China Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

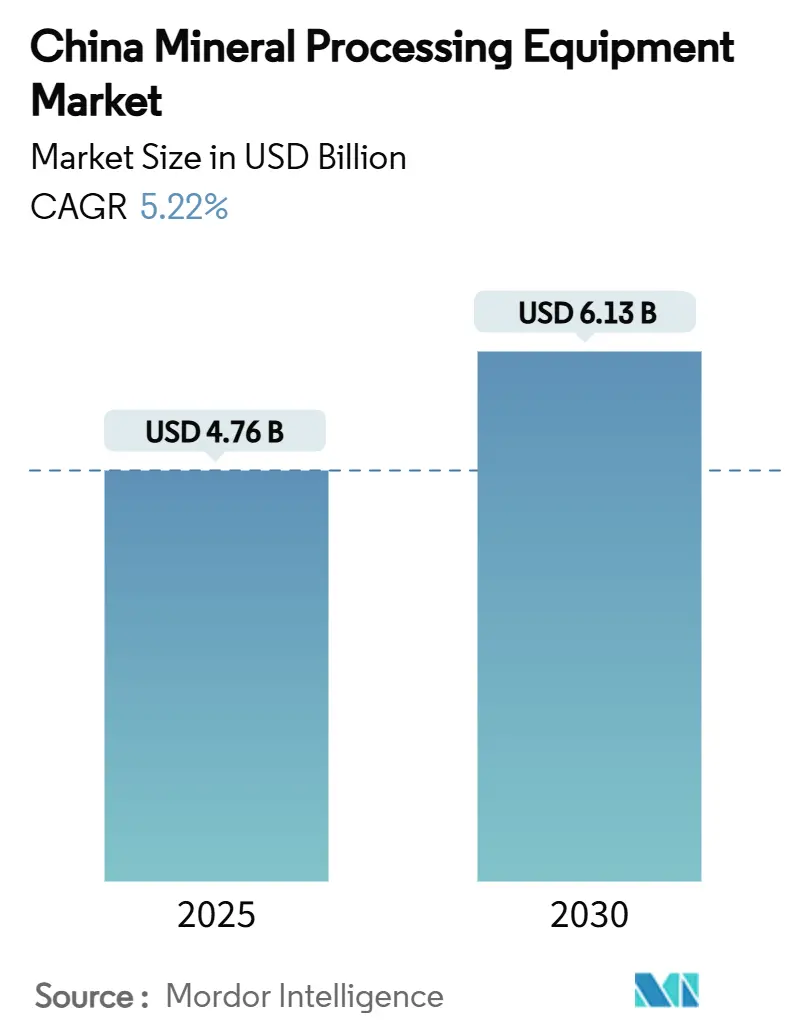

| Market Size (2025) | USD 4.76 Billion |

| Market Size (2030) | USD 6.13 Billion |

| Growth Rate (2025 - 2030) | 5.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Mineral Processing Equipment Market Analysis by Mordor Intelligence

The China Mineral Processing Equipment Market size is estimated at USD 4.76 billion in 2025, and is expected to reach USD 6.13 billion by 2030, at a CAGR of 5.22% during the forecast period (2025-2030). Robust demand for digital-ready, low-carbon machinery, a resurgence in Western and Central mining hubs, and new government mandates on intelligent operations are lifting overall sales. The China mineral processing equipment market also benefits from escalating rare-earth downstream capacity build-outs, fast-tracking of lithium extraction projects, and incentives that encourage tailings reprocessing for critical minerals. International suppliers are expanding local footprints to meet stricter localization rules, while domestic champions are exporting know-how to Africa and South-East Asia, boosting scale economies at home. Meanwhile, surging orders for AI-enabled crushers, conveyors, and dewatering systems underscore the sector’s pivot toward autonomous, high-throughput plants that meet the “Three Simultaneities” environmental framework.

Key Report Takeaways

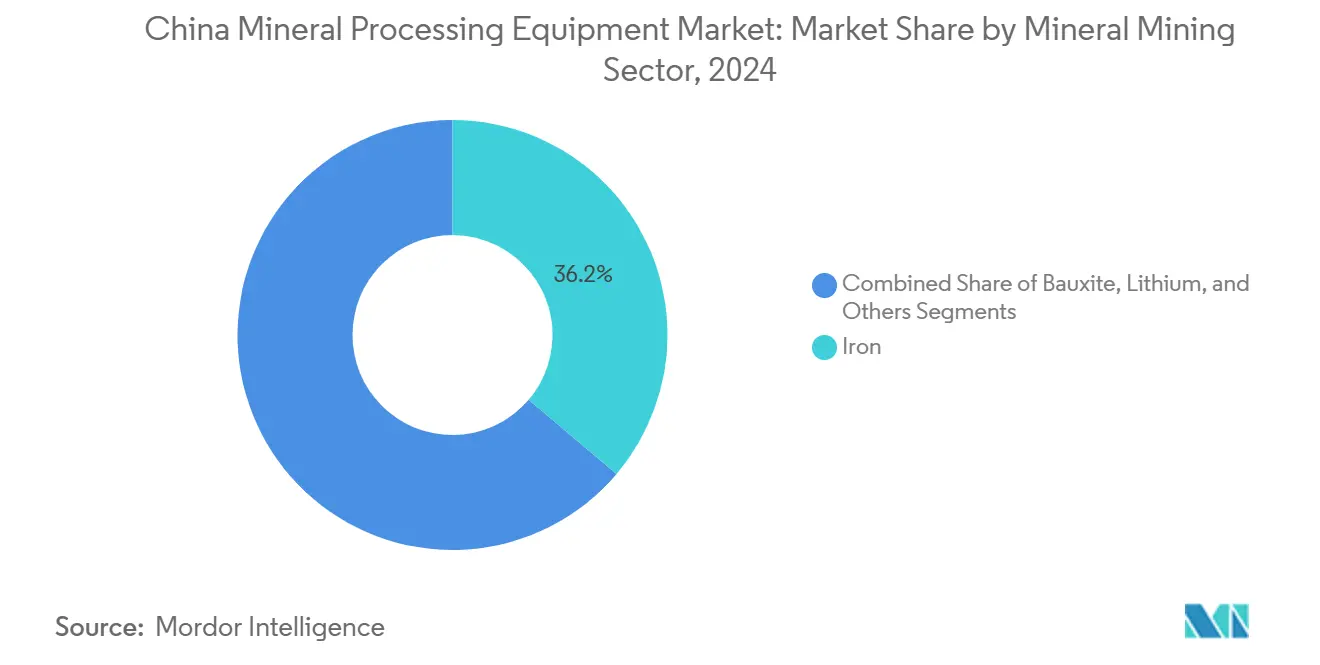

- By mineral mining sector, Iron commanded 36.17% of the China mineral processing equipment market share by mineral type in 2024. Lithium equipment is advancing at a 5.51% CAGR to 2030, the fastest among all mineral categories.

- By equipment type, crushers held 26.11% of the China mineral processing equipment market size in 2024, whereas drills and breakers posted the highest 5.57% CAGR through 2030.

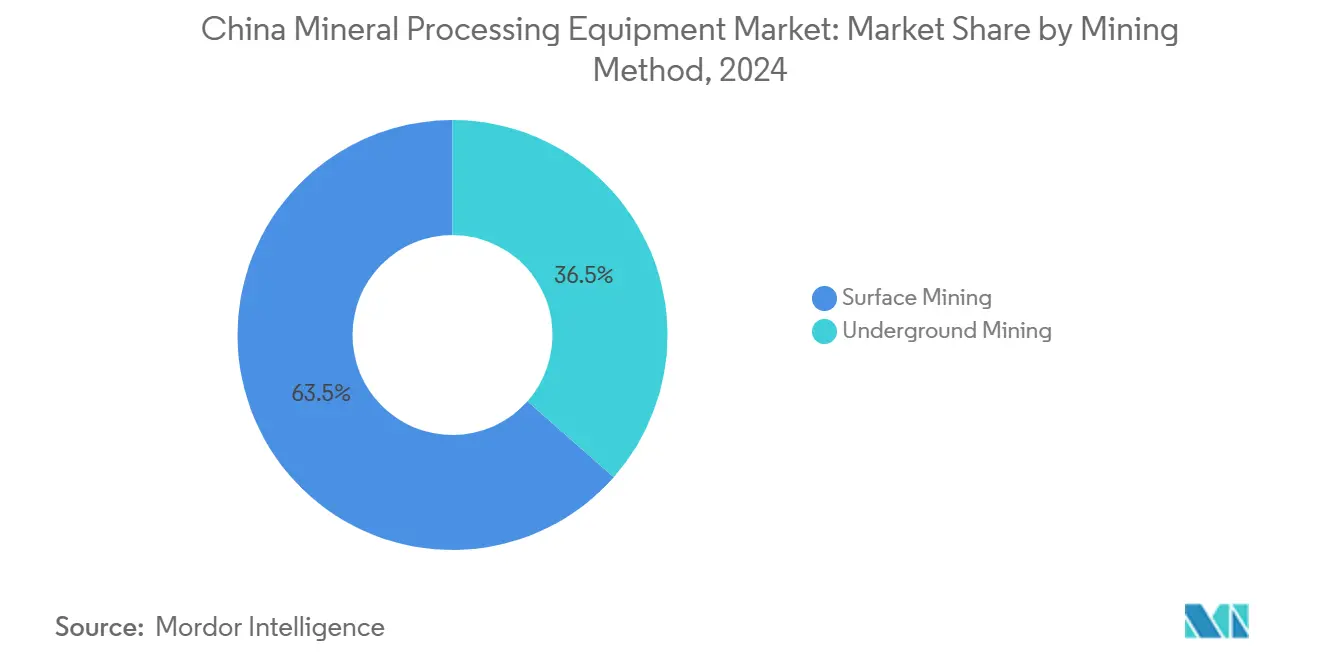

- By mining method, surface operations captured 63.47% of the China mineral processing equipment market share by mineral type in 2024, underground installations are expanding at a 5.48% CAGR to 2030.

- By automation level, manual systems accounted for 45.38% of the China mineral processing equipment market size in 2024, while fully automated units are rising at a 5.55% CAGR.

China participates in a competitive field that extends beyond its own borders. The market landscape in the global mineral processing equipment industry outlined by Mordor Intelligence covers that wider structure.

China Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Mineral Production Resurgence | 1.20% | Xinjiang, Inner Mongolia, Gansu | Medium term (2-4 years) |

| Accelerated Government-Backed Mine Digitalization | 1.00% | National, with early gains in Shanxi, Shaanxi | Short term (≤ 2 years) |

| Surge in Domestic Rare-Earth Downstream Capacity Build-Out | 0.80% | Baotou, Jiangxi, Sichuan | Medium term (2-4 years) |

| Demand for Low-Carbon Processing Equipment | 0.70% | National, priority in industrial clusters | Long term (≥ 4 years) |

| Circular-Economy Tailings-re-Processing Incentives | 0.60% | Hebei, Liaoning, Anhui | Long term (≥ 4 years) |

| Ultra-Low-Grade Iron-Ore Beneficiation Projects | 0.50% | Hebei, Liaoning | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing mineral production resurgence in Western & Central China

Inner Mongolia confirmed 52,400 t of new molybdenum and 591 million t of iron ore reserves in 2024 after allocating CNY 500 million for exploration[1]“2024 Mineral Resource Bulletin,” Inner Mongolia Government, innermongolia.gov.cn . Xinjiang’s Kubai Basin unveiled 2 million tons of zirconium dioxide resources that quintuple national reserves, spurring immediate orders for specialized basin-deposit processing lines. The Shitoumei No.1 coal mine in Hami now operates 91 autonomous haul trucks, illustrating how remote sites dictate demand for durable, self-maintaining plants. The government has budgeted a massive amount for strategic exploration in 2025, setting up a multi-year buying cycle across the Chinese mineral processing equipment market. Equipment vendors are responding with reinforced housings, dust-proof electronics, and AI health-monitoring to suit the desert climate.

Accelerated government-backed mine digitalization programmes

The National Energy Administration’s push for intelligent coal mines produced 118 such facilities and 1,491 smart mining sites in Shanxi[2]“Notice on Accelerating Intelligent Coal Mines,” National Energy Administration, nea.gov.cn . Dahaize Mine in Shaanxi achieved around two-fifths net margin after deploying AI-driven haulage, 5G sensor grids, and edge-based analytics. Yimin coal mine’s autonomous electric trucks rely on dual BeiDou and 5G-Advanced networks for centimeter-level guidance, reducing idle time and enabling 24/7 shifts. These advances require crushers, mills, and thickeners pre-fitted with IoT gateways and real-time process optimizers, lifting the technical bar across the China mineral processing equipment market. Vendors able to bundle digital twins and predictive-maintenance dashboards are gaining a clear pricing premium.

Surge in domestic rare-earth downstream capacity build-out

China Northern Rare Earth Group is expanding Baotou processing throughput to around two lakh tons per year, securing the majority of global dominance. The new rare-earth regulations in October 2024 curtail raw-ore exports and channel feedstock to local separators, amplifying domestic equipment sales. Baotou city aims for CNY 100 billion in rare-earth industrial output, including from deep-processing. Compliance with strict fluoride and ammonia emission caps accelerates uptake of closed-loop flotation cells, solvent-extraction columns, and waste acid recovery skids. Specialized suppliers of high-temperature alloys and corrosion-resistant linings are seeing record-high inquiry volumes in the Chinese mineral processing equipment market.

Circular-economy tailings-re-processing incentives

Pilot studies retrieved almost complete high-purity quartz from iron-ore tailings using wet high-intensity magnetic separation plus mixed-acid leach, turning waste into semiconductor-grade silica. Copper tailings bioleaching fields in Tibet and Jiangxi now employ tailor-made bioreactors that house selective microorganisms for copper recovery, slashing reagent cost by two-fifths. Mine-backfill blends that combine dewatered tailings with cementitious additives cut surface subsidence while monetizing waste fines. Such a circular economy drives demand for high-frequency dewatering screens, membrane presses, and automated reagent-dosing skids, extending revenue streams for the China mineral processing equipment market beyond virgin-ore projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent "Three Simultaneities" Environmental Compliance | -0.8% | National, stricter in eastern provinces | Short term (≤ 2 years) |

| High Upfront CAPEX | -0.6% | National, acute in smaller operations | Medium term (2-4 years) |

| Scarcity of Advanced Process-Control Talent | -0.4% | National, critical in remote western regions | Medium term (2-4 years) |

| Volatile Grid-Power Tariffs in Remote Mining Clusters | -0.3% | Western China, Inner Mongolia, Xinjiang | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent "Three Simultaneities" environmental compliance

The Ministry of Ecology and Environment has ordered that emission-control systems be designed, built, and commissioned alongside every new concentrator, heap-leach pad, and smelter. Coking chemical standards effective January 2027 for existing plants reinforce this trend. Smaller mines must now secure environmental bonds before procurement, limiting cash for productivity upgrades. As a result, some buyers prolong overhaul cycles or favor refurbished equipment, tempering short-term deliveries in the China mineral processing equipment market. Conversely, large operators with stronger balance sheets consolidate acreage, gradually raising overall market concentration.

High upfront CAPEX and long pay-back periods

AI-embedded crushers, 5G-ready haul trucks, and automated reagent dosing lines can cost 30% more than traditional options yet require specialized crews to run them. Volatile grid tariffs in remote clusters make ROI forecasts uncertain, particularly where renewables back-up is not yet installed. Extended operator-training commitments add hidden costs. These factors stretch pay-back horizons, prompting certain mid-tier miners to lease rather than buy, or to refurbish retired fleets, which marginally subdues growth in the China mineral processing equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Iron Dominance Amid Lithium Surge

Iron-ore concentrators accounted for 36.17% of the China mineral processing equipment market share in 2024 as domestic steelmakers expanded beneficiation to reduce imports. The Benxi Dataigou super-giant deposit in Liaoning drives multi-line crusher and magnetic-separator purchases that underpin segment maturity. In contrast, lithium installations are growing at a 5.51% CAGR as battery-grade carbonate demand accelerates. Tianqi Lithium plans to lift chemical output paired with Greenbushes feed, and alone fuel new crystallizer and calciner sales. Bauxite plants continue to invest in desilication washers, while molybdenum and zirconium complexes populate the “Others” bucket. Segment players are testing hydrogen-assisted direct-reduction kits and low-emission roasting kilns to meet steel decarbonization targets.

Second-order effects are reshaping supplier strategy. Premium-grade reagents and automated sample-assay loops gain traction as ore complexity rises. For lithium, closed-circuit evaporation systems that minimize brine discharge gain regulatory favor, hastening adoption across the Chinese mineral processing equipment market. Rare-earth refiners, now bound by output caps, opt for modular solvent-extraction lines to match production quotas.

By Equipment Type: Crushers Lead Technology Evolution

Crushers held 26.11% of the China mineral processing equipment market size in 2024, as every mine, regardless of scale, starts with primary crushing. Drills and breakers recorded the quickest CAGR of 5.57% through 2030, powered by demand for precision blast-hole patterns and battery-electric jumbos. Feeders and conveyors are mid-growth but see value uplift from predictive maintenance modules that cut unplanned stops. The “Others” category—covering autonomous rail-bound haulage and AI process control—expands as miners integrate digital twins across the China mineral processing equipment market.

Continuity handling systems shift from fixed-speed to variable-frequency drives, aligning belt power draw with ore flux. Crusher OEMs and drill suppliers co-develop algorithms that synchronize blast energy with downstream mill load, illustrating a holistic approach to plant optimization. Meanwhile, local foundries in Xuzhou and Changsha increase wear-part output, shortening lead times for high-Mn and Cr-Mo liners.

By Mining Method: Underground Growth Accelerates

Surface sites accounts for 63.47% of the China mineral processing equipment market share in 2024 turnover, cemented by large open-pit coal and iron mines that procure multi-megawatt conveyors and bucket-wheel reclaimers. Nevertheless, the Chinese mineral processing equipment market witnesses a 5.48% CAGR for underground gear as deposits deepen. New “excavation-backfill-retention” techniques necessitate compact crusher-grinder packages with built-in dust-scrubbers. Filling methods, although energy-intensive, cut subsidence risk and thus align with the “Green Mine” accreditation that regulators favor. The nationwide roll-out of 5G coverage in deep shafts also catalyzes orders for tele-operated loaders and drones that map stope stability.

AI cameras and LiDAR modules guide autonomous LHDs, shrinking headcount and raising safety compliance. Battery-electric locomotives, offering 50% less ventilation demand than diesel, further support lower OPEX, fuelling a replacement wave within the China mineral processing equipment market.

By Automation Level: Manual Operations Face Digital Disruption

Manual lines represented 45.38% of the China mineral processing equipment market share in 2024 factory-gate revenue, yet their share erodes each quarter as digitalization spreads. Semi-automated systems, bridging manual and full autonomy, remain popular where fiber connectivity is patchy. Fully automated units record a 5.55% CAGR, underpinned by 24/7 demand, labor shortages, and subsidy eligibility for “lights-out” mines. Mataihao mine’s IoT monitoring cut electricity usage by double digits, proving the economic case for innovative retrofits. National industrial internet platforms already serve more than 400 coal operations, pushing demand for plug-and-play sensor kits, edge PLCs, and AI analytics suites across the China mineral processing equipment market.

OEMs now bundle training in computer-vision safety modules, helping counter the skills gap. Meanwhile, provincial grants covering more than one-tenth of CAPEX on autonomous systems reduce initial cash pain and accelerate project approvals.

Geography Analysis

Resource-rich Western and Central provinces are the growth epicenter. Xinjiang alone attracted CNY 3.35 billion for a 30,000 t lithium-carbonate line, elevating the regional China mineral processing equipment market. Inner Mongolia’s 52,400 t molybdenum find and 591 million t iron-ore reserve draw high-capacity crushers and flotation banks. Both regions showcase large fleets of autonomous trucks 91 at Shitoumei and 100 at Yimin, underlining their readiness for digital mining.

Central provinces capitalize on brownfield upgrades. Shanxi hosts 118 intelligent coal mines and 1,491 smart pits, demanding IoT retrofits for feeders, screens, and pumps. Shaanxi’s Dahaize mine, with a 40% net margin, demonstrates the profitability of complete automation, pulling in vendors that offer integrated 5G-edge packages. Their rail links and skilled labor lower project risk, quickening adoption within the China mineral processing equipment market.

Eastern provinces pivot toward beneficiation and circular economy. Liaoning’s Benxi Dataigou, the world’s largest single iron-ore body, orders ultra-large cone crushers and hydrogen-compatible pelletizers. Hebei pilots 50,000 t vertical extrusion presses for low-grade ore briquetting, tightening demand for high-tonnage hydraulic circuits. Environmental scrutiny in populous east China forces plants to fit dry-stack tailings and regenerative heat units, creating niche sales opportunities for clean-tech OEMs.

Mordor Intelligence provides coverage of the mineral processing equipment market across other key regional markets. Detailed country-level analysis extends to Japan, Australia, Spain, South Korea, Argentina, Turkey, Mexico, Oman, and Egypt incorporating local coverage and market participation, as required.

Competitive Landscape

The playing field is moderately fragmented. CITIC Heavy Industries and BGRIMM Technology Group, both state-owned, broaden portfolios via overseas EPC wins, such as BGRIMM’s cobalt plant in the Democratic Republic of Congo. Their global exposure backfeeds process know-how into domestic bids, reinforcing scale advantages. International majors defend share through localization: Weir’s new Xuzhou foundry boosts crusher-liner availability, and FLSmidth’s mining division posted a 13.1% adjusted EBITA margin by emphasizing digital upgrades [3]“FY 2024 Annual Report,” FLSmidth, flsmidth.com .

Technology convergence defines rivalry. Huawei’s consortium used 5G-Advanced to orchestrate 100 autonomous trucks at Yimin, an emblematic showcase that compels traditional equipment firms to partner with telecom giants. Tailings-recovery specialists and hydrogen-reduction integrators occupy emerging niches where incumbents are less entrenched. Price competition persists in low-spec segments. Yet, total-cost-of-ownership messaging helps premium suppliers carve resilient margins across the China mineral processing equipment market.

M&A sentiment is rising as CAPEX demands outstrip small firms’ budgets. Mid-tier drill producers seek tie-ups with AI analytics start-ups, while pump makers eyeball slurry-sensor companies to complete digital stacks. State guidance encourages consolidation to curb overcapacity and elevate export competitiveness.

China Mineral Processing Equipment Industry Leaders

CITIC Heavy Industries

Metso Outotec

FLSmidth A/S

Sandvik AB

The Weir Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Huawei Technologies, China Huaneng Group, XCMG, and State Grid Smart Internet of Vehicles deployed 100 5G-Advanced autonomous electric trucks at Yimin open-pit mine, Inner Mongolia.

- March 2025: Tianqi Lithium confirmed expansion to 122,600 ton per year of lithium chemicals capacity via a new Jiangsu plant; Greenbushes ore feed will climb to 2.14 million ton per year.

China Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Others |

| Crushers |

| Feeders |

| Conveyors |

| Drills & Breakers |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Others | |

| By Equipment Type | Crushers |

| Feeders | |

| Conveyors | |

| Drills & Breakers | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

What is the projected value of the Chinese mineral processing equipment market by 2030?

The market is forecast to reach USD 6.13 billion by 2030, rising at a 5.22% CAGR.

Which mineral segment is expanding fastest within China’s equipment space?

Lithium-focused equipment posts the quickest 5.51% CAGR on the back of battery-supply-chain demand.

How significant is automation adoption in Chinese mines?

Fully automated systems show a 5.55% CAGR as 5G and AI roll-outs accelerate across more than 400 smart coal operations.

Why are tailings-reprocessing technologies gaining traction?

Circular-economy incentives allow miners to extract additional value and meet stricter environmental rules, creating new demand for dewatering, bioleaching, and magnetic-separation gear.

Which regions are driving new equipment purchases?

Western provinces such as Xinjiang and Inner Mongolia lead growth due to large lithium and iron discoveries, while Shanxi and Shaanxi upgrade existing mines with digital solutions.

What factors limit rapid equipment replacement?

High upfront CAPEX, extended pay-back periods, and stringent “Three Simultaneities” compliance requirements can delay purchase decisions, especially for smaller operators.

Page last updated on: