Mexico Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

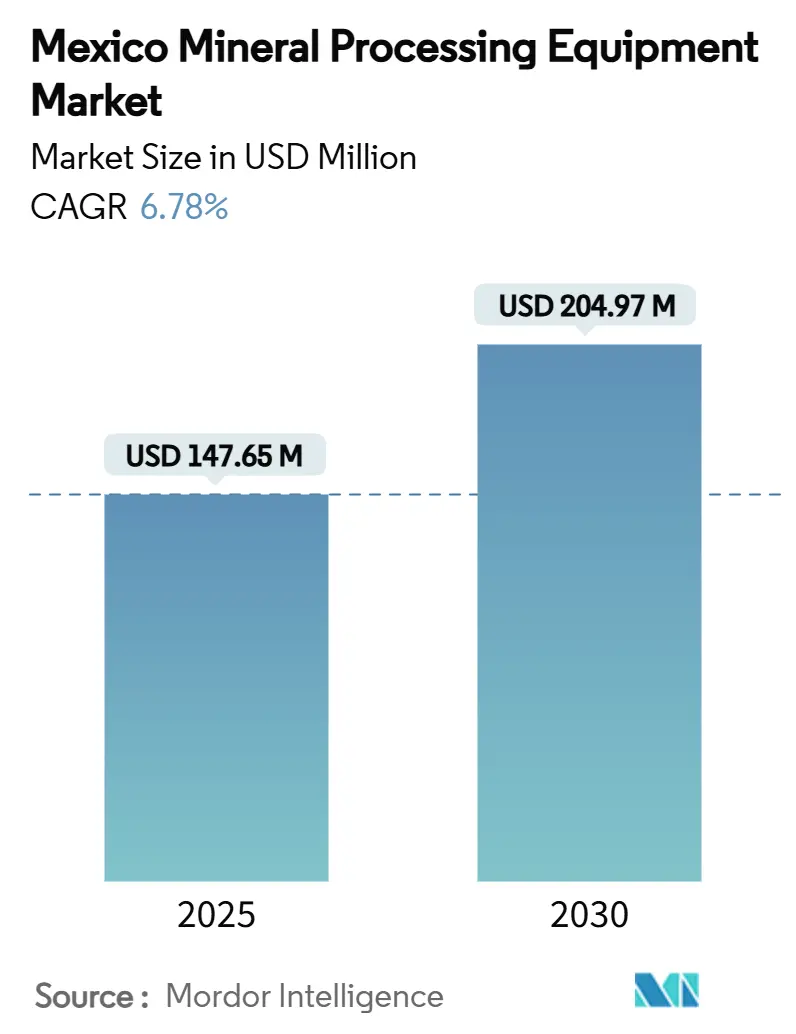

| Market Size (2025) | USD 147.65 Million |

| Market Size (2030) | USD 204.97 Million |

| Growth Rate (2025 - 2030) | 6.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Mexico mineral processing equipment market size stands at USD 147.65 million in 2025 and is projected to rise to USD 204.97 million by 2030, advancing at a 6.78% CAGR. Mexico’s status as a preferred near-shoring base for North American manufacturing, wide-ranging federal tax incentives, and a renewed focus on lithium and copper beneficiation underpin this outlook. I processing remains the structural backbone of the Mexico mineral processing equipment market. Yet, lithium projects anchored in Sonora are generating the fastest incremental demand for specialized flotation and roasting systems. Automation investments are accelerating as operators shift from semi-automated circuits toward fully digital plants to comply with tightening SEMARNAT standards and to offset skilled-labor shortages. Global suppliers are deepening local footprints, attracted by Mexico’s USD 36.28 billion 2023 foreign-direct-investment influx and brownfield expansions favoring high-value aftermarket contracts. At the same time, chronic water scarcity in northern states redirects capital toward dry stack tailings, high-efficiency thickeners, and closed-loop water circuits, reshaping procurement priorities across the Mexico mineral processing equipment market.

Key Report Takeaways

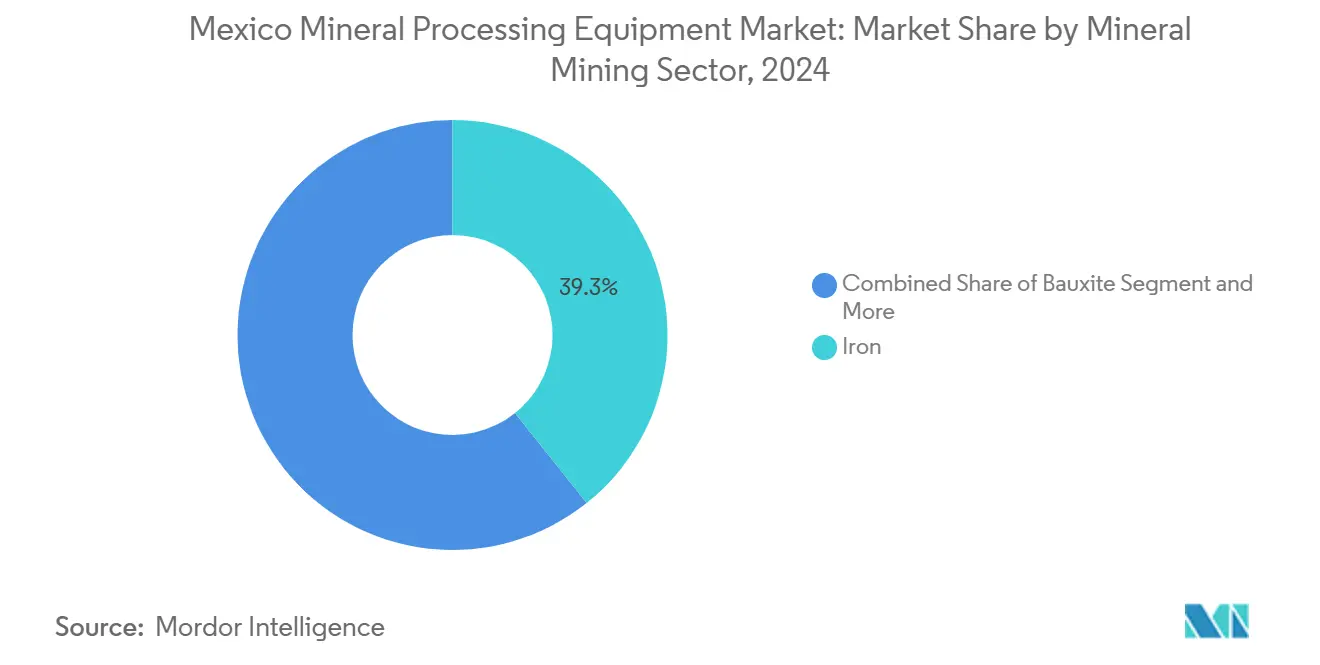

- By mineral mining sector, iron-ore beneficiation led with 39.27% of the Mexico mineral processing equipment market share in 2024, while lithium processing is forecast to expand at a 9.46% CAGR through 2030.

- By equipment type, crushers dominated with 29.72% share of the Mexico mineral processing equipment market size in 2024, whereas drills and breakers record the highest projected CAGR at 8.23% to 2030.

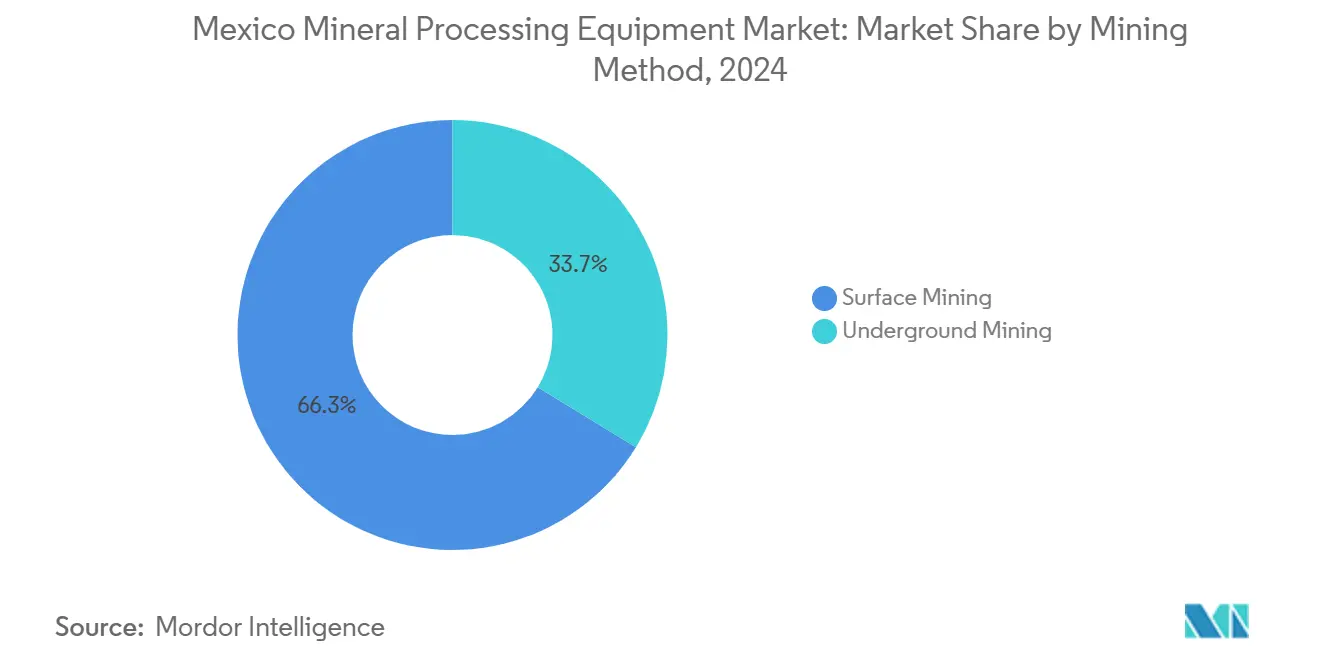

- By mining method, surface operations accounted for 66.26% of the Mexico mineral processing equipment market size in 2024, but underground-processing demand is advancing at a 9.28% CAGR to 2030.

- By automation level, semi-automated systems held 47.74% of the Mexico mineral processing equipment market share in 2024, while fully-automated plants are set to grow at a robust 10.37% CAGR through 2030.

Mexico contributes to a system defined not by any single country or region but by the interaction of many. The global mineral processing equipment market data by Mordor Intelligence represents that combined structure.

Mexico Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Iron-Ore, Copper & Lithium Output | +1.8% | National, concentrated in Sonora, Zacatecas, Coahuila | Medium term (2-4 years) |

| Strong Brown-Field Expansion Pipeline | +1.4% | Northern states, particularly Sonora and Chihuahua | Medium term (2-4 years) |

| Federal Tax Incentives & Mining Reforms | +1.2% | National, with enhanced benefits in Oaxaca, Veracruz, Yucatán | Short term (≤ 2 years) |

| EV Supply Chain Near-Shoring Boost | +1.1% | Central Mexico, automotive corridor states | Medium term (2-4 years) |

| Digital Automation for Legacy Mills | +0.9% | National, prioritizing established mining regions | Long term (≥ 4 years) |

| Tailings-Dam Risk Driving Re-Processing | 0.4% | National, focusing on legacy mining sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Iron-Ore, Copper and Lithium Output in Mexico

Mexico’s bulk and battery-metal production resurgence is translating directly into equipment orders. Buenavista Zinc, now 99% complete, will add 100,000 t of zinc and 20,000 t of copper annually, requiring high-throughput crushers, SAG mills, and bulk-handling conveyors[1]“Proyecto Buenavista Zinc Avanza 99%,”, Grupo México, gmexico.com. Simultaneously, confirmed reserves of 1.7 million t of lithium have moved Sonora to the forefront of North American battery-grade feedstock, spurring demand for calcining, roasting, and hydrometallurgical circuits designed explicitly for clay-hosted ore bodies. Clay-lithium separation technology has reached 95% pilot-scale completion, signaling imminent procurement of commercial-scale flotation and leaching packages[2]“Reservas Nacionales de Litio,”, Secretaría de Energía, gob.mx. Iron-ore giants such as Peña Colorada, which supplies 30% of domestic steel mills, continue to modernize primary crushing and wet-screening trains to preserve throughput as ore hardness rises. The combined surge across ferrous and critical-mineral streams anchors volume demand within the Mexico mineral processing equipment market.

Strong Pipeline of Brown-Field Plant Expansions

Over USD 15 billion in brownfield work is under construction or engineering review, signifying a strategic pivot away from greenfield risk. Southern Copper’s Pilares and Buenavista twin upgrades add over 89,000 t of annual copper concentrate capacity and mandate seamless integration of new ball-mill lines with legacy flotation trains. Torex Gold’s Media Luna project achieved its first copper concentrate in March 2025 using a hybrid processing flowsheet incorporating paste backfill and refurbished regrind mills to maximize existing infrastructure. Brownfield schemes usually demand more customized control-system engineering and bespoke wear-part packages than greenfield builds, thereby lifting average order values for OEMs active in the Mexico mineral processing equipment market.

Federal Tax Incentives and Mining-Friendly Reforms

The January 2025 executive decree allows accelerated depreciation of 35%-91% on new fixed assets and a further 25% deduction on workforce-training costs, with MXN 30 billion earmarked for claimable credits. The fiscal carrot is especially powerful for operators evaluating high-ticket grinding, thickening, and automation systems, since up-front tax relief shortens payback periods. Complementary regional programs along the Isthmus of Tehuantepec permit 100% income-tax credits for three years and immediate 100% asset depreciation, tilting equipment tenders toward installations inside designated corridors[3]“Decreto de Estímulos Fiscales Plan México,”, Gobierno de México, dof.gob.mx. Suppliers able to localize assembly or after-sales hubs in these zones gain a cost edge and often lock in multi-year parts agreements. As a result, the incentive stack is accelerating planning pipeline conversion into signed purchase orders across the Mexico mineral processing equipment market.

Digital-Automation Retrofits for Legacy Mills

Mill-wide digitalization is proving a low-capex lever for throughput and recovery gains. A large Mexican copper concentrator that embedded AI-enabled expert control into its SAG circuit lifted throughput 5% without structural plant upgrades. Similar success stories around model-predictive control and online particle-size measurement have spurred a wave of retrofit scopes covering instrumentation, fiber-optic networks, and cloud-based analytics layers. Vendors such as ANDRITZ and Metso are bundling retro-fits with subscription performance guarantees that tie payments to verified energy savings, a model well suited to the semiautomated profile dominating today’s Mexico mineral processing equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity Price Volatility Limiting CAPEX | -1.1% | National, affecting all mineral processing segments | Short term (≤ 2 years) |

| Chronic Water Scarcity in North | -0.9% | Northern Mexico, concentrated in Sonora, Chihuahua, Coahuila | Long term (≥ 4 years) |

| Stricter SEMARNAT Emission Standards | -0.8% | National, with stricter enforcement in urban-adjacent operations | Short term (≤ 2 years) |

| Community & Indigenous Permit Challenges | -0.6% | Southern states, particularly indigenous territories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility Curbing CAPEX Plans

Base-metal prices swung by more than 20% during 2024-2025, disrupting internal rate-of-return thresholds for multi-year plant expansions. Operators are responding by phasing capacity additions into modular tranches and favoring rental or lease-to-own terms for mobile crushing and screening gear. Suppliers that can underwrite commodity-linked payment schedules or embed production-based royalties into contracts are gaining traction. The volatile backdrop tempers headline spending yet concurrently boosts demand for flexible, quick-install equipment lines that reduce capital lock-in—an emerging sub-theme within the Mexico mineral processing equipment market.

Tightening SEMARNAT Air and Water Emission Standards

The 2025 launch of the VEA electronic platform ushers in real-time compliance auditing, compelling processors to install higher-rated dust collectors, enclosure hoods, and stack-monitoring probes[4]“Plataforma VEA,”, Secretaría de Medio Ambiente y Recursos Naturales, semarnat.gob.mx. New NOM-172 rules extend continuous monitoring to PM10 and PM2.5 thresholds, conditions that attract enclosed transfer points and water-mist suppression skids around primary crushing. For hydrometallurgy, updated NOM-147 soil-contamination criteria mandate lower residual arsenic and cadmium in tailings, leading plants to adopt high-density thickeners and paste backfill to cut seepage. Non-compliant units risk suspension, forcing even cash-strapped operators to prioritize environmental retrofits across the Mexico mineral processing equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Iron Dominance Shapes Procurement Playbooks

Iron-ore beneficiation maintained 39.27% of 2024 revenue, setting standardized flowsheets built around three-stage crushing, ball-mill grinding, and wet magnetic separation. That installed base drives stable parts and liner demand and anchors foundation orders for the Mexico mineral processing equipment market size attributed to bulk-commodity circuits. Lithium stands out as the fastest-advancing stream at 9.46% CAGR to 2030. Sonora’s clay-type deposits require roasting, fine grinding, and selective leach/precipitation units that differ markedly from brine or hard-rock lithium flowsheets, generating a specialized bid slate. Copper‐ and zinc-rich polymetallic ores in Zacatecas and Chihuahua add a third tier of demand centred on differential flotation trains. Together, these sub-sectors diversify order books and lessen the cyclical exposure that once tied equipment sales chiefly to iron tonnage.

With President Sheinbaum publicly backing lithium and copper value-addition, several juniors are fast-tracking pilot plants to secure offtake with battery and cable producers. Bacanora’s pilot line near Hermosillo demonstrates the high equipment intensity of calcine, roast, and carbonate-precipitation steps. These complex flowsheets help lift the Mexico mineral processing equipment market by favouring vendors who deliver integrated packages spanning kilns, gas scrubbers, and solvent-extraction circuits.

By Equipment Type: Crushers Hold the Lead While Drilling Accelerates

Crushing systems retained a 29.72% share of the Mexico mineral processing equipment market size in 2024, upheld by throughput upgrades at bulk-commodity concentrators and replacement cycles in aging gold mills. The cohort ranges from 1,000 t/h primary gyratories to compact, underground modular jaw units. Drills and breakers, posting an 8.23% CAGR outlook, benefit from the pivot to deeper ore bodies and the migration toward battery-electric rigs that ease ventilation loads in underground headings. Beyond the headline segments, demand for high-angle conveyors, air-classifiers, and hyper-saturated thickeners is climbing as plants chase smaller environmental footprints.

Local fabrication capacity is also rising. Bega Helicoidales now supplies screw conveyors and feeders compliant with ISO drive-train tolerances, shaving weeks off delivery for expansions in central Mexico. Concurrently, multinational OEMs are rolling out Mexico-assembled modules, a localization push that aligns with tariff-free trade under USMCA and keeps the Mexico mineral processing equipment market competitive.

By Mining Method: Surface Dominance Persists, Underground Pushes Higher

Surface facilities processed 66.26% of national ore in 2024. Their larger footprint favors high-capacity crushing stations, overland conveyors, and coarse-ore stockpiles that yield scale economies. Yet underground ore is forecast to grow at 9.28% CAGR to 2030, a shift propelled by depletion of shallow pits and social opposition to new surface excavations. Underground concentrators lean on compact, skid-mounted primary crushers and vertical stirred mills that fit within drift constraints. Such packages carry higher unit value and richer automation content, supporting revenue expansion even when bulk tonnage growth moderates.

Regulatory risk amplifies the trend. Draft reforms that contemplate curbs on new open-pit concessions have nudged operators like Alamos Gold to transition Puerto Del Aire to an underground plan entailing USD 165 million in specialized mucking, hoisting, and backfill systems. The resulting orders enhance the Mexico mineral processing equipment market as vendors tailor offerings for lower-profile, diesel-free underground operations.

By Automation Level: Semi-Automated Circuits Bridge Legacy and Digital Futures

Semi-automated lines, encompassing PLC-controlled pumps and partially computerised flotation banks, held 47.74% of 2024 turnover. These setups strike a balance between cost and control sophistication suited to Mexico’s mid-tier mines. Fully-automated facilities, however, are projected to expand at a 10.37% CAGR to 2030 as plants incorporate advanced process control, AI-driven ore-tracking, and autonomous hauling loops. Metso’s Skega Life rubber liners, promising 25% longer service life, typify how wear-part innovation underpins automation by extending campaign lengths between shutdowns.

Digital retrofits are spreading beyond flagship copper concentrators to midsize polymetallic mills, where cloud-based digital twins enable operators to run what-if scenarios and schedule maintenance by condition rather than by calendar. As this transition accelerates, aftermarket revenue tied to software licences and sensor upgrades is poised to become a larger slice of the Mexico mineral processing equipment market share.

Geography Analysis

Northern states—Sonora, Chihuahua, and Coahuila—absorb the lion’s share of capex, reflecting their mature infrastructure and proximity to United States smelters. Sonora alone hosts marquee copper and emerging lithium hubs that draw in high-capacity milling, solvent extraction, and battery-grade precipitation trains. The clustering effect simplifies spares logistics and supports local foundries that recast liners, advantages that translate into lower total cost of ownership for operators that buy within the Mexican mineral processing equipment market.

Central Mexico is climbing the demand curve on the back of the automotive corridor extending through Guanajuato, Querétaro, and Puebla. OEMs establishing EV component lines want secure domestic sources of cathode-grade copper and lithium carbonate, prompting integrated beneficiation projects within trucking distance of assembly plants. This geographic realignment tightens feedback loops between end-user quality requirements and upstream processing parameters, steadily upgrading equipment specifications toward cleaner concentrates and tighter grade control.

Southern states such as Oaxaca and Veracruz remain nascent but hold significant upside. Federal welfare corridors offer 100% corporate-tax relief for qualifying investments, an incentive likely to trigger feasibility work on copper-gold skarn and lateritic nickel deposits. Infrastructure outlays, exemplified by the USD 892 million refurbishment of nine hydro plants, reinforce the regional power grid and pave the way for grid-reliant concentrators. As permitting matures, the Mexican mineral processing equipment market is expected to see a new wave of tenders focused on modular plants that can be expanded as deposits are drilled.

The mineral processing equipment market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for Canada, Argentina, Egypt, Morocco, South Africa, Italy, Brazil, Saudi Arabia, and Australia, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The supplier field is moderately fragmented, illustrating a gradual shift toward consolidation. Metso’s investment in a Mexican service hub underscores the company's premium on rapid parts delivery and rebuild capabilities. FLSmidth maintains incumbency at large polymetallic plants by offering cradle-to-grave process packages—80% of Peñasquito’s concentrator operates on its technology. Sandvik’s 2025 battery-electric drill order from an Arizona border project signals its intent to lead the underground electrification niche that will influence future Mexican purchases.

Local and regional firms complement the landscape. Bega Maquinaria fabricates bulk-material screws, while Talleres y Aceros casts abrasion-resistant liners. Although individually niche, their responsiveness and peso-denominated pricing give them a share in brownfield expansions where import lead times are prohibitive. The ongoing USMCA tariff shield further incentivizes multinationals to assemble in Mexico, shrinking delivery windows and lowering landed costs.

Technology differentiation defines present competition. Dry stack tailings filters, advanced process-control algorithms, and wear-part monitoring sensors are the new battlegrounds. Suppliers can bundle these features into lifecycle service contracts to lock in recurring cash flow and deepen switching costs for mine operators. As electrified haulage and water-recycling standards become mainstream, the Mexican mineral processing equipment market will likely reward OEMs capable of integrating energy-storage systems, high-pressure filtration, and cloud-based analytics into turnkey offerings.

Mexico Mineral Processing Equipment Industry Leaders

Metso Outotec

FLSmidth A/S

Sandvik AB

The Weir Group PLC

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Luca Mining started commercial production at the Tahuehueto underground mine, completing a plant that can ramp to 1,000 t/d and signaling a fresh demand cycle for concentrate-grade control instrumentation.

- April 2025: Sandvik clinched a record USD 71 million contract to supply battery-electric trucks, loaders, bolters, and drills to the Hermosa critical-minerals project, with phased deliveries through 2030.

Mexico Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Others |

| Crushers |

| Feeders |

| Conveyors |

| Drills & Breakers |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Others | |

| By Equipment Type | Crushers |

| Feeders | |

| Conveyors | |

| Drills & Breakers | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

What is the 2025 value of the Mexico mineral processing equipment market?

The market stands at USD 147.65 million in 2025.

How fast will equipment demand in Mexico grow to 2030?

The market is forecast to expand at a 6.78% CAGR through 2030.

Which mineral segment is growing quickest in Mexico?

Lithium-processing equipment posts the fastest CAGR at 9.46% to 2030.

Why are fully automated plants gaining popularity?

Stricter SEMARNAT rules and labor-productivity goals are pushing operators toward fully digital circuits that cut emissions and downtime.

Which regions generate the most equipment demand?

Northern states led by Sonora dominate current spending, but central automotive-corridor states are rapidly catching up due to near-shoring.

Page last updated on: