Argentina Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

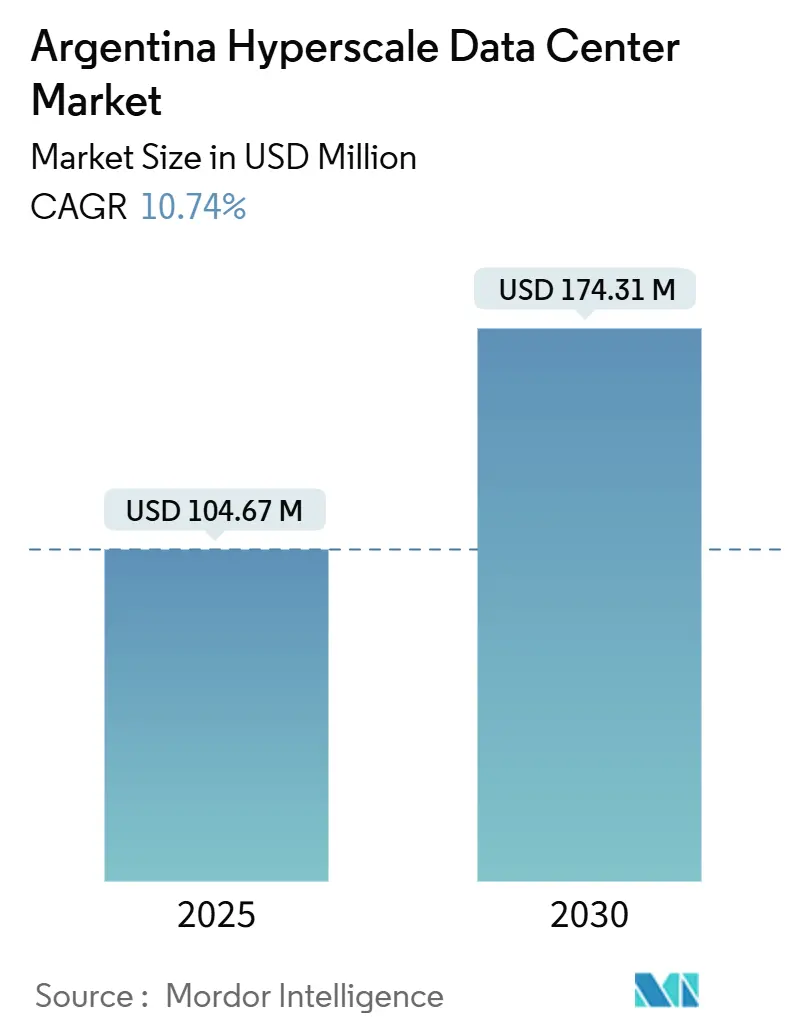

| Market Size (2025) | USD 104.67 Million |

| Market Size (2030) | USD 174.31 Million |

| Growth Rate (2025 - 2030) | 10.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Hyperscale Data Center Market Analysis by Mordor Intelligence

The Argentina Hyperscale Data Center Market size is estimated at USD 104.67 million in 2025, and is expected to reach USD 174.31 million by 2030, at a CAGR of 10.74% during the forecast period (2025-2030).

Growth rests on three inter-linked forces: surging AI workloads, a rapid pivot to public-sector cloud adoption, and tightening data-sovereignty requirements. Colocation providers are scaling capacity faster than self-build operators as enterprises avoid peso-linked capital risk. Renewable power purchase agreements are steadily lowering operating costs, while provincial tax incentives are encouraging new builds in Córdoba and Neuquén. At the same time, grid instability and currency depreciation inflate imported equipment costs, limiting near-term capacity additions despite robust demand.

Key Report Takeaways

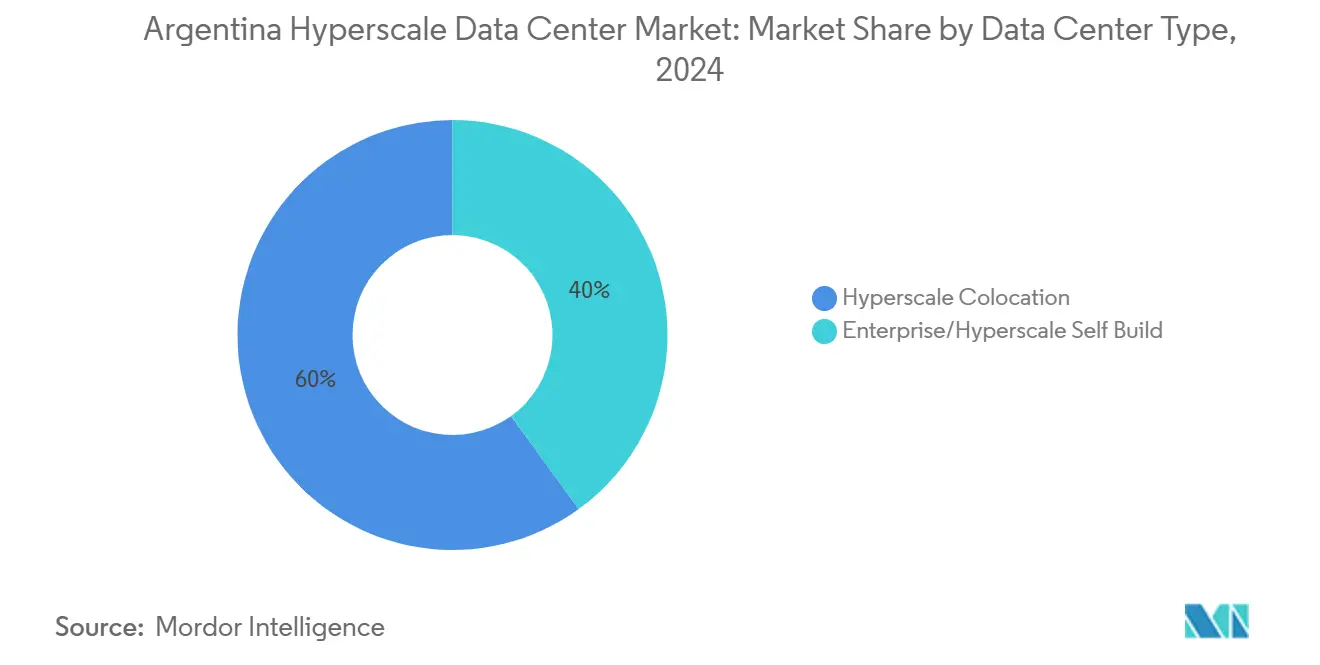

- By data center type, colocation led with 60% of the Argentina hyperscale data center market share in 2024; it is projected to post a 25% CAGR through 2030.

- By service model, IaaS held 70% share of the Argentina hyperscale data center market size in 2024, while SaaS is expected to advance at a 22% CAGR to 2030.

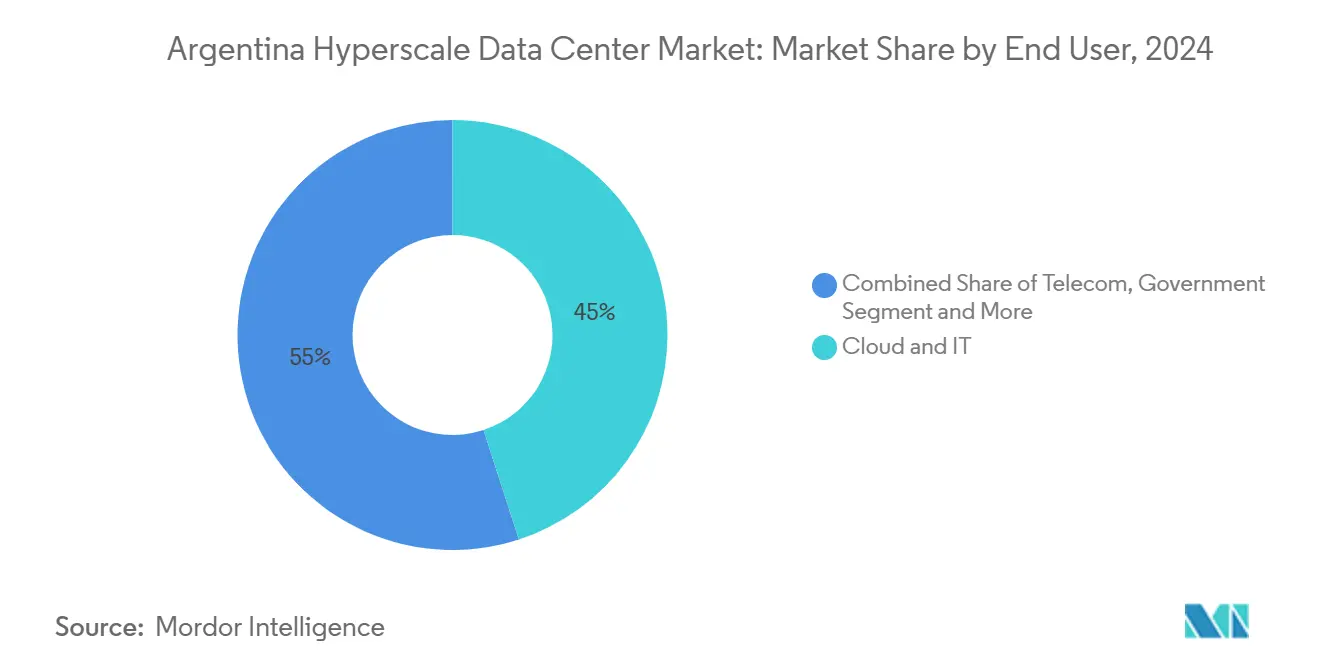

- By end user, cloud and IT providers accounted for 45% of the Argentina hyperscale data center market in 2024; e-commerce workloads are forecast to grow at a 30% CAGR between 2025-2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

The pace and direction of global change depend on shifts occurring across countries and regions simultaneously, not within any one of them alone. The global hyperscale data center market outlook research of Mordor Intelligence reflects this combined progression.

Argentina Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI workloads lift rack power densities | +3.2% | Buenos Aires clusters | Medium term (2-4 years) |

| Public-sector cloud migration | +2.5% | Federal agencies nationwide | Short term (≤ 2 years) |

| Data-sovereignty mandates tighten | +1.8% | National | Medium term (2-4 years) |

| Nationwide 5G roll-outs | +1.5% | Major urban centers | Medium term (2-4 years) |

| Wholesale renewable PPAs lowering energy OPEX | +1.2% | National, with focus on Neuquén, Córdoba | Medium term (2-4 years) |

| Niche provincial tax holidays for green DC builds (Neuquén, Córdoba) | +0.8% | Neuquén, Córdoba provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Workloads Lift Rack Power Densities

Rack densities are rising from 10 kW to 50 kW as AI training clusters dominate new deployments, forcing operators to adopt direct-to-chip liquid cooling and pursue megawatt-scale redundancies [1]Hitachi Energy, “Powering AI Data Centers: Challenges and Solutions,” hitachienergy.com. Large colocation campuses in Buenos Aires already integrate microgrids and AI-driven energy-management software that cuts facility-wide consumption by up to 30%. Grid operators are working with data-center owners to balance sudden load swings that occur when AI systems pause for model updates. Growing density has also sharpened interest in nuclear-sourced power, a resource Argentina can harness uniquely in the region. Providers willing to certify liquid-cooling skills enjoy faster occupancy and secure premium pricing.

Public-Sector Cloud Migration

Federal ministries and provincial utilities have accelerated cloud adoption to modernize citizen-facing services and cut IT overhead. This mandates in-country hyperscale capacity to maintain data residency, directly enlarging the Argentina hyperscale data center market. Multi-year procurement pipelines, often awarded under framework agreements, create stable revenue visibility for operators. Up-front compliance checks, however, lengthen deal cycles; providers able to demonstrate ISO 27001 and ENSA national security certifications capture contracts faster. Several ministries are experimenting with sovereign-cloud zones hosted inside colocation suites, a model expected to spread across state-owned enterprises by 2027.

Data-Sovereignty Mandates Tighten

The updated Personal Data Protection Bill aligns domestic rules with GDPR, effectively banning outbound personal-data transfers unless stringent contractual safeguards exist. Financial services, healthcare, and telecoms are required to process and store sensitive workloads on Argentine soil, fueling incremental rack demand across metro campuses. Operators respond by offering “trusted cloud” availability zones ring-fenced for compliance audits. The legislation is also pushing foreign SaaS vendors to localize databases, boosting near-term requirements for 3-5 MW increments.

Nationwide 5G Roll-Outs

Spectrum auctions concluded in 2025 unlock new edge-computing use cases that rely on hyperscale backhaul for AI-driven analytics. Telecom carriers partner with colocation specialists to build latency-optimized regional nodes, distributing traffic away from congested Buenos Aires. The expected wave of autonomous retail, tele-medicine, and industrial-IoT services strengthens the revenue mix of hyperscale operators by diversifying beyond traditional enterprise cloud tenants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic grid instability and diesel-price volatility | -2.1% | National, most severe in Buenos Aires province | Short term (≤ 2 years) |

| Peso-FX risk inflating imported CAPEX | -1.8% | National | Medium term (2-4 years) |

| Lengthy municipal permitting in Buenos Aires province | -1.2% | Buenos Aires province | Medium term (2-4 years) |

| Scarcity of local GPU-grade liquid-cooling expertise | -0.9% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid Instability and Diesel Volatility

Argentina suffers 3-5 times more power interruptions than Brazil, compelling operators to oversize UPS banks and diesel storage, driving opex 20% above regional peers [2]Fitch Ratings, “Argentina Electric Utilities Dashboard,” fitchratings.com. Diesel price spikes add budgeting uncertainty; some campuses now hedge fuel costs via multi-year forward contracts. Frequent grid events force automatic islanding of facilities, raising maintenance expenditure on switching gear. Although renewable PPAs are gaining traction, limited grid interconnection restrains maximum power draw in peak summer months, delaying expansion phases.

Peso-FX Swings Inflate CAPEX

High inflation and capital controls raise the landed cost of imported switchgear, batteries, and GPUs by as much as 40% [3]Telecom Argentina S.A., “2024 Annual Report,” telecom.com.ar. Financing structures such as dollar-linked contracts partially offset exposure yet introduce legal complexity. Long lead times further compound risk: payment schedules for chillers or generators often bridge multiple peso devaluations. As a result, some operators split projects into 5 MW blocks financed in foreign currency to cap risk, a practice slowing overall capacity delivery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Gains Momentum

Colocation facilities held 60% of the Argentina hyperscale data center market size in 2024, benefiting from enterprises that want scale without absorbing construction risk. The segment’s 25% CAGR to 2030 reflects sustained interest from multinational SaaS vendors localizing workloads to comply with data-sovereignty rules. Strong pre-leasing of entire data halls reduces payback periods and enables phased build-outs aligned with currency-hedged purchase agreements.

Colocation providers differentiate through design-build standardization, offering flat-pack modules that deliver 6–10 MW increments within 12 months. Conversely, self-build campuses managed by single enterprises control 40% of capacity yet proceed cautiously, given volatile import costs for transformers and high-density cooling skids. Some banks and critical-infrastructure operators keep self-build programs alive to retain control over power and cybersecurity stacks, but they increasingly lease colocation suites to meet bursting AI demand. The Argentina hyperscale data center market continues to reward operators that can deliver concurrent maintainability at PUE ≤ 1.3 and SLA guarantees resistant to peso shocks.

By Service Model: SaaS Surges Past Traditional IaaS

IaaS captured 70% of Argentina hyperscale data center market share in 2024, serving as the default off-premise compute layer for enterprises migrating legacy workloads. Sub-hour provisioning windows and consumption-based billing accelerate IaaS adoption among start-ups and state agencies alike. However, the SaaS segment is projected to grow at 22% CAGR, reflecting rising demand for sector-specific applications that eliminate infrastructure management overhead.

SaaS vendors partner with colocation hosts to guarantee local storage of citizen data and low-latency connections to public users. PaaS offerings occupy a strategic middle ground; integrated DevSecOps toolchains appeal to software houses clustered in Córdoba. Market leaders add AI inference APIs running on GPU clusters to monetize high-density compute pools. As the Argentina hyperscale data center industry matures, service diversification is expected to tilt revenue share toward SaaS by the end of the forecast period.

By End User: E-Commerce Accelerates Capacity Uptake

Cloud and IT providers contributed 45% to 2024 revenue, underpinning baseline demand across multiple availability zones. Their multi-year roadmaps ensure steady pipeline visibility for facility operators and drive early adoption of liquid cooling to minimize footprint.

E-commerce workloads are forecast to expand at 30% CAGR through 2030, spurred by rising digital-wallet usage and same-day delivery expectations. Retailers integrate real-time inventory analytics and recommendation engines that run on GPU-heavy clusters, intensifying power-density requirements. Telecommunications carriers follow closely, offloading 5G core functions into hyperscale nodes to reduce latency. Government, BFSI, and media groups fill remaining capacity slices, each bringing strict regulatory or streaming-bandwidth demands that influence facility design and connectivity routes. The diversified tenant mix cushions the Argentina hyperscale data center market against sector-specific shocks.

Geography Analysis

The Buenos Aires metropolitan area hosts roughly 75% of national hyperscale capacity, offering dense fiber routes, low-latency access to enterprise campuses, and proximity to key IXP. Land scarcity and time-consuming municipal permits, however, lengthen development cycles by up to 18 months. Operators mitigate risk by securing expansion parcels early and pre-ordering medium-voltage switchgear to bypass port delays. Despite grid challenges, Buenos Aires remains pivotal for financial trading, content delivery, and sovereign-cloud workloads that demand sub-5 ms round-trip times.

Córdoba and Rosario emerge as tier-2 hubs, lured by provincial tax holidays and skilled engineering talent fostered by local universities. Average land prices sit 35% below Buenos Aires, and provincial authorities fast-track environmental approvals within 90 days. Córdoba’s public-private innovation clusters anchor several 10 MW build-to-suit projects serving SaaS and gaming. Rosario leverages its logistics corridor to target edge deployments for agritech analytics. Both cities collectively add resilience to the Argentina hyperscale data center market by distributing risk away from the capital’s power bottlenecks.

Neuquén promotes Vaca Muerta’s abundant gas output to guarantee stable generation for energy-intensive data centers. Planned high-voltage interconnects could allow campuses to tap surplus renewables from Patagonia’s wind belt. Northern provinces with high solar irradiance remain under-developed owing to limited long-haul fiber but represent future sites for solar-co-located facilities as digital-inclusion programs widen backbone coverage. Southern Patagonia offers natural free-air cooling eight months a year, yet seismic considerations and sparse workforce availability delay sizeable investments. Over the forecast horizon, geography diversification is expected to trim aggregate latency by 15% and lower blended PUE for the Argentina hyperscale data center market.

Mordor Intelligence examines the hyperscale data center market across diverse other regional markets as well, including Europe, North America, and Middle East, while also offering granular country-level perspectives for United States, Canada, France, Saudi Arabia, Thailand, and Philippines and more.

Competitive Landscape

Global hyperscalers AWS, Microsoft, and Google anchor the market with multi-hundred-million-dollar investments in regional cloud zones. Their combined pre-leased power share sits near 60%, giving them scale economies in equipment procurement and renewable-energy contracting. Local colocation specialists counter by forming joint ventures that bundle sovereign-cloud compliance and managed services. Strategic partnerships with energy companies secure 10- to 15-year renewable PPAs, supporting aggressive sustainability roadmaps and reinforcing customer trust [4]Argus Media, “Argentina Renewable Push Gains Steam,” argusmedia.com.

M and A momentum is rising as investors consolidate smaller edge facilities to feed hyperscale campuses. The 2025 Incentive Regime for Large Investments (RIGI) grants tax abatements and FX stability, attracting infrastructure funds that previously avoided the market ibanet.org. Competitive intensity now hinges on power-purchase leverage and land-bank optionality rather than rack pricing alone. Providers capable of delivering sub-1.3 PUE at competitive lease rates will secure anchor tenants, locking in five-to-seven-year revenue streams and solidifying their foothold in the Argentina hyperscale data center market.

Argentina Hyperscale Data Center Industry Leaders

Amazon Web Services Inc.

Microsoft Corporation

Google LLC

IBM Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Patria Investments launched Omnia, a hyperscale data-center platform targeting Latin America, including projects in Argentina.

- January 2025: AWS committed USD 800 million for a regional data-center cluster in Bahía Blanca-Coronel Rosales under Knowledge Economy Law incentives.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Argentina hyperscale data center market as the annual value generated by facilities of at least 15 MW critical IT load that are purpose-built or wholesale-leased by cloud, digital media, fintech, and AI service providers across the country. Revenues from land purchase, shell construction, electrical and mechanical fit-out, plus recurring wholesale capacity charges are included, giving us a full-lifecycle view that, according to Mordor Intelligence, summed to USD 104.67 million in 2025.

Scope exclusion: Edge micro-sites below 15 MW, enterprise server rooms, and managed hosting racks inside telecom central offices are not covered.

Segmentation Overview

- By Data Center Type

- Hyperscale Colocation

- Enterprise/Hyperscale Self Build

- By Service Type

- IaaS ( Infrastructure-as-a-Service)

- PaaS ( Platform-as-a-Service)

- SaaS( Software-as-a-Service)

- By End User

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End User

Detailed Research Methodology and Data Validation

Primary Research

Our analysts speak with facility operators, electrical EPC contractors, cloud procurement managers, and provincial regulators in Buenos Aires, Cordoba, and Rosario. These interviews validate utilization ramps, typical construction cost per MW, and FX hedging practices, filling critical gaps left by public data.

Desk Research

We start with freely accessible tier-1 sources such as Enacom broadband statistics, Indec energy price indices, AFIP import filings for servers and switchgear, and trade-body releases from the Latin American Neutral Network Association. To anchor supply, customs shipment data and patent filings (via Questel) reveal inbound high-density racks and liquid cooling skids, while grid capacity updates from Cammesa confirm realistic power delivery timelines. Company 10-Ks, investor decks, and respected press articles round out demand signals. Paid databases (D&B Hoovers for financials and Dow Jones Factiva for deal flow) let us cross-check operator CAPEX. This list is illustrative; many additional sources inform individual datapoints.

Market-Sizing & Forecasting

A top-down capacity-build approach converts announced MW pipelines, occupancy curves, and average USD per MW build costs into market value, which is then corroborated through selective bottom-up checks such as sampled wholesale lease rates and rack counts. Key variables like installed IT MW, average rack density, electricity tariff trajectory, peso-USD exchange path, occupancy ramp-up, and typical MEP cost per MW drive the model. Multivariate regression projects each driver to 2030, and scenario analysis adjusts for grid reliability shocks.

Data Validation & Update Cycle

Outputs undergo variance checks against independent MW trackers and public CAPEX disclosures, followed by peer review and a final senior analyst sign-off. We refresh the model annually, with rapid updates triggered by material project announcements or tariff revisions.

Why Mordor's Argentina Hyperscale Data Center Baseline Deserve Your Confidence

We recognize published estimates differ because firms mix data center classes, convert currencies at varying dates, or model optimistic utilization ramps.

Key gap drivers include scope breadth (some roll in every facility type), reliance on press-release CAPEX without occupancy proof, or the absence of local FX risk adjustments that Mordor's analysts apply before finalizing the baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 104.67 million (2025) | Mordor Intelligence | - |

| USD 2,295.5 million (2024) | Global Consultancy A | Counts all data center formats; limited primary checks; no FX volatility weighting |

| USD 76 million (2024) | Trade Journal B | Focuses on retail colocation only; ignores hyperscale self-build spend and capacity ramp timing |

These contrasts show that Mordor Intelligence provides a balanced, transparent baseline that links clear variables to repeatable steps, giving decision-makers a dependable view of Argentina's hyperscale trajectory.

Key Questions Answered in the Report

What is the current value of the Argentina hyperscale data center market?

The market stands at USD 0.10 billion in 2025 and is forecast to reach USD 0.17 billion by 2030.

Which data center type is growing fastest in Argentina?

Colocation facilities are expanding at a 25% CAGR through 2030, outpacing self-build models

Why are AI workloads so important for Argentina’s hyperscale growth?

AI training clusters require 30–50 kW rack densities and large GPU pools, driving new power and cooling investments that boost overall capacity demand

How do provincial incentives influence site selection?

Tax holidays in Córdoba and Neuquén cut start-up costs and speed permits, encouraging operators to diversify away from Buenos Aires.

Page last updated on: