | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

Increasing Mineral Production Volumes Drive Equipment Modernization

Vale targets iron-ore output of 340-360 million t by 2026, lifting demand for high-capacity crushers, HPGRs, and stacker-reclaimers that can operate reliably at 8,000 t h−1 cycles[1]"Production and Sales Report Q1-2025,", Vale S.A., vale.com. Lithium shipments turned Brazil into the world's fifth-largest exporter in 2024, catalyzing the procurement of spodumene flotation cells, dense-media separators, and hydrometallurgical reactors for lithium-carbonate lines. Samarco's pellet and fines production soared in the first half of 2025. In H1 2025, Samarco's pellet and fines output rose 64 percent from the same period in 2024 to 7.1 million metric tons, illustrating how restart programs quickly translate into grinding mill and induration furnace orders worth hundreds of millions. The production push is broad-based, spanning copper, nickel, and bauxite, and compels operators to prioritize mean-time-between-failure metrics ahead of lowest-capex considerations

Government Policy Framework Accelerates Equipment Deployment

The BRL 300 billion Nova Indústria Brasil facility earmarks concessional credit for modern comminution and classification lines and local assembly plants, trimming typical payback periods by up to 18 months for tier-one miners[2]“Nova Indústria Brasil Policy Decree,”, Government of Brazil, gov.br. With 56 strategic mineral projects short-listed for BNDES lending, OEMs see predictable pipelines for both brownfield revamps and greenfield hubs, particularly in Pará and Minas Gerais.

ESG-Linked Financing Lowers Cost of Capital for “Green” Plants

In 2024, sustainability-linked loans indexed to Scope 1+2 emission reduction targets lowered average borrowing costs for Brazilian iron-ore producers. Equipment packages featuring high-efficiency motors, dry-stack tailings filters, and regenerative conveyor drives often qualify for these preferential rates, shifting purchase decisions toward mid-premium technology tiers. The trend is particularly pronounced in the Southeast, where large ESG-oriented funds are headquartered and strict screening protocols are maintained.

Mandatory Tailings-Dam Safety Upgrades Boost Equipment Orders

The post-Brumadinho regulation requires the decommissioning of all upstream dams by 2035. Operators are replacing wet tailings circuits with paste-thickening, deep-cone cycloning, and dry-stack filters. The retrofit wave is front-loaded because insurers apply premium surcharges on upstream-dam operations beginning in 2027, prompting accelerated capex in the short term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter licensing & carbon tax | −1.4% | National, concentration in Southeast | Medium term (2-4 years) |

| Rail/port bottlenecks | −0.8% | National, acute in Southeast & North | Long term (≥ 4 years) |

| High power tariffs | −0.6% | Nationwide, most severe in Southeast | Short term (≤ 2 years) |

| OT-cyber talent gap | −0.4% | National, critical in Southeast & North | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Industrial Electricity Tarrifs vs. Global Peers

In December 2024, Brazil's industrial electricity price averaged 877 Brazilian reals per megawatt-hour. The peak price was reached in October of the same year, at 925 Brazilian reals per megawatt-hour. Projects are staggering mill-start sequences to off-peak hours, yet this compresses daily processing windows and inflates equipment sizing requirements, raising capex per installed tonne.

Acute Shortage of OT-Cyber-Skilled Technicians

Full-stack automation requires specialists who can integrate PLCs, historian databases, and AI-enabled analytics. Brazil’s vocational pipeline produces low industrial automation graduates annually against mining demand, creating a talent gap that lengthens commissioning schedules by several quarters. Contractors respond by structuring long-term service agreements where OEMs embed their own staff on-site, effectively altering project economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Iron Dominance Faces Lithium Disruption

Iron ore accounted for 45.19% of Brazil's mineral processing equipment market share in 2024 on the back of 389 million t exports. The Brazil mineral processing equipment market size linked to iron flowsheets is expected to expand steadily but more slowly than critical-mineral circuits over the next five years. Lithium equipment demand, growing at a 12.26% CAGR, benefits from Sigma Lithium’s Phase 3 expansion and Companhia Brasileira de Lítio’s planned doubling of spodumene output. Bauxite and nickel retain mid-single-digit growth driven by aluminum sheet demand and EV-battery precursor projects. The inauguration of Aclara’s rare-earth pilot plant signals nascent categories requiring proprietary separation equipment that incumbents want to license locally.

Moving forward, iron-ore majors are pivoting toward dry concentration pathways to eliminate tailings dams; hence, investments will migrate from wet scrubber-cyclone clusters to air-separator skids. Though fewer in number, lithium brine conversion lines require high-purity crystallizers and triple-effect evaporators priced at USD 20-25 million each, quickly diluting iron’s share of the total Brazil mineral processing equipment market. Copper and nickel flowsheets increasingly integrate pressure-oxidation autoclaves and bio-leach reactors, elevating the technical bar for would-be entrants and reinforcing the premium charged by established high-temperature metallurgy suppliers

By Equipment Type: Crushers Lead While Flotation Cells Accelerate

Crushers held a 25.38% share of the Brazilian mineral processing equipment market in 2024 because every greenfield and brownfield line starts with primary size reduction. Cone-crusher upgrades that lift power draw above 1,200 kW are particularly sought in Carajás and Quadrilátero Ferrífero pits. Flotation cells are set for a 9.23% CAGR through 2030, fueled by the need to liberate finely disseminated lithium and copper minerals. Meanwhile, high-pressure grinding rolls penetrate hematite upgrades where water scarcity constrains conventional SAG-mill throughput.

Suppliers differentiate on wear-surface metallurgy, plug-and-play sensors, and reagent-optimization algorithms. FLSmidth’s next-generation gMAX hydrocyclones, for instance, increase sharpness of cut while lowering feed-pressure requirements, enabling smaller pump drives and saving 750 MWh annually per line. Tailings filtration has moved from niche to mainstream: each 35,000 t/d iron-ore concentrator now budgets USD 80-90 million for plate-press trains alone.

By Mining Method: Surface Operations Dominate Underground Growth

Surface mines generated 74.26% of Brazil mineral processing equipment market revenue in 2024, as Carajás, S11D and Itabira continue to rely on truck-shovel and in-pit crushing-and-conveying systems capable of 12,000 t h−1. Yet underground equipment is expected to clock an 11.28% CAGR assisted by deeper iron-ore stopes at Mariana and high-grade copper projects such as Vale’s Alemão deposit. The transition invites fleets of 35-t load-haul-dumpers, narrow-vein jumbo drills and sophisticated ventilation on-demand systems.

Autonomy is underpinning the cost curve for underground fleets. Jaguar Mining’s use of ExynAero drones to scan voids eliminates manual cavity monitoring that previously halted mucking for two hours per shift. Komatsu’s GHH acquisition adds low-profile loaders and scalers to address Brazil’s sub-3.5 m back heights. Surface players still outspend on IPCC and overland conveyors, but incremental brownfield expansions are slowing; thus relative wallet share will tilt toward underground technologies as resource depth increases

By Automation Level: Manual Operations Persist Despite Automation Surge

Manual plants comprised 62.28% of the Brazil mineral processing equipment market in 2024, largely because hundreds of mid-tier quarries and gold operations lack the capital expenditure to adopt robotics. However, the fully automated segment is tracking an 11.72% CAGR as Vale, Anglo American, and Samarco roll out fleet management, process control, and AI optimization layers. The Brazil mineral processing equipment market size tied to automated platforms is, therefore, growing almost twice as fast as the overall base.

Safety mandates reinforce automation economics. Remote operating centers in Belo Horizonte now control unmanned shovels 1,500 km away in Pará, reducing lost-time injuries and securing insurance discounts. Yet a chronic shortage of OT-cyber specialists triggers vendor-managed service models, where OEMs own uptime guarantees and absorb cyber-hardening liabilities. Small operators continue to favor manual setups but are adopting sensor kits that can be retro-fitted to legacy mills, effectively creating a staged journey toward autonomy.

Geography Analysis

The Southeast commanded 41.19% of the Brazil mineral processing equipment market in 2024 because Minas Gerais hosts the Quadrilátero Ferrífero iron belt plus clusters of lithium, gold and phosphate assets that together draw continuous brownfield capex. The region benefits from dual-track highways to Porto de Vitória and solid grid interconnectivity that simplifies installation of high-reliability SAG drives. Environmental scrutiny after the Brumadinho disaster is tightening tailings rules but simultaneously driving adoption of dry-stacking technologies, sustaining fresh demand for paste thickeners and belt-filter presses.

The North is projected to register the highest 8.84% CAGR to 2030, anchored by Vale’s project to lift Carajás output to 230 Mt y−1 and by new copper-gold deposits in Pará. Railway duplication on the Carajás Corridor eases inbound delivery of mill shells exceeding 300 t each, encouraging OEMs to pre-position laydown yards at Marabá. The Amazon biome presents ESG and community-approval hurdles; hence, suppliers embed life-cycle analysis and renewable-power sourcing to meet procurement scorecard thresholds.

The Northeast, South and Center-West collectively form a secondary equipment cluster. Bahia’s Ilhéus corridor is emerging as a lithium hub, stimulating orders for spodumene concentrators and calcining kilns. The South sustains moderate equipment replacement cycles for coal and industrial minerals, while the Center-West’s phosphate and potash mines underpin sales of attrition scrubbers and rotary dryers critical to fertilizer feedstocks. As infrastructure upgrades disperse economic activity, the Brazil mineral processing equipment market will see a more regionally balanced revenue profile.

For the mineral processing equipment market, country-specific intelligence is available for Argentina, Mexico, China, Canada, Germany, France, Spain, South Korea, and Turkey, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The Brazil mineral processing equipment market remains moderately fragmented. The major OEMs—Metso, FLSmidth, Caterpillar, Komatsu, and ABB—control new equipment and Tier-1 service contracts. Metso generated 23% of its EUR 4.8 billion 2024 sales in South America, supported by its Belo Horizonte performance center that assembles cone crushers and screens for local delivery. FLSmidth posted a 4% rise in mining-service revenue during Q1 2025, signaling a pivot away from cyclical capex cycles toward annuity-style spares and optimization work[3]“Q1-2025 Interim Report,”, FLSmidth, flsmidth.com.

Strategic moves are reshaping competition. Komatsu’s 2024 acquisition of GHH brings low-profile underground loaders into its Brazil catalog, positioning it against Sandvik and Epiroc in deep-level stopes. Caterpillar unveiled Dynamic Energy Transfer modules for trolley-assist haul-trucks, aligning with miners’ Scope 1 reduction pledges. ABB locked a multi-year global framework with BHP covering automation and electrification, giving it a pipeline for gearless-drive retrofits in Brazilian concentrators. Local automation integrators such as Torsi-Tec and Actemium are gaining share in plant-wide digital-twin deployments, forcing traditional OEMs to open API gateways or risk lock-out from integrated bids.

Sustainability credentials increasingly decide tender outcomes. Suppliers offering lifecycle LCA data, recyclable wear-parts, and renewable-powered service centers hold an edge with ESG-conscious miners who signal carbon-aligned procurement preferences to lenders. Market depth, therefore, favors providers that can bundle equipment, software, and on-site technicians into outcome-based contracts.

Brazil Mineral Processing Equipment Industry Leaders

-

Metso Outotec

-

FLSmidth A/S

-

Sandvik AB

-

The Weir Group PLC

-

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Vale confirms plans to eliminate water use in Carajás iron-ore processing by 2027, triggering large-scale investment in dry crushing and screening technologies.

- June 2025: Viridis Mining secures funding for its Colossus rare-earth project, paving the way for proprietary separation-equipment orders.

- April 2025: Aclara Resources inaugurates Brazil’s first heavy rare-earth pilot plant, requiring magnetic and solvent-extraction systems.

Brazil Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Nickel |

| Copper |

| Others |

| Crushers |

| Feeders |

| Conveyors |

| Grinding Mills |

| Screening & Classification |

| Flotation Cells |

| Magnetic & Gravity Separators |

| Tailings Management Systems |

| Drills & Breakers |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| North |

| Northeast |

| Southeast |

| South |

| Center-West |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Nickel | |

| Copper | |

| Others | |

| By Equipment Type | Crushers |

| Feeders | |

| Conveyors | |

| Grinding Mills | |

| Screening & Classification | |

| Flotation Cells | |

| Magnetic & Gravity Separators | |

| Tailings Management Systems | |

| Drills & Breakers | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated | |

| By Region | North |

| Northeast | |

| Southeast | |

| South | |

| Center-West |

Key Questions Answered in the Report

What is the forecast value of the Brazil mineral processing equipment market by 2030?

The market is projected to reach USD 682.53 million by 2030, growing at a 7.28% CAGR.

Which equipment category will grow the fastest through 2030?

Flotation cells are expected to post a 9.23% CAGR, the quickest among all equipment types.

Why is the North region considered the fastest-growing demand center?

Vale’s Carajas expansion, new copper and gold deposits, and railway upgrades position the North for an 8.84% CAGR in equipment demand.

How are ESG requirements influencing equipment procurement?

Sustainability-linked loans and stricter tailings regulations push operators to adopt dry-stack filters, energy-efficient drives and low-emission autonomous fleets.

Which mining method segment offers the strongest growth outlook?

Underground mining equipment is forecast to grow at 11.28% CAGR as surface deposits deplete and deeper orebodies are developed.

Page last updated on: