Sweden Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

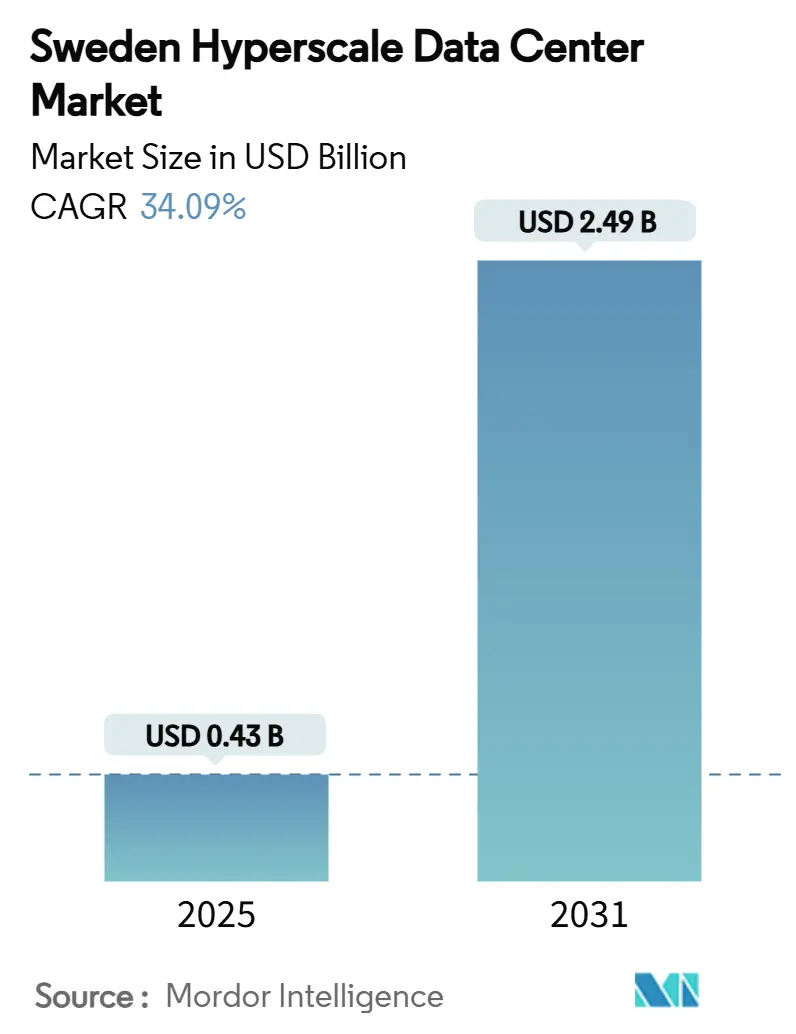

| Market Size (2025) | USD 0.43 Billion |

| Market Size (2031) | USD 2.49 Billion |

| Growth Rate (2025 - 2031) | 34.09% CAGR |

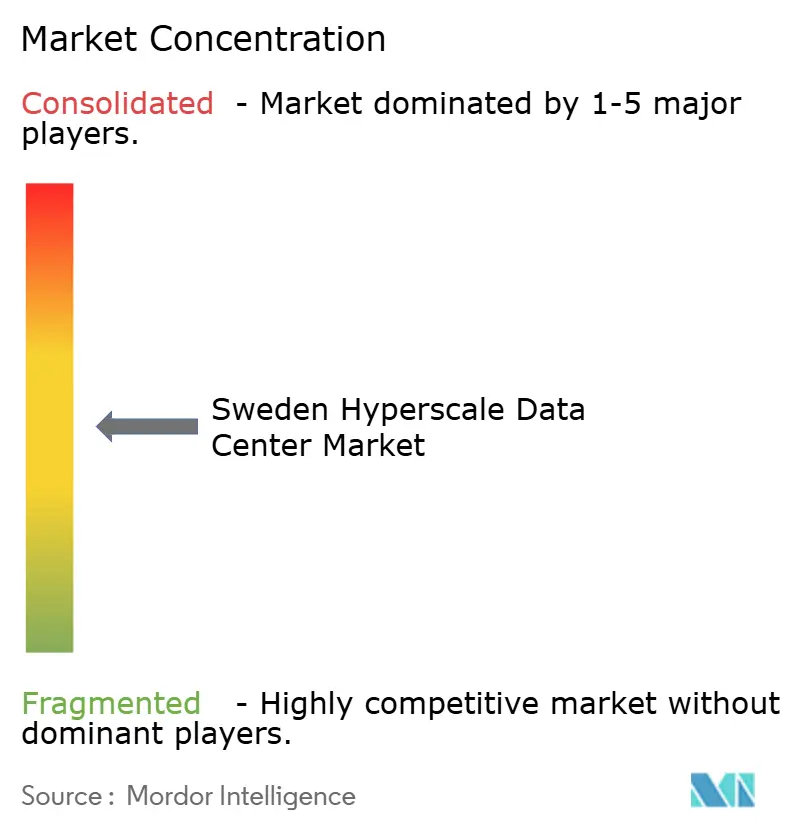

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Hyperscale Data Center Market Analysis by Mordor Intelligence

The Sweden hyperscale data center market size reached USD 427.64 million in 2025 and is forecast to climb to USD 2,485.94 million by 2031, reflecting a powerful 34.09% CAGR. Solid investment momentum, highly competitive renewable-energy pricing, and a policy environment that rewards domestic data processing underpin this expansion. Subsea cable upgrades strengthen international connectivity, while district-heat reuse programs lower operating costs and reinforce sustainability credentials. The arrival of ultra-large AI training clusters accelerates mechanical-infrastructure innovation, especially in liquid cooling. Together, these forces position the Sweden hyperscale data center market as the Nordic region’s primary magnet for next-generation cloud and AI workloads.

Key Report Takeaways

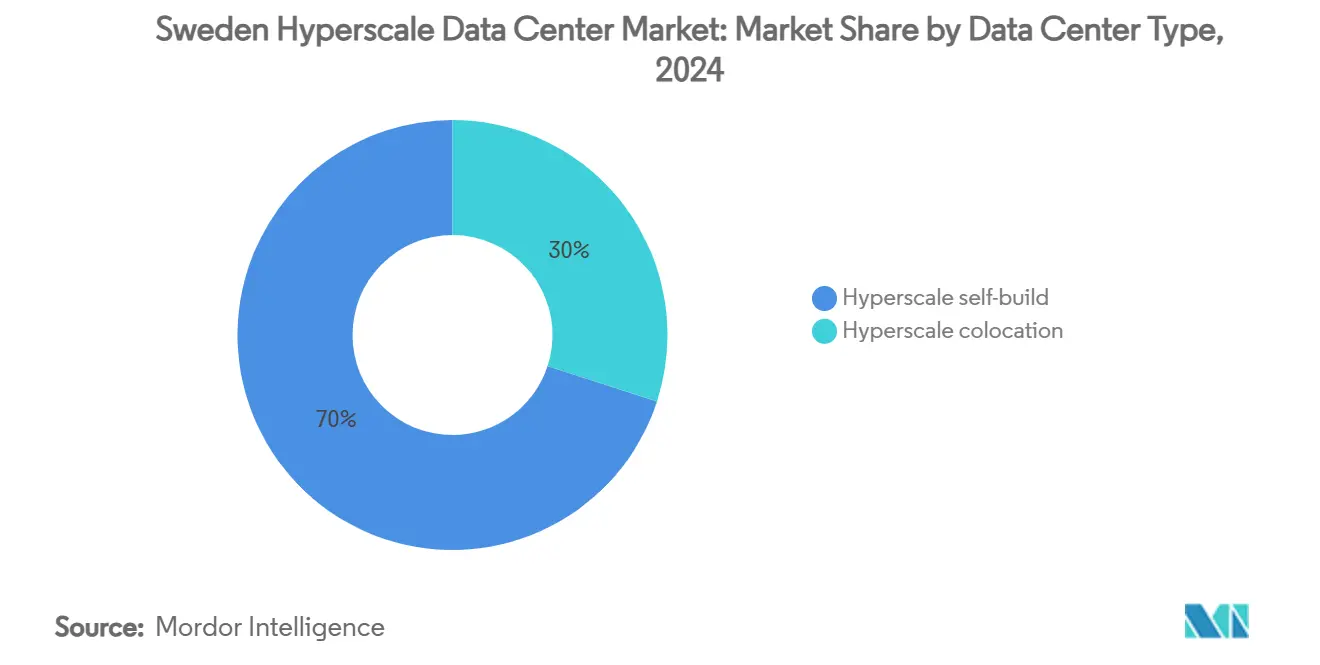

- By data center type, hyperscale self-builds held 70% of Sweden hyperscale data center market share in 2024, whereas hyperscale colocation is projected to expand at an 11.50% CAGR through 2030.

- By component, IT infrastructure commanded 45% share of the Sweden hyperscale data center market size in 2024, while mechanical infrastructure is advancing at a 12.00% CAGR to 2031.

- By tier standard, Tier III facilities accounted for 80% share of the Sweden hyperscale data center market size in 2024 and Tier IV deployments are rising at a 14.20% CAGR through 2031.

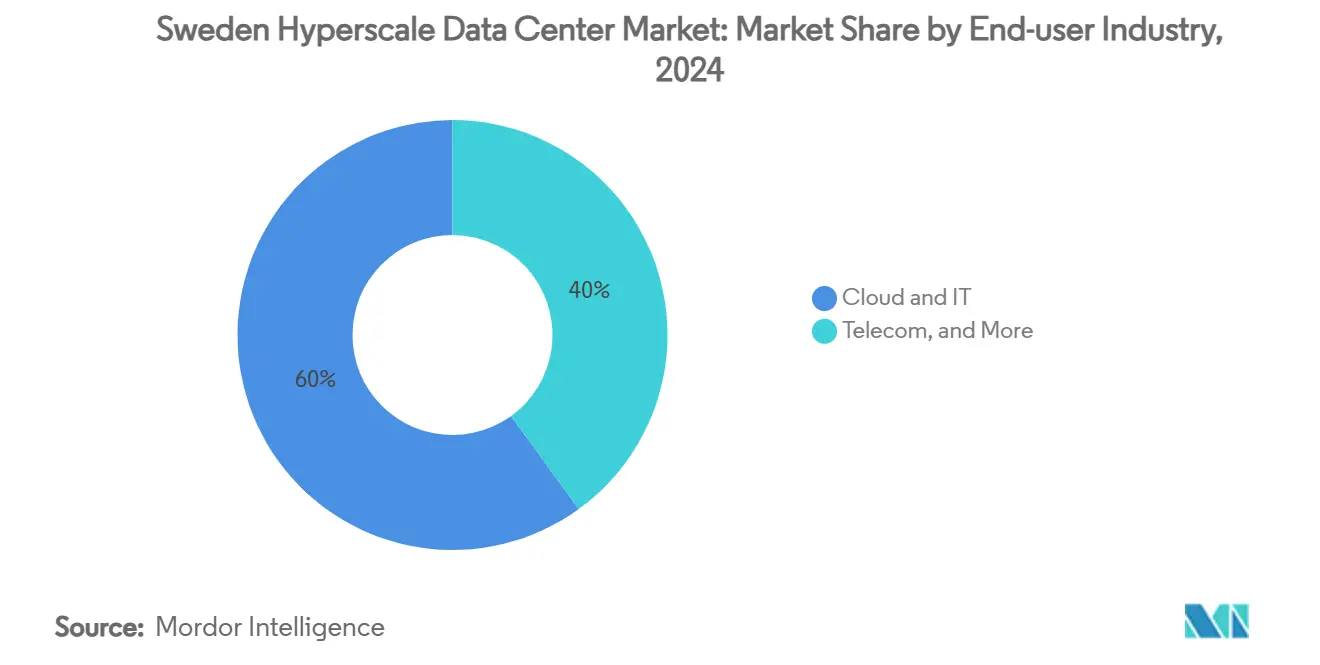

- By end-user industry, cloud and IT led with 60% revenue share in 2024; BFSI is forecast to expand at a 13.00% CAGR to 2031.

- By data center size, massive (greater than 25 MW and less than equal to 60 MW) captured 50% share of the Sweden hyperscale data center market size in 2024, while mega (greater than 60 MW) facilities post the fastest 15.00% CAGR to 2030.

Sweden participates in a competitive field that extends beyond its own borders. The market landscape in the global hyperscale data center industry outlined by Mordor Intelligence covers that wider structure.

Sweden Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in cloud-region launches by hyperscalers | +8.50% | National, concentrated in Stockholm-Mälardalen region | Short term (≤ 2 years) |

| Rapid build-out of new subsea cable landings to Swedish shores | +6.20% | Coastal regions, particularly west coast connectivity hubs | Medium term (2-4 years) |

| Government digital-sovereignty and data-residency mandates | +7.80% | National, with priority for government and BFSI sectors | Medium term (2-4 years) |

| Abundant hydro and wind PPAs lowering total energy cost | +5.90% | Northern Sweden hydroelectric regions, offshore wind zones | Long term (≥ 4 years) |

| Gen-AI inferencing demand spurring liquid-cooled edge nodes | +4.10% | Urban centers with high compute density requirements | Short term (≤ 2 years) |

| Mandated district-heat reuse unlocking new revenue streams | +2.40% | Urban districts with existing heating infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in cloud-region launches by hyperscalers

Microsoft’s USD 3.2 billion allocation for new Swedish cloud regions illustrates a sovereignty-first strategy that is reshaping hyperscale capital plans [1].Total Telecom, “Microsoft pours USD 3.2 billion in Swedish cloud infrastructure,” totaltele.com AWS is adding three facilities in Mälardalen using lower-carbon steel, cutting build-phase emissions by 70%. Each announcement compresses competitors’ rollout schedules, spurring a self-reinforcing investment cycle. Domestic newcomer Evroc is leveraging the momentum to secure land near Arlanda Airport for a hyperscale AI campus. These overlapping projects amplify demand for specialty cooling systems and high-voltage interconnects at a pace unseen in traditional colocation builds.

Rapid build-out of new subsea cable landings to Swedish shores

GlobalConnect’s Nordic Super Fiber Cable adds 3 Pbps of capacity and underpins Sweden’s pivot from a regional to a continental gateway. A SEK 75 million (USD 7.77 million) land link to Finland hardens Nordic redundancy and mitigates recent cable-break risks in the Baltic. Operators now prioritize coastal campuses that pair landing stations and data halls to shave milliseconds of latency. Enhanced resilience also elevates Sweden’s appeal for disaster-recovery nodes serving Germany, Poland, and the UK.

Government digital-sovereignty and data-residency mandates

Sweden’s 2025-2030 digitalization plan cements local data processing as a national-security pillar. The EUR 1 billion (USD 1.15 billion) public-sector infrastructure budget requires that sensitive workloads stay within national borders. Tele2’s sovereign-cloud platform and Swedbank’s domestic private-cloud rollout confirm that both public and financial institutions now index site selection on country-level sovereignty rather than price. These mandates widen the competitive moat for Sweden hyperscale data center market entrants that can provide in-country, Tier IV-certified capacity.

Abundant hydro and wind PPAs lowering total energy cost

Vattenfall’s 24/7 renewable-matching for Microsoft showcases how granular power-purchase agreements slash emissions without eroding uptime [2].Vattenfall, “Vattenfall to deliver renewable energy 24/7 to Microsoft’s Swedish datacenters,” vattenfall.com Google’s additional Swedish wind buys for its Finnish hub indicate cross-border arbitrage opportunities that reward hyperscale buyers willing to contract in bulk. Planned small modular reactors could supply carbon-free baseload, further flattening electricity price volatility

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transmission-grid congestion in urban clusters | -4.70% | Stockholm metropolitan area, Gothenburg region | Short term (≤ 2 years) |

| Shortage of HV electrical and mechanical O and M talent | -3.20% | National, acute in northern development zones | Medium term (2-4 years) |

| Water-stress moratoria on evaporative cooling designs | -2.10% | Southern Sweden, drought-prone municipalities | Long term (≥ 4 years) |

| GPU / photonics allocation bias toward Tier-1 European regions | -1.80% | National, affecting AI-optimized facility development | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Transmission-grid congestion in urban clusters

Multiple 50-100 MW interconnect requests converge on Stockholm’s 400 kV ring, stretching queue times to 18 months. Vattenfall’s fast-track program with Svenska Kraftnät mitigates delays yet still requires SEK 2 billion upgrades for Brookfield’s 750 MW Strängnäs campus. Northern hydro surplus remains stranded until long-lead reinforcement lines come online.

Shortage of HV electrical and mechanical O and M talent

Instalco reports a multi-year backlog for certified high-voltage technicians, forcing operators to import labor at premium rates [3].Instalco, “Annual Report and Sustainability Report 2023,” instalco.se Training programs at Luleå Technical University will not close the gap before 2027, compelling developers to pre-commit to workforce pipelines when securing land.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Self-Build Dominance Drives Market Evolution

Self-builds delivered 70% of Sweden hyperscale data center market revenue in 2024, a level that underscores hyperscalers’ need for architectural control over AI power and cooling. Operators deploy proprietary immersion-cooling loops that colocation landlords rarely accommodate. Microsoft’s Swedish campuses integrate patent-pending cold-plate designs, while AWS’s steel-based carbon-reduction effort drops embodied emissions by 70%.

Colocation, though smaller, is the fastest riser at an 11.50% CAGR. Providers such as atNorth employ 100% renewable supply and heat-capture integration to attract enterprise AI clusters that require low-carbon credentials without capex exposure. The converging design language between purpose-built halls and wholesale colocation indicates a hybrid future where hyperscalers lease edge nodes while maintaining core self-build campuses, sustaining long-term growth for Sweden hyperscale data center market.

By Component: Mechanical Infrastructure Leads Innovation Wave

IT hardware still absorbs 45% of spend, yet mechanical systems post the quickest 12.00% CAGR. Direct-to-chip liquid loops, rear-door heat exchangers, and industrial-scale heat-recovery units now form a greater share of bill-of-materials. SWEP’s brazed-plate exchangers enable PUE levels below 1.15, lifting both efficiency and heat-sale revenue.

Electrical infrastructure keeps pace as UPS units shift to lithium-ion chemistries that fit higher rack power densities. General construction gains strategic weight because facilities must embed district-heat interfaces and water-free cooling towers from day one, reshaping project timelines and capex profiles within the Sweden hyperscale data center market.

By Tier Standard: Tier IV Growth Reflects AI Reliability Demands

Tier III remains dominant but Tier IV’s 14.20% CAGR signals a pivot toward 99.995% uptime for latency-sensitive AI inference. DeepL’s SuperPod deployment illustrates the cost of learning interruptions, justifying redundant feed systems and 2N+1 mechanical topology.

New builds now embed Tier IV readiness at design stage rather than retrofit, compressing lifecycle costs. This trajectory elevates the Sweden hyperscale data center market size for premium power gear and extends average construction cycles, but the revenue upside offsets the schedule extensions.

By End-User Industry: BFSI Transformation Accelerates Digital Demand

Cloud and IT held 60% revenue in 2024, yet BFSI’s 13.00% CAGR reflects regulatory urgency for in-country compute. Nordea and Swedbank anchor large-footprint deals that require certified private-cloud zones within hyperscale campuses.

Public-sector modernization under the EUR 1 billion (USD 1.15 billion) Digital Transformation Infrastructure Plan injects steady demand across multiple counties, while manufacturers like SKF deploy Azure-Arc hybrid solutions that keep factory data local. Together these verticals diversify the Sweden hyperscale data center market revenue book and stabilize utilization rates.

By Data Center Size: Mega Facilities Drive Capacity Concentration

Massive camps between 25-60 MW offer 50% of live power, balancing grid-connection ease with economies of scale. Mega sites above 60 MW expand fastest at 15.00% CAGR as AI clusters prefer single-campus terabit interconnects. Brookfield’s 750 MW Strängnäs project exemplifies scale economics that compress network latency and centralize maintenance.

EcoDataCenter’s 240 MW Borlänge roadmap (expandable to 360 MW) illustrates phased-build tactics that align power-availability milestones with contracted AI demand. Such deployments elevate the Sweden hyperscale data center market size and signal grid-planning authorities to accelerate substation upgrades.

Geography Analysis

The Stockholm-Mälardalen corridor anchors 55% of Nordic internet traffic and hosts more than 125 carriers, anchoring it as the logical first stop for international entrants. Subsea landing upgrades fortify the capital’s role as the principal European gateway for Nordic cloud flows, encouraging hyperscalers to co-locate cable heads and compute halls. Urban district-heat grids enable operators to monetize thermal output, lowering effective PUE and trimming energy costs below EUR 0.03 per kWh.

Northern Sweden leverages abundant hydro resources and cool ambient temperatures that facilitate free-air cooling for up to 10 months each year. Facebook’s long-standing Luleå campus validated the region, and EcoDataCenter’s planned 150 MW Östersund site accelerates the northern cluster, adding renewable capacity without stressing urban grids. The prospect of small modular reactors near Ringhals introduces future baseload options that could further reduce carbon intensity.

Western coastal municipalities increasingly woo hyperscale investments to exploit newly reinforced subsea landings. GlobalConnect’s fiber corridors shorten round-trip times to Germany and the UK, offering an alternate to congested Danish routes. This tri-regional dynamic diversifies site selection within the Sweden hyperscale data center market and moderates power-price disparities across the country.

Mordor Intelligence provides coverage of the hyperscale data center market across other key regional markets, including Europe, North America, and Middle East, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Italy, United Kingdom, United States, Saudi Arabia, Taiwan, and South Korea incorporating local coverage and market participation, as required.

Competitive Landscape

Global hyperscalers—AWS, Microsoft, Google—anchor the ecosystem through self-build mega-campuses that set scale and efficiency benchmarks. International colocation leaders Equinix, Digital Realty, and NTT supplement capacity with carrier-dense facilities aimed at enterprises seeking rapid deployment. Nordic specialists EcoDataCenter, atNorth, and Bahnhof differentiate by offering climate-positive operations, heat-recovery integration, and low-carbon construction materials.

Sustainability narratives now extend to power sourcing transparency and embodied-carbon disclosure. EcoDataCenter’s biomass-augmented Falun campus and Digital Realty’s district-heat partnerships illustrate how operators translate green credentials into long-term price advantages. Small-modular-reactor developers such as Kärnfull Next represent a potential disruptive cohort, promising zero-carbon baseload that could reset market power-pricing curves within a decade.

Competitive focus is also shifting toward AI-optimized white space. The NVIDIA-backed AI Technology Center demonstrates how sovereign AI demand can concentrate GPU clusters within colocation environments, forcing incumbents to re-engineer layouts for liquid cooling and 100 kW racks. Operators able to marry carrier density, heat-reuse revenue, and Tier IV resiliency will command premium pricing in the Sweden hyperscale data center market.

Sweden Hyperscale Data Center Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Meta Platforms, Inc.

Digital Realty Trust, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: GlobalConnect completed a land-based Sweden-Finland fiber link carrying up to 3 Pbps, bolstering Nordic digital security.

- February 2025: STACK Infrastructure advanced a 30 MW Stockholm campus, with 18 MW under construction in a sustainability-focused global expansion.

- March 2025: Areim raised USD 977 million to fund green data-center projects across the Nordics, with Sweden as a priority.

- May 2025: A Swedish consortium with AstraZeneca, Ericsson, Saab, SEB, and Wallenberg Investments partnered with NVIDIA to deploy two DGX SuperPODs, creating Sweden’s largest enterprise AI supercomputer.

- June 2025: Brookfield committed SEK 95 billion (USD 9.9 billion) for a 750 MW AI data-center campus in Strängnäs, more than doubling its earlier plan.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Swedish hyperscale data center market as the annual revenue stream generated by newly built or leased facilities delivering at least 4 MW of IT load to a single owner or anchor tenant and engineered for cloud-scale automation, modular expansion, and PUE targets below 1.3.

Scope exclusion: Edge micro-sites below 4 MW and enterprise on-premises server rooms are excluded.

Segmentation Overview

- By Data Center Type

- Hyperscale self-build

- Hyperscale colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Unit

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction and Services

- Core and Shell Development

- Installation and Commisioning Services

- Design Engineering

- Fire Detection, Suppression and Physical Security

- DCIM/BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-User Industry

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End Users

- By Data Center Size

- Large (Less than equal to 25 MW)

- Massive (Greater than 25 MW and less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Primary Research

We interviewed Swedish grid planners, real-estate developers, Nordic cloud-region directors, HVAC OEM engineers, and channel partners across Stockholm, Vasteras, and Lulea. Their inputs helped validate power-price assumptions, attainable rack densities, and likely commissioning timetables, ensuring that survey feedback bridged gaps left by desk research.

Desk Research

Our analysts began with statutory and open datasets from bodies such as the Swedish Energy Agency, Svenska kraftnat, the Swedish Post & Telecom Authority, and Eurostat, which quantify grid capacity, latency corridors, and data-traffic growth. Trade association portals like SweDCI, Cloudscene, and the European Data Centre Association supplied facility counts and tier splits that anchor installed base estimates.

These insights were enriched with company filings, investor decks, and reputable press archives captured via D&B Hoovers and Dow Jones Factiva, while patent clusters for immersion cooling were sampled through Questel to flag emerging capex drivers. The sources listed are illustrative; many additional public and paid references were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

A top-down build starts with Stockholm and regional IT-load statistics, electricity-tax records, and announced hyperscale capex, which are then converted to revenue using sampled average build cost per deployed megawatt. Results are corroborated through a selective bottom-up roll-up of disclosed campus capacities and channel ASP × volume checks. Key variables like renewable-energy price index, average rack density, AI/Telco workload penetration, tax-rebate runway, and grid-connection lead time feed a multivariate regression that generates the 2025-2031 outlook. Scenario analysis adjusts for power-pricing shocks.

Data Validation & Update Cycle

Outputs pass variance scans against historical series, peer ratios, and fresh primary calls before senior review. Models refresh annually, with interim updates triggered by >=100 MW announcements or regulatory moves; a last-mile sense check precedes every client delivery.

Why Mordor's Sweden Hyperscale Data Center Baseline Rings True

Published numbers differ because firms mix geographies, measure spend instead of revenue, or omit cooling retrofits. Our disciplined scope, annual refresh, and dual-layer validation keep the 2025 market value at USD 427.64 million both transparent and repeatable.

Key gap drivers include: some publishers quote global or Nordic aggregates, others apply unvetted ASP uplifts, and a few rely on outdated capacity pipelines lacking on-site verification.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 427.64 M (2025) | Mordor Intelligence | - |

| USD 162.79 B (2024) | Global Consultancy A | Global scope, spend metric, single-step top-down model |

| USD 2.8 B (2023) | Trade Journal B | Investment value, mixes colocation & enterprise halls, unclear FX basis |

Taken together, the comparison shows that once scope and metric misalignments are stripped away, Mordor's grounded, variable-driven baseline offers decision-makers a dependable reference point for Sweden's rapidly scaling hyperscale landscape.

Key Questions Answered in the Report

What is the forecast value of the Sweden hyperscale data center market in 2031?

It is projected to reach USD 2,485.94 million by 2031, growing at a 34.09% CAGR.

Which segment is expanding fastest by tier standard?

Tier IV facilities are advancing at a 14.20% CAGR because AI training and inference workloads demand 99.995% uptime.

How do Sweden’s renewable resources benefit data-center operators?

Operators secure 24/7 hydro- and wind-matched PPAs that lower total energy cost and support aggressive sustainability targets.

Why is BFSI demand rising so quickly?

Domestic sovereignty rules require Swedish processing of sensitive financial data, driving a 13.00% CAGR for BFSI footprints.

Where are mega facilities being built?

Mega campuses exceeding 60 MW are clustering in Strängnäs, Borlänge, and other grid-reinforced zones to host large AI clusters.

What risk could slow near-term growth?

Urban transmission-grid congestion in Stockholm and Gothenburg may delay new power connections by up to 18 months.

Page last updated on: