Mexico Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

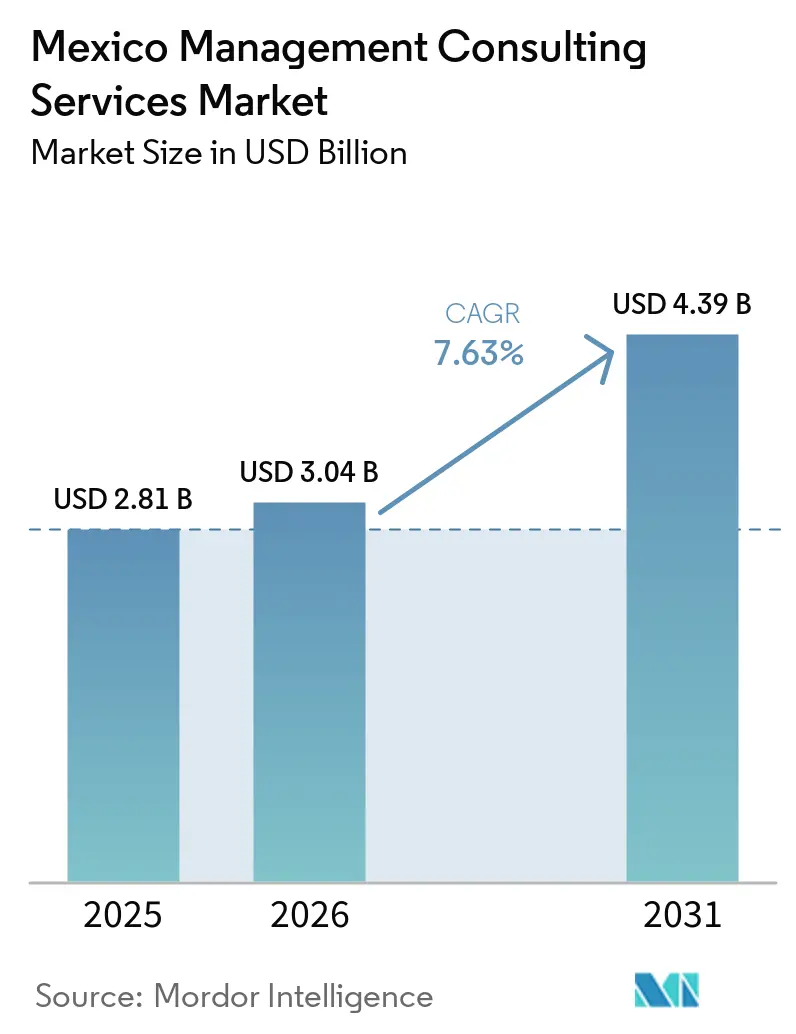

| Base Year Market Size (2025) | USD 2.81 Billion |

| Market Size (2026) | USD 3.04 Billion |

| Market Size (2031) | USD 4.39 Billion |

| Growth Rate (2026 - 2031) | 7.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Management Consulting Services Market Analysis by Mordor Intelligence

The Mexico management consulting services market size is projected to expand from USD 2.81 billion in 2025 and USD 3.04 billion in 2026 to USD 4.39 billion by 2031, registering a CAGR of 7.63% between 2026 to 2031. Near-shoring-related efficiency drives, mandatory sustainability reporting, and the ongoing digital-transformation cycle are combining to lift consulting spend across Mexican enterprises. Large manufacturers are fine-tuning production footprints to serve the United States more quickly, listed companies are racing to meet the NIS A-1 and B-1 disclosure rules, and boards are investing in cloud, analytics, and automation to counter energy and logistics bottlenecks. At the same time, the 2026 USMCA review and tighter anti-money-laundering laws are steering buyers toward governance-heavy advisory, while hybrid work keeps face-to-face workshops relevant even as remote delivery gains traction.

Key Report Takeaways

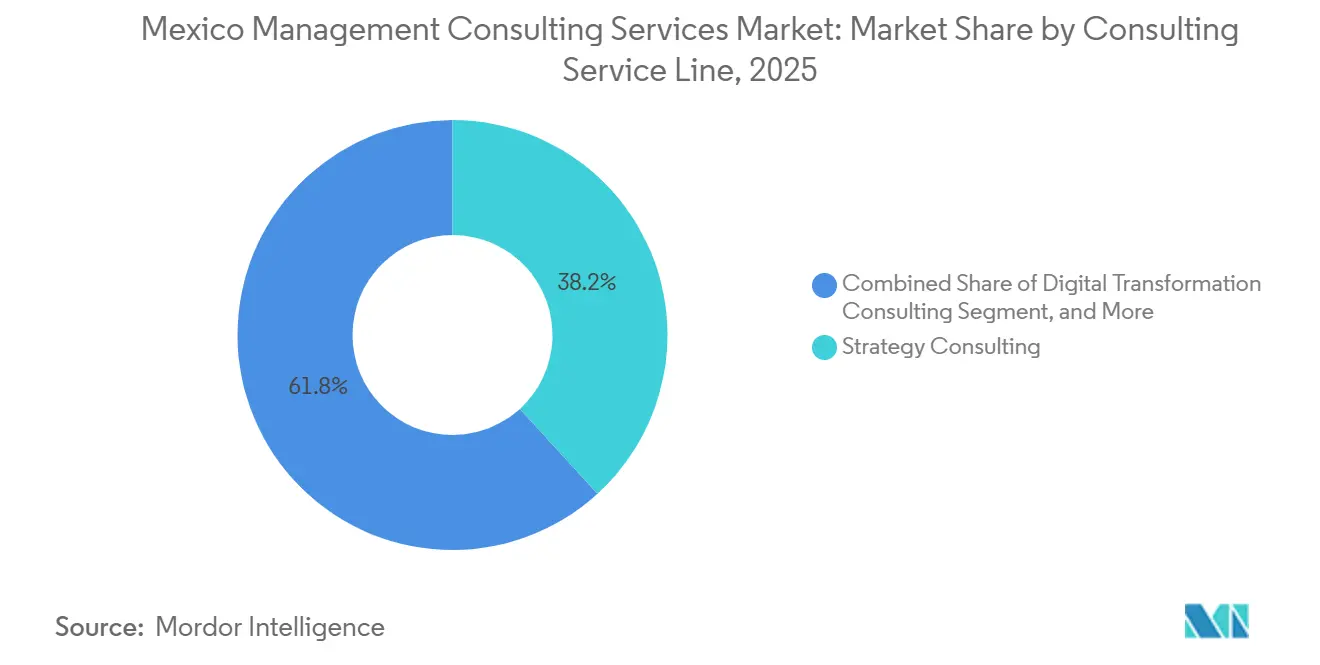

- By consulting service line, strategy consulting led with 38.23% of the Mexico management consulting services market share in 2025, whereas risk and compliance consulting is forecast to grow at a 7.89% CAGR through 2031.

- By organization size, large enterprises accounted for 72.08% of the Mexico management consulting services market size in 2025, while small and medium-sized enterprises are expanding at a 7.71% CAGR over 2026-2031.

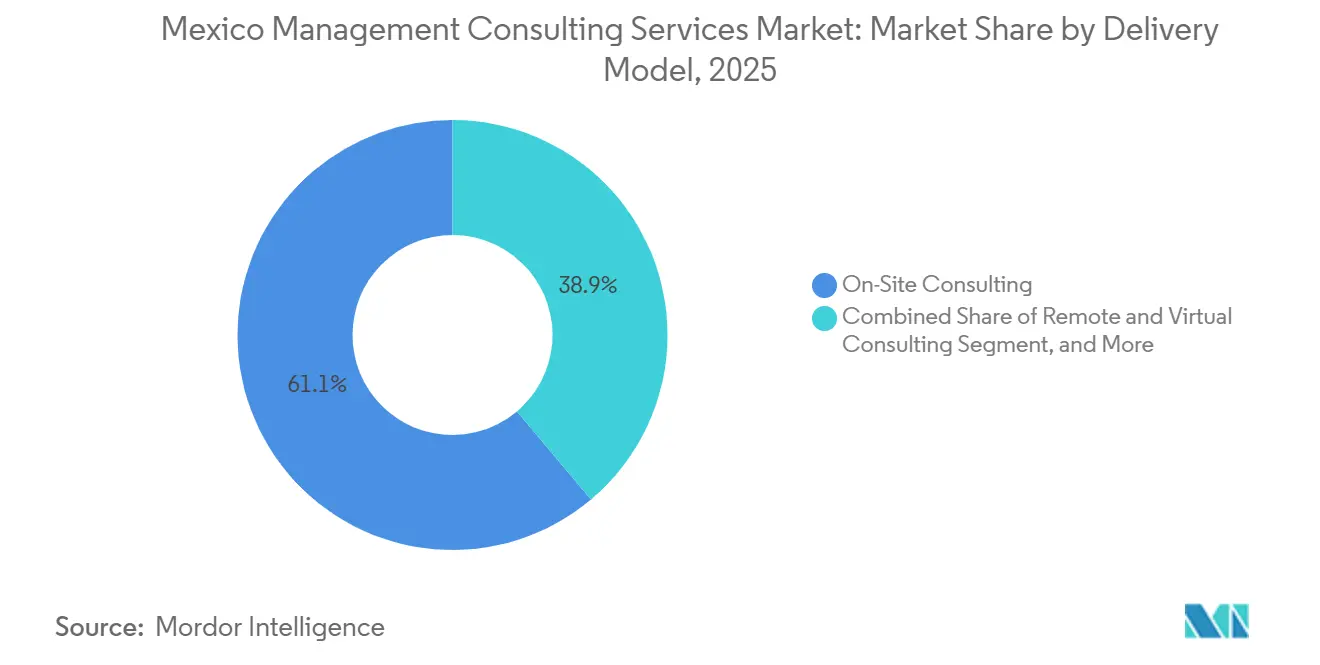

- By delivery model, on-site consulting captured 61.14% of the Mexico management consulting services market share in 2025, yet remote and virtual consulting is advancing at a 7.92% CAGR to 2031.

- By end-user industry, IT and telecommunications represented 26.48% of the Mexico management consulting services market size in 2025, and healthcare is projected to grow at a 7.83% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation Acceleration in Mexican Enterprises | +1.8% | National, focused in Mexico City, Monterrey, Guadalajara | Medium term (2-4 years) |

| Near-Shoring Wave Fueling Operational-Efficiency Advisory | +2.1% | Nuevo León, Querétaro, Baja California, Guanajuato | Short term (≤ 2 years) |

| Public-Sector Infrastructure Megaprojects (Maya Train, Interoceanic Corridor) | +0.9% | Southern states | Long term (≥ 4 years) |

| Mandatory Sustainability Reporting (NIS A-1, B-1) | +0.7% | National, early adoption among listed firms | Short term (≤ 2 years) |

| Expansion of Fintech Regulatory Sandbox | +0.6% | Mexico City hub | Medium term (2-4 years) |

| USMCA Annex 16 Work-Visa Fast-Track | +0.5% | Northern border states, Mexico City | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Acceleration in Mexican Enterprises

Cloud migration, analytics, and automation programs continue to dominate board agendas, with KPMG finding that 65% of Mexican executives approved new digital budgets for 2025. The push is strongest in consumer-goods, banking, and automotive groups that must integrate legacy ERP stacks with real-time supply-chain tools. Accenture’s December 2025 brief highlighted that rising electricity constraints in northern corridors are forcing companies to adopt hybrid-cloud architectures that balance on-premises loads with hyperscale capacity.[1]Accenture, “Macro Foresight Brief December 2025,” accenture.com Consulting mandates therefore bundle technology road-mapping with energy-efficiency playbooks, creating multi-disciplinary engagements that blend IT, operations, and sustainability skills. Vendors able to combine cloud engineering with regulatory insight are winning longer, outcome-based contracts, especially when they embed Mexican delivery teams to cut latency and cost.

Near-Shoring Wave Fueling Operational-Efficiency Advisory

Bilateral trade with the United States surpassed USD 800 billion in 2025, while foreign direct investment topped USD 40 billion, yet Deloitte observed that only 12% of announced factories had reached the operational stage by early 2026. Permitting queues, labor shortages, and last-mile logistics gaps are creating strong demand for consultants who can navigate IMMEX, supervise green-field construction, and stand up dual-use warehousing. Roland Berger estimates 20-25% labor-cost savings versus China for U.S.-bound shipments, but cautions that quality-control systems differ across 400+ Mexican industrial parks.[2]Roland Berger, “Nearshoring to Mexico,” rolandberger.com This complexity is steering engagements toward plant-layout redesign, supplier localization, and workforce-training partnerships with state technical institutes. The speed at which firms secure executive buy-in and government incentives often decides which consultants prevail.

Public-Sector Infrastructure Megaprojects

The 1,554-kilometer Maya Train and the Interoceanic Corridor freight link are unlocking advisory scopes in project-management offices, environmental compliance, and multimodal logistics. Mexico’s transport ministry confirmed phased openings through 2026, triggering tenders for cost-control and social-impact monitoring.[3]Government of Mexico, “Tren Maya,” gob.mx Yet persistent security incidents in Chiapas and Oaxaca raise execution risk, so firms with entrenched public-sector relationships or local partnerships are best positioned. Advisory teams are embedding specialists in public-private-partnership finance, indigenous community consultation, and NOM-level environmental assessments, often under tight scrutiny from civil-society groups. The multi-year horizon makes these engagements strategically attractive despite margin pressure in early phases.

Mandatory Sustainability Reporting

Mandatory disclosure under NIS A-1 and B-1 began in 2025, requiring listed companies to quantify greenhouse-gas inventories, climate risks, and transition plans in line with ISSB alignment.[4]CINIF, “NIS A-1 and NIS B-1 Sustainability Standards,” cinif.org.mx Early movers are banking, cement, and steel firms that already face investor pressure, while mid-caps are now onboarding consultants to design data pipelines and assure metrics ahead of the 2026 filing window. PwC’s Mexico Acceleration Center reports surging demand for automated ESG dashboards that plug directly into finance and procurement systems. Engagements commonly bundle materiality assessments, energy-efficiency audits, and supply-chain Scope 3 mapping, thereby favoring firms that field both sustainability strategists and data-engineering talent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slowing Real GDP Growth and Fiscal Tightening | -0.8% | National | Short term (≤ 2 years) |

| High Informality Limiting Addressable Spend | -0.6% | National, acute in southern and rural states | Long term (≥ 4 years) |

| Sub-Contracting Reform and STPS Registry Friction | -0.4% | Nationwide, especially manufacturing | Medium term (2-4 years) |

| Security and Infrastructure Gaps Raising Project-Execution Risk | -0.5% | Southern states, border corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Slowing Real GDP Growth and Fiscal Tightening

The International Monetary Fund expects real GDP to grow 1.5% in 2026, a slight dip from 2025, while the federal deficit is targeted to fall below 3% of GDP.[5]International Monetary Fund, “World Economic Outlook Update,” imf.org Public agencies are trimming discretionary spend, limiting advisory budgets to megaproject oversight and digital-government essentials. Banco de México kept its benchmark rate at 10% through most of 2025, and although a gradual easing cycle has started, real borrowing costs remain high, prompting private mid-caps to delay non-critical consulting engagements. In this climate, cost-out and turnaround work outperforms growth-strategy mandates, squeezing fee rates and shortening contract durations.

High Informality Limiting Addressable Spend

Roughly 55% of Mexico’s workforce remains in the informal economy, dampening the total pool of clients that must comply with complex labor and tax standards. November 2025 updates to the sub-contracting law raised penalties for non-registration under REPSE, nudging some firms toward formalization, yet many small merchants prefer to stay outside the system.[6]Secretaría del Trabajo y Previsión Social, “Sub-Contracting Reform,” stps.gob.mx Consulting firms therefore focus on the formal corporate core, listed entities, multinationals, and export-oriented manufacturers, leaving large swaths of retail, hospitality, and agriculture under-served. The structural cap on demand weighs on long-term market expansion even as GDP per capita climbs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance Pressures Elevate Risk Advisory

Risk and compliance consulting is set to record a 7.89% CAGR through 2031, buoyed by fresh anti-money-laundering rules and fintech sandbox oversight. Mexico management consulting services market size attached to this segment benefits from banks, fintechs, and multinational manufacturers seeking gap assessments ahead of the FATF review. Meanwhile, strategy consulting retained 38.23% Mexico management consulting services market share in 2025 on the back of near-shoring feasibility studies and M&A due diligence. Growth is now moderating because most footprint decisions for large manufacturers have been taken, shifting attention to execution and compliance.

Digital transformation consulting continues to gain as boards invest in cloud, analytics, and automation, yet electricity shortages in northern plants are making hybrid-cloud blueprints more attractive than full public-cloud migrations. Operations and HR consulting enjoy steady pipelines thanks to lean-manufacturing programs and acute talent shortages in robotics, welding, and cybersecurity. Financial advisory work tied to mid-market private-equity exits and valuation services stays resilient though more price sensitive.

By Organization Size: SME Formalization Unlocks Advisory Potential

Small and medium-sized enterprises will expand consulting spend at a 7.71% CAGR over 2026-2031, supported by stricter labor-registry rules that force business owners to formalize payroll processes. Although large enterprises represented 72.08% of the Mexico management consulting services market size in 2025, their forward growth rate slows as many have already completed the primary phases of site selection and core system upgrades.

SMEs are requesting packaged compliance, accounting, and payroll solutions, usually delivered via remote teams to keep fees affordable. Fintech adoption also pulls compliance advisers into startup ecosystems clustered in Mexico City and Guadalajara, where more than 100 sandbox participants must align with the Fintech Law 2.0 rulebook. For large enterprises, priority spending now tilts toward multi-year ESG, AI, and cybersecurity programs, engagements dominated by global integrators with end-to-end capabilities.

By Delivery Model: Hybrid Norms Sustain On-Site Dominance

On-site engagements still commanded 61.14% Mexico management consulting services market share in 2025 because Mexican executives value co-located problem-solving, yet remote and virtual services are growing fastest at 7.92% CAGR. Hybrid models that splice in-person workshops with asynchronous delivery now represent a rising mid-point, letting firms cut travel cost while preserving relationship intensity.

Remote delivery scales best for document-heavy work such as regulatory gap analyses, training, or analytics dashboards. Strategy and change-management engagements remain mostly in person, but even here, milestone reviews are often virtual. Slalom’s 2024 tech center launch in Mexico City illustrates the pivot to hybrid setups that combine local consultants with global domain leads. Near-shore centers in Monterrey and Guadalajara further enable follow-the-sun staffing for U.S. clients.

By End-User Industry: Healthcare Digital Transformation Accelerates Advisory Demand

Healthcare consulting is projected to grow at 7.83% CAGR as providers digitize records and insurers seek cost containment. The Mexico management consulting services market size attached to electronic health record rollouts is expanding as hospitals chase MXN 38 billion (USD 2.11 billion) of potential administrative savings each year.

IT and telecommunications held 26.48% share in 2025 due to 5G deployment and cybersecurity investments, but growth eases because flagship network builds conclude. Manufacturing remains an anchor buyer of operations consulting tied to lean and Six Sigma programs across more than 400 industrial parks. Banking and insurance focus on risk-model modernization ahead of Basel III and IFRS 17 deadlines, while public-sector demand hinges on the pace of fiscal consolidation.

Geography Analysis

Mexico City accounts for the lion’s share of advisory spending thanks to its concentration of corporate headquarters, financial institutions, and federal agencies. Strategy mandates, digital-transformation roadmaps, and large ESG programs are typically scoped and governed from the capital, explaining why every global integrator maintains a flagship office there. Monterrey follows as the operational-efficiency hub, its manufacturing base spanning automotive, aerospace, and steel. Nuevo León topped near-shoring FDI inflows in 2025 and is now home to aggressive plant-optimization and workforce-training projects that demand on-site consultant.

Guadalajara is emerging as a technology cluster, drawing cloud engineering and R&D strategy engagements, particularly in semiconductors and medical devices. Querétaro and Baja California rank as fast-growing secondary nodes, helped by cross-border e-commerce logistics and aerospace component plants. Southern states such as Chiapas and Tabasco rely on megaproject contracts tied to the Maya Train, creating a narrow but high-value niche for project-management offices capable of handling environmental impact statements.

Border cities, Tijuana, Ciudad Juárez, Reynosa, support maquiladora clients that need lean consulting and labor-reform advice, though security concerns make extended on-site work costlier. Central states including Guanajuato and Aguascalientes are leveraging automotive supply-chain expansions for IMMEX compliance consulting. USMCA Annex 16 simplifies work visas, letting U.S. and Canadian specialists fly in for short bursts, a factor that raises competitive pressure on local boutiques. The overall geography pattern shows demand clustering in three metros but gradually radiating toward both the northern border and emerging southern corridors.

Competitive Landscape

The Mexico management consulting services market remains moderately concentrated. Six global integrators, Accenture, Deloitte, PwC, McKinsey, Bain, and BCG, control the bulk of strategy and digital-transformation revenue. Deloitte’s expanded alliance with Amazon Web Services, announced in December 2025, typifies how these firms embed cloud platforms into advisory models to secure multi-year implementation revenue.

Mid-tier players such as BDO, Grant Thornton, and Alvarez and Marsal compete on compliance, restructuring, and mid-market M&A, fields where local knowledge and price agility matter. Grant Thornton Mexico reports USD 42.14 million in revenue, 858 staff, and nine offices, proof that scale is still necessary to win national frameworks. Technology consultancies, IBM, Infosys, HCLTech, Softtek, and NTT DATA, exploit near-shore delivery centers to sell managed services alongside advisory. Softtek alone employs more than 15,000 Mexican professionals, positioning it as a local champion.

Boutiques that specialize in AML/CFT, fintech compliance, or ESG data are emerging as disruptors because they offer pinpoint regulatory depth. NTT DATA’s 2026 AI factory initiative with NVIDIA illustrates the broader arms race for proprietary digital assets that differentiate offerings. Pricing models are slowly shifting toward outcome-based structures, requiring firms to quantify ROI within statements of work and invest in reusable accelerators.

Mexico Management Consulting Services Industry Leaders

Accenture Limited Liability Company

Deloitte Consulting Group Mexico Civil Society

PricewaterhouseCoopers Mexico Civil Society

McKinsey and Company Mexico Limited Liability Company

KPMG Cárdenas Dosal Civil Society

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Holland and Knight released an analysis of Mexico’s updated anti-money-laundering framework, signaling higher demand for AML gap assessments and remediation projects.

- March 2026: Baker McKenzie detailed statutory changes that expanded the definition of vulnerable activities, compelling financial institutions to tighten beneficial-ownership checks.

- March 2026: Deloitte’s Investment Monitor showed only 12% of announced near-shoring factories had gone live, intensifying calls for operational-efficiency consulting.

- December 2025: Accenture’s Macro Foresight Brief flagged electricity constraints in northern plants, steering clients toward hybrid-cloud advisories.

Mexico Management Consulting Services Market Report Scope

The Mexico Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Mexico management consulting services market and where is it headed?

The market stood at USD 3.04 billion in 2026 and is forecast to reach USD 4.39 billion by 2031, expanding at a 7.63% CAGR.

Which consulting service line is growing fastest in Mexico to 2031?

Risk and compliance consulting leads with a projected 7.89% CAGR, driven by tighter AML rules and fintech oversight.

How are small and medium-sized enterprises influencing consulting demand?

SME formalization under stricter labor-registry rules is lifting demand for packaged compliance, accounting, and payroll advisory, supporting a 7.71% CAGR for the segment.

What delivery model trend is shaping consulting engagements in Mexico?

Hybrid models that mix on-site workshops with virtual execution are rising fastest, although on-site work still holds the majority share.

Which industry vertical shows the strongest consulting growth outlook?

Healthcare is set to advance at a 7.83% CAGR as hospitals roll out electronic health records and insurers seek cost-containment solutions.

How will the 2026 USMCA review affect consulting activity?

While tariff uncertainty may temper investment decisions, Annex 16 visa provisions enable U.S. and Canadian consultants to support Mexican projects quickly, sustaining cross-border advisory flows.

Page last updated on: