Greece Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

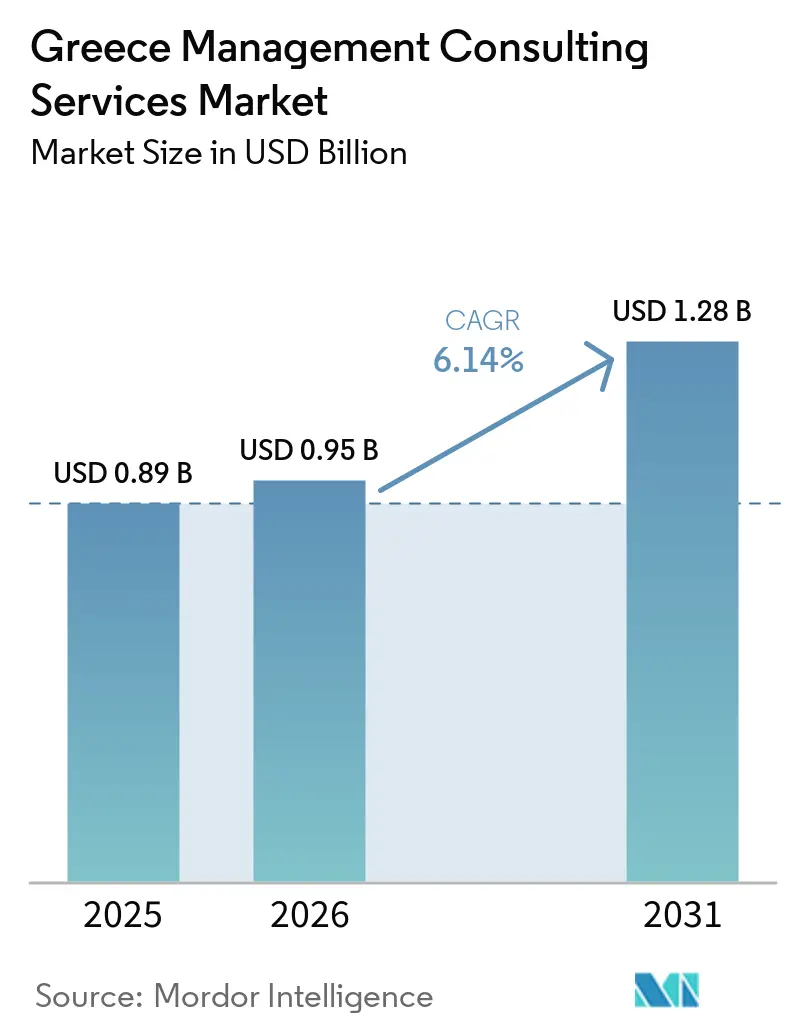

| Base Year Market Size (2025) | USD 0.89 Billion |

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece Management Consulting Services Market Analysis by Mordor Intelligence

The Greece management consulting services market size is expected to increase from USD 0.89 billion in 2025 to USD 0.95 billion in 2026 and reach USD 1.28 billion by 2031, growing at a CAGR of 6.14% over 2026-2031. A once-in-a-generation infusion of European Union recovery funds, new sustainability-reporting mandates, and an active privatization pipeline are compressing decision cycles and channeling large advisory budgets toward technology, risk, and transaction work. Digital vouchers for more than 100,000 small and medium-sized enterprises, an aggressive public-sector digitalization program, and rising cross-border mergers and acquisitions are broadening the client base beyond the traditional banking and state-owned segments. Competitive intensity is rising as the Big Four, global strategy houses, and a cadre of specialist boutiques race to staff projects amid an acute consultant talent shortage. Delivery models are shifting toward hybrid engagement as remote collaboration tools mature and Greek diaspora professionals return to the local market.

Key Report Takeaways

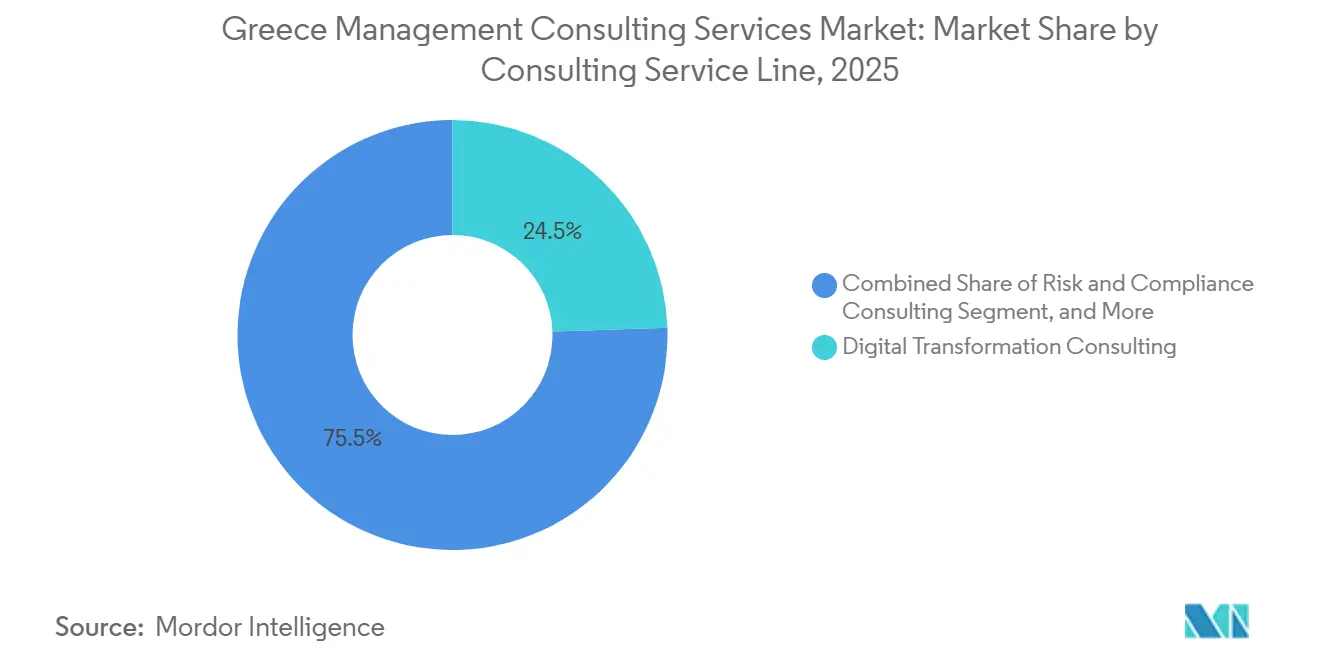

- By consulting service line, Digital Transformation led with 24.46% of the Greece management consulting services market share in 2025, while Risk and Compliance is projected to post the fastest 6.54% CAGR to 2031.

- By organization size, large enterprises accounted for 57.81% of spending in 2025, whereas small and medium-sized enterprises are forecast to expand at a 6.17% CAGR through 2031.

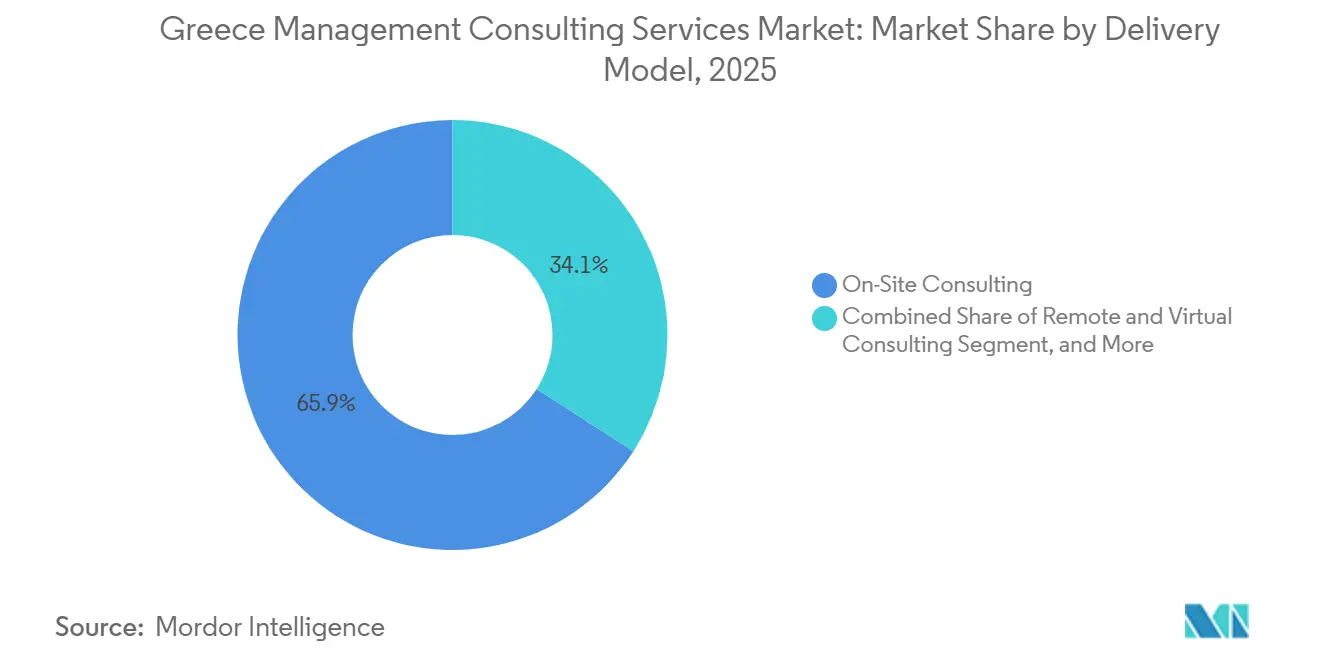

- By delivery model, on-site engagements retained 65.91% share in 2025, yet remote and virtual consulting is set to grow at a 6.62% CAGR through 2031.

- By end-user industry, the public sector contributed 23.07% of revenue in 2025, while energy and resources is expected to register the fastest 6.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Greece Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Recovery-Funded Digital Transformation Wave | +1.8% | National, concentrated in Attica, Thessaloniki, tourism regions | Short term (≤ 2 years) |

| Regulatory and ESG Compliance Pressures | +1.5% | National, early adoption by large firms in Athens | Medium term (2-4 years) |

| Accelerated Technology Adoption Across Industries | +1.2% | National, led by banking, telecom, and energy | Medium term (2-4 years) |

| M&A and Privatization Advisory Demand Surge | +0.9% | National, focused on energy, infrastructure, finance | Short term (≤ 2 years) |

| International-Expansion Ambitions of Greek SMEs | +0.4% | National, export-oriented manufacturing, agri-food, tourism | Long term (≥ 4 years) |

| EU Agri-Tech Digitization Incentives | +0.3% | Rural regions: Thessaly, Central Greece, Peloponnese | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Recovery-Funded Digital Transformation Wave

The EUR 31 billion (USD 35.03 billion) Greece 2.0 Recovery and Resilience Facility funnels grants and loans toward public-sector modernization, SME digital vouchers, and infrastructure upgrades, all of which must be completed by end-2026. Consultants are helping ministries digitize 1.035 billion archival pages, deploy nationwide cloud services, and launch e-procurement systems before the deadline.[1]European Investment Bank, “Greece: EIB Managing up to €5bn of Recovery and Resilience Facility Loan Fund,” eib.org Advisory demand is further amplified by the Digital Transformation Bible 2026-2030, which extends the technology roadmap beyond the RRF period. The compressed procurement window is pulling multi-year projects into a 24-month execution sprint. As a result, Digital Transformation Consulting captured nearly one-quarter of the Greece management consulting services market in 2025.

Regulatory and ESG Compliance Pressures

Law 5164/2024 transposed the Corporate Sustainability Reporting Directive, phasing in double-materiality disclosure and imposing fines of up to EUR 500,000 (USD 565,000) on auditors that fall short. Although the 2025 “Stop-the-Clock” Directive delayed some waves, it also lengthened the advisory runway for risk, data-governance, and assurance services.[2]European Commission, “Corporate Sustainability Reporting Directive,” eur-lex.europa.eu ICAP CRIF recorded double-digit revenue and EBITDA growth in 2024 by selling ESG scores and advisory to more than 7,700 clients. Greek corporations are turning to consultants to map environmental and social impacts, embed metrics into finance systems, and prepare for mandatory external assurance. Consequently, Risk and Compliance commands the fastest forecast growth rate in the Greece management consulting services industry.

Accelerated Technology Adoption Across Industries

National Bank of Greece completed a USD 1.13 billion, five-year overhaul that involved 500,000 consultant workdays and produced more than 4 million digital users. Eurobank’s AI factory, developed with EY, Microsoft, and Fairfax, showcases a new wave of agentic AI initiatives that require specialized advisory on data, ethics, and model deployment. Manufacturing pilots such as Greece4.0 are rolling out digital twins and robotics to lift productivity.[3]Greece4.0, “National Industry 4.0 Project,” greece40.gr Yet only 4% of Greek firms used AI in 2025 versus an 8% EU average, leaving a sizable adoption gap. Consultants able to bridge technology, change management, and skills development stand to gain material share of upcoming budgets.

M&A and Privatization Advisory Demand Surge

The sale of 49% of HEDNO to Macquarie for EUR 2.116 billion (USD 2.39 billion) and TotalEnergies’ EUR 508 million (USD 574 million) renewables divestment signal renewed investor appetite for Greek assets.[4]Watson Farley and Williams, “WFW Advises FRV on Sale of 500 MW Battery Storage Portfolio,” wfw.com A pipeline covering regional airports, interconnection grids, and battery storage systems demands valuation, due-diligence, and post-merger integration support. Advisory firms are packaging sector knowledge, regulatory insight, and local relationships to win mandates, lifting Financial Advisory’s contribution to overall market expansion. These transactions contribute 0.9 percentage points to the forecast CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic and Inflation Headwinds | -0.6% | National, heavier burden on SMEs and cash-strapped public entities | Short term (≤ 2 years) |

| Acute Consultant Talent Shortage | -0.5% | National, acute in Athens and Thessaloniki for digital and ESG roles | Medium term (2-4 years) |

| Rising Price Pressure and In-House Capabilities | -0.3% | National, large enterprises scaling internal teams | Medium term (2-4 years) |

| Cultural Bias Toward Internal Decision-Making | -0.2% | National, persistent in legacy public-sector and family-owned enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic and Inflation Headwinds

Inflation is pushing clients to negotiate fixed-price contracts and shorten engagement horizons, squeezing consultant margins even as the top 500 Greek companies posted USD 168 billion in turnover during 2024.[5]ICAP CRIF, “ICAP Group Financial Results 2024,” icap.gr Profit growth is skewed toward the 20 largest groups, leaving mid-market firms with limited discretionary budgets. Energy and labor cost spikes in capital-intensive industries further undermine consulting spend. Advisory providers are responding with outcome-based pricing and modular service offerings to defend wallet share amid budget volatility.

Acute Consultant Talent Shortage

Time-to-fill for financial-services roles has doubled since 2019, and senior actuarial searches now average 8.4 months. ICT specialists represent just 2.5% of the national workforce, the lowest ratio in the European Union. Firms are poaching Greek diaspora professionals, launching in-house academies, and expanding remote delivery centers such as Deloitte’s Alexander Competence Center to alleviate capacity gaps. Persistent scarcity risks delaying project timelines and inflating billing rates, tempering the sector’s mid-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Transformation Outpaces Traditional Strategy Work

Digital Transformation held the largest 24.46% Greece management consulting services market share in 2025 as ministries, banks, and utilities raced to meet Greece 2.0 deadlines. The Greece management consulting services market size attributed to Risk and Compliance is projected to climb at a 6.54% CAGR through 2031 on the back of CSRD enforcement. Demand is shifting toward platform-based delivery, with EY spending USD 250 million on AI-powered diligence and value-creation tools. Operations and supply-chain engagements are rising as manufacturers implement Industry 4.0 pilots, while niche sustainability and crisis-management practices win contracts linked to the energy transition.

Consultants that combine sector expertise with data engineering and cyber-security skills are winning longer retainers. Strategy work remains central for portfolio-level capital allocation, but fee rates are flattening as clients internalize analytics capabilities. The entrance of AI-native boutiques is intensifying price competition in mid-market technology projects.

By Organization Size: SMEs Close the Gap on Enterprise Clients

Large corporates generated 57.81% of 2025 billings, anchored by multi-year digital cores and privatization mandates. Yet voucher schemes, agri-tech grants, and export-help desks are spurring smaller companies to seek growth and compliance advice, adding a forecast 6.17% CAGR to the SME segment of the Greece management consulting services market size. Consultants are tailoring tiered service menus and subscription models to match mid-market budget cycles.

Enterprises continue to rationalize external spend by hiring former consultants directly, but still rely on advisory partners for specialized diligence, AI ethics, and complex integrations. In contrast, SMEs lack scale to sustain in-house analytics or sustainability teams, keeping external demand more resilient.

By Delivery Model: Hybrid Becomes the Default

On-site engagements retained 65.91% share during 2025 as clients valued proximity for regulatory, tax, and transformation work. However, hybrid models that blend field visits with remote sprints are growing at a 6.62% CAGR. The Greece management consulting services market share for virtual delivery is underpinned by cloud workspaces, 24-hour collaboration hubs, and AI code copilots that accelerate document production.

Remote delivery is also widening the talent pool, allowing firms to deploy diaspora Greeks and specialists from lower-cost provinces. As more ministries accept virtual workshops for RRF reporting, even public-sector clients are embracing mixed formats.

By End User Industry: Public Programs Lead, Energy Transitions Accelerate

The public sector captured 23.07% of 2025 fees, reflecting a surge of e-government and civil-protection tenders tied to EU funds. Energy and resources is poised for the fastest 6.29% CAGR as Greece targets net-exporter status and rolls out 4.7 GW of battery storage. These moves will raise the Greece management consulting services market size linked to power-system planning and permitting.

Banks, insurers, and telecom operators remain heavy technology spenders, yet profit-cycle sensitivity may temper growth beyond 2028. Manufacturing and agri-food clients are layering predictive maintenance and farm-management tools onto grant-funded capital upgrades, generating new advisory flows around data architecture and skills transfer.

Geography Analysis

Athens and wider Attica host most headquarters, ministries, and investor roadshows, anchoring more than half of national consulting revenue. Projects include Gov.gr’s customer-relationship platform and Eurobank’s agentic AI factory, both delivered through mixed on-site and remote squads. Talent density in finance and law keeps the capital region the preferred base for high-value transaction and regulatory engagements.

Thessaloniki is evolving into a secondary hub as Deloitte’s Alexander Competence Center and several AI boutiques tap North Macedonian and Balkan labor pools. Port upgrades, hospital digitization, and a new cruise strategy signal diversification beyond traditional logistics work. Universities provide a steady stream of engineers who can be trained in RPA, cloud, and analytics, improving project staffing flexibility.

Elsewhere, Crete, the Peloponnese, and Central Greece contribute growing shares of agri-tech, tourism, and renewable-energy contracts. CAP Strategic Plan grants and the BESS Acceleration Scheme push advisory demand into rural regions for subsidy applications, site selection, and stakeholder engagement. Consultants are building satellite offices and virtual-first teams to serve these dispersed opportunities.

Competitive Landscape

The market remains moderately fragmented: the Big Four and top strategy houses dominate large deals, while mid-tier internationals and Greek specialists compete fiercely for SME and regional mandates. EY’s acquisition of Aqurance underscores a vertical-specialization play, adding life-sciences depth to an already broad portfolio. Grant Thornton’s partnership with Athena Research Center illustrates how mid-sized firms use academic alliances to scale data-science credentials.

Technology partnerships are now critical differentiators. EY has bundled Microsoft and OpenAI models into diligence and capital-planning platforms, whereas Deloitte funnels cloud and RPA work to its Thessaloniki center to cut delivery cost. Boutique disruptors such as Proxima and Northbound Tech lever generative AI to underprice routine automation projects, squeezing traditional fee models. ISO certifications and public-sector framework agreements remain gatekeepers for many tendered projects, reinforcing incumbents’ advantage even as new entrants raise competitive pressure.

Greece Management Consulting Services Industry Leaders

PwC Greece

EY Greece

Deloitte Greece

KPMG Greece

Accenture Greece

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Grant Thornton Greece and Athena Research Center signed a four-year memorandum of understanding to launch an AI Center of Excellence.

- March 2026: EY Greece acquired Aqurance, adding 65 life-sciences specialists and Veeva expertise.

- March 2026: Thessaloniki Port Authority engaged Five Senses Consulting and Development to craft a cruise-sector growth roadmap.

- February 2025: EY Greece rebranded its deal and strategy practices under EY-Parthenon and invested USD 250 million in AI platforms.

Greece Management Consulting Services Market Report Scope

The Greece Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current Greece management consulting services market size and how fast will it grow?

The market stands at USD 0.95 billion in 2026 and is forecast to reach USD 1.28 billion by 2031, reflecting a 6.14% CAGR.

Which service line generates the largest share of consulting revenue in Greece?

Digital Transformation services contributed 24.46% of 2025 revenue, driven by EU-funded modernization projects.

Why is ESG consulting demand rising among Greek companies?

Law 5164/2024 implements the Corporate Sustainability Reporting Directive, exposing firms to steep penalties and pushing them to seek external ESG expertise.

How are delivery models changing in the Greek consulting market?

Hybrid formats that mix limited on-site work with remote sprints are expanding at a 6.62% CAGR as clients embrace virtual collaboration.

Which industries are expected to drive the fastest consulting growth to 2031?

Energy and resources projects, especially battery storage and renewables, are set to deliver the highest 6.29% CAGR thanks to Greece's net-exporter energy goal.

What competitive strategies are consulting firms adopting to address the talent shortage?

Firms are opening regional delivery centers, recruiting diaspora professionals, and investing in AI-enabled tools to boost consultant productivity and scale.

Page last updated on: