Argentina Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

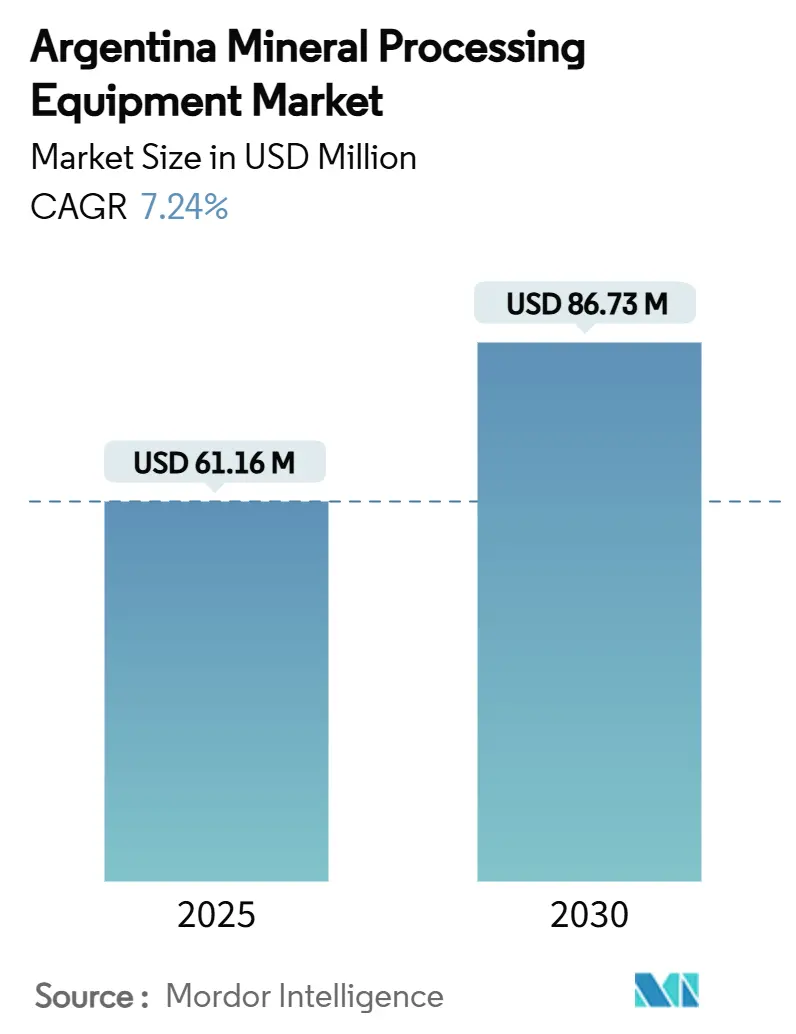

| Market Size (2025) | USD 61.16 Million |

| Market Size (2030) | USD 86.73 Million |

| Growth Rate (2025 - 2030) | 7.24% CAGR |

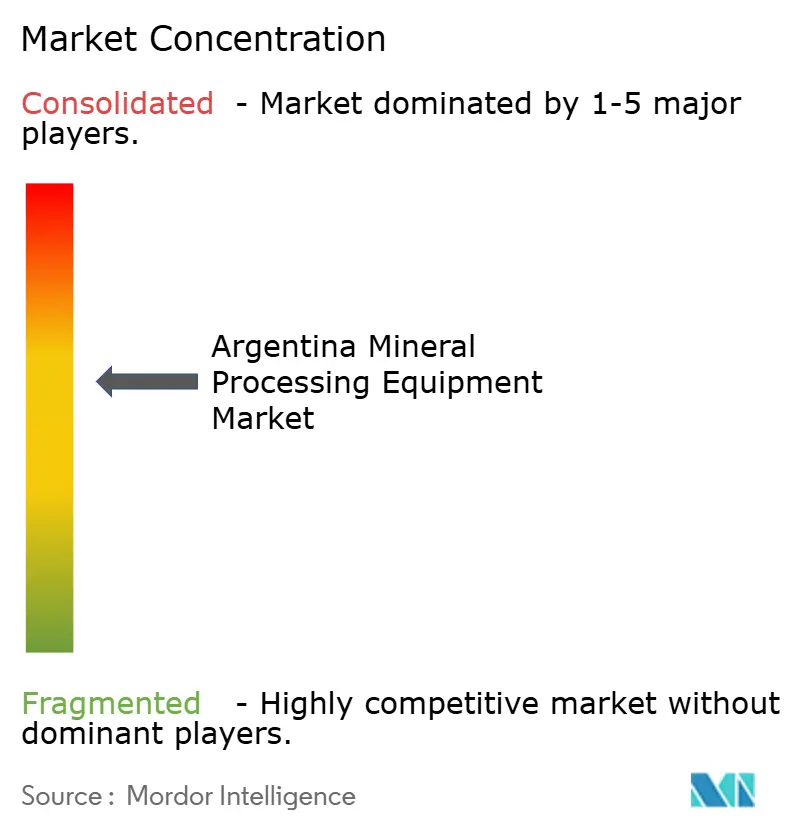

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Argentina mineral processing equipment market size is valued at USD 61.16 million in 2025 and is forecast to reach USD 86.73 million by 2030, expanding at a 7.24% CAGR. A surge of large‐scale lithium and copper projects, stronger provincial cooperation across the lithium triangle, and a federal investment regime that grants 30-year fiscal stability are creating a steady pipeline of greenfield processing facilities. U.S. suppliers currently dominate equipment imports, yet local distributors are winning share by offering rapid field service in Catamarca and Salta. Rising electricity tariffs have sharply increased the payback advantage of energy-efficient comminution circuits, while automation retrofits are progressing from pilot projects to full plant roll-outs. The net result is a market where technology differentiation and after-sales support have become the primary levers of competitive advantage, outweighing pure purchase-price considerations.

Key Report Takeaways

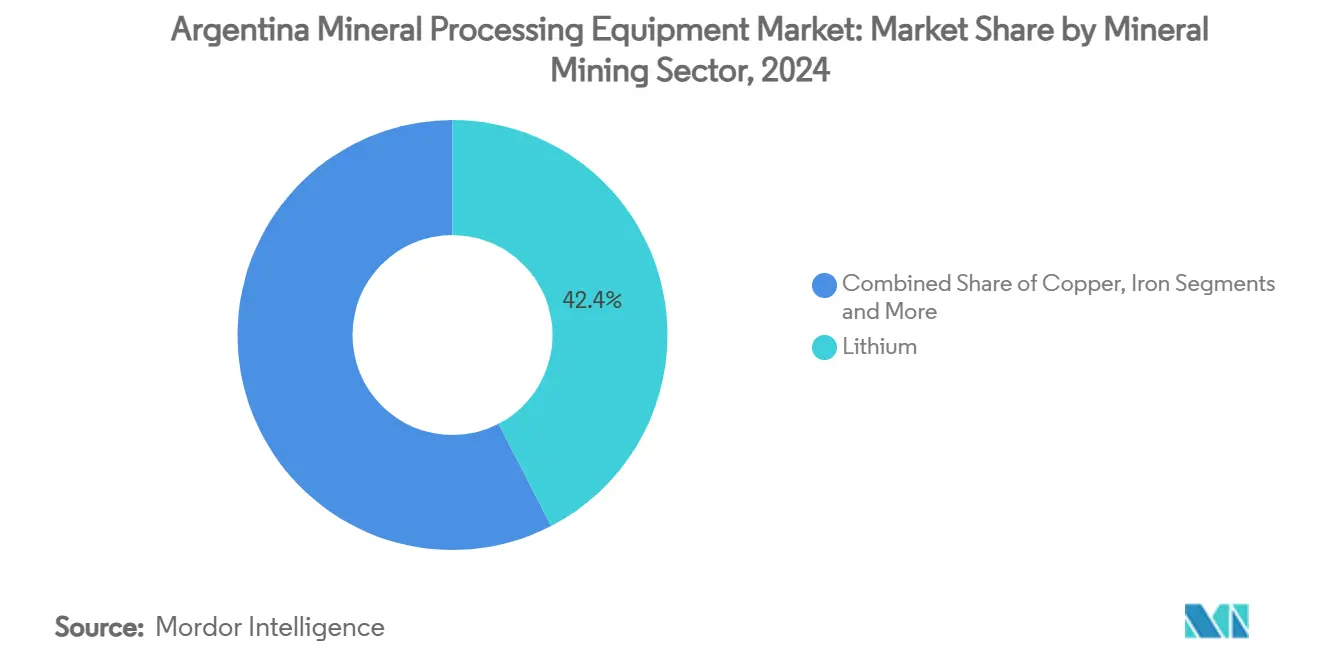

- By mineral mining sector, lithium held 42.39% of Argentina mineral processing equipment market share in 2024 and is advancing at an 11.87% CAGR through 2030.

- By equipment type, mills represent the fastest-growing segment with a 9.58% CAGR, while crushers captured a 28.14% revenue share in 2024.

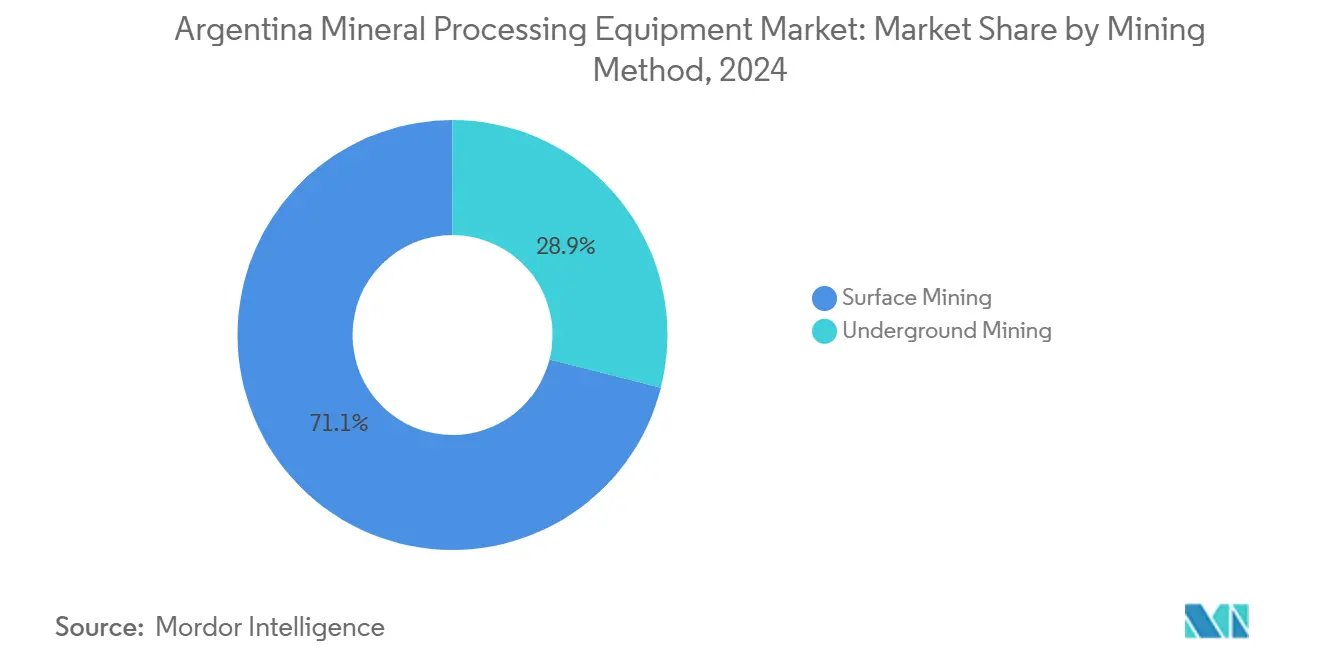

- By mining method, surface operations commanded 71.06% of the Argentina mineral processing equipment market size in 2024 and will rise at a 7.47% CAGR to 2030.

- By automation level, the semi-automated segment commanded 54.27% share, while the fully-automated segment demonstrated 13.23% CAGR.

- By geography, Catamarca led with 24.18% revenue share in 2024; Jujuy is forecast to expand at the second-highest 9.82% CAGR to 2030.

Companies active in Argentina may frequently operate across several geographies, linking regional presence to global strategy. Mordor Intelligence captures the entire market landscape of the global mineral processing equipment industry and how these positions are distributed.

Argentina Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Lithium and Copper Project Pipeline | +2.1% | Catamarca, Jujuy, Salta | Medium Term (2–4 Years) |

| State Incentives and FDI Facilitation Programmes | +1.8% | National, with concentration in Lithium Triangle provinces | Long Term (≥ 4 Years) |

| Adoption of Energy-Efficient Comminution Circuits | +1.3% | National, particularly large-scale operations | Medium Term (2–4 Years) |

| Digital/Automation Retrofits for Legacy Plants | +0.9% | National, emphasis on established mining regions | Long Term (≥ 4 Years) |

| Shared Lithium-Triangle Infrastructure Build-Out | +0.7% | Catamarca, Jujuy, Salta | Long Term (≥ 4 Years) |

| Modular Pilot-Plant Demand from Junior Miners | +0.4% | Emerging mining districts across northern provinces | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Surging Lithium and Copper Project Pipeline

Argentina's demand for mineral processing equipment is experiencing unprecedented acceleration due to massive project commitments that fundamentally reshape the country's mining infrastructure requirements. Rio Tinto's USD 6.7 billion acquisition of Arcadium Lithium in March 2025, combined with the USD 2.5 billion Rincon project expansion, positions the company as the third-largest global lithium producer while creating substantial equipment procurement cycles[1]"Rio Tinto completes $6.7 billion acquisition of Arcadium Lithium," Compass Lexecon, compasslexecon.com.. The copper sector demonstrates equally compelling momentum through BHP and Lundin Mining's USD 2.1 billion joint venture to develop the Filo del Sol and Josemaria projects, leveraging shared infrastructure to optimize equipment utilization across the Vicuña district. McEwen Copper's USD 2.7 billion Los Azules project application to the RIGI regime further validates the copper equipment demand trajectory, with construction potentially starting in early 2026.

These developments represent over USD 11 billion in committed capital to drive equipment procurement across crushing, grinding, and processing systems. The pipeline's geographic concentration in the lithium triangle creates equipment demand clusters that enable suppliers to achieve economies of scale while reducing logistical complexities inherent in Argentina's remote mining locations.

State Incentives and FDI Facilitation Programs

Argentina's regulatory transformation through the Large Investment Incentive Regime (RIGI) creates unprecedented equipment financing advantages that directly impact procurement decisions and supplier market entry strategies. The regime's 25% corporate income tax rate, combined with accelerated depreciation for mining investments and 30-year regulatory stability guarantees, fundamentally alters the economics of capital-intensive equipment purchases. Provincial coordination between Salta, Jujuy, and Catamarca ensures uniform benefits across the lithium triangle, eliminating regulatory arbitrage concerns that previously complicated multi-provincial equipment deployment strategies.

The Mining Investment Law's extension of tax benefits to mining suppliers, including VAT and income tax withholding exemptions, reduces equipment costs while improving supplier cash flow dynamics. Foreign exchange incentives allowing percentage-based export collection retention provide mining companies with dollar-denominated equipment purchasing power, mitigating peso devaluation risks that historically constrained capital expenditure cycles. The regime's success in attracting only one approved project out of seven applications highlights implementation bottlenecks, yet creates competitive advantages for early movers who secure regulatory approval and equipment supply agreements.

Adoption of Energy-Efficient Comminution Circuits

Energy optimization imperatives are driving fundamental shifts in comminution technology selection, with High Pressure Grinding Rolls (HPGR) and advanced grinding solutions achieving 25% power savings compared to conventional ball mill circuits. Metso's EUR 45 million clean comminution order demonstrates industry commitment to sustainable crushing and grinding technologies that combine HRCe high-pressure grinding rolls with Vertimill systems to reduce energy consumption and CO2 emissions[2]"Metso Outotec wins €45M 'clean comminution' order," Mining Magazine, miningmagazine.com.. The technology's circuit simplification potential, reducing equipment requirements from 13 units to 1 in certain applications, creates compelling total cost of ownership advantages while improving process control and optimization capabilities. Argentina's mining operations increasingly prioritize energy-efficient solutions due to rising electricity costs and sustainability mandates, with renewable energy integration becoming critical for long-term operational viability.

The cumulative kinetic model (CKM) applications in critical metal ore processing provide simplified procedures for determining kinetic parameters, enabling more accurate Work Index estimations that optimize grinding circuit design for Argentina's diverse mineral portfolio. Equipment suppliers who demonstrate measurable energy efficiency improvements gain competitive advantages in procurement processes, particularly for large-scale operations where power consumption represents significant operational expenditure.

Digital/Automation Retrofits for Legacy Plants

Argentina's mining sector is experiencing accelerated digital transformation as operators retrofit legacy facilities with IoT sensors, predictive maintenance systems, and autonomous equipment to improve safety and operational efficiency. Techint Engineering & Construction's implementation of Sigfox IoT technology for equipment monitoring demonstrates how digital solutions enable real-time data transmission regarding equipment usage, pressure, and temperature across remote mining locations. Machine learning applications in copper milling processes show measurable improvements in energy efficiency and recovery rates, with low-code platforms democratizing AI tools for industry professionals who lack extensive programming expertise. The integration of Advanced Work Packaging (AWP), Building Information Modeling (BIM), and digital twins remains underutilized despite proven benefits in other sectors, creating opportunities for equipment suppliers who can demonstrate integrated digital solutions.

Epiroc's expansion of autonomous mining equipment, with 42% of its portfolio available in battery-electric versions, reflects industry movement toward zero-entry mining concepts where human presence in hazardous areas is minimized through automation. Cultural resistance and interoperability challenges continue to limit adoption rates, yet mining companies that successfully implement digital retrofits achieve significant competitive advantages through improved equipment utilization and reduced maintenance costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Federal and Provincial Environmental Approvals | -1.4% | National, with stricter enforcement in populated areas | Medium Term (2–4 Years) |

| Commodity-Price Volatility Dampening CAPEX Cycles | -1.1% | National, affecting all mining sectors | Short Term (≤ 2 Years) |

| Shortage of Skilled Maintenance Labour in Remote Andes | -0.9% | Remote Andean mining districts | Medium Term (2–4 Years) |

| Peso/FX Instability Inflating Imported CAPEX | -1.2% | National, especially import-reliant junior miners | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Tightening Federal and Provincial Environmental Approvals

Environmental Impact Assessment (EIA) requirements are becoming increasingly stringent across Argentina's mining jurisdictions, creating equipment procurement delays and additional compliance costs that impact project timelines and capital allocation decisions. Argentina's reliance on EIAs as the primary pollution prevention mechanism requires separate assessments for each mining phase, with provincial authorities maintaining discretionary approval powers that can extend project development cycles[3]"Pollution Prevention and Mining," Environmental Law Institute, eli.org.. The regulatory framework's emphasis on Free, Prior, and Informed Consultation (FPIC) with local communities introduces additional complexity layers, particularly for equipment installations in sensitive ecological areas where lithium operations intersect with wetland preservation requirements.

Mining companies increasingly specify environmental compliance features in equipment procurement specifications, driving demand for closed-loop systems and emission control technologies that add 15-20% to baseline equipment costs. The divergence between private transnational standards and public regulations creates compliance complexity, with equipment suppliers required to meet multiple certification requirements that extend delivery timelines and increase project risk profiles. Provincial variations in environmental enforcement create regulatory arbitrage opportunities, yet also complicate standardized equipment deployment strategies across multi-jurisdictional mining operations.

Commodity-Price Volatility Dampening CAPEX Cycles

Commodity price fluctuations continue to create equipment procurement uncertainty, with lithium prices falling due to oversupply and reduced electric vehicle demand growth, directly impacting capital expenditure decisions across Argentina's mining sector. The Argentine Chamber of Mining Companies' projection of USD 5 billion mining exports by 2025, despite lithium price pressures, reflects the sector's resilience yet highlights the sensitivity of equipment investment cycles to commodity market dynamics. Copper project economics remain more stable, with Argentina's ambition to become a top-10 global copper producer supporting sustained equipment demand despite short-term price volatility.

Mining companies increasingly adopt flexible equipment procurement strategies, including lease arrangements and modular solutions that enable rapid scaling based on commodity price movements and market conditions. The peso's historical volatility against the U.S. dollar compounds commodity price risks, with equipment imports requiring sophisticated hedging strategies to manage foreign exchange exposure across multi-year procurement contracts. Equipment suppliers who offer flexible financing terms and currency hedging support gain competitive advantages in volatile market conditions, particularly for capital-intensive processing equipment where procurement decisions involve significant financial commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Lithium Dominance Drives Equipment Innovation

Lithium mining commands 42.39% of Argentina's mineral processing equipment market share in 2024, while achieving the fastest growth rate at 11.87% CAGR through 2030, reflecting the sector's strategic importance in global energy transition dynamics. The lithium triangle's concentration of world-class brine deposits creates unique equipment requirements for direct lithium extraction (DLE) technologies, with pilot plants gaining regulatory approval in Jujuy province to optimize extraction processes and yields. Copper mining represents the second-largest equipment demand segment, driven by projects like Los Azules and Filo del Sol that require conventional crushing and grinding circuits for porphyry ore processing. Gold and silver operations maintain steady equipment demand through established mines like Barrick's Veladero, where USD 219 million in facility improvements demonstrate ongoing capital investment in processing infrastructure.

Iron ore and uranium sectors represent emerging opportunities, with uranium and thorium inclusion in the Investment Regime for Mining Activity expanding equipment procurement possibilities for nuclear fuel cycle applications. The "Others" category encompasses diverse mineral processing requirements, including boron, zinc, and specialty metals that require customized equipment solutions. Ganfeng Lithium's USD 980 million Mariana Project demonstrates the scale of lithium processing investments, with annual production capacity of 20,000 tons creating substantial equipment demand for processing plant infrastructure. The sector's evolution toward sustainable extraction methods drives demand for closed-loop systems and water recycling equipment, particularly critical in Argentina's arid lithium-producing regions where water conservation represents both environmental and operational imperatives.

By Equipment Type: Crushers Lead While Mills Accelerate

Crushers maintain the most significant equipment market share at 28.14% in 2024, reflecting their fundamental role in primary ore processing across Argentina's diverse mining operations. Yet, mills demonstrate the fastest growth trajectory at 9.58% CAGR through 2030 as operations optimize grinding circuits for improved recovery rates. The crusher segment's dominance stems from universal application requirements across surface mining operations, representing 71.06% of Argentina's mining activities, with primary crushers essential for initial ore size reduction in both lithium brine processing and complex rock mining applications. Mills' experience accelerated demand growth through energy-efficient grinding solutions, including Vertimill systems and HPGR technologies that achieve superior energy performance compared to conventional ball mills. Conveyors represent critical infrastructure components for Argentina's large-scale mining operations, with belt conveyor systems essential for material transport across extensive open-pit operations in remote locations.

Drills and breakers serve specialized functions in exploration and production phases, with automated drilling systems gaining traction as mining companies prioritize worker safety in hazardous underground environments. Screens complete the primary processing equipment category, with vibrating screen technologies essential for material classification and sizing across mineral processing circuits. The "Others" category encompasses specialized equipment, including flotation cells, thickeners, and filtration systems for specific mineral processing requirements. Metso Corporation's 2024 financial performance, showing EUR 5,140 million in orders despite 2% decline, reflects global mining equipment market dynamics that influence Argentina's procurement patterns. Equipment suppliers increasingly offer integrated solutions that combine multiple processing stages, with modular designs enabling flexible deployment across Argentina's diverse mining environments and operational scales.

By Mining Method: Surface Operations Dominate Infrastructure Demand

Surface mining operations command 71.06% market share in 2024 and maintain the fastest growth rate at 7.47% CAGR through 2030, driven by Argentina's lithium brine deposits and large-scale copper porphyry systems that favor open-pit extraction methods. The surface mining dominance reflects geological characteristics of Argentina's mineral deposits, with lithium brines requiring extensive evaporation pond infrastructure and copper porphyries necessitating large-scale earthmoving equipment for overburden removal. Open-pit operations create substantial equipment demand for primary crushers, conveyor systems, and material handling infrastructure that can process high-tonnage throughput requirements characteristic of Argentina's world-class mineral deposits. The Agua Rica Integrated Project in Catamarca exemplifies surface mining equipment requirements, with proposed 110,000 tons per day ore processing and 190,000 tons per day waste handling, creating massive equipment procurement opportunities.

Underground mining represents 28.94% market share, serving specialized applications including high-grade gold deposits and deep copper mineralization where surface extraction becomes economically unfeasible. Underground operations require different equipment specifications, including Load-Haul-Dump (LHD) machines, underground crushers, and ventilation systems designed for confined space operations. The mining method segmentation reflects Argentina's geological diversity, with surface methods predominating in the lithium triangle and northern copper belt, while underground applications concentrate in established gold mining districts. Barrick's Veladero operation demonstrates surface mining equipment evolution, with heap leach facility commissioning extending mine life beyond 10 years through optimized processing infrastructure. Equipment suppliers must maintain dual capability portfolios to serve both surface and underground applications, with increasing emphasis on autonomous and remote-controlled systems that improve safety across both mining methods.

By Automation Level: Semi-Automated Leads While Fully Automated Surges

Semi-automated equipment holds 54.27% market share in 2024, representing the current industry standard where human operators work alongside automated systems to optimize safety and productivity, while fully automated solutions achieve 13.23% CAGR through 2030 as mining companies pursue zero-entry mining concepts. The automation evolution reflects Argentina's mining sector maturation, with established operations upgrading legacy equipment while new projects incorporate advanced automation from initial development phases. Manual operations maintain relevance in specialized applications and smaller-scale mining activities, yet face declining market share as labor costs increase and safety regulations tighten across Argentina's remote mining locations. The transition toward full automation accelerates through equipment supplier innovations, with Epiroc's autonomous mining portfolio demonstrating 42% battery-electric availability that addresses both automation and sustainability requirements.

Fully automated equipment growth reflects mining companies' strategic priorities around worker safety, operational efficiency, and remote monitoring capabilities essential for Argentina's challenging operating environments. The Autonomous Collaborative Mining paradigm enables human-machine cooperation where operators provide strategic oversight while automated systems handle routine and hazardous tasks. Semi-automated systems balance operational control and safety enhancement, allowing the operators to maintain decision-making authority while benefiting from automated safety interlocks and process optimization. The automation progression creates equipment replacement cycles as mining companies upgrade from manual to semi-automated and eventually fully computerized systems, generating sustained equipment demand across multiple technology generations. Equipment suppliers demonstrating measurable safety improvements and operational efficiency gains through automation technologies secure competitive advantages in Argentina's evolving mining equipment market.

Geography Analysis

Catamarca, at 24.18% revenue share in 2024, is the undisputed equipment epicenter owing to concurrent lithium and copper project build-outs. The province’s 10.13% CAGR through 2030 outpaces national growth, powered by Rincon, Agua Rica, and numerous juniors consolidating brine tenements. Catamarca’s corridor rail upgrade, slated for completion in 2027, will lower inbound freight costs, enabling OEMs to deliver pre-assembled mill shells that previously exceeded road weight limits.

Jujuy and Salta together account for an additional 31% of 2024 revenues, anchored by Olaroz, Cauchari, and Mariana. Governmental alignment on royalty structures has streamlined multi-site procurement, prompting Rio Tinto and Ganfeng to negotiate province-wide service contracts that guarantee spare-part availability within 48 hours. San Juan ranks next, leveraging decades of gold mining know-how; new copper porphyry finds are reviving demand for larger-diameter grinding mills, conveyor extensions, and tailings filtration.

Santa Cruz and “Rest of Argentina” provinces collectively supply the balance. Patagonia Gold’s 746,000-ounce Calcatreu project will introduce new demand for gravity concentration spirals and detoxification reactors in Rio Negro by 2028. Mendoza’s PSJ Cobre Mendocino brings 40,000 t/y fine copper output, driving eastward growth of the supply chain toward the Andean foothills. OEMs capable of maintaining regional depots across this vast geography are reducing downtime and earning multi-year maintenance contracts, strengthening the resilience of the Argentina mineral processing equipment market.

The mineral processing equipment market is assessed by Mordor Intelligence through a multi-layered geographic lens, with detailed country-level analysis for Brazil, Canada, Oman, Egypt, Morocco, South Africa, Italy, Saudi Arabia, and Australia.

Competitive Landscape

Argentina's mineral processing equipment market exhibits fragmented competition with U.S. suppliers commanding 75% market share, creating opportunities for established international players while challenging local and regional competitors to differentiate through specialized services and rapid response capabilities. The competitive intensity reflects diverse customer requirements across lithium brine processing, copper porphyry operations, and precious metal extraction, with equipment suppliers requiring broad technology portfolios to serve multiple mineral processing applications. Market fragmentation enables niche players to establish strongholds in specialized equipment categories. At the same time, larger suppliers leverage economies of scale and comprehensive service networks to maintain dominant positions across primary processing equipment segments.

Strategic patterns emphasize technology differentiation and energy efficiency improvements, with suppliers increasingly competing on total cost of ownership rather than initial equipment pricing, particularly relevant for Argentina's remote mining locations where operational efficiency directly impacts profitability. White-space opportunities exist in automation retrofits for legacy facilities and modular processing solutions for junior miners, with digital transformation creating new competitive battlegrounds around IoT integration, predictive maintenance, and remote monitoring capabilities.

FLSmidth's MissionZero program, targeting zero-emissions mining by 2030, demonstrates how sustainability commitments create competitive differentiation in equipment procurement decisions. Emerging disruptors focus on specialized technologies, including direct lithium extraction systems and energy-efficient comminution circuits, leveraging Argentina's unique geological characteristics to develop tailored solutions that challenge conventional processing approaches.

Argentina Mineral Processing Equipment Industry Leaders

-

Metso

-

FLSmidth

-

Sandvik AB

-

The Weir Group PLC

-

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: McEwen Copper applied for Los Azules copper project admission to Argentina's Large Investment Incentive Regime (RIGI), involving USD 2.7 billion investment with construction potentially starting in early 2026. The project aims to benefit from reduced corporate tax rates and regulatory stability, positioning it among the top 10 copper projects globally.

- May 2025: Argentina approved its first mining project under the RIGI incentive regime, valued at USD 2.5 billion, marking a significant milestone for the country's investment attraction efforts.

- April 2025: Patagonia Gold announced USD 40 million investment agreement with Black River Mine Inc. for the Calcatreu Project in Rio Negro province, with 746,000 ounces of gold equivalent in measured and indicated resources.

Argentina Mineral Processing Equipment Market Report Scope

| Lithium |

| Copper |

| Gold and Silver |

| Iron |

| Uranium |

| Others |

| Crushers |

| Mills |

| Conveyors |

| Drills and Breakers |

| Screens |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| Jujuy |

| Salta |

| Catamarca |

| San Juan |

| Santa Cruz |

| Rest of Argentina |

| By Mineral Mining Sector | Lithium |

| Copper | |

| Gold and Silver | |

| Iron | |

| Uranium | |

| Others | |

| By Equipment Type | Crushers |

| Mills | |

| Conveyors | |

| Drills and Breakers | |

| Screens | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated | |

| By Geography | Jujuy |

| Salta | |

| Catamarca | |

| San Juan | |

| Santa Cruz | |

| Rest of Argentina |

Key Questions Answered in the Report

How large is Argentina’s mineral processing equipment market in 2025?

It is valued at USD 61.16 million and is forecast to expand at 7.24% CAGR to USD 86.73 million by 2030.

Which mineral drives the strongest equipment demand in Argentina?

Lithium, representing 42.39% of 2024 revenue and posting an 11.87% CAGR through 2030.

Why are mills growing faster than crushers in new orders?

Plants are switching to energy-efficient Vertimill and HPGR-SAG hybrids, lifting mill demand at 9.58% CAGR.

What federal incentive supports large mining CAPEX in Argentina?

The Large Investment Incentive Regime (RIGI) grants 30-year fiscal stability and reduced corporate tax for projects over USD 200 million.

How is automation impacting equipment purchasing?

Fully automated assets, though still niche, are scaling at 13.23% CAGR as miners seek zero-entry operations and lower maintenance costs.

Which province accounts for the highest share of equipment sales?

Catamarca leads with 24.18% of national revenue in 2024 and a 10.13% projected CAGR through 2030.

Page last updated on: