France Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

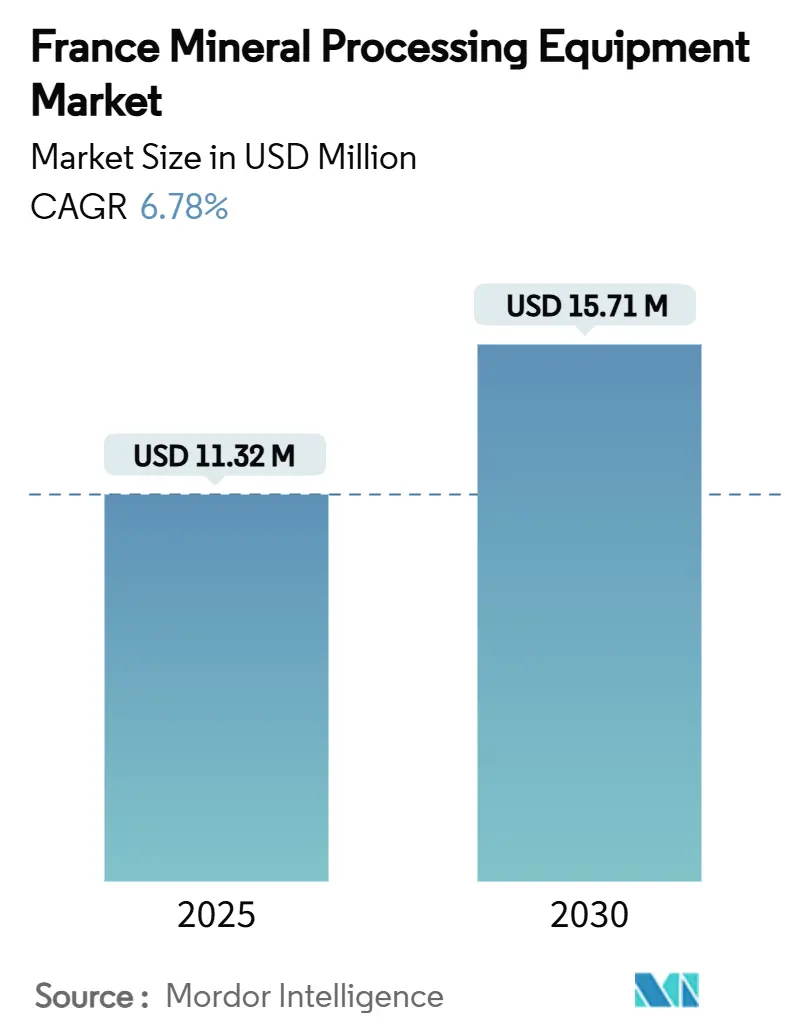

| Market Size (2025) | USD 11.32 Million |

| Market Size (2030) | USD 15.71 Million |

| Growth Rate (2025 - 2030) | 6.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Mineral Processing Equipment Market Analysis by Mordor Intelligence

The France Mineral Processing Equipment Market size is estimated at USD 11.32 million in 2025, and is expected to reach USD 15.71 million by 2030, at a CAGR of 6.78% during the forecast period (2025-2030). Ongoing investments under the France 2030 program, alignment with the EU Critical Raw Materials Act, and almost three-fifths tax credits for green industrial technology are accelerating equipment upgrades across the country. Increasing pressure to meet the Carbon Border Adjustment Mechanism (CBAM) deadlines from 2026 drives early adoption of low-carbon crushers, conveyors, and digital control systems. Continuous replacement of aging fleets, expansion of lithium and rare-earth projects such as Imerys’ EMILI and Caremag’s Lacq facility, and the rapid uptake of predictive-maintenance platforms underpin replacement demand. The French mineral processing equipment market is further buoyed by labor shortages pushing operators to automate handling, loading, and grinding lines.

Key Report Takeaways

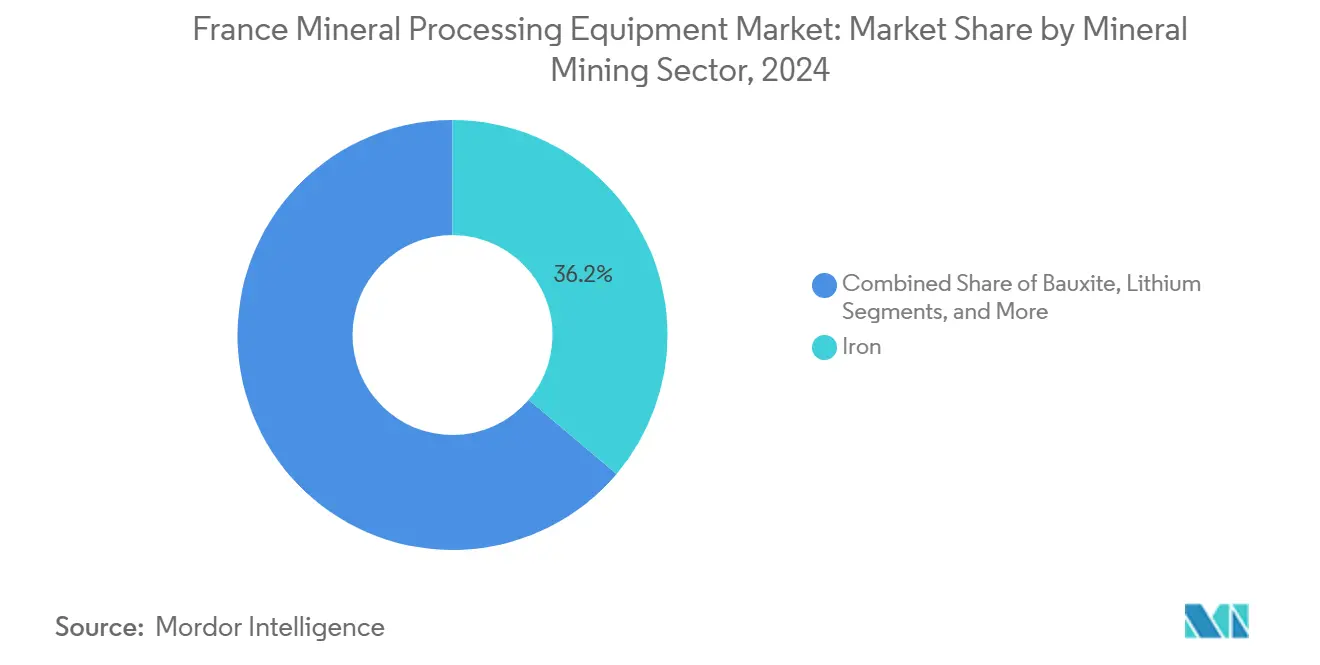

- By mineral mining sector, Iron led with 36.17% of the France mineral processing equipment market share in the mineral mining sector in 2024, while lithium posted the quickest expansion at a 6.83% CAGR through 2030.

- By equipment type, crushers commanded a 32.21% share of the France mineral processing equipment market in 2024, whereas conveyors are slated to grow at a 6.91% CAGR by 2030.

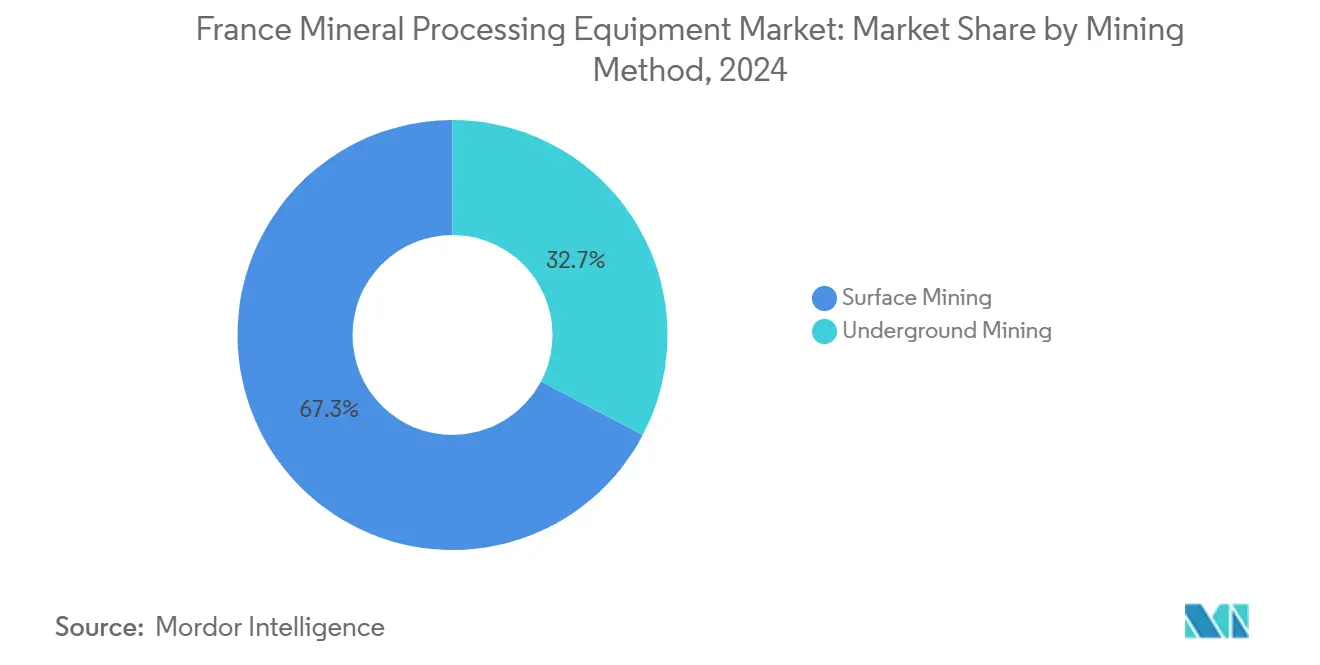

- By mining method, surface operations captured 67.31% of the France mineral processing equipment market size in 2024; underground techniques hold the top growth outlook at 6.88% CAGR to 2030.

- By automation level, semi-automated systems held a 47.84% share of the France mineral processing equipment market in 2024. However, fully automated units are forecast to advance at a 6.93% CAGR over the same horizon.

Understanding the full system requires moving beyond France boundaries into a wider international view. Mordor Intelligence captures the global mineral processing equipment market scope in its worldwide coverage.

France Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Demand for Critical Battery Minerals | +1.8% | National, with concentration in Massif Central and Vosges regions | Medium term (2-4 years) |

| Rapid Adoption of Automation and Digitalization | +1.5% | National, with early adoption in major industrial centers | Medium term (2-4 years) |

| Government Incentives | +1.2% | National, enhanced in designated industrial zones | Short term (≤ 2 years) |

| EU CBAM Compliance Push | +1.1% | National, with spillover effects to EU trading partners | Short term (≤ 2 years) |

| Increasing Maintenance and Replacement | +0.9% | National, concentrated in traditional mining regions | Long term (≥ 4 years) |

| Repurposing of Abandoned Mine Sites | +0.7% | Limousin, Provence, and Languedoc regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Demand for Critical Battery Minerals

Surging EV cell demand across Europe places lithium, cobalt, and nickel at the center of France's mineral processing equipment market expansion. The Infravia fund funnels capital toward domestic hydroxide and sulfate refineries, pushing orders for high-temperature kilns and mica concentrators suited to Imerys’ EMILI project, which targets 34,000 t/y lithium hydroxide from 2028[1]“EMILI Lithium Project,” Imerys, imerys.com . The France-Japan Caremag plant in Lacq channels to heavy rare-earth separation, requiring solvent-extraction columns and hybrid membrane filters. Updated BRGM geophysical surveys financed in 2025 widen the exploration footprint across five regions, guaranteeing future equipment pipelines[2]“Strategic Minerals Inventory,” Bureau de Recherches Géologiques et Minières, brgm.fr . These initiatives lift throughput capacity and strengthen the French mineral processing equipment market.

Rapid Adoption of Automation & Digitalization

Eramet’s Plant 4.0 program blends AI, edge-sensor networks, and predictive analytics, extending overall equipment effectiveness and slashing downtime across manganese and nickel lines[3]“Plant 4.0 Program,” Eramet, eramet.com . Sandvik’s AutoMine haulage clusters have entered French quarries, offsetting labor gaps while raising payload hours. ABB’s eMine conveyor drives and trolley assist cut on-site CO₂ by up to 70%, a benchmark now embedded in CBAM compliance audits. Battery-electric drills and LHDs trim ventilation costs in underground headings, widening profit margins. Demand for data-rich retrofits intensifies, fueling software and sensor sales in France's mineral processing equipment market.

Government Incentives for Sustainable Mining Modernization

A green industry investment credit grants around three-fifths relief on capital spent for low-emission mills, electric haulage, and AI-driven control rooms, stimulating swift conversion of legacy lines. The France 2030 plan has disbursed EUR 13.8 billion out of a EUR 54 billion envelope, backing upgrades such as Constellium’s Neuf-Brisach rolling plant and geothermal lithium pilot rigs in Alsace. Subsidies of EUR 5,000 per industrial heat pump catalyze electrified leaching circuits, enabling operators to meet France’s pledge to cut half the emissions of its 50 heaviest sites by 2030. The financial shield accelerates procurement within the French mineral processing equipment market.

Increasing Maintenance & Replacement of Aging Equipment Fleets

A century of extraction left France with mills, crushers, and feeders exceeding design life. Studies place optimal replacement after a decade and half; many French units cross that threshold by 2025. Aging assets coexist with several job openings in manufacturing, compelling firms to seek remote-monitoring kits that permit minimal on-site staffing. Exploration permits issued for dormant metallic deposits since 2013 re-open shafts that require brand-new circuits rather than patchwork, driving orders for modular skids and plug-and-play crushing plants. French OEMs answer with retrofit classifiers and energy-efficient HPGR modules, sustaining the French mineral processing equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental Permitting and Emissions Standards | -1.4% | National, with heightened scrutiny in sensitive ecological zones | Short term (≤ 2 years) |

| Escalating Capital Expenditure | -1.1% | National, with particular impact on smaller operators | Medium term (2-4 years) |

| Supply-Chain Fragility | -1.0% | National, with dependency on Asian and North American suppliers | Medium term (2-4 years) |

| Limited Skilled Labor for Advanced Processing Technologies | -1.0% | National, concentrated in industrial regions and technical centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Permitting & Emissions Standards

Revisions to the Mining Code in 2022 fold all new plants under the ICPE regime, forcing complete ecological assessments, community hearings, and biodiversity offsets before commissioning. Approval windows can stretch almost a year or more, delaying cash flows and dampening short-term orders for the French mineral processing equipment market. CBAM adds a carbon-reporting layer by 2026; processors must document electrification levels and green-power intensity, compelling extra metering devices. Permit hurdles rise sharply in Natura 2000 or wetland zones, where NGOs carry judicial influence, boosting pre-development costs and stalling greenfield crusher installations.

Escalating Capital Expenditure and Operating Costs

Supply-chain snarls since 2022 have raised landed prices for crushers, screens, and motors by 15–25%. Electricity tariffs climbed on volatile LNG inputs, eroding margins for energy-hungry comminution circuits. Skilled-labor premiums swell payrolls as firms overbid to fill 76,000 specialized technician vacancies. Higher Euribor rates inflate borrowing costs, making smaller operators reluctant to green-light expansion. Logistics bills for importing spare parts, particularly electrified drivetrain components add volatility. Collectively, these factors weigh down purchasing decisions in the French mineral processing equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Iron Dominance Amid Lithium Surge

Iron retained a 36.17% France mineral processing equipment market share in 2024 due to deep-rooted steel value chains, blast-furnace revamps, and supportive hydrogen-based direct-reduction pilots such as thyssenkrupp’s retrofits. Parallel European decarbonization goals obligate pellet plants to adopt water-efficient classifiers and high-pressure grinding rolls. Lithium pipelines bring the highest upside: Imerys’ EMILI alone underpins a 6.83% CAGR, prompting orders for slurrying pumps, attrition scrubbers, and mica flotation cells that withstand higher abrasiveness than iron-ore circuits. Bauxite, copper, and rare-earth ventures in Limousin, Provence, and Languedoc maintain modest but strategic positions.

Exploration permits granted in 2024 for polymetallic veins revive dormant shafts, elevating demand for hybrid crushers and column flotation suited to complex ores. IB2’s high-silica bauxite processing proof-of-concept exports French IP globally, providing a back-loop of engineering royalties that finance domestic upgrades. The sector’s diversification cushions volatility tied to steel cycles and improves national supply resilience, reinforcing mid-term revenue visibility for the French mineral processing equipment market.

By Equipment Type: Crusher Leadership Challenged by Conveyor Innovation

Crushers owned 32.21% of the France mineral processing equipment market size in 2024 on the back of indispensable primary size-reduction tasks. Weir Group’s GBP 53 million HPGR award in July 2024 validated appetite for energy-efficient comminution. Yet conveyors race ahead at a 6.91% CAGR, fueled by fully-automated pit-to-plant material flows and steep CO₂ abatements. ABB’s gearless systems eliminate diesel haul trucks, displaying almost four-fifths of emissions cut benchmark adopted by French quarries. Feeders and drills consolidate via electrification; remote-controlled breaker booms address safety mandates.

FLSmidth’s Q1 2025 mining service revenue rise confirm sustained upgrade cycles anchored around MissionZero platforms such as REFLUX and coarseAIR flotation. Optical sorters, AI-guided ore tracking, and 5G-enabled condition monitoring occupy the “Others” pocket, widening the solution set and upping aftermarket value density. While crushers keep the lion’s share, conveyor investments reshape capex allocation and inject new automation layers into the French mineral processing equipment market.

By Mining Method: Surface Dominates Despite Underground Momentum

Surface mining represented 67.31% France mineral processing equipment market size in 2024, reflecting historical quarrying patterns and lower unit costs per tonne. However, underground projects shoot ahead at 6.88% CAGR through 2030 on environmental acceptance and ore-body depth. Imerys’ EMILI uses underground stopes to access high-grade lithium while minimizing surface footprints, requiring battery-electric loaders and low-profile jaw crushers. Komatsu’s WX04B battery LHD, launched in 2024, aligns with narrow-vein parameters typical of French hard-rock contexts. Abandoned coal and potash galleries are re-evaluated for rare-earth recycling, demanding specialized slurry pipelines and pick-and-carry crushers.

Battery-electric mobility slashes ventilation energy and associated costs, moving underground opex curves closer to surface benchmarks. Remote operation centers in Lyon and Paris manage fleets across multiple headings, unlocking scale economies. Surface fleet retrofits remain important particularly for granite and limestone, yet underground expenditures increasingly shape growth trajectories for the France mineral processing equipment market.

By Automation Level: Semi-Automated Systems Lead Transition to Full Autonomy

Semi-automated units, controlling 47.84% share in 2024, deliver tangible productivity gains without relinquishing manual oversight. Metso Plus programs supply AI-augmented dashboards that overlay predictive alerts onto operator screens, enhancing throughput and liner change-out scheduling. Manual modes persist in artisanal or test-bench applications requiring flexibility and rapid parameter swings. Fully automated installations, rising at 6.93% CAGR, capitalize on labor scarcity and safety demands. Epiroc recorded French orders for autonomous drilling rigs that self-navigate blast patterns and feed fragmentation data into plant control layers.

Government digital-transformation grants remove adoption barriers, while the CBAM scoreboard incentivizes real-time carbon disclosures only possible through fully networked sensors. An integrated architecture combining autonomous haulage, smart conveyors, and cloud analytics renders payback within three to five years. Increasing interoperability between OEM platforms further accelerates the shift to full autonomy across the French mineral processing equipment market.

Geography Analysis

Northern steel corridors, Alsace geothermal fields, and Occitanie rare-earth clusters anchor France's mineral processing equipment demand. Surface quarries in Hauts-de-France dominate iron and aggregates, leveraging existing rail arteries to serve Benelux steel mills. Eramet’s Ageli initiative in the east plans more than 10 kt/y lithium carbonate from geothermal brines, spurring specialized ion-exchange columns and high-density polyethylene piping.

Massif Central and Vosges record the highest uptick in exploration budgets under BRGM’s survey, creating forward pipelines for small-scale crushing and drill-core assays. Limousin’s four polymetallic permits, approved in 2024, reroute capital to modular flotation cells that can handle copper-gold concentrates within tight environmental envelopes. Provence and Languedoc exploit dormant bauxite landscapes where hybrid alumina-rare-earth flowsheets call for adaptable separators.

France’s cross-channel ports and Rhine corridor provide economically favorable routes for imported concentrates needing EU CBAM-compliant processing, cementing the country as a logistical hub for neighboring markets. The French mineral processing equipment market, therefore, benefits not only from domestic ore bodies but also from transit and toll-processing volumes arriving from Scandinavia, Iberia, and North Africa.

Mordor Intelligence examines the mineral processing equipment market across diverse other regional markets as well, offering granular country-level perspectives for Turkey, Italy, Argentina, Japan, Mexico, Oman, Egypt, Morocco, and South Africa and more.

Competitive Landscape

Global major players Metso, FLSmidth, Sandvik, and Weir command product breadth from crushing to automation services, yet together they hold only about one-third of shipments, indicating moderate concentration. FLSmidth’s adjusted margin sustained by aftermarket packages and digital twins. Sandvik fortifies its share through AutoMine and RockPulse drilling analytics, while Weir pursues almost one-fifths operating-margin goal via the Performance Excellence program.

Domestic integrators emphasize niche automation and retrofit expertise, often acting as system partners to global OEMs. Start-ups specializing in battery-electric drivetrain conversions and AI-powered ore sorting are emerging disruptors. Patent intensity in autonomous control systems and energy-efficient classifiers marks a battleground for future differentiation.

Sustainability branding is paramount; vendors routinely pledge net-zero manufacturing targets to satisfy CBAM-aware buyers. Consolidation is plausible as smaller workshops struggle with capex inflation and compliance overheads. Still, the current balance favors competitive project bidding and choice diversity for end users of the French mineral processing equipment market.

France Mineral Processing Equipment Industry Leaders

Metso Outotec

Sandvik AB

FLSmidth A/S

Weir Group PLC

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Japan and France committed EUR 216 million to build the Caremag heavy-rare-earth plant in Lacq, which will meet 20% of Japan’s dysprosium and terbium requirements.

- March 2025: The European Commission shortlisted 47 Strategic Projects across 13 Member States, allocating EUR 22.5 billion to boost domestic critical-material processing.

- March 2025: Metso introduced a sustainable copper sulfide concentrate leach process, achieving high copper recovery without smelting.

- February 2025: BRGM began a EUR 53 million mineral inventory program in five regions to map lithium, cobalt, and rare-earth potential.

France Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Others |

| Crushers |

| Feeders |

| Conveyors |

| Drills & Breakers |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Others | |

| By Equipment Type | Crushers |

| Feeders | |

| Conveyors | |

| Drills & Breakers | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

What is the current value of the French mineral processing equipment market?

It is valued at USD 11.32 million in 2025, with a forecast CAGR of 6.78% toward 2030.

Which mineral segment is growing the fastest in France?

Lithium leads growth, expanding at a 6.83% CAGR on the back of projects such as Imerys’ EMILI.

Which equipment category records the highest market share?

Crushers held 32.21% of 2024 revenue, driven by their central role in primary comminution.

How will CBAM influence equipment demand?

The mechanism enforces low-carbon production, accelerating electrified conveyors and autonomous haulage orders.

Are underground mining methods gaining relevance?

Underground techniques grow at a 6.88% CAGR due to lithium extraction and urban-mining projects.

Page last updated on: