Italy Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

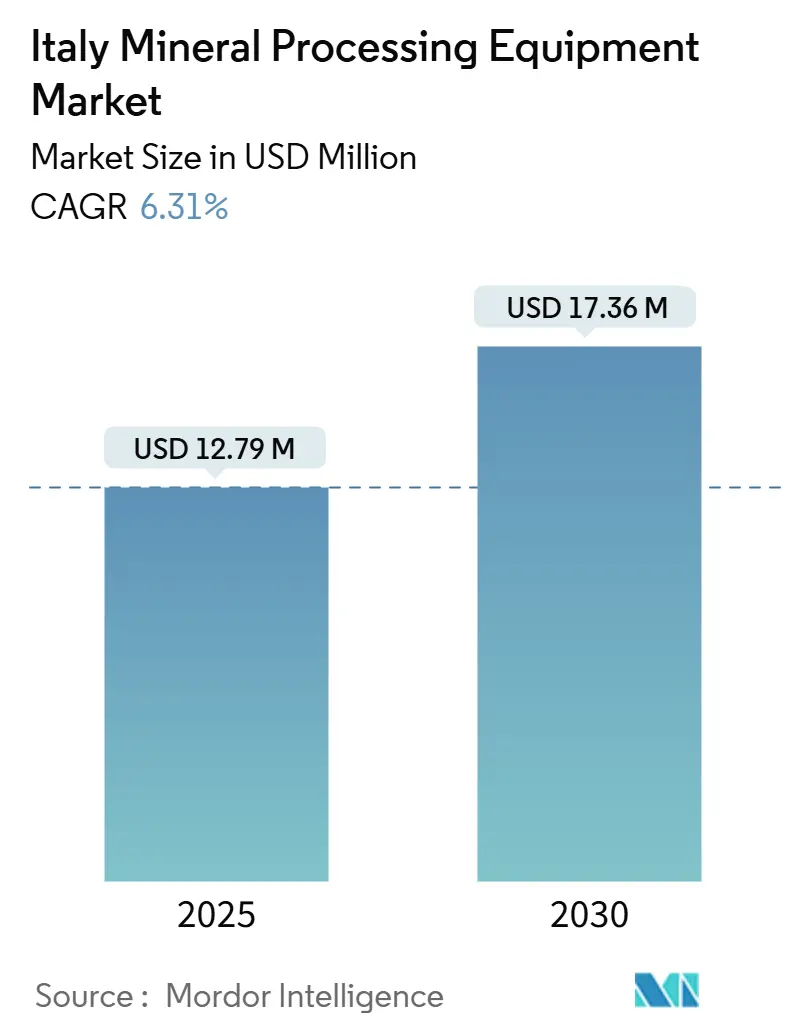

| Market Size (2025) | USD 12.79 Million |

| Market Size (2030) | USD 17.36 Million |

| Growth Rate (2025 - 2030) | 6.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Italy Mineral Processing Equipment Market size is estimated at USD 12.79 million in 2025, and is expected to reach USD 17.36 million by 2030, at a CAGR of 6.31% during the forecast period (2025-2030). Continued alignment between the National Recovery and Resilience Plan and EU mineral-security directives sustains capital spending. At the same time, a surge in digital-twin projects improves plant utilization and lowers operating costs. Reshoring of ceramic and metals production fuels near-term equipment orders, and EU incentives for local critical-material supply chains add long-run volume certainty. Vendors that blend energy-efficient designs with integrated process automation seize the clearest opportunity, because electricity price volatility remains the leading cost-planning risk. Competitive differentiation hinges on turnkey service capacity, environmental-compliance expertise, and rapid-response parts delivery across Italy’s diverse regional quarries.

Key Report Takeaways

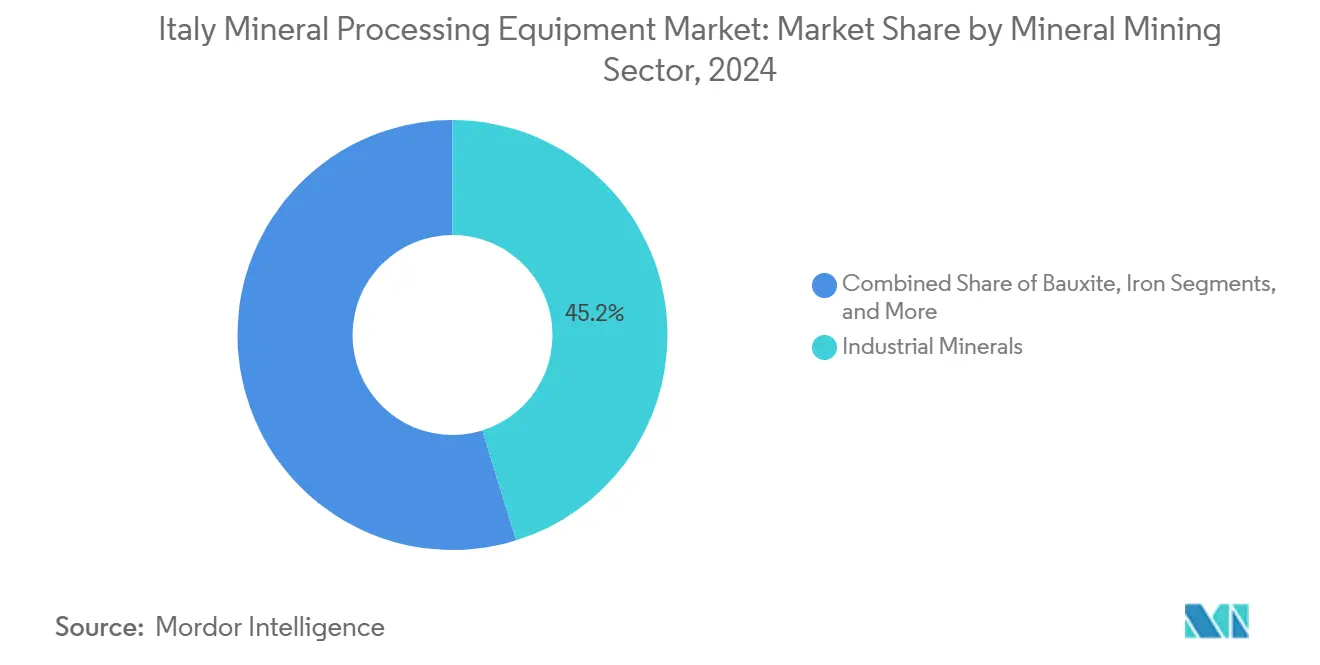

- By mineral mining sector, industrial minerals led with 45.18% revenue share of the Italian mineral processing equipment market in 2024, whereas in the mineral mining sector, critical battery minerals are advancing at a 6.43% CAGR through 2030.

- By equipment type, crushers commanded 36.58% of the Italian mineral processing equipment market size in 2024, whereas process control and automation systems are expanding at a 6.51% CAGR between 2025 and 2030.

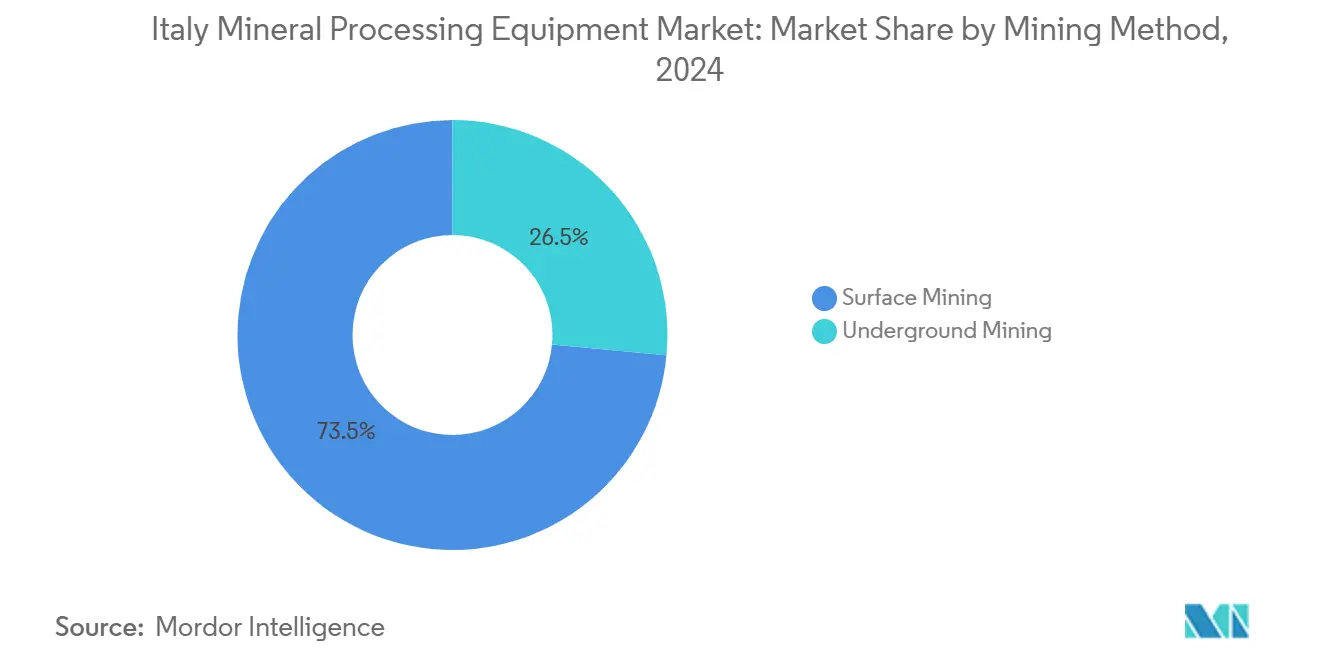

- By mining method, surface operations accounted for 73.48% share of the Italian mineral processing equipment market size in 2024, whereas underground activity is rising fastest, at a 6.47% CAGR through 2030.

- By automation level, manual plants held 56.11% of the Italian mineral processing equipment market in 2024, while fully automated lines grew at 6.55% CAGR to 2030.

Italy operates as part of an interconnected international environment rather than as a self-contained country level unit. The mineral processing equipment market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

Italy Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-Funded Mine-Modernisation Programs | +1.8% | National, concentrated in Southern Italy and Sardinia | Medium term (2-4 years) |

| Reshoring-Driven Demand | +1.2% | Northern Italy industrial clusters, Emilia-Romagna | Short term (≤ 2 years) |

| EU Critical Raw Materials Act Incentives | +1.1% | National, with priority zones in Alpine and Apennine regions | Long term (≥ 4 years) |

| Infrastructure Renovation & Construction Stimulus | +0.9% | National, emphasis on high-speed rail corridors | Medium term (2-4 years) |

| Adoption of Digital-Twin-Enabled Process Optimisation | +0.8% | Industrial districts in Lombardy, Veneto, Piedmont | Medium term (2-4 years) |

| Pilot Hydrogen-Fueled Thermal Processing Lines | +0.3% | Northern Italy steel and chemical corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-Funded Mine-Modernisation Programs

EU recovery funds earmarked for mineral-sector upgrades lower capital hurdles for smaller Italian operators. The fifth PNRR tranche directed a massive amount toward industrial renewal, and allocations for Sardinian and Sicilian processing plants include equipment procurement grants. Co-financing arrangements mean suppliers can close sales faster, while domestic manufacturing depth keeps delivery lead times short. Regional authorities now anchor procurement criteria on energy performance and emissions data, giving advantage to vendors with validated life-cycle footprints. Resulting equipment demand improves factory utilization for Italian OEMs, cementing a domestic demand–supply loop that protects local value addition.

Reshoring-Driven Demand from Metals & Ceramics Industries

Ceramics producers clustered around Emilia-Romagna re-evaluate overseas sourcing as freight volatility and geopolitical risks persist. Plants that pivot to local mineral feedstocks require new comminution, classification, and de-dusting lines tailored to Italy’s mixed-grade clays. WAMGROUP reported order momentum in bulk solids handling, reflecting this shift[1]“Annual Report 2024,” WAMGROUP, wamgroup.com . Therefore, the Italian mineral processing equipment market sees immediate call-offs for modular conveyors, bag filters, and automated batching units that integrate with existing kiln infrastructure. Short project-cycle expectations favor plug-and-play offerings that minimize downtime.

EU Critical Raw Materials Act Incentives

The Act stipulates that around one-tenth of strategic minerals consumed in the EU be sourced domestically by 2030. Projects targeting Tuscan lithium pegmatites and Sardinian rare-earth veins have accelerated feasibility studies. These deposits need fine-grind mills, selective flotation, and solvent-extraction circuits that differ from those used in industrial-mineral quarries. Altamin’s Sardinian redevelopment plan, launched in 2015, highlights the pivot toward battery-material flowsheets[2]“Sardinian Critical Minerals Projects,” Altamin Ltd., altamin.com . This legislative pressure reorients capital budgets toward high-precision, automation-ready equipment that can meet tight impurity thresholds.

Infrastructure Renovation & Construction Stimulus Boosting Aggregates Demand

Webuild disclosed a massive backlog covering rail, metro, and water schemes, guaranteeing high volumes of crushed rock and recycled concrete through 2030. Quarries from the Alps to Sicily expand capacity, preserving crushers’ leading share in the Italian mineral processing equipment market. MB Crusher promotes on-site recycling attachments that convert demolition waste into graded aggregates, aligning with procurement rules that mandate recycled content. Stable multi-year visibility allows OEMs to schedule capacity additions and negotiate favorable steel input contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU Environmental Permitting | -0.7% | National, particularly in protected Alpine and coastal zones | Short term (≤ 2 years) |

| Volatile Electricity & Natural-Gas Prices | -0.5% | National, with acute impact on energy-intensive operations | Short term (≤ 2 years) |

| Cyclical Mining Investment | -0.4% | National, with emphasis on export-oriented operations | Medium term (2-4 years) |

| Local Opposition in Heritage & Tourist Zones | -0.3% | Tuscany, Umbria, coastal regions, UNESCO sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Environmental Permitting

Stricter ecological assessments lengthen approval cycles for both greenfield and retrofit projects. Carrara marble quarries illustrate the challenge; operators must file comprehensive noise, particulate, and water-use models for every machinery change. This extends lead times and inflates engineering budgets. Suppliers with documented best-available-technology credentials win bids when buyers seek turnkey compliance packages. Therefore, the Italian mineral processing equipment market sees demand skew toward premium, low-emission designs, favoring well-capitalized vendors able to certify performance with third-party data.

Volatile Electricity & Natural-Gas Prices

ARERA’s 2024 report highlighted persistent tariff swings even after Energy Release 2.0 relief was granted to high-consumption firms. Operators hesitate to commit to power-intensive gear unless payback is secured through higher efficiency or variable-load capability. Manufacturers respond by adding hybrid drives and energy-storage integration. Magaldi’s thermal-storage solution, for instance, stores excess heat for later use, smoothing kiln duty cycles. Capital decisions increasingly couple mechanical specifications with predictive energy-cost analysis.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Industrial Minerals Drive Traditional Demand

Industrial minerals secured 45.18% of the Italian mineral processing equipment market 2024, confirming their entrenched role in ceramics, glass, and construction supply chains. Demand concentrates in Tuscany and Emilia-Romagna, where decades-old quarries tap limestone, kaolin, and feldspar reserves feeding downstream tile and sanitary-ware plants. Upgrades focus on dust suppression, modular screens, and high-efficiency classifiers that meet tightened particulate regulations.

Critical battery minerals, while still a minor revenue contributor, post a 6.43% CAGR to 2030, outpacing every other mineral group. Projects targeting Tuscan lithium and Sardinian rare earths seek closed-circuit milling, magnetic separation, and hydrometallurgical reactors. Automation depth is higher than in legacy quarries, pushing order sizes upward. The Italian mineral processing equipment market size for battery-material projects is projected to triple over the forecast horizon, anchored by EU offtake guarantees.

By Equipment Type: Automation Systems Accelerate Growth

Crushers retained a 36.58% share of the Italian mineral processing equipment market size in 2024, buoyed by construction-aggregate production for rail and metro corridors. Fixed-jaw and cone configurations dominate, though tracked mobile units gain share near urban jobsites. Energy-efficient drive packages and wear-resistant metallurgy cut lifetime costs, keeping replacement demand steady.

Process control and automation systems record the fastest trajectory at 6.51% CAGR to 2030. Plants retrofit PLCs, SCADA, and AI-driven optimisation suites that slash unplanned downtime. Average automation spending per tonne processed rises as digital-twin adoption spreads. The Italian mineral processing equipment industry confronts a talent gap in controls engineering, so vendors that bundle training capture service revenue streams.

By Mining Method: Underground Operations Gain Momentum

Surface extraction accounted for 73.48% of the Italian mineral processing equipment market share in 2024, reflecting abundant open-pit marble, aggregates, and pozzolana quarries. Compliance with new dust and visual-impact norms drives screening-plant relocations and enclosure projects, sustaining mechanical equipment orders.

Although only a quarter of installed capacity, underground operations will increase at a 6.47% CAGR through 2030. Alpine and Apennine deposits move subsurface to appease heritage and tourism concerns. This shift triggers demand for low-profile trucks, shotcrete pumps, and remote-operated scalers. Vendors with underground-specific safety certifications see higher tender hit rates. The Italian mineral processing equipment market size for underground projects relies on EU funding for dewatering and ventilation infrastructure, which locks in multiyear visibility.

By Automation Level: Digital Transformation Accelerates

Manual plants still comprise 56.11% of installed capacity, a legacy of family-owned quarries with low technical complexity. Rising labor costs and occupational health scrutiny push owners toward semi-automated retrofits, starting with weigh-belt feeders and camera-based particle-size analyzers.

Fully automated lines, however, log a 6.55% CAGR through 2030. These facilities integrate robotic stackers, condition-monitoring sensors, and AI scheduling that cut cycle time. A leather-tanning cluster in Santa Croce sull'Arno reported over two-fifths lower downtime after adopting advanced analytics, and mines are now piloting similar systems. The Italian mineral processing equipment market is expanding as grants offset workforce upskilling expenses.

Geography Analysis

Northern Italy, encompassing Lombardy, Piedmont, and Veneto, captures the largest share of the Italian mineral processing equipment market. These regions co-locate equipment OEMs, metal-mechanical know-how, and dense highway and rail links that minimize logistics costs. Plants processing feldspar and kaolin supply Europe-wide ceramic tile demand, while Lombardy’s chemical sector drives demand for highly controlled milling lines. Environmental regulations require enclosed conveyors and negative-pressure dust systems, adding automation components to traditional mechanical scopes.

Central Italy centers on Tuscany’s marble and emerging lithium prospects. Marble cutting needs heavy-duty wire saws and water-recirculation units, while lithium pilot plants specify fine-grind mills and leach reactors. Proximity to ports in Livorno and Piombino simplifies equipment import and finished-product export, lowering total landed cost. Lazio’s infrastructure renovation generates recycled-aggregate projects that apply MB Crusher buckets to onsite demolition materials. This supports mobile crushing fleet growth within the Italian mineral processing equipment market.

Southern Italy, including Sardinia and Sicily, posts the fastest regional CAGR. EU modernisation funds target Sardinian mining heritage, where Altamin and regional authorities collaborate on rare-earth redevelopment. Equipment demand centers on modular flotation skids, solvent-extraction cells, and paste-thickener units designed for water-scarce conditions. Sicily’s volcanic-basalt quarries anchor a high-strength aggregate supply for Mediterranean construction markets. OEMs tailor wear-part metallurgy to handle abrasive lava rock, and integrated diesel-solar hybrids address grid-stability constraints.

The mineral processing equipment market is assessed by Mordor Intelligence through a multi-layered geographic lens, with detailed country-level analysis for France, Spain, Saudi Arabia, Australia, China, Canada, Germany, South Korea, and Argentina.

Competitive Landscape

International major players including FLSmidth, Metso, and Sandvik, retain leading positions by pairing global R&D with Italian field-service density. FLSmidth reported just above a percent growth in 2024 mining-service orders, underscoring the service-heavy profile of Italy’s mature installed base. Metso’s minerals segment logged a decrease in orders in Q3 2024, proving that digital-integrated upgrades maintain profitability[3]“Q3 2024 Interim Review,” Metso Corporation, metso.com .

Italian mid-tier specialists such as Baioni, Bedeschi, MB Crusher, and Tesmec focus on niche configurations and rapid customization. MB Crusher’s portable jaw attachments for recycled concrete aggregates meet sustainability clauses in public works tenders. Baioni’s skid-mounted washing plants address small quarry footprints, while Bedeschi supplies triple-roll crushers for sticky clay.

Differentiation gravitating toward Industry 4.0 capability sees mechanical OEMs acquire software integrators. Piovan adds control-system talent to its plastics roots and now bids on mineral plants. Simem Underground Solutions leverages its tunneling pedigree to deliver custom paste-backfill mixers. Suppliers that certify environmental-performance data gain an advantage in lengthy permitting cycles, solidifying moderate market concentration.

Italy Mineral Processing Equipment Industry Leaders

Metso Outotec

FLSmidth A/S

Sandvik AB

The Weir Group PLC

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: ErreDue S.p.A. secured a EUR 1.7 million contract to build a green-hydrogen plant in Livorno to supply 432 kg per day for industrial heating in mineral processing.

- July 2024: Tenaris, Snam, and Tenova completed a six-month hydrogen trial at the Dalmine steel facility to test green hydrogen in pipe reheating furnaces, validating emission-cutting potential for thermal processing lines.

Italy Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Industrial Minerals |

| Critical Battery Minerals |

| Others |

| Crushers |

| Screening & Feeding Equipment |

| Conveyors & Material Handling Systems |

| Grinding Mills & Breakers |

| Process Control & Automation Systems |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Industrial Minerals | |

| Critical Battery Minerals | |

| Others | |

| By Equipment Type | Crushers |

| Screening & Feeding Equipment | |

| Conveyors & Material Handling Systems | |

| Grinding Mills & Breakers | |

| Process Control & Automation Systems | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

What is the current value of the Italian mineral processing equipment market?

The Italian mineral processing equipment market will be worth USD 12.79 million in 2025, with a 6.31% CAGR to 2030.

Which mineral segment is growing fastest in Italy?

Critical battery minerals post the highest 6.43% CAGR as EU sourcing mandates spur lithium and rare-earth projects.

Which equipment category leads sales?

Crushers account for 36.58% of 2024 revenue because infrastructure projects consume large aggregate volumes.

How are energy prices shaping equipment choices?

Persistent electricity and natural-gas volatility push buyers toward energy-efficient drives and hybrid-power solutions.

Which automation level is expanding the quickest?

Fully automated plants grow at 6.55% CAGR, driven by Industry 4.0 incentives and labor-cost pressures.

Who are the key suppliers in the country?

Global leaders FLSmidth, Metso, and Sandvik dominate, while Italian specialists MB Crusher, Bedeschi, and Baioni thrive in custom niches.

Page last updated on: