Europe Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

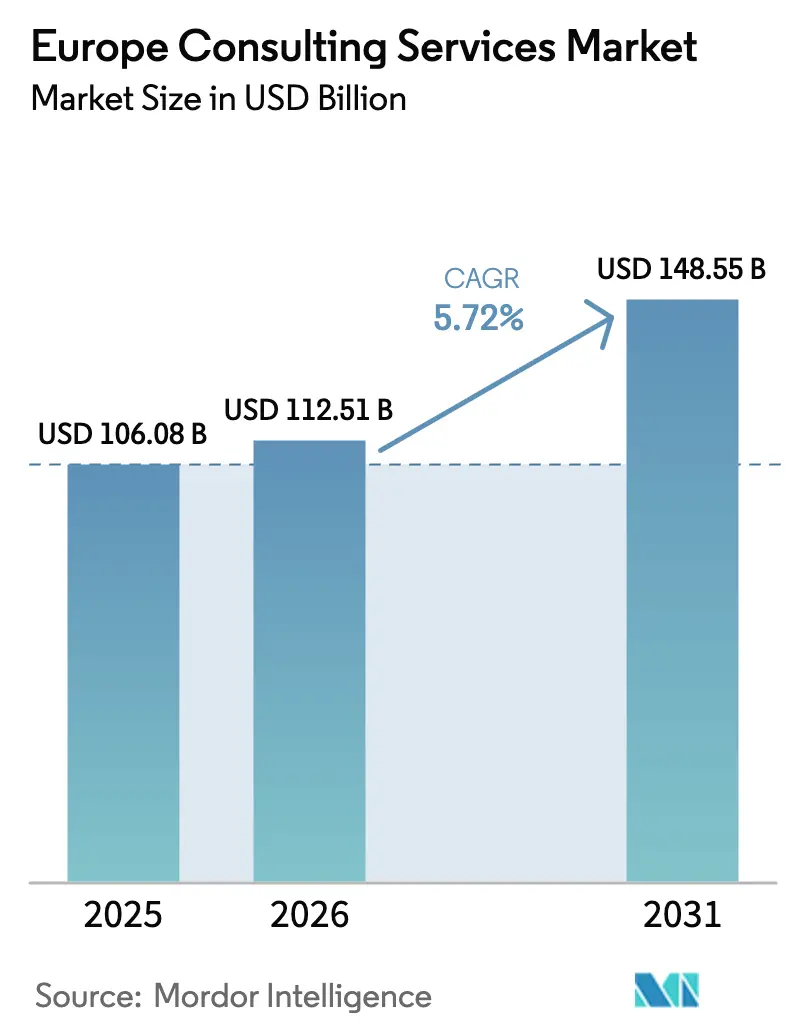

| Base Year Market Size (2025) | USD 106.08 Billion |

| Market Size (2026) | USD 112.51 Billion |

| Market Size (2031) | USD 148.55 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Consulting Services Market Analysis by Mordor Intelligence

The Europe consulting services market size is projected to be USD 106.08 billion in 2025, USD 112.51 billion in 2026, and reach USD 148.55 billion by 2031, growing at a CAGR of 5.71% from 2026 to 2031. The expansion reflects rising advisory spend on Corporate Sustainability Reporting Directive compliance, rapid generative-AI deployment, and Recovery and Resilience Facility-funded digitalization programs. Enterprises are reallocating budgets from discretionary strategy projects toward legally mandated sustainability reporting and technology-enabled productivity gains. Generative-AI adoption is reshaping delivery models, with remote and virtual execution taking share from traditional on-site work. Competitive intensity is escalating as Big Four integrators, strategy houses, and IT-services majors converge on outcome-based, technology-infused engagements.

Key Report Takeaways

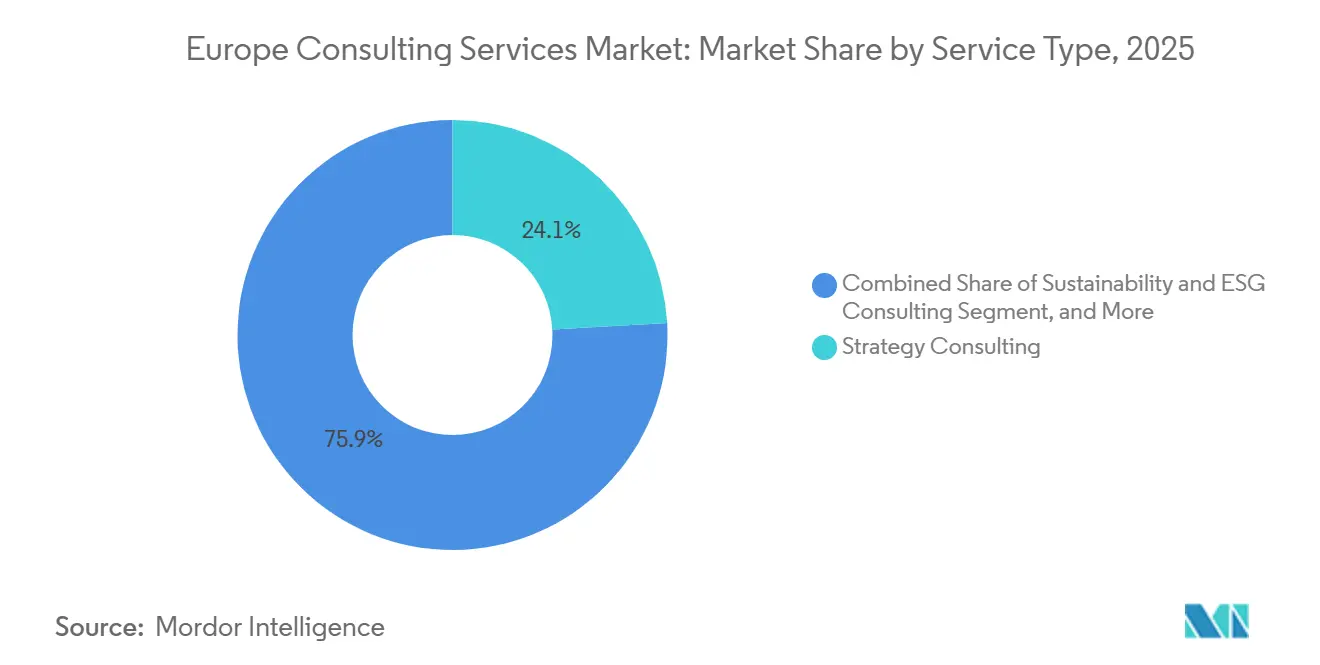

- By service type, strategy consulting held 24.11% revenue share in 2025, while sustainability and ESG consulting is forecast to expand at a 6.81% CAGR through 2031.

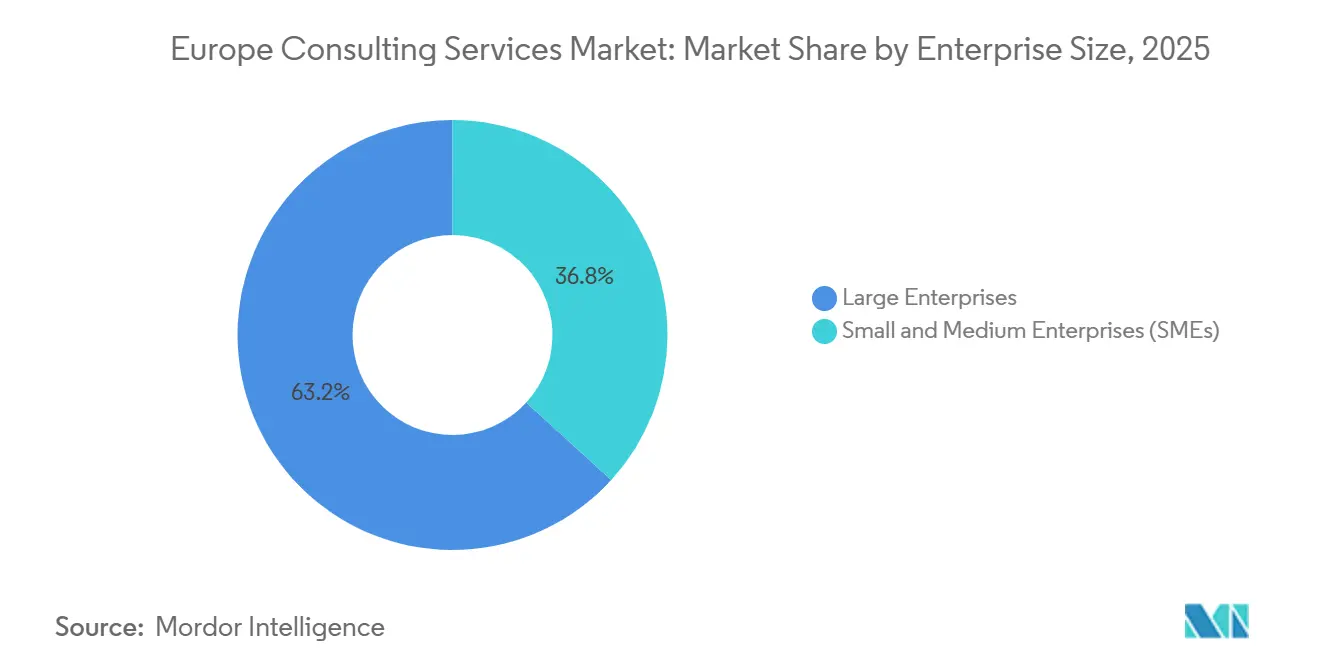

- By enterprise size, large enterprises commanded 63.21% of 2025 spending, whereas SMEs are projected to grow at a 6.23% CAGR through 2031.

- By client industry, BFSI generated 19.87% of 2025 revenue, yet energy and utilities consulting is projected to grow at a 6.58% CAGR through 2031.

- By delivery model, hybrid formats accounted for 49.53% of 2025 engagements, while remote delivery is set to expand at a 6.35% CAGR to 2031.

- By geography, the United Kingdom led with 27.39% share of the Europe consulting services market in 2025; Spain is advancing at the fastest 6.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal and CSRD compliance pressures | +1.20% | EU-wide, strongest in Germany, France, Nordics | Medium term (2-4 years) |

| Accelerated client demand for AI-enabled productivity consulting | +1.00% | Global, concentrated in UK, Germany, Benelux | Short term (≤ 2 years) |

| SME digital-maturity funding via EU RRF grants | +0.90% | Spain, Italy, Central and Eastern Europe | Medium term (2-4 years) |

| Regulatory convergence for cross-border services | +0.70% | EU-wide, particularly Benelux, Nordics | Long term (≥ 4 years) |

| Shift to outcome-based pricing models | +0.50% | UK, Germany, France | Medium term (2-4 years) |

| Near-shoring driven by geopolitical risk in supply chains | +0.40% | Central and Eastern Europe, Spain, Portugal | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Green Deal and CSRD Compliance Pressures

Roughly 50,000 European companies must publish audited sustainability disclosures beginning with fiscal-year 2025 reports, a tenfold increase versus prior regimes.[1]European Commission, “Corporate Sustainability Reporting Directive (CSRD),” finance.ec.europa.eu Advisory demand centers on ESG data platforms, Scope 3 modelling, and assurance readiness, with one large firm citing a 43% year-on-year rise in CSRD-linked work in 2025.[2]Deloitte, “CSRD Corporate Sustainability Reporting Directive: Implementation Guide,” deloitte.com Legal liability now extends to chief financial officers, making ESG a board-level compliance priority rather than a reputational initiative. The directive’s double-materiality principle requires companies to quantify both climate-related financial risk and their environmental footprint, capabilities rarely found in-house. Germany and France moved fastest due to stringent national enforcement, while Southern and Eastern members are scaling more gradually pending final guidance.[3]PwC, “CSRD Implementation Guide for European Enterprises,” pwc.com

Accelerated Client Demand for AI-Enabled Productivity Consulting

Generative-AI adoption in European enterprises climbed from 12% in early 2024 to 38% by December 2025.[4]McKinsey and Company, “The State of AI in 2025: Generative AI's Breakout Year,” mckinsey.com Consulting engagements now span model selection, prompt engineering, and EU AI Act compliance. Firms bundle use-case road-mapping, pilot execution, and workforce reskilling into multi-year programs that increasingly rely on outcome-based pricing; 62% of one integrator’s European AI projects in 2025 carried success-linked fees. The UK and Germany dominate spend thanks to large talent pools and mature cloud infrastructure, while Southern markets accelerate as hyperscale’s localize data centers to satisfy residency rules.

SME Digital-Maturity Funding via EU RRF Grants

Spain and Italy together received more than EUR 261 billion in RRF allocations through 2026, with at least 20% earmarked for digital transition. Programs such as Spain’s Digitalization Kit subsidize up to EUR 12,000 per SME for advisory services. Italy’s Transizione 4.0 tax credits drive similar uptake, especially in northern industrial clusters. Central and Eastern European members deploy grants to modernize public administration and healthcare IT, compressing timelines and favouring consultancies with pre-built accelerators. The funding window closing in 2026 intensifies demand for rapid advisory interventions.

Regulatory Convergence for Cross-Border Services

The EU Services Directive and mutual-recognition schemes are reducing administrative barriers for multi-country consulting delivery. A January 2025 proposal to standardize engagement contracts seeks to lower legal costs for mid-sized firms expanding across borders. Benelux and the Nordics already recognize professional qualifications across borders, enabling seamless project staffing. Harmonization is most valuable for scarce niche skills such as transfer-pricing or clinical-trial design, where clients demand consistent coverage in multiple jurisdictions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent talent deficit in advanced analytics | -0.80% | Germany, UK, Nordics | Medium term (2-4 years) |

| Fee-compression from procurement-led negotiations | -0.60% | UK, France, Germany | Short term (≤ 2 years) |

| Generative-AI DIY toolkits reducing entry-level work | -0.40% | Global, most acute in UK, Benelux | Short term (≤ 2 years) |

| Regulatory scrutiny on large integrator-consultant MandA | -0.30% | EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Talent Deficit in Advanced Analytics

Germany reported 124,000 unfilled IT and data-analytics roles in December 2025, 17% higher than the prior year. Scarcity inflates salaries, squeezes project margins, and drives firms to acquire boutiques or open near-shore hubs. UK immigration caps further restrict non-EU data-scientist inflow, prompting London practices to shift delivery to Dublin and Warsaw. Nordic universities produce fewer computer-science graduates than local demand, exacerbating the deficit despite liberal visa rules. Regulated clients often insist on onshore teams, limiting off shoring as a mitigation lever.

Fee-Compression from Procurement-Led Negotiations

European corporates centralized consulting spend under category-management frameworks that cut average day rates 15–25% since 2023. Procurement now co-approves engagements above EUR 500,000 and benchmarks proposals against offshore or internal alternatives. Outcome-based pricing shifts delivery risk onto consultancies and demands upfront investment in proprietary tools, challenging mid-sized firms. Generative-AI research assistants further erode willingness to pay for junior labour, pressuring firms to reposition toward high-value C-suite advisory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Sustainability Consulting Outpaces Traditional Lines

Strategy consulting generated the largest 24.11% share of Europe consulting services market revenue in 2025. Sustainability and ESG projects, however, are forecast to post the highest 6.81% CAGR, propelled by CSRD deadlines and board-level climate-risk oversight. Digital transformation engagements capture adjacent demand as clients embed ESG metrics into ERP and customer dashboards. Operations consulting remains resilient due to cost-containment and supply-chain volatility. Financial advisory benefits from brisk renewable-energy and healthcare deal flow, while technology and cybersecurity advisory converge under the stricter NIS2 regime.

Sustainability’s momentum is shifting wallet share. Firms with verified CSRD methodologies and Scope 3 accounting accelerators are winning multi-year retainers. The Europe consulting services market size linked to ESG assurance is projected to grow faster than any other sub-line through 2031. Meanwhile, outcome-based pricing gains traction in operations and digital transformation, though strategy and financial advisory engagements largely remain time and materials due to intangible value creation. HR and change-management practices pivot toward AI-enabled workforce planning, integrating generative-AI training in more than half of 2025 engagements.

By Client Industry: Energy Transition Fuels Utilities Consulting

BFSI contributed 19.87% of 2025 fees, anchored by Basel IV and Digital Operational Resilience Act compliance programs. Energy and utilities engagements are expected to log the fastest 6.58% CAGR, reflecting grid-modernization mandates under REPowerEU. Manufacturing clients sustain robust spend on Industry 4.0 and circular-economy transitions, while healthcare consulting expands alongside record drug approvals in 2025.

Utilities projects increasingly bundle strategy, technology road-mapping, and predictive-maintenance analytics, lifting the Europe consulting services market size attached to the sector. Consumer and retail demand rebounds, centering on omnichannel integration and sustainability labelling. Public-sector engagements grow as governments deploy RRF funds for digital services, and transportation client’s partner on decarbonization roadmaps aligned with Fit for 55 CO₂ standards.

By Enterprise Size: SMEs Accelerate Advisory Adoption

Large companies captured 63.21% of spending in 2025, yet SMEs are forecast to post the brisker 6.23% CAGR. Grant-backed programs such as Spain’s Digitalization Kit reduce advisory entry costs, expanding the Europe consulting services market share of SME engagements. Standardized accelerators and modular pricing help large consultancies penetrate mid-market demand, while boutiques leverage local language and sector specialization.

Remote delivery lowers travel costs, making it economical to serve SMEs in peripheral regions. The Europe consulting services market size for SME advisory is poised to expand as contract harmonization proposals reduce legal complexity across member states. Large enterprises will continue to dominate capital-intensive ERP and post-merger programs, though procurement pressure compresses margins and forces firms to differentiate through proprietary analytics and co-investment models.

By Delivery Model: Hybrid Dominates, Remote Gains Ground

Hybrid formats held 49.53% of 2025 engagements, balancing on-site relationship building with virtual execution efficiencies. Remote delivery, the fastest-growing model at a 6.35% CAGR, benefits from mature collaboration platforms and client cost discipline. The Europe consulting services market size associated with fully remote work is expanding as engagements deploy specialized talent across borders without visa hurdles.

On-site presence remains essential for high-stakes integration and change-management programs but increasingly follows an immersion-week cadence rather than continuous residency. Remote delivery also supports advisory access for SMEs and niche projects in regulated verticals. Proposed EU guidance on cross-border remote-work taxation could further accelerate adoption by easing compliance burdens.

Geography Analysis

The United Kingdom accounted for 27.39% of 2025 revenue, sustained by London’s concentration of global headquarters and deep capital markets. Germany and France jointly represent roughly 35% of spend, driven by large industrial bases and complex regulatory landscapes. Benelux nations punch above their economic weight owing to dense SME populations and advanced digital infrastructure.

Spain is projected to record the quickest 6.31% CAGR through 2031 as EUR 69.5 billion in RRF grants fund digital and green transitions. Italy follows a similar trajectory propelled by Transizione 4.0 incentives targeting northern industrial clusters. Nordic countries exhibit high consulting intensity per capita, underpinned by early adoption of sustainability reporting and leading AI uptake.

Central and Eastern Europe gains traction as a near-shoring hub for manufacturing and shared services, bolstering demand for supply-chain and cybersecurity advisory. Ireland benefits from its role as a European base for technology and pharmaceutical multinationals, while Portugal and Greece see project activity tied to tourism modernization and smart-manufacturing investments. The Baltics exploit their e-government pedigree to attract fintech and cybersecurity consulting, reinforcing geographic diversity across the Europe consulting services market.

Competitive Landscape

The market remains moderately concentrated; the Big Four collectively hold roughly 35–40% revenue but none exceeds 12% individually. Deloitte, PwC, EY, and KPMG leverage multidisciplinary footprints and audit relationships to win large transformation mandates. Strategy houses McKinsey, BCG, and Bain dominate C-suite advisory, commanding premium rates yet increasingly compete with IT-services majors such as Accenture, Capgemini, IBM Consulting, Infosys, TCS, and Wipro, which bundle advisory with implementation and managed services.

Mid-sized European firms including Roland Berger, BearingPoint, and PA Consulting differentiate through industry specialization and local delivery agility. White-space opportunities in sustainability and generative-AI consulting allow boutiques with deep domain skill to command premium pricing and attract acquisition bids.

Antitrust thresholds introduced in January 2025 slow mega-deals but create room for sub-EUR 500 million tuck-ins, reshaping the competitive chessboard. Technology capability is emerging as the decisive differentiator, with leading firms deploying proprietary analytics platforms, AI assistants, and self-service client portals that raise switching costs.

Europe Consulting Services Industry Leaders

Deloitte Touche Tohmatsu Limited

Ernst & Young Global Limited

KPMG International

PricewaterhouseCoopers LLP

McKinsey & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: European Investment Fund mobilised EUR 2.5 billion for Spanish SME innovation, sustainability, and digitalization financing, benefiting more than 6,000 businesses.

- April 2025: Bridgepoint took a minority stake in Argon & Co, valuing the global operations-strategy consultancy in a market worth EUR 4.4 billion and growing 7% annually.

- April 2025: CGI agreed to acquire Apside, adding 2,500 engineers across France, Canada, and Switzerland.

- March 2025: Deloitte launched Zora AI and EY released 150 tax-compliance agents, advancing service-as-software delivery models.

- January 2025: A.T. Kearney acquired Project Partners Management GmbH to strengthen SAP S/4HANA transformation capacity in the DACH region.

- November 2024: Visionet Systems bought Rödl Dynamics to expand Microsoft Dynamics consulting across German-speaking markets.

Europe Consulting Services Market Report Scope

The Europe Consulting Services Market Report is Segmented by Service Type (Operations, Strategy, Financial Advisory, Technology Advisory, HR and Change Management, Sustainability and ESG, Digital Transformation), Client Industry (BFSI, Manufacturing, Healthcare, Energy, ICT, Consumer, Rest), Enterprise Size (Large, SMEs), Delivery Model (On-site, Remote, Hybrid), and Geography (UK, Germany, France, Benelux, Italy, Nordics, Spain, CEE, Rest). Market Forecasts are Provided in Value (USD).

| Operations Consulting |

| Strategy Consulting |

| Financial Advisory |

| Technology Advisory |

| HR and Change Management |

| Sustainability and ESG Consulting |

| Digital Transformation Consulting |

| BFSI |

| Manufacturing and Industrials |

| Healthcare and Life Sciences |

| Energy and Utilities |

| ICT and Media |

| Consumer and Retail |

| Rest of Client Industries |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| On-site Engagement |

| Remote/Virtual |

| Hybrid Model |

| United Kingdom |

| Germany |

| France |

| Benelux |

| Italy |

| Nordics |

| Spain |

| Central and Eastern Europe (incl. Poland) |

| Rest of Europe |

| By Service Type | Operations Consulting |

| Strategy Consulting | |

| Financial Advisory | |

| Technology Advisory | |

| HR and Change Management | |

| Sustainability and ESG Consulting | |

| Digital Transformation Consulting | |

| By Client Industry | BFSI |

| Manufacturing and Industrials | |

| Healthcare and Life Sciences | |

| Energy and Utilities | |

| ICT and Media | |

| Consumer and Retail | |

| Rest of Client Industries | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Delivery Model | On-site Engagement |

| Remote/Virtual | |

| Hybrid Model | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Benelux | |

| Italy | |

| Nordics | |

| Spain | |

| Central and Eastern Europe (incl. Poland) | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe consulting services market in 2026 and what is its growth rate?

It stands at USD 112.51 billion in 2026 and is projected to grow at a 5.71% CAGR through 2031.

Which service line is expanding the fastest?

Sustainability and ESG consulting is forecast to post the highest 6.81% CAGR as CSRD compliance deadlines approach.

Which client industry shows the strongest growth potential?

Energy and utilities consulting is projected to expand at a 6.58% CAGR, reflecting grid-modernization and energy-transition investments.

What delivery model is gaining share most rapidly?

Remote and virtual delivery is growing at a 6.35% CAGR as clients seek cost efficiency and talent flexibility.

How are SMEs influencing market dynamics?

SME advisory spend is rising at a 6.23% CAGR, fueled by EU grants that subsidize digitalization and sustainability consulting.

What factors are putting pressure on consulting fees?

Centralized procurement negotiations and the availability of generative-AI research tools are compressing day rates by 1525%.

Page last updated on: