Australia Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

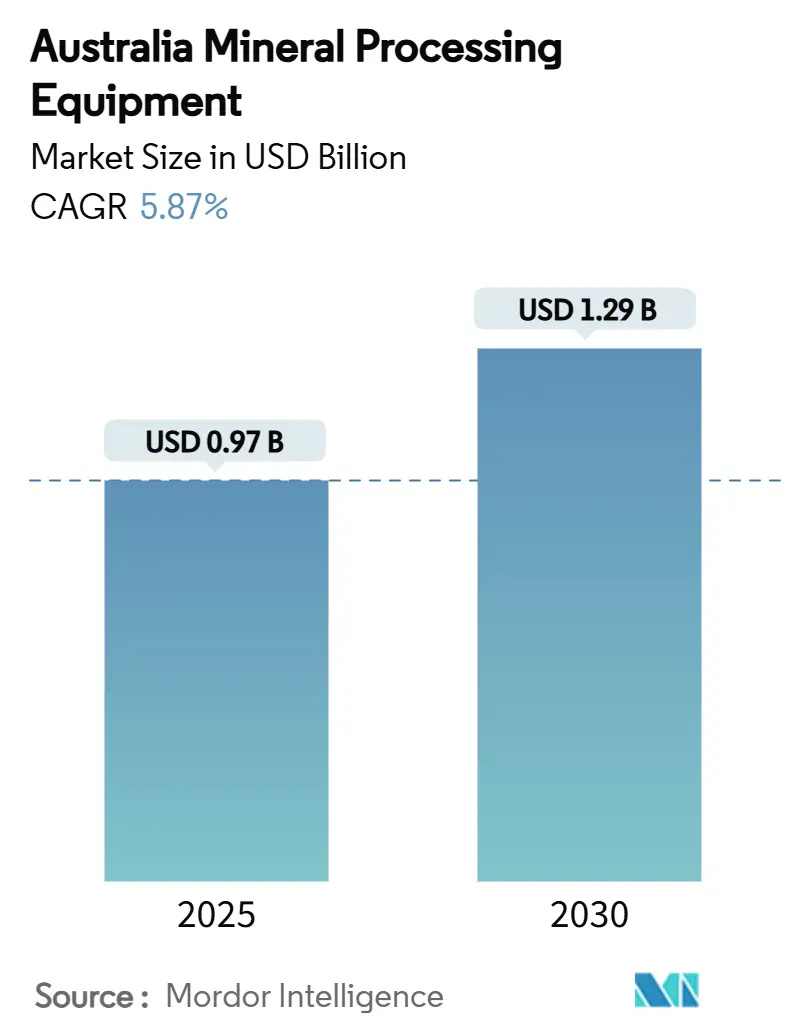

| Market Size (2025) | USD 0.97 Billion |

| Market Size (2030) | USD 1.29 Billion |

| Growth Rate (2025 - 2030) | 5.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Australia Mineral Processing Equipment Market size is estimated at USD 0.97 billion in 2025, and is expected to reach USD 1.29 billion by 2030, at a CAGR of 5.87% during the forecast period (2025-2030). The core growth pillars include sustained replacement spending on Pilbara iron-ore circuits, rising demand from battery-mineral concentrators, and policy support under the Future Made in Australia (FMIA) program. Suppliers prioritize robust crushers that handle abrasive iron ore, but filtration systems for drier tailings are gaining momentum as federal regulators tighten waste-storage rules. Investments in semi- and fully-automated equipment continue as labor shortages in remote Western Australia persist, while energy-efficient grinding technologies offset rising electricity tariffs. Competitive pressure from lower-cost Chinese OEMs forces global brands to differentiate through local service hubs, modular plant designs, and digital optimization add-ons.

Key Report Takeaways

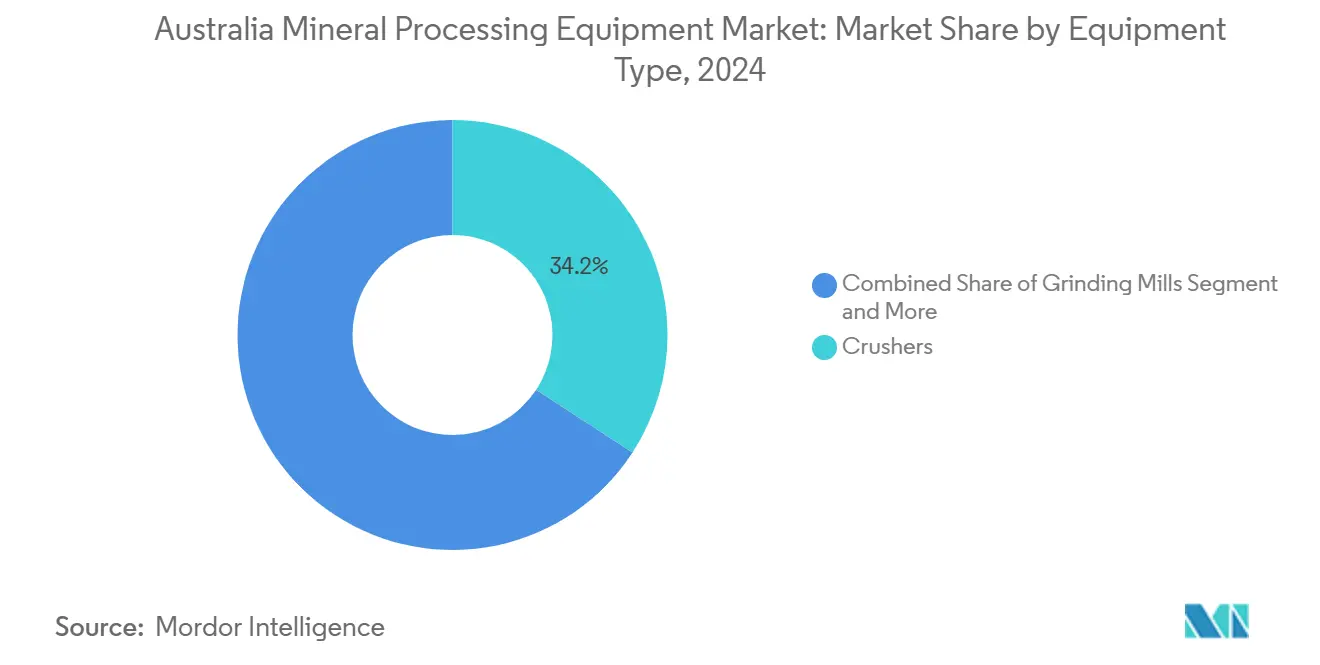

- By equipment type, crushers led with 34.17% revenue share in 2024; dewatering and tailings equipment is projected to expand at a 5.91% CAGR through 2030.

- By mineral commodity, iron ore processing held a 45.13% share in 2024; lithium processing equipment is forecast to grow at a 5.95% CAGR to 2030.

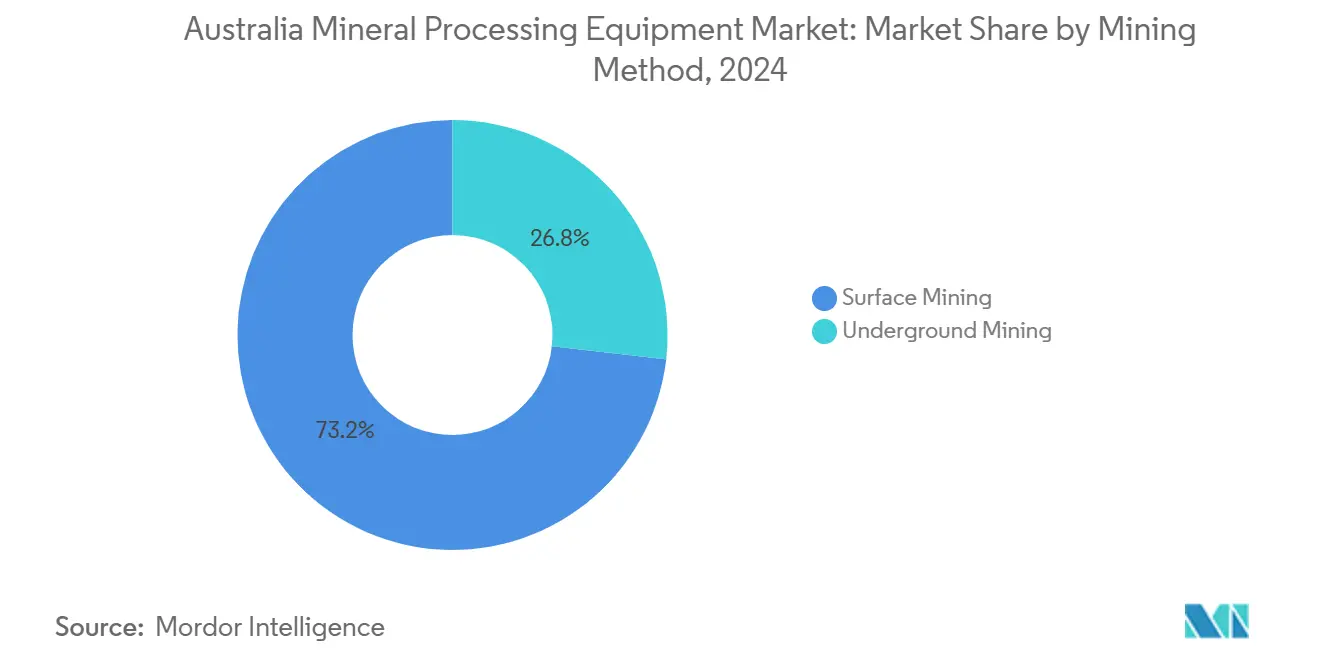

- By mining method, surface mining accounted for 73.24% of 2024 revenue; underground mining equipment is poised to advance at a 5.89% CAGR through 2030.

- By automation level, semi-automated systems captured 47.81% share in 2024; fully automated equipment is expected to register a 6.11% CAGR over 2025–2030.

Australia holds a defined position within a broader international distribution. The mineral processing equipment market share data by Mordor Intelligence maps that allocation across all contributing countries and regions, globally.

Australia Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Record Pilbara Iron-Ore Output Driving Replacement Capex | +1.2% | Western Australia Pilbara region | Medium term (2-4 years) |

| Battery-Mineral Boom Spurring New Concentrators | +0.9% | Western Australia, South Australia | Long term (≥ 4 years) |

| FMIA Incentives | +0.8% | National, with focus on WA and SA | Long term (≥ 4 years) |

| Stricter Tailings-Dam Rules | +0.7% | National, particularly WA and NSW | Medium term (2-4 years) |

| Sensor-Based Ore-Sorting Compressing Comminution | +0.6% | National, early adoption in WA | Medium term (2-4 years) |

| Indigenous Procurement Targets | +0.5% | National, concentrated in remote mining regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Record Pilbara iron-ore output driving replacement capex

Rio Tinto has allocated USD 1.8 billion to extend Brockman Syncline and USD 1.6 billion for Hope Downs 2 in 2025, replacing aging crushers, screens, and conveyors as existing assets near end-of-life in abrasive Pilbara conditions[1]“Brockman Syncline and Hope Downs 2 Investment Release,” Rio Tinto, riotinto.com.The demand concentration in a single region encourages OEMs to establish localized rebuild centers and inventory hubs, cutting lead times and boosting service revenue.

Battery-mineral boom spurring new concentrators

The Critical Minerals Production Tax Incentive that starts in 2027 is catalyzing lithium, nickel, and rare-earth concentrator builds, each requiring custom flotation cells, magnetic separators, and fine grinding mills[2]“LithSonic Low-Carbon Lithium Extraction Technology,” CSIRO, csiro.au. CSIRO’s LithSonic technology offers cleaner lithium extraction, underscoring the technical leap needed in new plants. Although Albemarle halted the third train at Kemerton, long-run EV adoption secures equipment demand.

FMIA incentives for on-shore processing

The FMIA package commits USD 22.7 billion over ten years, more than one-fifth is earmarked for critical-mineral processing, tilting project economics toward local value-adding plants. Eneabba will house the country’s first fully integrated rare-earth refinery, favoring modular circuits that are easier to fabricate domestically and install in remote sites.

Stricter tailings-dam rules boosting filtration demand

Regulators, responding to incidents such as the 2024 suspension at Newmont's Telfer mine, now mandate filtered tailings with over 80% water recovery. This shift has spurred a heightened demand for large-format filter presses and paste thickeners, which are critical for meeting these stringent requirements. Meanwhile, fines imposed at Cadia underscore the escalating compliance costs, prompting swift equipment retrofits to align with regulatory standards and avoid further penalties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Approval Delays | -0.4% | National, particularly NSW and Victoria | Medium term (2-4 years) |

| Rising Grid-Power Tariffs | -0.3% | National, acute in WA and SA | Short term (≤ 2 years) |

| Skilled-Trades Shortage | -0.2% | Western Australia, particularly Pilbara region | Medium term (2-4 years) |

| Price Pressure From Low-Cost Chinese OEMs | -0.1% | National, most acute in emerging market segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental approval delays

Victoria significantly raised mining fees, impacting the operational costs for mining companies. Meanwhile, community challenges, such as those encountered by the FI Joint Venture in Yalgoo, are extending permit cycles by as much as two years. These prolonged cycles stall equipment orders, disrupt supplier capacity planning, and create uncertainties in project timelines. As a result, OEMs are now compelled to factor in schedule risks or offer flexible delivery clauses to mitigate potential delays.

Rising grid-power tariffs for grinding circuits

CSIRO’s GenCost report shows around one-fifth uplift in electricity technology costs in recent years, with WA and SA mines paying the steepest tariffs. Operators are adopting on-site solar plus storage, meeting more than half of the average load, yet the CAPEX burden diverts funds from new mill installations. Suppliers offering high-pressure grinding rolls or hybrid-power crushers gain an edge as clients seek lower specific energy draws.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Crushers Anchor Spending while Tailings Drive Growth

Crushing systems accounted for 34.17% of the Australian mineral processing equipment market in 2024, underscoring their indispensable role in high-tonnage Pilbara iron-ore flowsheets. Rio Tinto’s Brockman Syncline plant includes a 34 million tpa primary crusher that epitomizes the throughput scale standard to the region. Grinding mills form the second-largest pool as miners pursue finer grind sizes to unlock grade uplift, especially in copper and gold circuits. Screens, feeders, and overland conveyors are integral to long-distance, mine-to-port logistics.

Demand for tailings-filtration units is expanding at a 5.91% CAGR, the fastest of all equipment groups. New thickener designs and large filter presses enable operators to meet dry-stack mandates and recycle process water, which is crucial in arid WA and NSW settings. Sensor-based sorting, automated samplers, and AI-driven analyzers represent emerging sub-segments as mines adopt Industry 4.0 workflows. This evolution signals a pivot from bulk handling toward smarter, water-conserving equipment suites that can satisfy both productivity and ESG goals.

By Mineral Commodity: Iron-Ore Rules as Lithium Accelerates

With 45.13% of the Australian mineral processing equipment market share in 2024, iron ore dominates procurement, propelled by Rio Tinto’s USD 13 billion spend to lift Pilbara capacity to 345–360 million tpy by 2027. Bauxite sits second thanks to substantial northern reserves, though miners lobby for its re-classification as a critical mineral to unlock FMIA funds. Copper appliances benefit from BHP’s plan to refine copper cathode in South Australia.

Lithium circuits register the quickest climb at 5.95% CAGR. Australia produced around two-fifths of global lithium in 2024, and the state's push for hydroxide refining plants ensures robust order books for specialized flotation, calcination, and crystallization lines, even after Kemerton scaled back. Nickel and rare-earth equipment add niche volumes, while tungsten and mineral-sands facilities broaden the commodity base and underpin supplier diversification.

By Mining Method: Surface Dominance with Underground Catch-Up

Surface operations captured 73.24% of the Australian mineral processing equipment market in 2024 as the Pilbara, Bowen Basin, and Hunter Valley rely on large-scale open pits, autonomous haulage, and in-pit crushing and conveying. Fortescue’s deal for 360 battery-electric trucks plus Caterpillar’s massive number of meters of autonomous drilling at Mt Arthur South reflect ongoing capex in surface fleets. Water- and energy-saving upgrades such as AI-controlled pumps continue to lower per-ton costs.

Underground equipment is growing at a 5.89% CAGR as ore bodies deepen. Newmont’s Tanami expansion will sink Australia’s deepest shaft at 1.5 km, driving orders for battery-electric loaders like Komatsu’s WX04B that cut diesel emissions and improve air quality. Underground machinery commands higher unit prices and presents technology showcase opportunities, attracting premium margins for OEMs.

By Automation Level: Semi-Automated Present, Fully Automated Future

Semi-automated rigs held 47.81% of the Australian mineral processing equipment market in 2024, balancing capital outlay with immediate productivity gains. Remote-operated drill rigs, AI-enabled predictive maintenance, and digital twins enhance availability without displacing entire crews, fitting current workforce transition plans.

Fully automated assets post the leading 6.11% CAGR as Australia now hosts several autonomous trucks, the largest global fleet. Rio Tinto’s Autonomy Program and Epiroc’s Fortescue order for autonomous electric drills show greenfield projects skipping the semi-stage. As edge computing and reliable LTE networks reach remote leases, entirely crew-free plants are expected to spread beyond iron ore into base metal and critical mineral hubs.

Geography Analysis

Western Australia dominates the Australian mineral processing equipment market, anchored by Pilbara iron ore and fast-growing battery-mineral hubs. Rio Tinto alone will channel USD 13 billion into the Pilbara region of Western Australia over the next three years. The state’s 2015 Code of Practice on autonomous mining tools fosters early uptake of driverless trucks and drills, positioning WA as a proving ground for cutting-edge processing trains.

South Australia is the next growth pole, leveraging BHP’s plan to refine a considerable amount of copper cathode annually and emerging rare-earth projects such as Eneabba. The FMIA’s critical-minerals incentives and a new state skills program combat labor shortages, making Adelaide a growing hub for engineering talent.

New South Wales and Queensland fill specialized roles: NSW hosts gold assets like the expanded Tanami operation. At the same time, Queensland supplies coal processors requiring heavy-duty screens and dense-medium cyclones, even as the state charts an energy-transition course. Victoria risks marginalization after hiking mining fees, a move industry groups predict will dampen exploration and equipment orders. Northern Territory and Tasmania remain small yet rising; the former benefits from greenfields critical-mineral finds, and the latter from mineral-sands upgrades that need compact, modular circuits.

Mordor Intelligence delivers a comprehensive view of the mineral processing equipment market with country-level analysis for South Korea, Japan, Germany, France, Spain, Argentina, Turkey, Mexico, and Oman, each offering a view of the local market realities.

Competitive Landscape

Competition is moderately fragmented. In high-volume product families such as crushers, mills, and screens, global incumbents Metso, FLSmidth, and Sandvik retain scale advantages, yet face price attacks from XCMG, CITIC Heavy, and other Chinese entrants. These challengers gained traction after agreements like BHP’s June 2025 partnership with XCMG for mining fleet solutions.

OEMs are countering by localizing service: Metso’s three-year liner contract with BHP establishes rapid-response WA repair centers, while Weir’s tie-up with De Grey Mining embeds HPGR specialists on site. Technology-led disrupters focus on niche steps, Gekko Systems launched the OLGA Mk3 inline gold analyzer and TOMRA dominates XRT sorters, creating segments where smaller firms can out-innovate giants[3]“OLGA Mk3 Online Gold Analyzer Launch,” Gekko Systems, gekkos.com .

Indigenous procurement adds another layer: miners spent a massive amount with First Nations businesses in 2024. Global brands increasingly form joint ventures or subcontract to Indigenous fabricators to qualify for bid lists, reshaping supply chains and driving modular plant adoption. Continued downward pressure on grinding power costs, tailings compliance, and autonomous fleet performance will define the next competitive battlegrounds.

Australia Mineral Processing Equipment Industry Leaders

Metso Corp.

FLSmidth A/S

Sandvik AB

Weir Group plc

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BHP signed agreements with CATL and BYD to deploy battery technology across heavy vehicles and stationary plant at Australian mine sites.

- June 2025: BHP partnered with XCMG to co-develop haulage and loading solutions tailored to Pilbara conditions, introducing additional Chinese competition into the market.

- June 2025: Rio Tinto and Hancock Prospecting approved USD 1.6 billion for Hope Downs 2, a 31 million tones Pilbara iron-ore mine requiring primary crushers, overland conveyors, and wet-plant upgrades.

Australia Mineral Processing Equipment Market Report Scope

| Crushers |

| Grinding Mills |

| Screening Equipment |

| Flotation & Separation |

| Conveyors & Feeders |

| Dewatering & Tailings |

| Other Specialised Equipment |

| Iron Ore |

| Bauxite |

| Copper |

| Gold |

| Lithium |

| Nickel |

| Rare Earths |

| Other Minerals |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Equipment Type | Crushers |

| Grinding Mills | |

| Screening Equipment | |

| Flotation & Separation | |

| Conveyors & Feeders | |

| Dewatering & Tailings | |

| Other Specialised Equipment | |

| By Mineral Commodity | Iron Ore |

| Bauxite | |

| Copper | |

| Gold | |

| Lithium | |

| Nickel | |

| Rare Earths | |

| Other Minerals | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

What is the current value of the Australia mineral processing equipment market?

The Australian mineral processing equipment market is valued at USD 0.97 billion in 2025 and is forecast to reach USD 1.29 billion by 2030.

Which equipment category commands the largest spend?

Crushers lead spending, holding 34.17% revenue share in 2024 due to high-tonnage Pilbara iron-ore operations.

Which segment is growing fastest?

Dewatering and tailings-filtration equipment shows the quickest rise, expanding at a 5.91% CAGR due to stricter waste-storage rules.

How significant is automation adoption in Australia?

Semi-automated systems hold 47.81% share today, yet fully autonomous fleets are climbing at a 6.11% CAGR, backed by 706 driverless trucks already in operation.

Which state represents the biggest market opportunity?

Western Australia remains the key market, driven by iron-ore replacement spend and emerging battery-mineral processing hubs around the Pilbara and Kwinana.

Page last updated on: