Spain Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

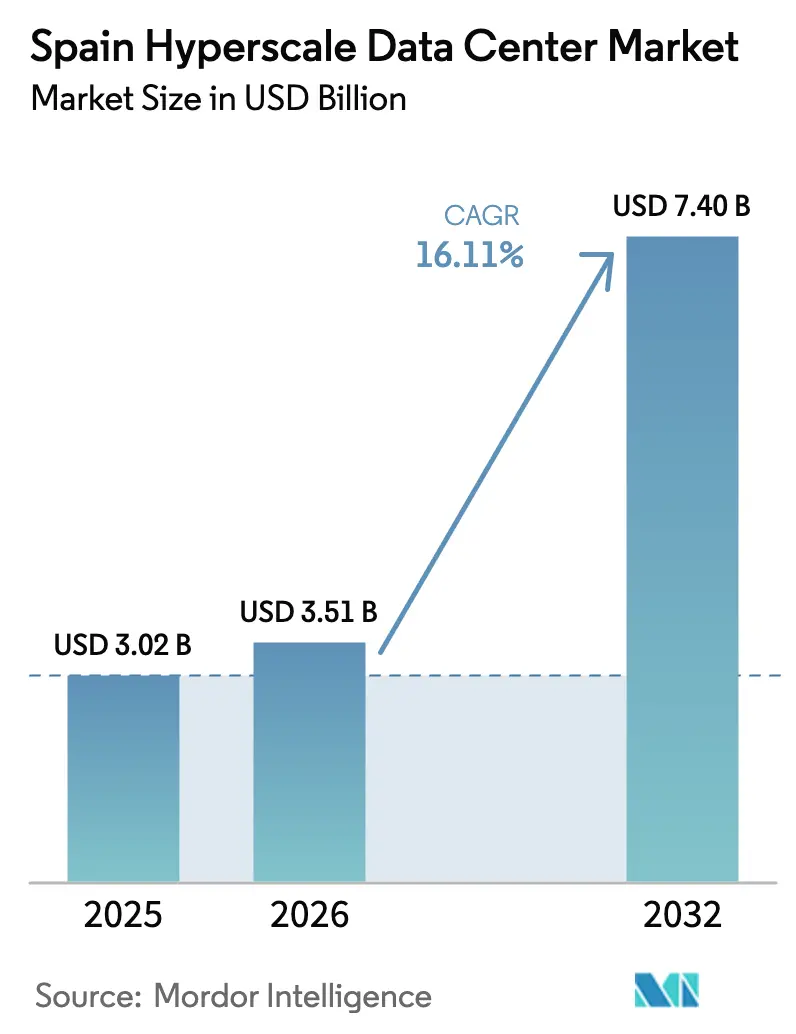

| Base Year Market Size (2025) | USD 3.02 Billion |

| Market Size (2026) | USD 3.51 Billion |

| Market Size (2032) | USD 7.4 Billion |

| Growth Rate (2026 - 2032) | 16.11% CAGR |

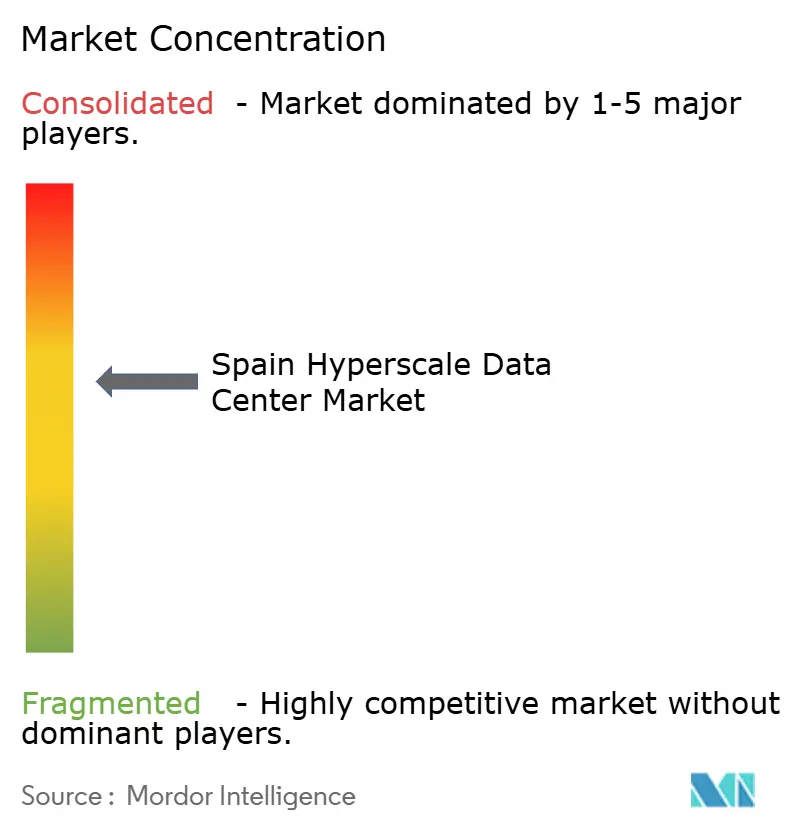

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Hyperscale Data Center Market Analysis by Mordor Intelligence

Spain hyperscale data center market size in 2026 is estimated at USD 3.51 billion, growing from 2025 value of USD 3.02 billion with 2031 projections showing USD 7.4 billion, growing at 16.11% CAGR over 2026-2031. Capacity additions from 1.316 thousand MW to 2.197 thousand MW indicate that infrastructure density is improving in parallel with monetary growth. Sovereign-region launches by Amazon Web Services (AWS), Microsoft, Google and Meta are redirecting deployments from traditional FLAP hubs to Spain, helped by abundant renewable-energy resources, multiple new trans-Atlantic cables, and a permitting framework that favors large-scale campuses. The Spain hyperscale data center market is further supported by corporate power-purchase agreements (PPAs) that lock in renewable supply, while immersion and direct-liquid cooling adoption reduce energy and water demand. Competitive intensity is rising as CoreWeave, Oracle and domestic players such as Nabiax join established colocation specialists, creating price pressure but also stimulating innovation in energy management and modular construction. Infrastructure bottlenecks around grid interconnection in Madrid, plus skilled-labor shortages in high-voltage maintenance, remain the principal operational obstacles.

Key Report Takeaways

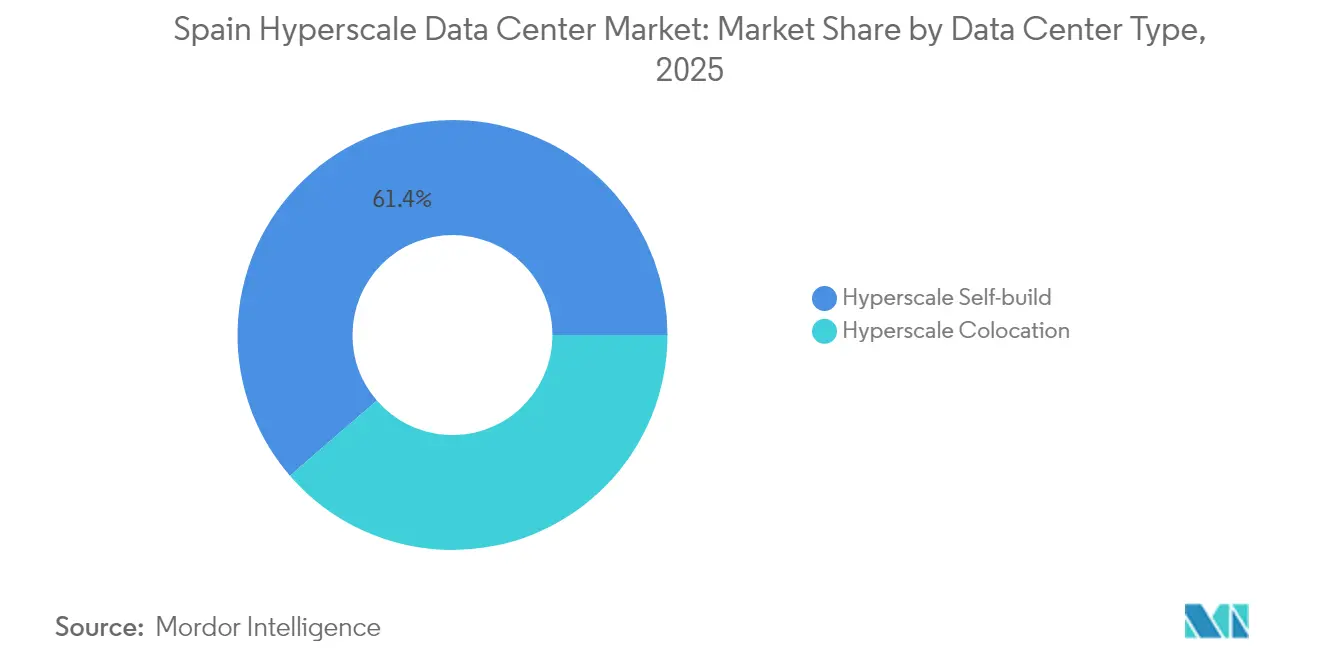

- By data center type, self-build facilities held 61.35% of Spain hyperscale data center market share in 2025 while colocation posted the highest projected 22.95% CAGR through 2031.

- By component, IT infrastructure accounted for 35.20% of Spain hyperscale data center market size in 2025; liquid-cooling systems are forecast to grow at a 28.4% CAGR to 2031.

- By tier standard, Tier III deployments captured 72.20% of Spain hyperscale data center market size in 2025, whereas Tier IV is set to expand at an 17.6% CAGR.

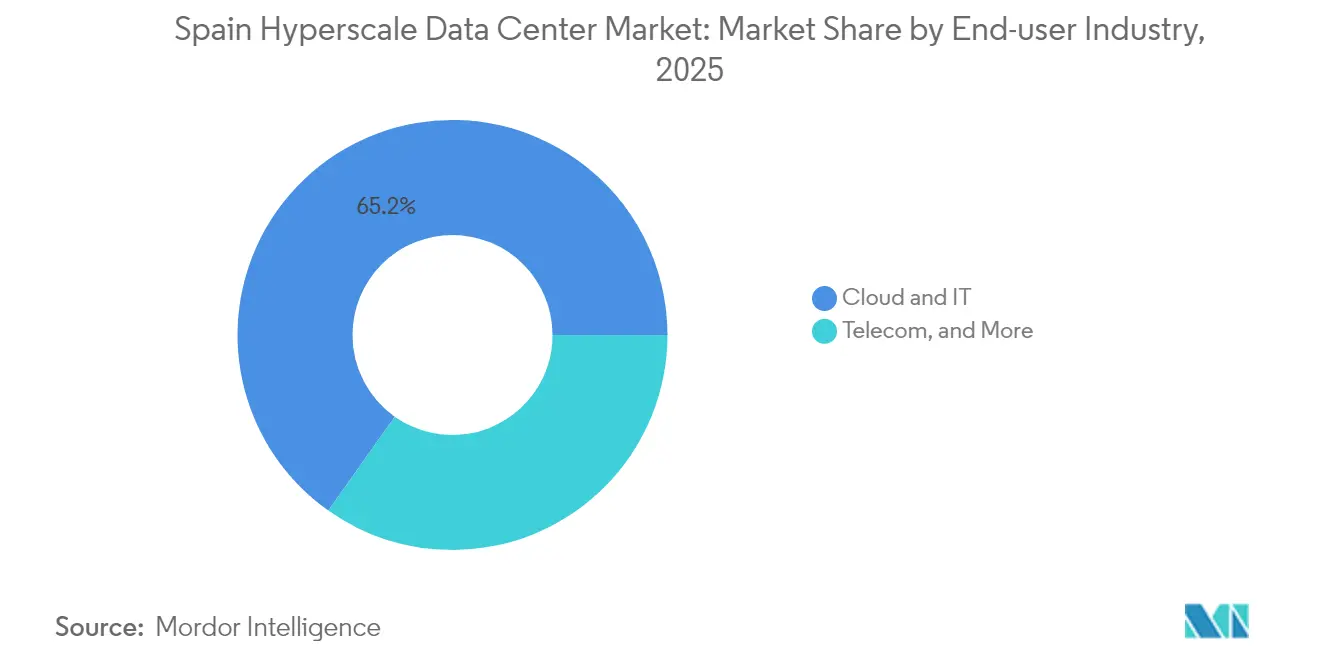

- By end-user industry, cloud and IT services contributed 65.20% of Spain hyperscale data center market size in 2025 and will accelerate at a 23.35% CAGR through 2031.

- By data center size, massive (greater than 25 MW and less than equal to 60 MW) sites controlled 40.40% of Spain hyperscale data center market share in 2025, while mega (greater than 60 MW) facilities will rise at a 20.9% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple countries and regions, with Spain contributing to the overall trajectory. The outlook on worldwide hyperscale data center market reflects how these are expected to evolve collectively.

Spain Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscaler region launches | +4.20% | Global, concentrated in Madrid and Aragon | Medium term (2-4 years) |

| Sub-sea cable spurs | +2.80% | Coastal regions, primarily Barcelona and Santander | Long term (≥ 4 years) |

| Renewable-PPA boom (solar + wind hybrids) | +3.50% | National, strongest in Aragon and Extremadura | Medium term (2-4 years) |

| Digital-sovereignty and Schrems-II compliance | +2.10% | EU-wide, concentrated in major metros | Short term (≤ 2 years) |

| Gen-AI inference nodes needing liquid-cooled edge | +3.80% | Major metros, expanding to secondary cities | Short term (≤ 2 years) |

| SMR-based micro-grid pilots for DCs | +1.40% | National, pilot regions in Extremadura | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Hyperscaler Region Launches

AWS committed EUR 15.7 billion (USD 18.37 billion) to five proprietary sites in Aragon, creating Spain’s first hyperscale cloud region outside the FLAP corridor [1].About Amazon Team, “AWS plans to invest €15.7 billion in Spain, supporting 17,500 jobs annually,” About Amazon, aboutamazon.eu Microsoft has followed with multibillion-euro campuses in Madrid and Zaragoza, confirming the country’s pull factors of land availability, renewable-energy head-room and submarine-cable proximity. These announcements create a rapid demand signal for local supply chains, ranging from HV-switchgear to specialist engineering, and accelerate capacity build-out schedules from the typical 36 months to nearer 24 months. Sovereign-region branding also reassures EU enterprises that latency and data-residency requirements are met, thereby shifting SaaS and PaaS workloads to the Spain hyperscale data center market. The clustering effect around Zaragoza is expected to transform regional logistics and construction industries, providing a template for other secondary Spanish metros to attract future builds.

Renewable-PPA Boom (Solar + Wind Hybrids)

Spain generated 60% of its electricity from renewables in 2024, and grid operator Redeia earmarked EUR 3.9 billion for transmission upgrades to unlock additional green capacity [2].Redeia, “Results Presentation First Half 2024,” redeia.com Hyperscalers are signing 10- to 15-year PPAs, fixing both power costs and carbon intensity. Samca Group’s vertically-integrated model couples seven wind farms with three data-center campuses, achieving 60% self-sufficiency while supporting 2,300 construction jobs SAMCA.ES. PPAs also allow operators to offer grid-balancing services, monetizing flexible load during peak renewable curtailments that hit 1.08 TWh in 2022. Regulatory preference for regions with high renewable penetration pushes new projects toward Aragon and Extremadura, further decentralizing the Spain hyperscale data center market away from the saturated Madrid grid.

Gen-AI Inference Nodes Needing Liquid-Cooled Edge

High-density GPU racks now exceed 100 kW, far beyond legacy CRAH limits. Submer’s latest immersion tank cuts facility energy use by 70% and captured USD 55 million in growth funding in 2024. Telefónica deployed Submer technology in Madrid, recording rack-level PUE below 1.10 and eliminating evaporative cooling water demand. CoreWeave’s 39 MW Barcelona campus is sized for AI inference loads and mandates liquid cooling from day one. These deployments showcase a path to sustain Spain’s renewables-heavy power mix while meeting thermal needs, strengthening the country’s attractiveness for AI-first hyperscale clusters.

Digital-Sovereignty and Schrems-II Compliance

After the Schrems-II ruling, EU regulators require customer-controlled encryption keys and local data processing. VMware’s sovereign-cloud reference architecture underpins new Spanish offerings that guarantee no cross-border data movement. Cisco now hosts observability telemetry solely inside the EU, giving clients residency assurances. Local operators gain an advantage by certifying their supply chains and facility management under ISO 27001 and ENS High standards. These controls are turning compliance into a sourcing criterion that shifts enterprise and public-sector workloads into the Spain hyperscale data center market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion and energy-price volatility | -2.40% | Madrid metro, expanding to Barcelona | Short term (≤ 2 years) |

| Skilled-talent shortage in HV-M and E O and M | -1.80% | National, acute in technical roles | Medium term (2-4 years) |

| Water-stress caps on evaporative cooling | -1.60% | Aragon, Andalusia, central regions | Medium term (2-4 years) |

| GPU/optic allocation bias toward Tier-1 FLAP cities | -1.20% | Secondary Spanish metros | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid Congestion and Energy-Price Volatility

Redundant-capacity requests in Madrid already exceed available substations, forcing new entrants to queue for up to three years for grid connection. Redeia’s 400 kV Valdemoro corridor upgrade is scheduled no earlier than 2027, leaving operators to secure interim on-site generation at volatile spot-market prices. Renewable output curtailments spike wholesale prices in evening peaks, complicating PPA modeling and pushing some hyperscalers toward Aragon or Catalonia where grid head-room is higher. The resulting regional re-balancing could temper headline growth rates for the Madrid cluster within the Spain hyperscale data center market.

Skilled-Talent Shortage in HV-M and E Operations

Industry surveys find Spain will require 2,000 additional certified engineers by 2026 to operate new data centers safely [3].Computerworld España, “España necesitará 2.000 nuevos profesionales…,” computerworld.es High-voltage and mission-critical mechanical roles command 25% wage premiums versus pre-2024 levels, raising opex for smaller colocation providers. Universities have begun offering dedicated data-center engineering tracks, yet the average graduate-to-competent-operator timeline remains four years. International recruitment is constrained by language skills and visa quotas, prompting hyperscalers to fund in-house academies and joint apprenticeships with OEMs. Until the pipeline matures, manpower scarcity will cap the rollout speed of new capacity in the Spain hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Madrid opened 2025 with 56.55% of installed capacity, underpinned by the DE-CIX Iberian Internet Exchange and a dense enterprise customer base. Despite grid congestion, the region’s pipeline still exceeds 400 MW, aided by a one-stop-shop permitting office. To mitigate power bottlenecks, operators deploy on-site solar-plus-battery micro-grids and contract rotating-reserve from adjacent provinces.

Aragon is the breakout star with a 19.25% compound growth trajectory through 2031. Abundant wind potential, land priced 40% below Madrid’s outskirts and fast-track environmental clearance fuel unprecedented investment from AWS, Microsoft and Blackstone. Government incentives include rebate-linked job-creation thresholds and property-tax abatements. These factors give Aragon the lowest delivered-power cost among Spain’s data-center provinces, drawing AI-centric tenants and reinforcing the Spain hyperscale data center market’s decentralization.

Catalonia advances as the Mediterranean connectivity node where the EllaLink, Medusa and future submarine systems converge. AQ Compute’s 60 MW Barcelona build and CoreWeave’s AI cluster validate the region’s edge-to-Africa positioning. Sub-regions like Andalusia and the Basque Country court developers with brownfield industrial parks, yet limited transformer availability and longer fiber backhaul times slow adoption. Overall, geographic diversification spreads risk, taps renewable zones and positions Spain as the EU’s southern digital gateway.

Analysis of the hyperscale data center market by Mordor Intelligence spans multiple other regional evaluations across Europe, North America, and Middle East, supported by country-level insights for France, Norway, United States, Saudi Arabia, Poland, and Australia, wherein local market conditions keep varying from one country to another.

Segment Analysis

By Data Center Type: Self-Build Dominance Drives Control

Self-build projects represented 61.35% of Spain hyperscale data center market share in 2025. AWS’s Aragon campus alone adds five proprietary halls tailored to its networking fabric and security stack. Hyperscalers favor direct ownership to guarantee design repeatability, integrate on-site solar PPAs and deploy experimental cooling. Colocation, although smaller today, is expanding at a 22.95% CAGR as Equinix and Digital Realty construct xScale halls offering 4-10 MW suites that appeal to AI start-ups needing burst capacity. The Spain hyperscale data center market size for colocation is therefore on a steep upward trajectory driven by flexible contract demand.

Colocation providers respond by adopting build-to-suit wings, offering customers dedicated meet-me rooms and guaranteed liquid-cooling readiness. Strategic joint ventures with pension funds lower cost of capital, letting operators compress wholesale pricing while preserving EBITDA margins. Over time, the two models are converging: hyperscalers lease entire buildings from colocation REITs under long leases, while REITs market their sites as near-self-build options. This symbiosis ensures both segments grow, but ownership economics remain skewed toward hyperscaler balance sheets within the Spain hyperscale data center market.

By Component: IT Infrastructure Leads Amid Cooling Revolution

IT infrastructure captured 35.20% of Spain hyperscale data center market size in 2025 as GPU clusters, NVMe storage and 400 Gbps switching dominated capex. Liquid-cooling systems, though a smaller base, will race ahead at 28.4% CAGR thanks to Submer’s immersion tanks and direct-chip cold-plate designs. Electrical infrastructure is evolving toward grid-interactive UPS that can export 10-15 MW during frequency events, generating ancillary-service income. Mechanical racks now ship pre-equipped with rear-door heat exchangers, cutting integration lead times by 30%. General-construction contractors have adopted modular skids that arrive factory-tested, shaving eight weeks off build schedules. These shifts align Spain’s supply chain with next-generation AI workload demands and reinforce its position as a continental sustainability benchmark.

The Spain hyperscale data center market is consequently pivoting toward capex that prioritizes performance-per-watt and deployment velocity over raw square-meter counts. Vendors highlight LCA-verified materials, while operators benchmark embodied carbon in concrete and steel. The component mix will continue to tilt toward high-density compute and advanced cooling, shrinking the mechanical-to-IT spend ratio even as total spend accelerates.

By Tier Standard: Tier III Stability Meets Tier IV Growth

Tier III campuses represented 72.20% of Spain hyperscale data center market size in 2025 because cloud architectures achieve application-level redundancy across multiple sites rather than within a single hall. Operators therefore favor N+1 electrical paths and concurrently maintainable cooling that satisfy most SLA targets without the capital burden of 2N systems. Tier IV, although only a minority today, is expanding at an 17.6% CAGR as financial-services, healthcare and critical national workloads migrate to domestic sovereign clouds.

High-revenue AI training clusters also justify Tier IV designs, since an outage during a week-long model run can wipe out millions in GPU utilization. As a result, Spain hyperscale data center market share for Tier IV will reach double-digit weight by 2031. Nevertheless, Tier III will remain the baseline for most hyperscaler footprints, sustaining a dual-tier landscape that satisfies divergent risk tolerances.

By End-User Industry: Cloud Dominance Accelerates AI Transformation

Cloud and IT services contributed 65.20% of Spain hyperscale data center market size in 2025 and are forecast to grow fastest at 23.35% CAGR. AWS targets AI-optimized EC2 instances in Aragon, while Microsoft positions its Zaragoza region for Azure OpenAI use-cases. Telecom operators leverage 5G network-function virtualization inside carrier-neutral sites; Telefónica’s Cloud Garden platform already on-boards more than 8,000 business customers. BFSI workloads demand sovereign storage, driving interest in Tier IV colocation with hardware root-of-trust.

Manufacturing and e-commerce trails are smaller but rising as Industry 4.0 and omnichannel retail push real-time analytics to the edge. Government digital services, including tax and health portals, favor domestic hosting to meet compliance thresholds. Together, these verticals diversify revenue streams and insulate the Spain hyperscale data center industry from single-sector shocks.

By Data Center Size: Massive Facilities Dominate Current Deployments

Massive (25-60 MW) sites secured 40.40% of Spain hyperscale data center market share in 2025 because they balance economies of scale with permitting agility. Microsoft’s Zaragoza build falls squarely in this bracket, offering phased expansion modules of 10 MW each. Mega-facilities will, however, post the strongest 20.9% CAGR as AI training clusters benefit from single-campus low-latency fabrics. Blackstone’s 300 MW Project Rodes epitomizes this shift toward giga-scale campuses that rival the largest Fremont or Ashburn complexes.

Large (Less than equal to 25 MW) sites footprints remain relevant for edge nodes and latency-sensitive gaming or streaming content but will lose market percentage as tenants consolidate into hyperscale parks. Regulatory heat-reuse mandates could bolster smaller urban sites that feed district-heating networks, yet their contribution to Spain hyperscale data center market size will taper relative to mega builds.

Competitive Landscape

The Spain hyperscale data center market shows moderate concentration, anchored by AWS, Microsoft and Google whose self-build campuses embed proprietary network fabrics and security pipelines. Their vertical integration assures predictable unit economics and accelerates innovation cycles; AWS, for example, incorporates on-site hydrogen fuel-cell pilots for backup generation.

Equinix, Digital Realty and Data4 compete via neutrality and early access to new submarine-cable landing hubs. They court enterprise tenants requiring multi-cloud connectivity, while also signing multi-megawatt leases to hyperscalers that prefer asset-light capacity during rapid demand spikes. The REIT model lets them amortize capex over 20-year depreciation schedules, delivering attractive AFFO yields.

Specialist challengers exploit technology niches: CoreWeave markets GPU-optimized bare-metal nodes, signing take-or-pay deals with AI start-ups; Submer licenses immersion tanks to legacy halls upgrading beyond 30 kW per rack. Spanish construction conglomerates ACS and Acciona enter via design-build-operate contracts bundled with renewable PPAs, bringing balance-sheet heft that could upend traditional REIT dominance. These trends ensure healthy rivalry and sustained innovation across the Spain hyperscale data center market.

Spain Hyperscale Data Center Industry Leaders

Meta Platforms, Inc.

Amazon Web Services, Inc.

Microsoft Corporation (Azure)

QTS Realty Trust, LLC

Digital Realty (Interxion)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: VDR Group unveiled a 300 MW campus outside Pamplona with projected USD 4.1 billion capex and 2029 completion.

- May 2025: CoreWeave and MERLIN Properties opened a 39 MW Barcelona facility that anchors CoreWeave’s European headquarters.

- April 2025: ACS Group confirmed its first Aragon hyperscale project, marking construction majors’ entry into data-center operations.

- March 2025: AWS requested additional municipal water allocation to support expanded liquid-cooling loops at its Aragon campus.

- July 2024: AQ Compute began construction of its second 60 MW Barcelona hall with 100% renewable supply.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Spain's hyperscale data center market as the revenue generated from newly built, large-footprint facilities (>=4 MW of contiguous IT load) that are owned or leased by cloud service providers or internet companies to support scalable compute and storage workloads. Power, cooling, racks, network fabric, and on-site construction services tied to these facilities are fully counted in value terms.

Scope exclusion: Small enterprise on-premise rooms below 4 MW and pure colocation suites that do not meet hyperscale density thresholds are outside the remit.

Segmentation Overview

- By Data Center Type

- Hyperscale self-build

- Hyperscale colocation

- By Component

- IT Infrastructure

- Server Infratsructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Unit

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction and Services

- Core and Shell Development

- Installation and Commissioning

- Design Engineering

- Fire, Security and Safety Systems

- DCIM / BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-user Industry

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-commerce

- Other End Users

- By Data Center Size

- Large (Less than equal to 25 MW)

- Massive (Greater than 25 MW and less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Primary Research

Interviews were conducted with data center design engineers, power utilities, cloud procurement managers, and facility integrators across Madrid, Barcelona, and Zaragoza. These discussions clarified average selling price per deployed MW, realistic ramp-up curves, and grid-connection lead times, thereby filling gaps left by public disclosures.

Desk Research

Mordor analysts began with structured pulls from national statistics portals such as INE for fiber and power price baselines, Spain DC association white papers for installed IT load, and Red Electrica de Espana for renewable capacity additions. Trade filings and investor decks from global cloud operators, together with construction permits logged in Madrid and Aragon registries, provided deal sizes and commissioning timelines. Paid databases like D&B Hoovers, Dow Jones Factiva, and Questel helped triangulate company capex, news flow, and patent intensity around liquid-cooling. The sources cited above illustrate our desktop foundation; many more inputs informed subsequent validation.

Market-Sizing & Forecasting

A top-down and bottom-up blend underpins the model. National hyperscale demand was first reconstructed from announced capacity pipelines, commissioning schedules, and historical utilization to build a 2019-2024 installed base. Supplier roll-ups of switchgear, UPS, and high-density racks supplied selective bottoms-up checks. Key variables like average EUR / kWh for wholesale power, hyperscaler capex per MW, cloud IaaS revenue in Spain, submarine cable landings, and renewable share in electricity mix drive annual value and volume projections. Forecasts through 2031 apply multivariate regression with scenario analysis, correlating capacity uptake to GDP digital-services elasticity and power-cost trajectories. Where partial data existed (e.g. privately financed self-build sites), regional averages from primary interviews bridged gaps.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance tests against third-party load trackers, and anomaly checks on ASP drift. The model refreshes yearly, with interim updates triggered by material events such as multi-gigawatt campus approvals or tariff revisions. A last-minute validation sweep ensures clients receive the latest numbers.

Why Our Spain Hyperscale Data Center Baseline Commands Reliability

Published estimates vary because firms choose different service scopes, deployment cut-offs, and currency conversions.

Key gap drivers include: some publishers narrow their lens to cloud-delivered services, excluding self-build megacampuses; others aggregate every data center form factor, inflating totals; refresh cadences differ, so recent multi-billion-EUR investments may be missing. Mordor's disciplined scope, annual refresh, and double-sourced variables position our USD 3.02 billion 2025 baseline as the dependable midpoint for strategic planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.02 bn (2025) | Mordor Intelligence | |

| USD 0.43 bn (2024) | Regional Consultancy A | Counts only cloud service revenue, excludes self-build construction spend and power infrastructure |

| USD 6.48 bn (2024) | Global Consultancy B | Combines hyperscale, enterprise, and edge facilities; applies uniform ASP without adjusting for Spain's lower power pricing |

In sum, while external figures swing widely, Mordor's model anchors on clear facility thresholds, Spain-specific cost structures, and time-stamped capacity pipelines, giving decision-makers a transparent, reproducible baseline.

Key Questions Answered in the Report

What is the current Spain hyperscale data center market size?

The market was valued at USD 3.51 billion in 2026 and is forecast to reach USD 7.4 billion by 2031.

Which segment holds the largest Spain hyperscale data center market share?

Self-build hyperscale campuses lead with 61.35% share, reflecting cloud providers’ preference for owning critical infrastructure.

How are cooling technologies evolving in the Spain hyperscale data center industry?

Operators are shifting from air to immersion and direct-liquid cooling, cutting energy use by up to 70% and enabling 100 kW-plus rack densities.

What are the main restraints on market growth?

Madrid grid congestion and a national shortage of certified high-voltage engineers are the two most significant hurdles, reducing projected CAGR by a combined 4.2%.

How concentrated is the competitive landscape?

The top five players hold slightly more than 60% of capacity, giving the market a concentration score of 6 on a 10-point scale.

Page last updated on: