Italy Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

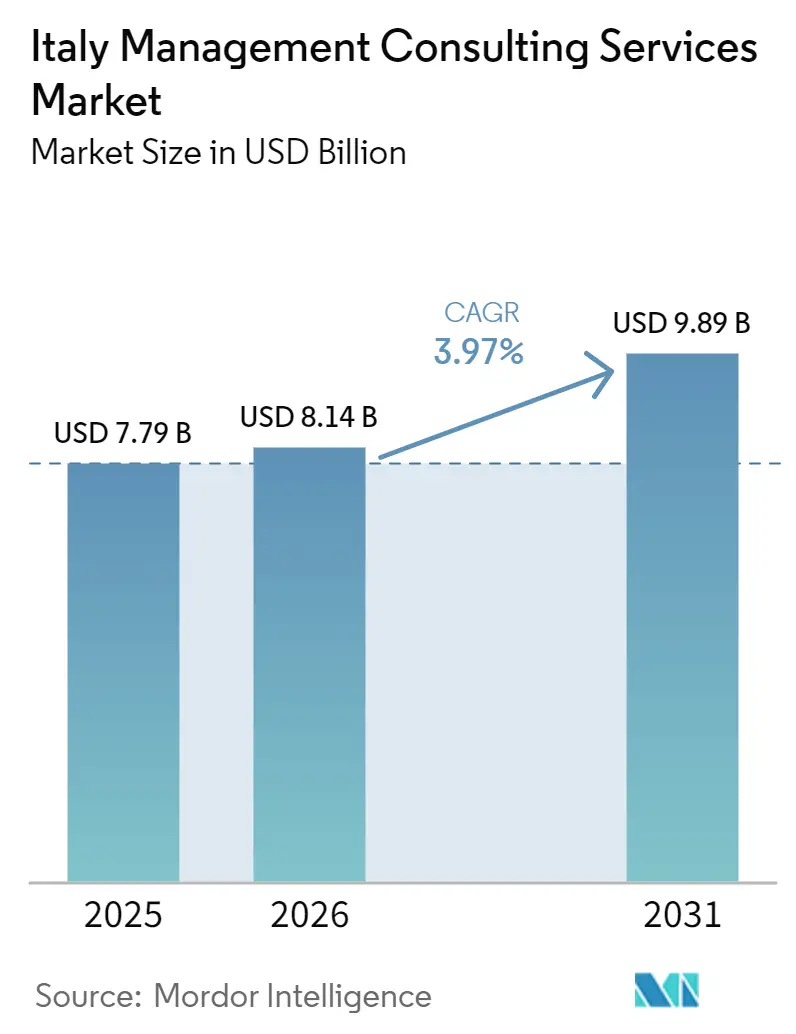

| Base Year Market Size (2025) | USD 7.79 Billion |

| Market Size (2026) | USD 8.14 Billion |

| Market Size (2031) | USD 9.89 Billion |

| Growth Rate (2026 - 2031) | 3.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Management Consulting Services Market Analysis by Mordor Intelligence

The Italy management consulting services market size is expected to increase from USD 7.79 billion in 2025 to USD 8.14 billion in 2026 and reach USD 9.89 billion by 2031, growing at a CAGR of 3.97% over 2026-2031. Advisory budgets are tilting toward compliance-linked and digitally enabled mandates as enterprises translate Recovery and Resilience Facility funding and Corporate Sustainability Reporting Directive obligations into technology and change-management roadmaps. Fee-capped public contracts and elongated milestone schedules temper near-term revenue velocity, yet the full contract pipeline remains solid, locking in billable backlogs for large firms. Generative-AI tooling is compressing low-value diagnostics and documentation work, prompting consultants to reposition around implementation, data architecture, and outcome-based engagements. Competitive dynamics favor firms that couple sector expertise with technology delivery at scale, while boutiques hedge through deep vertical focus and success-fee pricing models.

Key Report Takeaways

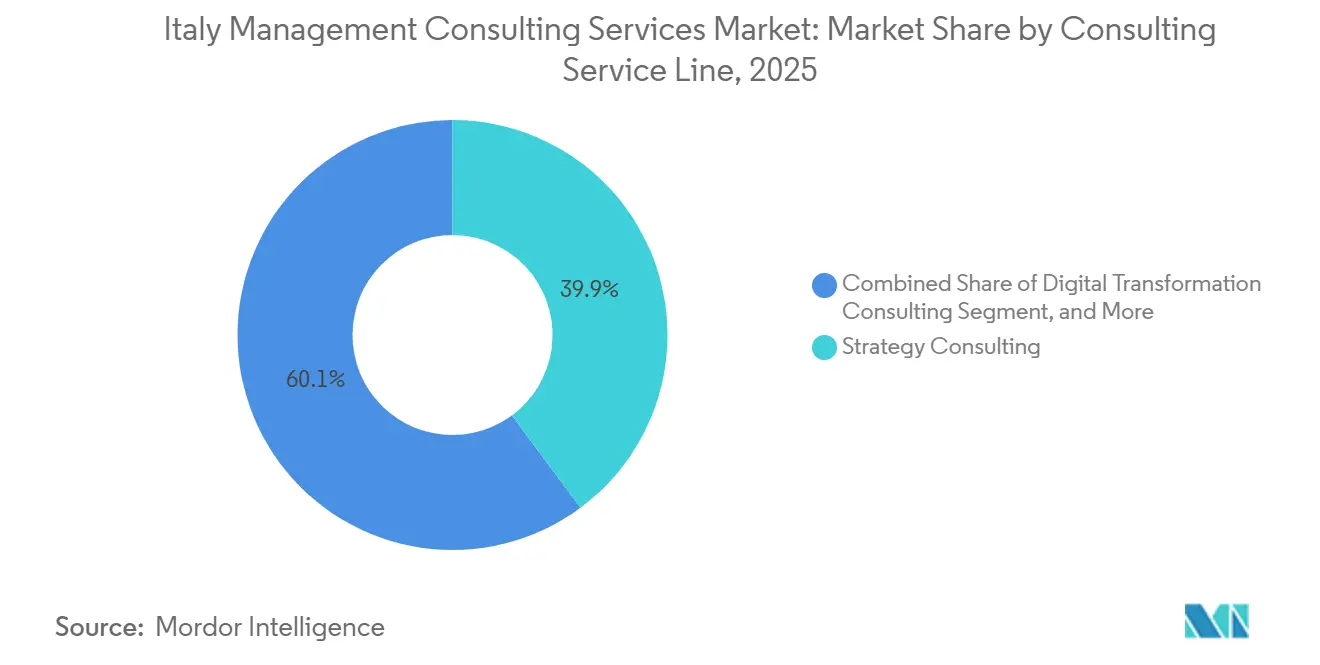

- By consulting service line, Strategy Consulting led with 39.86% of the Italy management consulting services market share in 2025, while Digital Transformation Consulting is projected to expand at a 4.89% CAGR through 2031.

- By organization size, Large Enterprises held 66.43% of the Italy management consulting services market size in 2025, whereas Small and Medium-Sized Enterprises are set to record a 4.07% CAGR between 2026-2031.

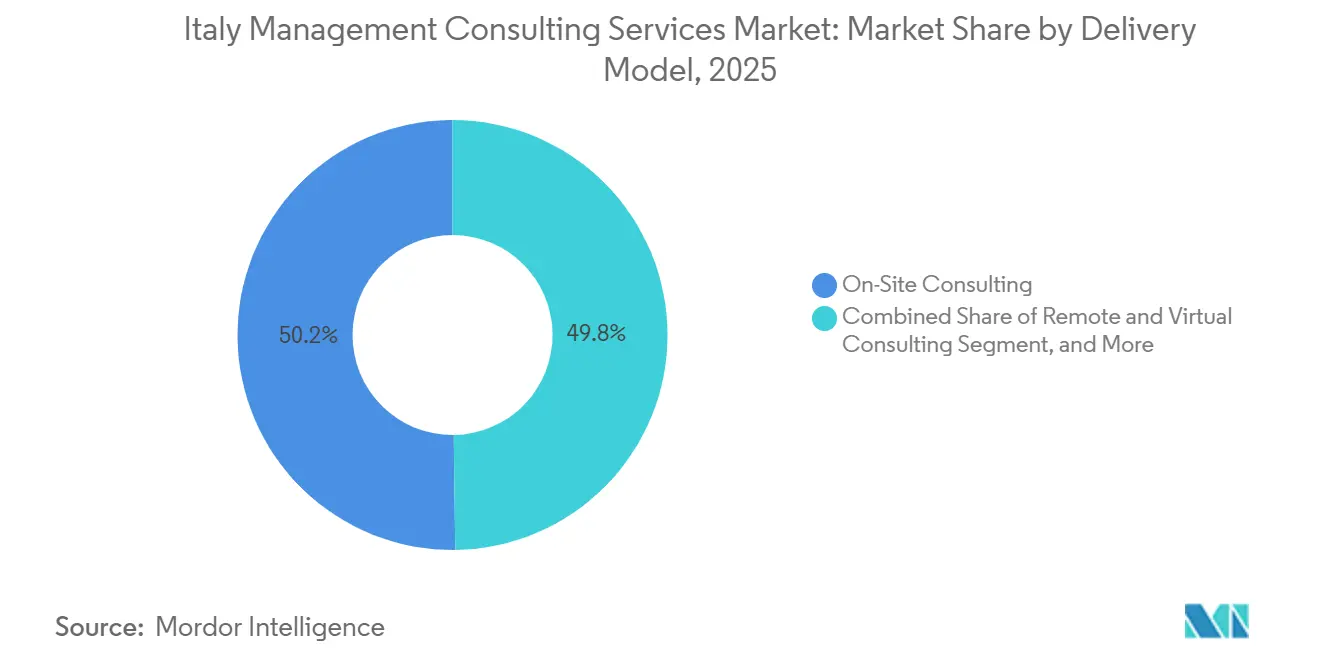

- By delivery model, On-Site Consulting accounted for 50.21% share of the Italy management consulting services market size in 2025 and Hybrid Consulting is advancing at a 4.63% CAGR through 2031.

- By end user industry, the Public Sector commanded 16.38% revenue share in 2025; Energy and Resources is forecast to post the fastest 4.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Digital-Transformation Funding From PNRR | +1.2% | National, concentration in Lombardy, Lazio, Emilia-Romagna | Medium term (2-4 years) |

| ESG-Linked Compliance Deadlines Under CSRD | +0.9% | National, early adoption in listed corporations and financial services | Short term (≤ 2 years) |

| Growing Mid-Market Demand for Outcome-Based Contracts | +0.8% | National, strongest in Veneto and Piedmont manufacturing hubs | Long term (≥ 4 years) |

| Reshoring of Manufacturing Supply Chains | +0.7% | Northern Italy with spillover to Central regions | Medium term (2-4 years) |

| Generative-AI Productivity Tools for Project Delivery | +0.5% | National, led by technology and professional-services sectors | Short term (≤ 2 years) |

| Regional Cohesion Funds Unlocking Southern-Italy Demand | +0.4% | Southern Italy (Campania, Sicily, Puglia, Calabria) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital-Transformation Funding From PNRR

EUR 40.7 billion (USD 46 billion) of recovery grants have seeded the largest publicly funded digital modernization wave in Italy’s post-war history. Ministries and municipalities missed many 2024 cloud-migration targets, so advisory work has pivoted from blueprinting to embedded execution teams that integrate agile delivery with procurement oversight.[1]Agenzia per l'Italia Digitale, “Strategia Nazionale per l'Intelligenza Artificiale 2024-2026,” agid.gov.it Consultancies able to pair enterprise-grade cybersecurity, data-platform design, and change-management capability capture disproportionate wallet share. As milestone slippage triggers renegotiations, firms with scalable hybrid staffing models preserve margin by combining remote architects with on-site scrum leads.

ESG-Linked Compliance Deadlines Under CSRD

Roughly 2,000 Italian issuers must publish double-materiality sustainability statements in 2026, escalating to several thousand mid-caps by 2027 after the Omnibus Directive phase-in.[2]European Commission, “Corporate Sustainability Reporting Directive,” ec.europa.eu Listed corporations are front-loading spending to build auditable data architectures that stitch Scope 3 emissions, governance metrics, and social indicators into existing ERP stacks. High-touch, multi-year transformation programs dominate at the top end, while mid-market clients postpone until lower-cost, productized toolkits mature, creating a bifurcated demand pattern that rewards consultancies offering both premium bespoke builds and plug-and-play diagnostics.

Growing Mid-Market Demand for Outcome-Based Contracts

Cost-sensitive firms with EUR 10-250 million (USD 11.6-292 million) revenue increasingly accept external advice when payment hinges on measurable gains. Success-fee engagements flourish in e-commerce acceleration, working-capital optimization, and sales-force digitization because performance data are transparent and cycle times short. Advisors absorb greater delivery risk and therefore concentrate on repeatable solutions with clear benchmarks. The model tilts market power toward larger firms that can fund upfront effort, but it also grants nimble boutiques an entry route if they lock in referenceable wins within narrow verticals.

Reshoring of Manufacturing Supply Chains

Transizione 4.0 tax credits covering automation and digital upgrades spur manufacturers to relocate production from Asia to Northern Italy’s industrial corridors.[3]Ministero delle Imprese e del Made in Italy, “Transizione 4.0 - Incentivi per la Trasformazione Digitale,” mimit.gov.it The advisory workload spans site assessment, supplier network recertification, workforce reskilling, and carbon-footprint modeling. Assignments integrate operations excellence with ESG positioning, as boards showcase shortened logistics chains to meet emissions targets. Engagements thus blend classic lean consulting with data-driven sustainability analytics, favoring firms fielding cross-functional teams versed in plant engineering and carbon accounting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-Procurement Price Caps on Consulting Fees | -0.6% | National, most acute in central government and regional contracts | Short term (≤ 2 years) |

| Expansion of In-House Strategy Units at Large Enterprises | -0.5% | National, concentrated in banking, utilities, telecommunications | Medium term (2-4 years) |

| Fragmented SME Client Base With Limited Budgets | -0.3% | National, higher impact in Southern and rural areas | Long term (≥ 4 years) |

| AI-Driven Self-Service Advisory Platforms | -0.2% | National, early adoption in technology and professional-services sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Public-Procurement Price Caps on Consulting Fees

Revised Codice degli Appalti ceilings limit senior-consultant rates to EUR 120-150 (USD 135.6-169.5) per hour, roughly half private-sector billing norms. Margin compression pushes premium talent toward corporates, degrading skill depth on public assignments and extending delivery timelines.[4]Italian Parliament, “Parliamentary Inquiry on PNRR Implementation and Consulting Expenditure,” camera.it To compensate, firms industrialize delivery through accelerators, templatized diagnostics, and near-shore support centers, but complex PNRR programs still risk overruns that caps rarely cover.

Expansion of In-House Strategy Units at Large Enterprises

Banks, utilities, and telecom majors are staffing former tier-one consultants to retain institutional know-how and cut recurring advisory outlays. Routine planning and KPI tracking migrate inside, shrinking the baseline addressable pool for external vendors. Consultants remain relevant for episodic transformations and regulatory shocks, yet must differentiate through proprietary data assets, sector-specific analytics, and execution capacity that captive teams cannot replicate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Strategy Anchors, Digital Accelerates

Strategy Consulting led the Italy management consulting services market in 2025, capturing 39.86% share on the back of restructuring and succession-driven M&A mandates. The service line remains essential when boards need independent validation of portfolio moves, but discretionary spend is gradually ceding ground to tech-centric mandates. Digital Transformation Consulting, projected to post a 4.89% CAGR, benefits directly from PNRR cloud-migration grants and pervasive generative-AI pilots, shifting budgets toward data-architecture design and change management. The Italy management consulting services market size linked to Digital projects expands as public agencies and corporates scale pilots into enterprise rollouts.

Operations, HR, and Financial Advisory consulting maintain mid-single-digit shares as manufacturers optimize re-shored facilities and banks manage Basel IV and MiFID II updates. ESG-centric offerings, often bundled into Risk and Compliance practices, are emerging as stand-alone profit pools. Firms that weave carbon-accounting templates into ERP upgrades lock in cross-functional contracts, while boutiques unable to fund tooling investments pivot toward niche verticals such as luxury-goods customer experience or pharma supply-chain validation.

By Organization Size: Enterprises Dominate, SMEs Gain Momentum

Large Enterprises accounted for 66.43% of 2025 revenue because multi-year transformations, regulatory compliance, and cross-border M&A demand scale and multidisciplinary teams. They continue to award framework agreements that bundle advisory, implementation, and managed services, anchoring predictable revenue for global firms. Yet the Italy management consulting services market is progressively widening as SMEs tap Transizione 4.0 credits that reimburse up to 50% of eligible digital-consulting invoices. The Italy management consulting services market share attributable to SMEs is forecast to climb through 2031, underpinned by simplified, productized solutions delivered in sprint formats that cut cost and time to value.

Winning the SME wallet demands localized marketing, partnerships with trade associations, and success-fee billing. Delivery risk is higher because owner-managers may lack project governance structures, so consultants standardize playbooks and reserve on-site visits for critical milestones. Hybrid and remote delivery models expand margin headroom by blending regional engagement managers with lower-cost virtual specialists.

By Delivery Model: Hybrid Consulting Builds Scale

On-Site engagements still represented just over half of 2025 spend as Italian business culture prizes face-to-face sessions for strategic or sensitive mandates. However, hybrid arrangements are advancing at a 4.63% CAGR thanks to improved virtual-workplace adoption and client focus on travel-cost containment. The Italy management consulting services market size attached to hybrid models reflects savings that consultants pass back to clients while protecting profit through higher utilization of global specialist pools.

Pure remote consulting remains a niche, attractive to tech-savvy founders and minor public tenders with stringent cost ceilings. Hybrid delivery, by contrast, supports accountability and relationship depth without requiring weeks of on-site presence. Firms invest in secure digital workspaces and train facilitators on virtual sprint orchestration to avoid collaboration friction. Clients reciprocate by opening data-room access and decision windows on cloud platforms, further legitimizing blended delivery.

By End User Industry: Public Sector Leads, Energy Surges

Public agencies, driven by recovery-fund programs and healthcare digitization, consumed 16.38% of 2025 spend. Despite price caps, project volumes remain high, sustaining a critical book of business for tier-one and audit-linked consultancies. Energy and Resources engagements, supported by Enel’s EUR 3.2 billion (USD 3.6 billion) grid investment and hydrogen-economy pilots, are on track to grow at 4.42% CAGR, the fastest among verticals. The Italy management consulting services market size attached to energy transitions expands as utilities seek counsel on EU taxonomy alignment, smart-grid engineering, and power-purchase-agreement structuring.

Banking and Insurance retains a stable share owing to ongoing regulatory waves and omnichannel transformation. Manufacturing demand rebounds as reshoring and automation lift capital-expenditure planning, while healthcare institutions chase electronic-medical-record integration and telehealth scaling. Niche sectors, from luxury retail to tourism, procure experience-design and data-driven marketing expertise, giving smaller boutiques room to specialize and command premium pricing for tailored domain knowledge.

Geography Analysis

Regional concentration shapes how the Italy management consulting services market unfolds. Northern regions led by Lombardy, Veneto, Piedmont, and Emilia-Romagna generated roughly 65% of 2025 demand, underpinned by dense corporate headquarters, industrial clusters, and financial hubs. Central Italy absorbed around 25%, fueled by Rome’s ministerial ecosystem and Lazio’s services corridor. Southern Italy and the Islands contributed the remaining 10%, reflecting lower enterprise density and project scale. Cohesion-fund inflows and Just Transition subsidies aim to rebalance the footprint, yet historical under-utilization of EU grants signals execution risk that consultancies must factor into resourcing.

Firms calibrate office footprints accordingly: global majors field multi-disciplinary teams in Milan and Rome, while maintaining satellite pods in Naples, Palermo, and Bari to chase EU-funded public projects. Italian boutiques cluster near Northern manufacturing belts and serve Southern clients through hybrid models, limiting fixed overhead. This distribution reinforces a two-tier market, with premium advisory concentrated in the North and grant-compliance support prevalent in the South.

Pan-European mandates further influence geography. Cross-border cloud migrations and CSRD rollouts require harmonized delivery across corporate footprints, advantaging consultancies that integrate Italian workstreams into broader EU networks. Political volatility and changing coalition governments inject uncertainty into public-sector tendering, nudging risk-averse clients to opt for established brands with proven delivery in comparable EU jurisdictions.

Competitive Landscape

Roughly 45% of 2025 revenue accrued to the Big Four plus McKinsey, Bain, and Boston Consulting Group, yet the Italy management consulting services market remains contestable because no single player exceeds 15% share. Tier-one firms leverage global playbooks, analytics assets, and audit-linked relationships to monopolize large public tenders and multinational frameworks. Mid-tier integrators such as Accenture, Capgemini, and IBM Consulting compete on end-to-end execution and proprietary technology accelerators, while Italian specialists, notably Reply, Engineering, and BIP, win mid-market digital mandates through localized talent and outcome-based pricing.

Strategic moves reinforce these positions. Accenture’s acquisition of IQT added 400 SAP and Oracle consultants, enabling deeper penetration of PNRR-funded ERP modernizations. Reply’s double-digit revenue expansion validates a productized, cloud-native delivery model that blends advisory with deployment and managed services. Capgemini’s partnership with Enel demonstrates the advantage of pairing sector expertise with engineering depth on large-scale energy-transition programs.

Emerging disruptors include AI-powered self-service platforms that automate benchmarking and proposal drafting. Top firms embed large-language-model copilots to cut production hours, but must manage client expectations on originality and data security. Boutiques unable to fund comparable tooling lean into deep vertical specialization or alliance membership in global consulting networks to maintain relevance.

Italy Management Consulting Services Industry Leaders

Accenture Plc

Deloitte Italy

PwC Italy

KPMG Advisory

EY Advisory

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NTT DATA unveiled its Smart AI Agent Ecosystem, converting legacy RPA bots into autonomous agents for healthcare, automotive, finance, and supply-chain clients.

- April 2025: EY Italy appointed Stefania Boschetti as CEO, the first woman to lead a Big 4 firm in the country, following a 65% revenue rise since 2020.

- April 2025: McKinsey Italy issued a hydrogen-economy outlook estimating EUR 10 billion (USD 11.3 billion) in annual investment potential by 2030.

- January 2025: Accenture closed the acquisition of IQT, a 400-employee SAP and Oracle specialist with EUR 60 million (USD 67.8 million) revenue, bolstering public-sector ERP capacity.

Italy Management Consulting Services Market Report Scope

The Italy Management Consulting Services Market Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Italy management consulting services market and how fast is it growing?

The market stands at USD 8.14 billion in 2026 and is projected to reach USD 9.89 billion by 2031, reflecting a 3.97% CAGR from 2026.

Which consulting service line is expanding the fastest in Italy?

Digital Transformation Consulting leads growth with a projected 4.89% CAGR through 2031, buoyed by cloud migrations and generative-AI adoption.

How are outcome-based contracts changing client adoption among Italian SMEs?

By tying fees to measurable performance, outcome-based models lower cost barriers, unlocking latent demand and pushing SME consulting spend to a 4.07% CAGR.

What regional factors shape demand within Italy?

Northern regions generate about 65% of consulting revenue due to industrial density, while Southern demand depends heavily on EU cohesion funds and public projects.

How do public-procurement fee caps affect consulting firms?

Hourly-rate ceilings compress margins on PNRR contracts, driving firms to industrialize delivery and cross-sell uncapped software or training services.

Which industry vertical is expected to post the highest consulting growth through 2031?

Energy and Resources is forecast to expand at 4.42% CAGR as utilities invest in grid digitalization and renewable-energy integration projects.

Page last updated on: