Spain Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

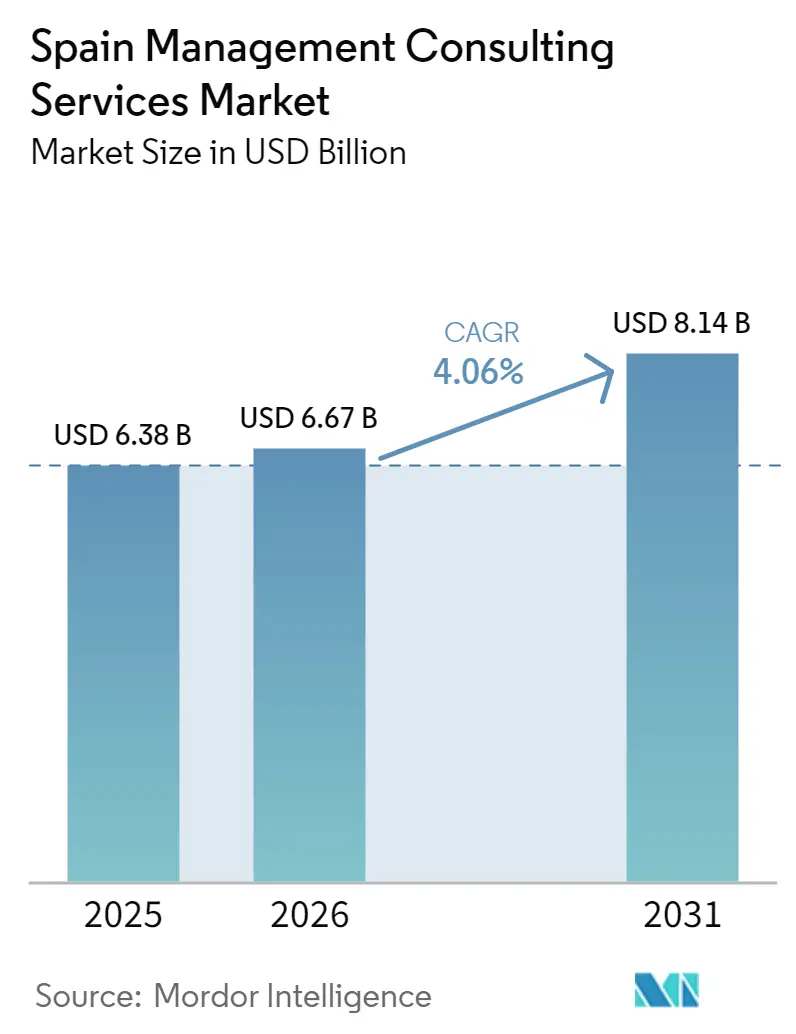

| Base Year Market Size (2025) | USD 6.38 Billion |

| Market Size (2026) | USD 6.67 Billion |

| Market Size (2031) | USD 8.14 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Management Consulting Services Market Analysis by Mordor Intelligence

The Spain management consulting services market size was valued at USD 6.38 billion in 2025 and estimated to grow from USD 6.67 billion in 2026 to reach USD 8.14 billion by 2031, at a CAGR of 4.06% during the forecast period (2026-2031). Robust public-sector modernization funded by EU recovery grants, mandatory climate and sustainability disclosures, and sustained digital transformation programs continue to underpin demand. Consulting spend remains resilient despite price pressure because enterprises rely on external expertise to close talent gaps in cloud architecture, generative artificial intelligence, and environmental social and governance reporting. At the same time, margin compression on commoditized work is accelerating the shift toward outcome-based pricing and proprietary intellectual property. Consolidation among mid-tier specialists and a rising mix of hybrid delivery models are reshaping competitive dynamics as firms balance cost efficiency with client expectations for onsite strategic engagement.

Key Report Takeaways

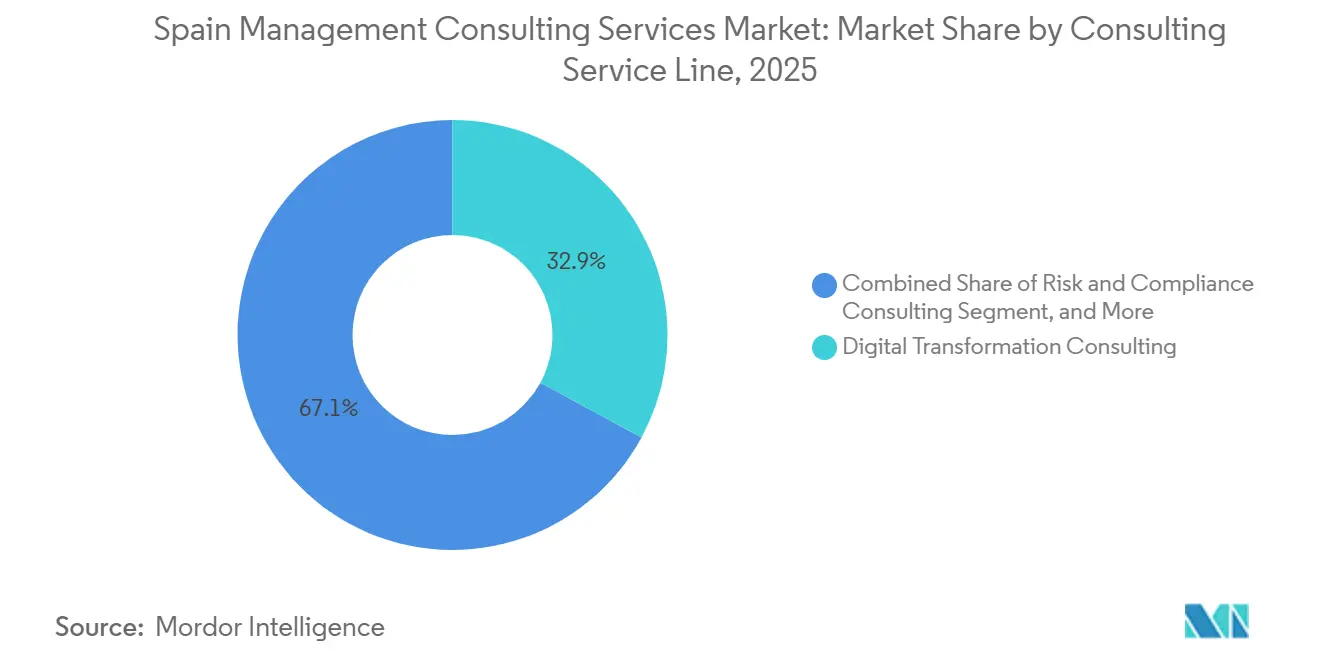

- By consulting service line, Digital Transformation Consulting led with 32.91% of revenue in 2025, while Risk and Compliance Consulting is forecast to post the highest 4.89% CAGR through 2031.

- By organization size, Large Enterprises accounted for 64.02% of 2025 spending, yet Small and Medium-Sized Enterprises are projected to expand at a faster 4.67% CAGR to 2031.

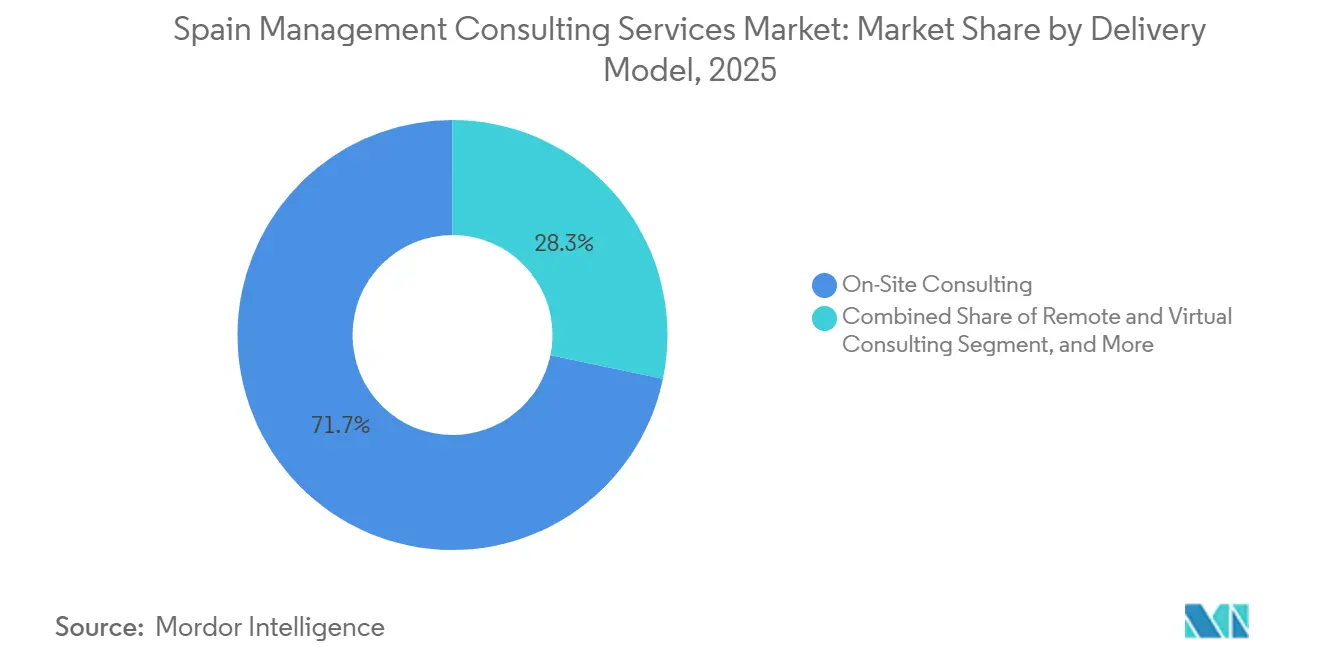

- By delivery model, On-Site Consulting held 71.74% share in 2025, whereas Hybrid Consulting is expected to grow the quickest at 4.76% over the forecast period.

- By end user industry, Information Technology and Telecommunications commanded 26.27% of 2025 demand, while Energy and Resources is projected to log the fastest 4.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation and Cloud Migration Momentum | +1.2% | National, concentrated in Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Regulatory Compliance Advisory Demand (GDPR, ESG, Labor Reforms) | +0.9% | National, with EU-wide spillover | Short term (≤ 2 years) |

| EU-Funded Next Generation Recovery Investments | +0.8% | National, emphasis on public sector and infrastructure hubs | Medium term (2-4 years) |

| Surge in Demand for GenAI Governance Playbooks | +0.7% | National, early adoption in financial services and telecom | Short term (≤ 2 years) |

| Accelerated Decarbonization Roadmaps for CNMV Climate Disclosures | +0.5% | National, energy and industrial sectors | Long term (≥ 4 years) |

| Cross-Border Post-Merger Integration Following Corporate Relocation | +0.4% | Iberia, with activity from France and United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation and Cloud Migration Momentum

Spanish companies continue shifting legacy systems to hybrid clouds to support distributed workforces and integrate artificial intelligence workloads, as illustrated by the managed-cloud alliance between Kyndryl España and MasOrange announced in late 2025.[1]Kyndryl, “Kyndryl and MasOrange announce strategic partnership,” kyndryl.com Major banks sustain this push: CaixaBank earmarked more than EUR 5 billion (USD 5.8 billion) through 2027 for technology upgrades that include generative artificial intelligence enhancements to its customer channels. Consulting firms are responding by creating cloud centers of excellence and acquiring niche analytics boutiques, such as Bain’s purchase of Madrid-based PiperLab, which formed a new regional artificial intelligence hub.[2]IT User, “Bain and Company amplía su oferta de IA con la adquisición de la española PiperLab,” ituser.es As hybrid architectures mature, clients increasingly request FinOps governance frameworks that optimize consumption costs, prompting multiyear advisory retainer agreements. This driver therefore sustains premium demand across financial services, healthcare, and public administration within the Spain management consulting services market.

Regulatory Compliance Advisory Demand (GDPR, ESG, Labor Reforms)

The Corporate Sustainability Reporting Directive expansion and Spain’s Royal Decree 214/2025 require thousands of companies to publish environmental, social, and governance metrics, even after Omnibus I trimmed mandatory data points from 1,073 to 320. Compliance complexity is compounded by information and communications technology risk-management rules under the Digital Operational Resilience Act that took effect in January 2025. In parallel, Spain’s data-protection authority issued guidance on public-sector generative artificial intelligence in February 2026, forcing agencies to complete data-protection impact assessments before deployment.[3]Agencia Española de Protección de Datos, “AEPD publica guía sobre IA agentes en el sector público,” aepd.es Mid-market firms lacking dedicated sustainability or privacy teams hire consultants to translate these overlapping mandates into internal controls, sustaining a predictable pipeline of governance and assurance projects.

EU-Funded Next Generation Recovery Investments

Spain secured significant recovery funds that flow through competitive public tenders for digital government, infrastructure, and social programs. Large framework contracts require multidisciplinary teams that can blend legal, technical, and impact-measurement skills. Tier-one firms and local champions with proven delivery credentials win the bulk of this work, lifting utilization and backlog visibility. The resulting project pipeline strengthens regional consulting footprints beyond Madrid and Barcelona, expanding addressable revenue for the Spain management consulting services market.

Surge in Demand for GenAI Governance Playbooks

Enterprises are eager to scale generative artificial intelligence, yet concerns over data protection, bias, and intellectual property leakage create hesitation. National data-protection guidance and sector standards now mandate structured governance. Consulting firms monetize this gap by codifying model selection criteria, prompt engineering guidelines, and audit trails into service offerings. Advisory demand spans policy definition through change-management rollouts, adding a new recurring revenue stream that supports pricing resilience within the Spain management consulting services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Pressure and Commoditization of Standard Engagements | -0.6% | National, acute in mid-market segment | Short term (≤ 2 years) |

| Talent Shortages and Wage Inflation for Senior Consultants | -0.5% | National, concentrated in Madrid, Barcelona | Medium term (2-4 years) |

| Expansion of Internal Corporate Venture Studios | -0.3% | National, large enterprises and multinationals | Medium term (2-4 years) |

| Slow Analytics Adoption Among Rural SMEs Outside Madrid-Barcelona Corridor | -0.2% | Regional, peripheral provinces and islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Pressure and Commoditization of Standard Engagements

Clients increasingly disaggregate projects, sourcing discrete deliverables through competitive tenders that favor the lowest price. Outcome-based fee models shift risk onto providers and squeeze gross margins for firms lacking proprietary accelerators.[4]Bondo Advisors, “Informe M and A Consultoría TI Iberia 2025,” bondoadvisors.com Mid-tier consultancies respond by verticalizing into niches where domain knowledge commands premium pricing, yet the sustained influx of freelancers and boutique advisors keeps negotiating leverage with buyers. This restraint moderates revenue growth for the Spain management consulting services market, especially in routine process mapping and compliance gap analysis.

Talent Shortages and Wage Inflation for Senior Consultants

Open vacancies in information and communications technology roles continue climbing, particularly in Madrid and Barcelona. Madrid posted 12,400 open information and communications technology vacancies in 2025, a 23% year-on-year jump, underscoring chronic skills scarcity. Scarcity of cloud architects, data engineers, and sustainability specialists fuels double-digit wage inflation, eroding project profitability unless cost pass-through mechanisms exist. Firms intensify campus recruiting, upskilling programs, and nearshore delivery, yet attrition from big tech and private equity still drains experienced talent. Capacity bottlenecks can delay project starts and constrain scalability, capping upside for the Spain management consulting services market in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Demand Shifts Toward Risk and Compliance

Digital Transformation Consulting captured 32.91% of 2025 revenue, the largest slice of the Spain management consulting services market share. Risk and Compliance Consulting is projected to advance at a 4.89% CAGR through 2031, supported by overlapping mandates that compel firms to overhaul data-governance and sustainability controls. The Spain management consulting services market size tied to these two lines is therefore expanding on both breadth and depth as clients bundle technology enablement with regulatory assurance. Strategy Consulting remains relevant for portfolio optimization and nearshoring questions, yet its growth trails implementation-heavy work as procurement chiefs demand quantifiable benefits. Operations Consulting gains momentum from automotive electrification and supply-chain reconfiguration, while Human Resources Consulting monetizes hybrid-work policy design and talent-retention analytics. Financial Advisory Consulting enjoys episodic spikes around record mergers and acquisitions deal flow, reinforcing the need for integration playbooks that span finance, information technology, and culture. Smaller niches such as innovation management and real-estate advisory aggregate into a meaningful revenue pool for boutiques that differentiate on intellectual property. Providers increasingly cross-sell between service lines, positioning integrated teams to win multiyear programs and expand wallet share.

The blurring of boundaries drives firms to package cloud migration, cybersecurity, and environmental social and governance reporting into single statements of work, tightening client lock-in. Large enterprises often award master agreements that integrate six or more capabilities, forcing mid-tier contenders to partner or risk exclusion. As a result, the Spain management consulting services market experiences steady consolidation among specialists seeking scale, although green-field opportunities persist in sectors like renewable hydrogen where domain expertise is scarce. Providers that invest early in accelerators and proprietary data sets can defend pricing even as commoditized diagnostics lose margin. Over the forecast window, the mix of revenue will keep tilting toward segments that fuse technology enablement with compliance outcomes, sustaining double-digit growth pockets within the wider 4.06% headline rate.

By Organization Size: SMEs Narrow the Gap

Large Enterprises generated 64.02% of 2025 spend, reflecting complex multiyear transformation mandates and deep pockets for change-management support. Yet government vouchers under the Digital Kit and Consulting Kit programs are closing the affordability gap, allowing smaller firms to engage advisors for e-commerce, cybersecurity, and sustainability roadmaps. The Spain management consulting services market size attributable to Small and Medium-Sized Enterprises is projected to expand faster than the overall headline CAGR, reflecting latent demand unlocked as digital financing ties loan eligibility to modernization milestones. Providers respond with modular offerings, fixed-price starter packs, and remote accelerators that lower entry tickets without eroding profitability.

SME adoption still faces hurdles, notably limited digital literacy outside Spain’s two largest metros. Consultants therefore embed capability-building workshops and managed services options that transfer execution risk from owners to advisory firms. Hybrid delivery further reduces cost, encouraging rural manufacturers and tourism operators to outsource technology governance. Over time, sustained exposure to professional advisory elevates operational maturity, positioning many SMEs for cross-border expansion and subsequent higher-value consulting engagements. This structural catch-up dynamic provides a durable growth layer for the Spain management consulting services market while diversifying revenue beyond the concentrated corporate core.

By Delivery Model: Hybrid Engagements Scale

On-Site Consulting retained 71.74% share in 2025 because executive alignment sessions, labor negotiations, and crisis response still require physical presence. However, Hybrid Consulting, which marries remote diagnostics with strategic in-person workshops, is increasing at a 4.76% pace, the fastest within delivery models of the Spain management consulting services market. Clients value travel cost savings combined with targeted face-time when project milestones demand stakeholder buy-in. Providers leverage collaboration platforms, asynchronous knowledge hubs, and nearshore centers to orchestrate global talent while keeping senior teams on deck for politically sensitive moments.

Purely virtual engagements stabilize as a niche for standardized benchmarking and compliance audits, although conversational artificial intelligence and virtual-reality workshops are widening the scope of remote value delivery. The Spain management consulting services industry is therefore re-tooling its operating model, shifting utilization targets, and redesigning career pathways that reward expertise over billable travel days. Firms that perfect hybrid orchestration unlock margin resilience, whereas laggards risk client attrition to cloud-native boutiques that were remote-first from inception.

By End User Industry: Energy and Resources Rises Fastest

Information Technology and Telecommunications held 26.27% of 2025 end-user demand, maintaining its rank as the single largest vertical in the Spain management consulting services market. Energy and Resources is forecast to grow at 4.92% annually through 2031, propelled by the National Energy and Climate Plan and record renewable investment pipelines. Consultants design program-management offices for utility-scale solar, structure green-hydrogen joint ventures, and align project financing with evolving taxonomy rules, all of which deepen engagement intensity. Banking and Insurance continues to invest heavily in Digital Operational Resilience Act compliance and data-driven underwriting, sustaining a recurring flow of cyber-resilience and cloud-core banking assignments.

Manufacturing embraces Industry 4.0, forcing plant retooling, supply-chain reshoring, and workforce reskilling that require multidisciplinary advisory. Healthcare accelerates telemedicine, imaging analytics, and electronic record integration, reinforcing demand for privacy-by-design frameworks. Public-sector entities, flush with EU grants, tender mega contracts for digital government platforms, amplifying addressable volume in secondary cities. Retail, hospitality, and logistics verticals pursue artificial intelligence for demand forecasting and dynamic pricing, albeit through smaller ticket engagements spread across dozens of clients. Collectively, this diversity shields the Spain management consulting services market from sector-specific shocks and supports balanced revenue growth.

Geography Analysis

Madrid and Barcelona together generate roughly 70% of consulting fees, anchored by headquarters of multinationals, ministerial agencies, and vibrant start-up ecosystems. Madrid leads in banking, telecommunication, and public-policy mandates, while Barcelona scores in life sciences, logistics, and creative industries. Valencia rises as a third pole, capitalizing on port digitalization and agritech exports, drawing steady advisory work on supply-chain optimization and renewable-energy siting. Andalucía deploys EU recovery funds aggressively, exemplified by a EUR 200 million framework to operate more than 3,000 information systems, attracting tier-one and mid-tier consortia.

Galicia positions itself as an aerospace and defense digital hub, driven by Minsait’s growing Center of Excellence and regional incentives that lower talent costs compared with the capital. Basque Country and Navarra secure niche Industry 4.0 projects in automotive components and smart-grid technology, leveraging long-standing manufacturing depth. Canary and Balearic Islands lag in cloud usage and artificial intelligence uptake, yet tourism rebound fuels demand for revenue-management and sustainability certifications, opening greenfield prospects. Extremadura and Castilla-La Mancha gain attention for utility-scale solar and data-center site selection, requiring environmental impact studies and grid interconnection advice.

Regional wage differentials and hybrid delivery allow firms to relocate delivery pods to secondary cities such as Málaga and Bilbao, diversifying talent sourcing and improving retention. The Spain management consulting services market therefore displays a widening geographic footprint beyond its historic duopoly, aligning with policy objectives that seek balanced national development. Over the forecast period, continued dispersion of EU-funded digital transformation projects is expected to keep regional pipelines active and reduce concentration risk.

Competitive Landscape

Big Four audit-anchored consultancies plus the three strategy titans capture an estimated 45-50% of revenue, setting the tone on pricing, talent, and intellectual property investment. Accenture, Deloitte, PwC, KPMG, and Ernst and Young dominate cross-functional transformation and regulatory remediation programs by combining offshore scale with local partner intimacy. McKinsey, Boston Consulting Group, and Bain focus on board-level strategy and advanced analytics, highlighted by Bain’s acquisition of PiperLab that seeded an artificial intelligence hub in Madrid. Technology consultancies such as Capgemini Invent, NTT Data Spain, and IBM Consulting close the gap by bundling managed services, giving them a durable seat at long-cycle digital-core replacement deals.

Spanish-heritage firms Indra’s Minsait, Seidor, and Auren play the national champion card, leveraging cultural fluency and regional offices to penetrate public sector and mid-market accounts that value proximity. Private-equity backing accelerates their acquisition pipelines, exemplified by Auren’s target to double revenue within two years via 15-plus takeovers. Grant Thornton scales through lateral partner hires and specialist bolt-ons, aiming to lift multidisciplinary share in legal, tax, and technology advisory. The freelance and boutique ecosystem continues to fragment the tail, offering cost-efficient micro-engagements that challenge traditional pyramids on commoditized scopes.

Competitive intensity drives firms to invest in sovereign artificial intelligence platforms, sustainability data lakes, and sector-specific accelerators that compress delivery timelines. Outcome-based commercial terms are gaining adoption, rewarding providers that can measure and guarantee impact. Talent scarcity remains the great equalizer: firms able to articulate purpose, offer rapid upskilling, and embrace flexible work models win the recruiting war. Mergers and acquisitions momentum is expected to sustain through 2027, suggesting that the Spain management consulting services market will trend toward moderate consolidation while preserving room for innovators.

Spain Management Consulting Services Industry Leaders

Accenture España

Deloitte España

KPMG España

PwC España

EY España

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Minsait secured a EUR 8.23 million (USD 8.89 million) Banco de España contract for technology-infrastructure support.

- March 2026: Grant Thornton Spain appointed Aurora Sanz as head of legal and tax services, expanding multidisciplinary capacity.

- March 2026: Minsait launched IndraMind, a sovereign artificial intelligence ecosystem for public administrations in Galicia.

- February 2026: Bain and Company predicted record 2026 mergers and acquisitions volumes after a 66% surge to EUR 62.38 billion (USD 72.92 billion) in 2025.

Spain Management Consulting Services Market Report Scope

The Spain Management Consulting Services Market Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current Spain management consulting services market size and projected growth?

The market stood at USD 6.67 billion in 2026 and is forecast to reach USD 8.14 billion by 2031, reflecting a 4.06% CAGR.

Which service line is growing fastest within Spanish consulting?

Risk and Compliance Consulting is projected to grow at a 4.89% CAGR as firms navigate new European and national regulations.

How are hybrid delivery models affecting consulting engagements in Spain?

Hybrid models blend remote diagnostics with targeted on-site workshops, lowering travel costs while preserving strategic depth, and are expanding at 4.76% annually.

Why is Energy and Resources the most dynamic end-user vertical?

Ambitious renewable-energy targets and a EUR 294 billion (USD 343 billion) investment pipeline are driving demand for decarbonization strategy, project finance, and supply-chain advisory.

How do talent shortages impact consulting fees?

Scarcity of cloud, artificial intelligence, and sustainability experts in Madrid and Barcelona is pushing senior-consultant wages up by as much as 15% each year, pressuring margins.

Which Spanish regions outside Madrid and Barcelona are emerging for consulting work?

Andalucía, Galicia, and Valencia are attracting sizeable public-sector digital contracts and renewable-energy projects, broadening regional revenue streams.

Page last updated on: