Canada Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

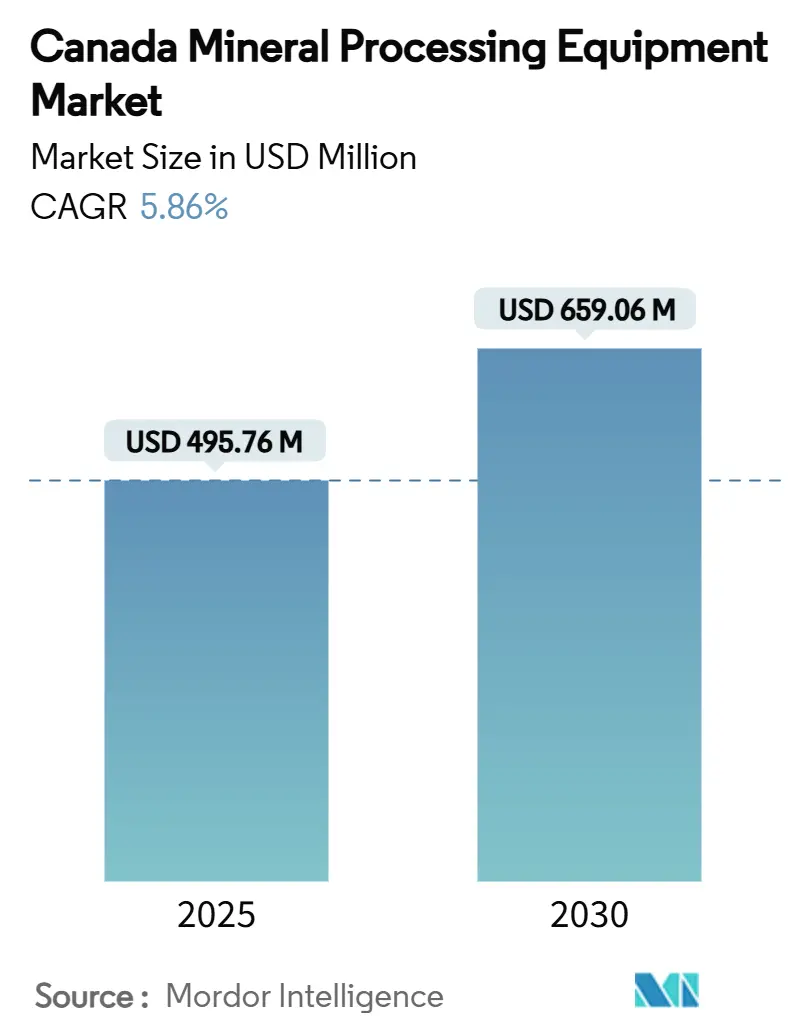

| Market Size (2025) | USD 495.76 Million |

| Market Size (2030) | USD 659.06 Million |

| Growth Rate (2025 - 2030) | 5.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Canada Mineral Processing Equipment Market size is estimated at USD 495.76 million in 2025, and is expected to reach USD 659.06 million by 2030, at a CAGR of 5.86% during the forecast period (2025-2030). Surging critical-mineral demand from electric-vehicle battery supply chains, combined with the federal CAD 3.8 billion Critical Minerals Strategy, anchors growth momentum. Automation-driven productivity gains are equally decisive, as fully-automated solutions help operators offset a nationwide skilled-labor shortfall while shrinking unit costs. Indigenous equity frameworks and loan guarantees widen capital-spending headroom, steering fresh equipment orders toward projects with strong community partnerships. At the same time, provincial clean-energy mandates are accelerating adoption of process control systems that curb emissions and improve water stewardship, ensuring that the Canadian mineral processing equipment market stays aligned with ESG expectations.

Key Report Takeaways

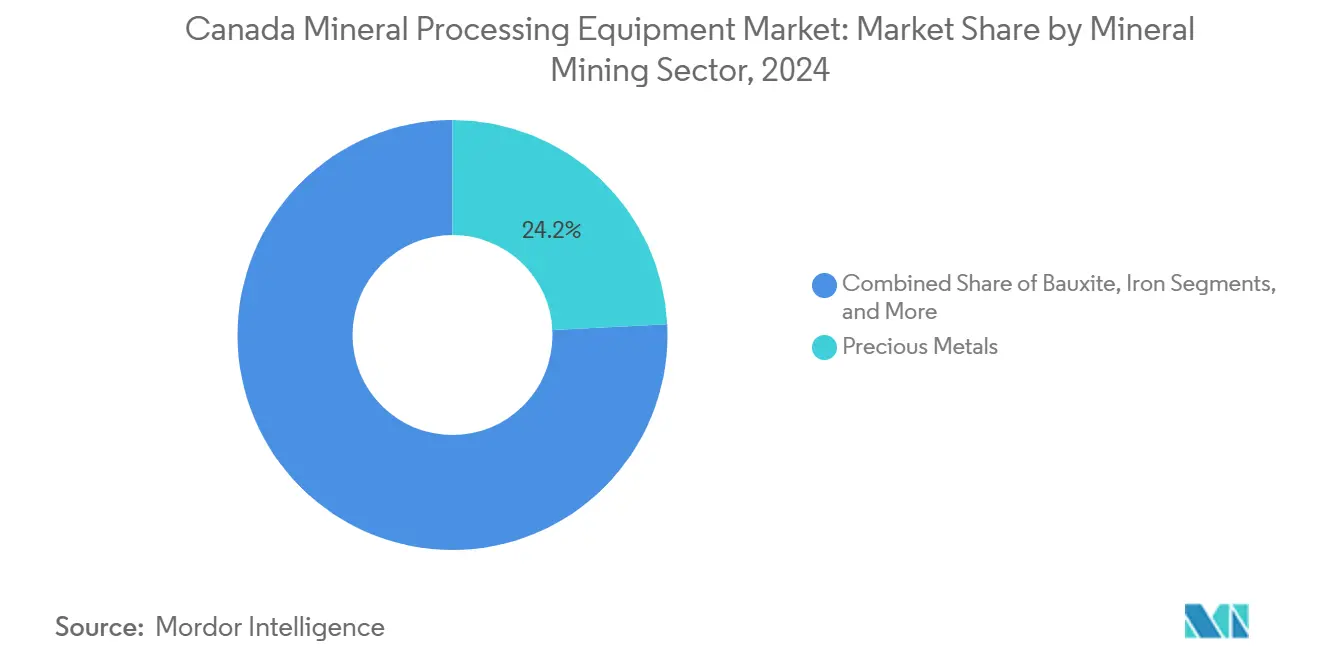

- By mineral mining sector, precious metals led with a 24.16% share of the Canada mineral processing equipment market size in 2024, whereas lithium equipment is projected to expand at a 5.97% CAGR through 2030.

- By equipment type, crushers held 21.83% share of the Canada mineral processing equipment market size in 2024; process control systems will advance at a 5.88% CAGR to 2030.

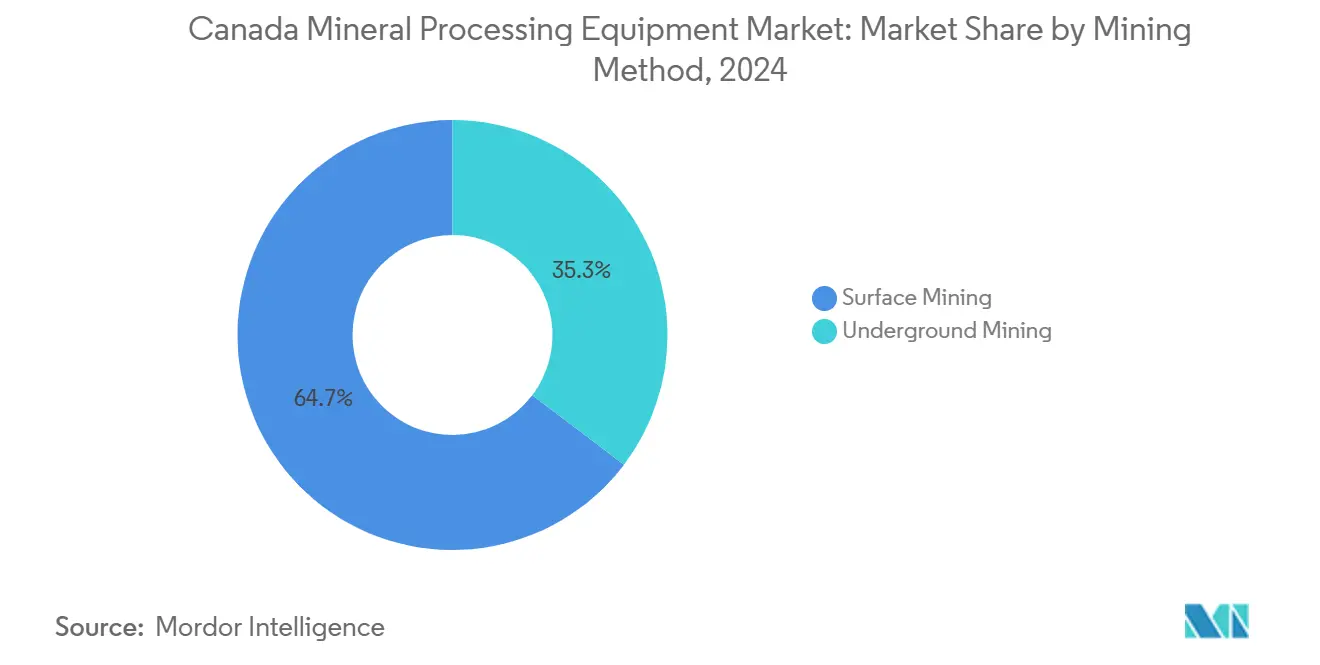

- By mining method, surface mining captured 64.72% share of the Canada mineral processing equipment market size in 2024, while underground mining equipment is growing at a 5.92% CAGR through 2030.

- By automation level, semi-automated equipment accounted for 46.28% share of the Canada mineral processing equipment market size in 2024; fully-automated solutions are progressing at a 6.04% CAGR to 2030.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide mineral processing equipment market outlook captures this forward trajectory.

Canada Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-Mineral Demand Surge | +1.8% | National, with concentration in Quebec, Ontario, British Columbia | Medium term (2-4 years) |

| CAD 3.8Bn Federal Critical Minerals Strategy Incentives | +1.2% | National, with priority funding for Northern Ontario, Yukon, Quebec | Short term (≤ 2 years) |

| Automation and Digitalisation | +0.9% | National, with early adoption in Alberta, British Columbia mining operations | Long term (≥ 4 years) |

| EV-Battery Gigafactories Ignite Mid-Stream Processing CAPEX | +0.7% | Ontario, Quebec manufacturing corridors | Short term (≤ 2 years) |

| Western Canada Hydromet Pilot-Plant Build-Outs | +0.6% | Western Canada, particularly Alberta, British Columbia | Medium term (2-4 years) |

| Indigenous Equity Frameworks Unlocking Capex | +0.4% | National, with strongest impact in Northern territories, British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Demand Surge from EV Batteries

Electric-vehicle battery manufacturing catalyzes unprecedented mid-stream investment, led by Volkswagen’s St. Thomas gigafactory and Stellantis-LG’s billion Windsor complex[1]“Volkswagen Chooses St. Thomas for First North American Cell Plant,” Volkswagen AG, volkswagen-newsroom.com . The local supply-chain imperative extends beyond mining into recycling and refining. Electra Battery Materials’ Ontario black-mass pilot achieved over four-fifths manganese recovery and almost one-fifth rise in lithium-carbonate quality. LithiumBank Resources’ Calgary direct-lithium-extraction (DLE) facility posted 98% lithium recoveries, signaling viable domestic processing routes. Equipment suppliers respond with specialized hydrometallurgical systems; Metso introduced a low-emission copper-sulfide concentrate leaching process featuring high metal recovery efficiencies[2]“Metso Launches Sustainable Leaching Process for Copper Concentrates,” Metso, metso.com . As OEMs race to secure regional cathode-grade inputs, the Canada mineral processing equipment market is capturing diversified orders spanning hard-rock spodumene plants, brine-based DLE units, and battery-recycling lines.

CAD 3.8 Billion Critical Minerals Strategy Incentives

The federal Critical Minerals Strategy is the most significant federal mining stimulus since the 1970s, earmarking investment for infrastructure via the Critical Minerals Infrastructure Fund. Natural Resources Canada has approved projects, including Quebec lithium processing and CAD 40 million for Yukon grid upgrades. A 30% Clean-Technology Manufacturing investment tax credit covers extraction, processing, and recycling equipment. Concurrently, Ontario’s indigenous participation initiative supplies loan guarantees that can double project debt envelopes, fast-tracking procurement decisions. The coordinated fiscal package compresses development timelines, a tailwind for equipment vendors able to meet battery-grade specifications. Consequently, the Canadian mineral processing equipment market enjoys a pipeline of shovel-ready projects that might otherwise have stalled.

Automation & Digitalisation to Ease Skilled-Labor Crunch

Canada’s mining sector needs nearly a lakh of new workers by 2030, yet just more than one-fifth of young Canadians consider mining careers. Autonomous haulage at the Côte Gold mine already handles 30,000 t per day, lifting productivity 30% while trimming workforce size. High salaries—process-control technicians now command over CAD 120,000—sharpen the return on automated monitoring systems, often delivering payback in under three years. Digitalisation reaches into predictive maintenance, where connected plants cut unplanned downtime by 15-20%. However, the expanded attack surface means mining ranks among Canada’s most targeted critical-infrastructure sectors, with 89% of initial cyberintrusions exploiting social-engineering vectors.

Western Canada Hydromet Pilot-Plant Build-outs

Alberta and British Columbia are coalescing into a hydrometallurgical hub, leveraging abundant hydropower and Asian export proximity. FPX Nickel’s awaruite refinery concept and Teck Resources’ battery-materials recycling studies reveal a pivot toward urban mining and mid-stream processing. British Columbia’s clean-power grid aligns with ESG mandates, lowering the Scope 2 footprint of new facilities. Cyclic Materials rare-earth recycling center showcases modular processing that scales from pilot to commercial output. Suppliers are customizing skids and piping systems to withstand wide temperature swings and rigorous permitting, reinforcing Western Canada as a proving ground for next-generation hydromet technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-Price Volatility and High Cap-Intensity | -1.1% | National, with regional variations based on commodity exposure | Short term (≤ 2 years) |

| Federal Carbon-Pricing | -0.8% | National, with highest impact on energy-intensive processing operations | Medium term (2-4 years) |

| Lengthy Environmental | -0.6% | National, with extended delays in environmentally sensitive regions | Long term (≥ 4 years) |

| Cyber-Security Gaps | -0.4% | National, with higher risk in automated operations and remote facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility & High Cap-Intensity

Copper’s 2024 price swings and lithium’s post-2022 retracement illustrate heightened market turbulence. The Ekati Diamond Mine paused Point Lake stripping after rough diamond prices slipped 20%, underlining how price collapses cascade into idled fleets and deferred replacements. Cap-ex intensity is steep, central processing lines frequently exceed half a billion USD, so operators prioritize assets with sub-three-year paybacks and modular expandability. Suppliers face lumpy order flow, complicating production planning and inventory management.

Federal Carbon-Pricing & Emissions Caps

The consumer carbon levy ends in April 2025, industrial carbon prices persist under the Output-Based Pricing System, affecting facilities exceeding half a lakh ton CO₂e annually. Mining companies are weighing electric crushers and trolley-assist haulage to sidestep compliance costs, yet the policy’s evolving parameters inject budgeting uncertainty. Offset credits and compliance banking soften immediate impacts, but multi-decade financing models still incorporate carbon-price sensitivity, tempering equipment-buying velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Lithium Processing Drives Equipment Innovation

Canada mineral processing equipment market size for precious-metals plants represented 24.16% of revenues in 2024, reflecting robust gold projects such as B2Gold’s Goose mine first-pour milestone. Lithium equipment, however, is tracking a 5.97% CAGR through 2030, more than double the market average, as DLE pilots mature into commercial plants in Alberta brine basins. Operators require finer particle-size control, specialized solvent-extraction columns, and high-purity crystallizers to meet battery-grade carbonate thresholds.

Second-order impacts are evident in copper, where Highland Valley’s expansion to 178,000 t-per-day throughput calls for higher-capacity grinding mills and flotation lines. Iron ore beneficiation maintains steady demand because pelletizing lines at Labrador Trough complexes sustain replacement cycles. Nickel-processing interest is revitalized by Canada Nickel’s Reid resource, which is aligned with refinery pilots employing hydromet circuits. This mineral diversification compels OEMs to design multi-commodity modules that minimize lead times and enhance swap-over flexibility during price swings, keeping the Canada mineral processing equipment market responsive to cross-cycle dynamics.

By Equipment Type: Process Control Systems Lead Automation Wave

Crushers retained a 21.83% Canada mineral processing equipment market share in 2024 on the back of universal primary-comminution requirements across open-pit and underground mines. Nonetheless, process-control and automation systems headline growth at a 5.88% CAGR to 2030, as plants integrate sensors, AI-enabled analytics, and centralized dashboards. Grinding mills incorporate Metso Outotec’s high-pressure grinding-roll (HPGR) platforms to reduce power draw up to one-fifth. Flotation cells adopt gas-dispersion upgrades that elevate recovery rates, while modular thickening packages address water-use regulations.

Due to abrasive wear profiles, de-watering, pumps, and hydrocyclones show consistent replacement demand. Screen and classifier vendors deploy high-strength polyurethane panels that extend change-out intervals. The convergence of sensing, actuation, and predictive maintenance reshapes procurement criteria, shifting value from mechanical performance to lifecycle data integration. OEMs capable of bundling hardware with analytics software secure long-term service contracts, strengthening their position in the Canadian mineral processing equipment market.

By Mining Method: Underground Automation Accelerates Growth

Surface-mine installations contributed 64.72% of the Canada mineral processing equipment market in 2024, buoyed by large pits such as Greenstone and Côté. Open-pit fleets continue to dominate tonnage movement; however, underground equipment revenue is expanding at a 5.92% CAGR, outpacing the broader Canada mineral processing equipment market. Battery-electric loaders and autonomous haulage carriers improve air quality and worker safety, decreasing ventilation power demand.

Technological gains extend to geosteering and face-mapping tools that optimize blast designs and trimming dilution. Indigenous ownership of underground assets illustrated by Selkirk First Nation’s Minto acquisition introduces community objectives into procurement decisions, emphasizing low-noise, low-emission gear. Safety regulations intensify data-logging and collision-avoidance requirements, ensuring the underground segment embraces cutting-edge digital solutions sooner than its surface counterparts.

By Automation Level: Fully-Automated Solutions Gain Traction

Semi-automated assets will still hold a 46.28% of the Canada mineral processing equipment market share in 2024 because they blend human oversight with automated functions suited to Canada’s mixed-skill workforce. Manual systems linger in artisanal operations but are ceding ground rapidly. Fully automated units are growing at a 6.04% CAGR, outstripping every other automation stratum in the Canadian mineral processing equipment market.

Interoperability advances underpin adoption. Wenco’s ISO 23725:2024 platform allows multi-vendor fleets to share ordinary data buses, eliminating vendor lock-in and simplifying lifecycle upgrades. 5G-enabled latencies under 40 milliseconds facilitate real-time ore-body sensing, closed-loop mill-feed adjustments, and remote diagnostics. Cybersecurity protocols follow zero-trust principles and multilayer encryption, reflecting heightened threat awareness across critical infrastructure operators.

Geography Analysis

Ontario remains the epicenter of demand, driven by the Greenstone Gold project’s 2024 commissioning of key crushing and grinding assets and by the province’s Critical Minerals Innovation Fund that reimburses up to CAD 500,000 per processing-tech initiative. Adjacent equipment clusters in Sudbury and Timmins shorten lead times for overhauls and spares, further reinforcing Ontario’s purchasing power within the Canadian mineral processing equipment market.

Quebec trails closely as a lithium and nickel processing nucleus. The province’s language of early-stage flow-sheet innovation attracts OEM application centers, ensuring rapid prototype-to-plant transitions. British Columbia leverages vast hydro-electric capacity and a 25% Indigenous-ownership threshold for new clean-energy projects. The province’s Highland Valley Copper life-extension demands large replacement crushers, screens, and flotation lines, stimulating localized supply partners. Western provinces, notably Alberta, exploit existing oil-patch infrastructure to fast-track hydromet pilot plants, sharing logistics corridors with established hydrocarbon mid-stream systems.

This evolving spatial pattern diffuses procurement from a few legacy hubs toward a network of specialized regional clusters, each fine-tuned to specific minerals or processing stages. As transport links improve, OEMs adopt hub-and-spoke service models, positioning satellite technicians within one-day travel of remote concentrators. Such decentralization is essential to sustaining uptime guarantees that modern service contracts impose, thereby underpinning long-run growth in the Canadian mineral processing equipment market.

The mineral processing equipment market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for Mexico, Brazil, South Korea, Argentina, Turkey, Japan, Oman, Egypt, and Morocco, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Canada mineral processing equipment market is moderately fragmented, with global heavyweights and agile regional suppliers sharing the arena. FLSmidth posted \mining-service order growth in 2024, lifting its adjusted EBITA margin[3]“2024 Annual Report,” FLSmidth, flsmidth.com . Metso, meanwhile, logged a climb in Q3 2024 equipment orders, highlighting its pivot to sustainability-led flow-sheet solutions. Sandvik’s record USD 71 million order for battery-electric mining fleets at South32’s Hermosa project underscores growing end-user appetite for low-emission machinery[4]“Sandvik Wins Largest BEV Order to Date,” Sandvik, sandvik.com .

Mid-tier disruptors pursue niches. CAUR Technologies’ ambient-noise tomography streamlines geophysical target delineation, changing upstream equipment roadmaps. Canadian-owned Multotec specializes in tailor-made hydrocyclones optimized for Arctic climate tolerances, garnering loyalty among northern operators. Competitive edges increasingly hinge on software ecosystems; OEMs bundling AI-powered predictive-maintenance suites secure recurring revenues that can equal or exceed original equipment margins.

New tenders emphasize ESG and Indigenous-partnership criteria, requiring bidders to show credible frameworks for community ownership and carbon mitigation. Such stipulations tilt awards toward suppliers with transparent supply chains, low-carbon manufacturing footprints, and robust training programs for local technicians. Amid this landscape, strategic alliances and technology-licensing deals proliferate, enabling participants to plug capability gaps quickly while preserving capital. Consolidation remains sporadic, the January 2025 FASTech acquisition by Sandvik is emblematic, yet no single player approaches a dominant position, sustaining healthy rivalry within the Canadian mineral processing equipment market.

Canada Mineral Processing Equipment Industry Leaders

Metso Outotec

Sandvik AB

FLSmidth A/S

Caterpillar Inc.

Sepro Mineral Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Canada Growth Fund committed USD 111 million to Foran Mining’s McIlvenna Bay project, accelerating plant-equipment procurement.

- March 2025: Metso introduced a copper-sulfide concentrate leach process that delivers high copper recoveries with reduced environmental impact.

- January 2025: Sandvik acquired FASTech, a high-end CAM reseller, boosting local service capabilities for advanced processing systems.

Canada Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Copper |

| Nickel |

| Precious Metals (Gold, Silver, PGMs) |

| Others |

| Crushers |

| Grinding Mills |

| Feeders & Conveyors |

| Drills & Breakers |

| Screens & Classifiers |

| Flotation Cells |

| Hydrocyclones & Pumps |

| Thickening & Dewatering |

| Process Control & Automation Systems |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully-Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Copper | |

| Nickel | |

| Precious Metals (Gold, Silver, PGMs) | |

| Others | |

| By Equipment Type | Crushers |

| Grinding Mills | |

| Feeders & Conveyors | |

| Drills & Breakers | |

| Screens & Classifiers | |

| Flotation Cells | |

| Hydrocyclones & Pumps | |

| Thickening & Dewatering | |

| Process Control & Automation Systems | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully-Automated |

Key Questions Answered in the Report

What is the current value of the Canadian mineral processing equipment market?

The market was valued at USD 495.76 million in 2025 and is projected to reach USD 659.06 million by 2030.

Which mineral segment is expanding fastest in Canada?

Lithium processing equipment is advancing at a 5.97% CAGR through 2030, the highest among all mineral segments.

How significant is automation in new equipment purchases?

Fully-automated solutions are the quickest-growing automation tier, registering a 6.04% CAGR as operators offset skilled-labor shortages.

Which provinces lead to the demand for mineral processing equipment?

Ontario, Quebec, and British Columbia collectively dominate demand due to ample greenfield and brownfield projects.

Page last updated on: