Italy Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.45 Billion |

| Market Size (2026) | USD 1.96 Billion |

| Market Size (2031) | USD 9.08 Billion |

| Growth Rate (2026 - 2031) | 35.88% CAGR |

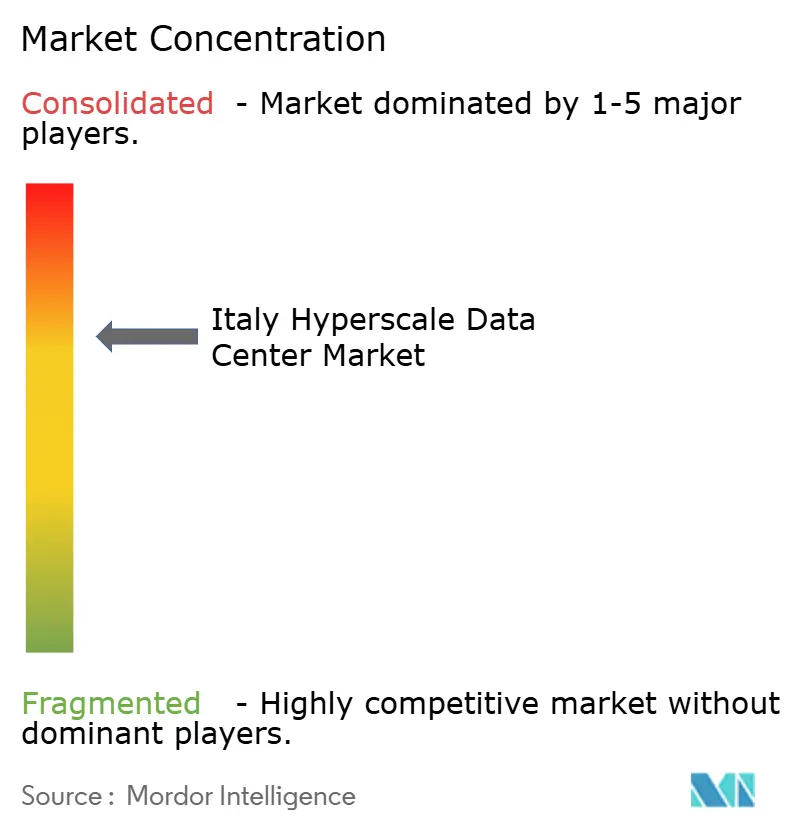

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Hyperscale Data Center Market Analysis by Mordor Intelligence

The Italy hyperscale data center market size is expected to increase from USD 1.45 billion in 2025 to USD 1.96 billion in 2026 and reach USD 9.08 billion by 2031, growing at a CAGR of 35.88% over 2026-2031. Sovereign-cloud mandates under the EU Digital Decade program, sizable grants from Italy’s National Recovery and Resilience Plan, and stepped-up cloud-region launches by U.S. hyperscalers are pulling new capacity toward Milan and Rome. Subsea cable landings in Sicily are repositioning southern Italy as a low-latency gateway to North Africa, while generative-AI clusters are pushing rack densities above 40 kW and accelerating the shift to direct-to-chip liquid cooling. Developers are reserving grid capacity two years ahead of construction to avoid Lombardy’s head-room constraints, and many are pairing those allocations with long-term renewable power purchase agreements that cap electricity costs below EUR 50 per MWh. Competitive intensity is further magnified by the rush to pre-lease white space that meets Gaia-X and Tier IV requirements, giving turnkey colocation campuses a time-to-market edge over self-build projects.

Key Report Takeaways

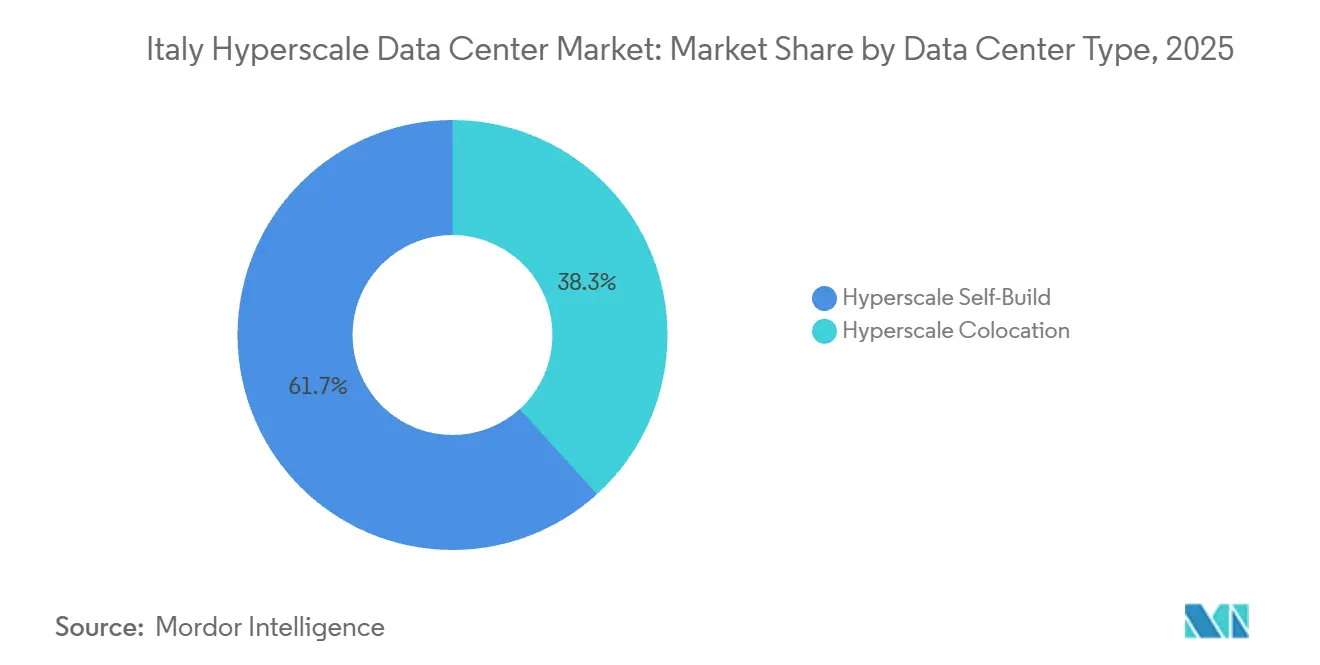

- By data center type, self-build facilities held 61.73% share in 2025, while hyperscale colocation is projected to log the fastest 36.73% CAGR through 2031.

- By component, IT infrastructure led with 52.88% market share in 2025, whereas mechanical infrastructure is forecast to expand at a 36.84% CAGR to 2031.

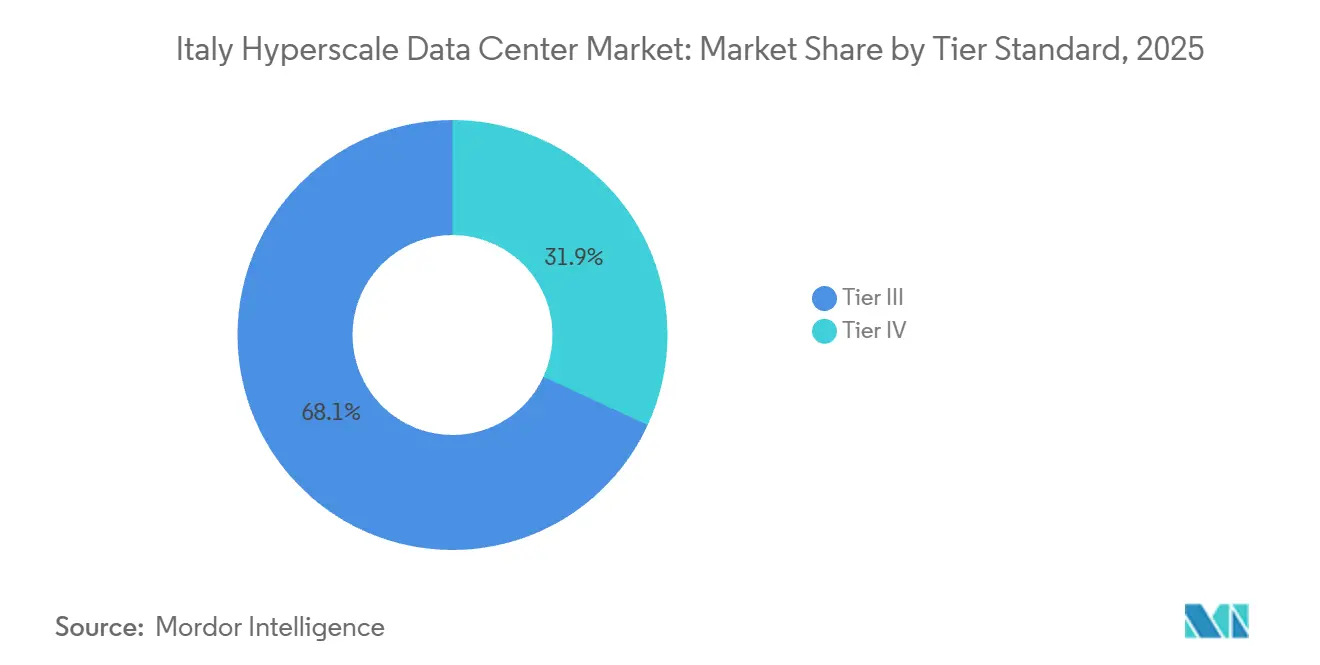

- By tier standard, tier III captured 68.13% of share in 2025, but tier IV is advancing at a 36.57% CAGR on the back of fintech and sovereign-cloud demand.

- By capacity range, massive-scale builds between 25-60 MW commanded 43.64% of share 2025, yet mega-scale campuses above 60 MW are set to grow at 36.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's hyperscale data center market share coverage captures this comparative structure.

Italy Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Cloud-Region Roll-Outs by AWS, Microsoft Azure and Google Cloud | +8.2% | National, concentrated in Lombardy (Milan) and Lazio (Rome) | Medium term (2-4 years) |

| Deployment of New Subsea Cables Landing in Sicily | +5.1% | Southern Italy (Sicily, Calabria), spillover to Lazio and Campania | Long term (≥ 4 years) |

| EU Digital-Sovereignty and Gaia-X Compliance Boosting Local Builds | +6.4% | National, with early gains in Milan, Rome, Turin | Medium term (2-4 years) |

| Corporate PPAs Tapping Italy's Solar and Wind Surge | +4.7% | National, strongest in southern regions (Puglia, Sicily, Sardinia) | Long term (≥ 4 years) |

| GenAI Inference Clusters Requiring Liquid-Cooled Edge Zones | +7.3% | Lombardy, Piedmont, Lazio | Short term (≤ 2 years) |

| Tier IV Fintech And Instant-Payments Hubs in Milan-Turin Corridor | +3.9% | Lombardy and Piedmont (Milan, Turin, Bergamo) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Cloud-Region Roll-Outs by AWS, Microsoft Azure and Google Cloud

Cloud majors are accelerating multi-availability-zone builds in Milan and Rome to satisfy GDPR location clauses and DORA resilience rules. AWS has earmarked EUR 1.2 billion for its Milan region through 2029, while Microsoft is injecting EUR 4.3 billion into Italy North, each project adding three or more zones interconnected by sub-10-millisecond fiber paths.[1]Microsoft Azure, “Azure Italy Regions,” azure.microsoft.com Oracle’s second cloud region in Turin, opened in late 2025, widened the competitive field and created an ecosystem effect in which colocation providers pre-lease shells next door to hyperscaler on-ramps. The clustering compresses procurement cycles for switchgear, generators and prefabricated liquid-cooling loops, pulling lead times below 40 weeks for some mechanical packages. Tenant urgency is further evident in DATA4’s MIL02 campus where 60% of the first 15 MW phase was pre-committed before foundations were poured.

Deployment of New Subsea Cables Landing in Sicily

Sparkle’s Unitirreno system went live in October 2025 with 24 fiber pairs, cutting round-trip latency between Milan and Tunis from 45 milliseconds to under 15 milliseconds and bringing Palermo within one hop of North African traffic flows.[2]Sparkle, “Activation of the Unitirreno Submarine Cable,” tisparkle.com The cable coincides with Terna’s 1,000 MW Tyrrhenian Link HVDC interconnector, giving Sicilian sites both bandwidth and clean-power head-room. Edge nodes near Catania are already processing maritime sensor feeds and drone video within strict 20-millisecond budgets, use cases that would be unviable over Milan-routed paths. Developers able to secure 20-30 MW at 150 kV substations near the Palermo landing station can under-cut Lombardy’s land prices by half while using solar-backed PPAs to keep operating costs flat.

EU Digital-Sovereignty and Gaia-X Compliance Boosting Local Builds

The Digital Decade program says 75% of EU firms must adopt cloud by 2030, provided workloads remain in EU-domiciled, federated environments. Italian public agencies migrating to the Public Services Network must therefore house data in facilities that display Gaia-X conformity seals showing transparent governance, reversible encryption and open API interoperability.[3]European Commission, “Digital Decade Policy Programme 2030,” digital-strategy.ec.europa.eu Aruba’s IT4 Rome campus added liquid cooling and ISO 27001 controls in 2025 and began the Gaia-X assessment process to pull ministries and local health authorities into its Tier IV halls. Compliance is becoming a commercial differentiator that lets local incumbents win against larger FLAP-D rivals despite smaller economies of scale.

Corporate PPAs Tapping Italy’s Solar and Wind Surge

Italy installed 63 GW of renewables by 2025, much of it utility-scale solar in Puglia and offshore wind in the Adriatic. Data-center operators are locking ten-year PPAs at prices well below grid tariffs; Equinix signed for 53 MW of solar power in 2025 to cover its Milan IBX portfolio. DATA4 followed with a 500 GWh wind-and-solar agreement that helps Italy’s hyperscale data center market meet the Energy Efficiency Directive’s PUE-reporting rule coming in 2026. By matching generation peaks with flexible liquid-cooling loops that allow 45 °C water inlets, campuses can run without energy-guppy penalties during summer, lifting EBITDA margins despite volatile spot prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Capacity Head-Room Constraints in Lombardy and Lazio | -4.8% | Lombardy (Milan, Bergamo) and Lazio (Rome, Pomezia) | Medium term (2-4 years) |

| Scarcity of HV/MV Engineering Talent for 24x7 O & M | -3.2% | National, acute in Lombardy, Piedmont, Lazio | Long term (≥ 4 years) |

| Water-Stress Curbs on Evaporative Cooling in Po Valley | -2.6% | Po Valley (Lombardy, Emilia-Romagna, Veneto) | Medium term (2-4 years) |

| AI-Grade GPU and Optics Preferentially Allocated to FLAP-D Hubs | -3.7% | National, with spillover delays from FLAP-D prioritization | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Capacity Head-Room Constraints in Lombardy and Lazio

Terna warns that substations around Milan and Rome could face a 150 MW shortfall by 2028 as cumulative data-center demand breaches 500 MW. Developers now secure allocations 18-24 months before breaking ground and, in some cases, pre-pay grid-access charges that raise land costs by 10-15%. Vantage Data Centers absorbed this premium at its MXP2 site, buying 96 MW capacity upfront to guarantee phased expansion. Operators that miss the queue must invest in on-site battery energy storage or accept curtailment penalties that erode service-level guarantees.

AI-Grade GPU and Optics Preferentially Allocated to FLAP-D Hubs

H100 and H200 supply constraints continue to favor Frankfurt, London, Amsterdam, Paris and Dublin. Italian buyers report 6-9-month lead times and must often accept partial shipments lacking 800G optics. The shortage delays large-language-model clusters and forces tenants to consider AMD Instinct MI300X accelerators, complicating power-and-cooling design. Colocation providers willing to stockpile optics and offer vendor-agnostic liquid-cooling manifolds can monetise the supply gap, but they also shoulder inventory risk if NVIDIA clears its backlog sooner than expected.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Gains On CapEx Discipline

Self-build campuses held the majority Italy hyperscale data center market share at 61.73% in 2025, but the capital-light appeal of turnkey white space is steering hyperscalers toward third-party halls that achieve the same security envelope without tying up balance sheets. The Italy hyperscale data center market size for colocation halls is projected to expand at a 36.73% CAGR through 2031, a trajectory underpinned by MXP2’s 32 MW first phase that attracted two cloud majors and one sovereign tenant before slab pour. Such early commitments shave a year off time-to-market compared with green-field self-builds, giving enterprises faster on-ramps for AI inference workloads.

Self-build remains entrenched in scenarios requiring bespoke hot-aisle geometry or proprietary optical fabrics, as seen in Oracle’s Turin region that integrates directly with TIM’s backbone for deterministic throughput. Even so, colocation operators are absorbing the steep entry cost of liquid cooling, letting tenants scale 60 kW racks without single-client outlay. That shift unlocks demand from fintechs and SaaS firms that would otherwise push training jobs to Frankfurt, enhancing geographic stickiness inside Italy hyperscale data center market clusters.

By Component: Mechanical Systems Surge On Liquid-Cooling Retrofits

IT infrastructure accounted for 52.88% of the share in 2025 due to GPU-dense servers, while mechanical systems are projected to grow the fastest at a 36.84% CAGR as operators replace CRAC units with immersion tanks to maintain PUE below 1.15. Each GB200 NVL72 rack dissipates 132 kW, requiring facilities to implement 480 V backbones, 2N+1 UPS strings, and chilled-water loops rated for 45 °C inlet. These upgrades are expected to increase wallet share for switchgear and pumps.

Immersion cooling also allows higher supply-air temperatures in surrounding cold aisles, trimming fan energy and lifting overall facility efficiency. These gains explain why the Italy hyperscale data center market share for mechanical packages tied to liquid cooling is expected to eclipse legacy CRAC spend by 2028. Electrical infrastructure follows the same curve, as campuses add bus ducts and static transfer switches sized for 30 MW blocks to support staggered cloud availability zones.

By Tier Standard: Tier IV Accelerates On Fintech And Public-Sector Mandates

Tier III still accounted for 68.13% of the share in 2025, but fintech regulations are shifting investments toward Tier IV due to its 99.995% uptime guarantee. The Italy hyperscale data center market size for Tier IV halls is projected to grow at a 36.57% CAGR. This growth is driven by payment processors that must limit annual downtime to 1.6 minutes to comply with the Bank of Italy’s instant-payment law.

Aruba’s IT4 Rome facility, certified at ANSI/TIA-942 Rating 4, now hosts card-authorization and health-records platforms that previously sat in lower-tier halls. Although Tier IV commands a 30% capex premium, colocation models spread that uplift across multiple tenants, making monthly rents palatable for firms that would not build such redundancy alone. Consequently, Tier III facilities increasingly pivot toward CDN caches and batch analytics that can ride through brief outages, keeping both tiers viable within the Italy hyperscale data center market.

By Data Center Size: Mega-Scale Builds Amortize Fixed Costs

Facilities between 25-60 MW captured 43.64% of share in 2025. However, mega campuses above 60 MW are logging a 36.34% CAGR as hyperscalers chase lower per-MW build costs. Vantage’s 96 MW master plan near Milan demonstrates how early grid-capacity bookings and phased 32 MW blocks slash transformer, generator, and cooling overhead on a dollar-per-kilowatt basis.

Smaller sub-25 MW projects remain relevant for edge compute or sovereign clouds wary of co-tenancy. However, rising power densities and corporate PPAs favor campuses large enough to host on-site 50 MWh battery systems and switch between grid and renewable sources. Consequently, the Italy hyperscale data center market size for mega facilities is likely to surpass the large-facility bracket before the mid-forecast horizon.

Geography Analysis

Installed hyperscale capacity is heavily clustered in Lombardy and Lazio, which jointly accounted for roughly 70% of national megawatt inventory in 2025. Lombardy’s leadership stems from Milan’s MIX internet exchange, dense metro fiber rings and proximity to Italy’s banking core, conditions that let operators offer sub-2-millisecond round trips to corporate campuses while tapping 380 kV Terna substations for scalable power. AWS, Microsoft and Google all located new regions within a 30-kilometer arc of the city, reinforcing a virtuous loop of talent, fiber and investment.

Southern Italy is rising as an alternative thanks to Sparkle’s Unitirreno cable and abundant photovoltaic capacity across Sicily and Sardinia. Land near Palermo trades at half Milan prices, and PPAs below EUR 50 per MWh make operating costs attractive to AI startups targeting North African latency windows. Yet grid reinforcement lags demand, with only EUR 400 million committed to Sicilian upgrades versus EUR 2.1 billion for Lombardy, so large projects must budget for diesel or battery bridging until 2029 grid works arrive.

Secondary clusters are forming in Piedmont and Emilia-Romagna. Oracle’s Turin cloud region pulls workloads north-westward, leveraging Alpine hydropower and lower seismic risk, while Bologna’s CINECA supercomputer anchors an HPC corridor focused on automotive and life-science modeling. The Po Valley’s water-stress rules, however, prohibit new evaporative towers, nudging operators toward closed-loop liquid cooling that adds up to 20% to mechanical capex. Veneto and Friuli-Venezia Giulia attract edge builds for cross-border logistics, though fiber density remains insufficient for true hyperscale halls, keeping these regions in the sub-10 MW bracket of the Italy hyperscale data center market.

Analysis of the hyperscale data center market by Mordor Intelligence spans multiple other regional evaluations across Europe, North America, and Middle East, supported by country-level insights for Germany, Spain, United States, Saudi Arabia, Brazil, and Argentina, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The competitive field is bifurcating between global colocation specialists and domestic incumbents repositioning around sovereign-cloud demand. Vantage Data Centers and DATA4 collectively secured more than EUR 850 million for Milan-area campuses during 2024-2025, giving them first-mover scale in turnkey liquid-ready halls. AWS, Microsoft and Google dominate the self-build lane but increasingly lean on third-party campuses for satellite zones, blurring the once-clear line between wholesale and do-it-yourself footprints.

Local players such as Aruba, Retelit and Rai Way defend share by combining Gaia-X compliance, low PUE scores and proximity to government or media workloads. Aruba’s 2025 retrofit of cold-plate manifolds in Rome allowed it to accommodate H100 clusters months before GPU inventory flowed freely to Lombardy, illustrating how technology upgrades can offset scale disadvantages. Meanwhile, energy majors like Eni are entering with vertically integrated models that bundle real-estate, power and sustainability reporting, creating a new axis of competition rooted in megawatt self-sufficiency rather than whitespace volume.

Technology differentiation centers on cooling and monitoring stacks. Vertiv’s reference designs for NVIDIA’s GB200 NVL72 have become table stakes for campuses chasing AI tenants, while Schneider Electric’s EcoStruxure adds predictive maintenance layers that trim opex by automating valve positions and fan curves. Operators unable to document PUE below 1.20 face a two-tier rental market where sustainability-minded customers will pay up to 10% more for greener halls, accelerating obsolescence for facilities stuck on legacy air cooling.

Italy Hyperscale Data Center Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Meta Platforms Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Targa Telematics completed the migration of its fleet-management platform to Equinix’s ML5 Milan and FR4 Frankfurt campuses, using Equinix Fabric for sub-5-millisecond replication.

- January 2026: The Bank of Italy’s instant-payments mandate entered into force, pushing payment service providers into Tier IV halls with sub-5-millisecond latency to TIPS.

- November 2025: Oracle opened its second Italian cloud region in Turin, partnering with Telecom Italia for low-latency OCI delivery.

- October 2025: Sparkle activated the Unitirreno submarine cable that links Genoa, Palermo and Cagliari with 400 Gbps wavelengths.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italy hyperscale data center market as revenue generated from large-scale, single-tenant or multi-tenant facilities built or leased by cloud and digital platforms that provision at least 4 MW of contiguous IT load in one campus and feature highly automated, synchronized power and cooling systems. Capacity additions tied to international connectivity nodes around Milan, Turin, and Genoa are included in the scope.

Scope Exclusion: Edge sites under 4 MW, enterprise on-premises rooms, and containerized micro data centers are outside our coverage.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-Build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Units

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning Services

- Design Engineering

- Fire Detection, Suppression and Physical Security

- DCIM/BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By Data Center Size

- Large ( Less than or equal to 25 MW)

- Massive (Greater than 25 MW and Less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Desk Research

We initiated our work with published capacity registers from the Data Center Observatory, energy and emissions datasets from Terna, and installation approvals logged by Italy's Ministry of Enterprises and Made in Italy. Trade association white papers from CISPE and Italia Datacenter Association, customs imports of high-density racks (ITC HS 8471), and peer-reviewed cooling efficiency studies supplied foundational inputs. Commercial insights were refined with D&B Hoovers revenue splits, Dow Jones Factiva news runs, and Questel patent searches on liquid cooling manifolds. The sources noted illustrate, not exhaust, the secondary evidence base used throughout the exercise.

Primary Research

Mordor analysts interviewed power-utility planners, colocation development heads, cloud procurement leads, and equipment OEM engineers across Lombardy, Lazio, and Liguria. These discussions clarified lead-time bottlenecks, rack power road maps, and achievable price-per-kW ranges that desk work alone could not capture.

Market-Sizing & Forecasting

We began with a top-down reconstruction of hyperscale demand by rolling forward announced megawatt pipelines and historical utilization, then validated totals with bottom-up spot checks on supplier bookings and sampled average service prices per installed kilowatt. Key variables included grid connection lead time, average rack density, renewable energy share, hyperscaler cloud spending in Italy, inflation-adjusted construction costs, and Milan-to-FLAP-D spillover ratios. A multivariate regression model linked these drivers to achieved revenue, while scenario analysis adjusted for energy price volatility. Gaps in bottom-up estimates, such as undisclosed self-build costs, were bridged using benchmark ratios agreed upon during expert calls.

Data Validation & Update Cycle

Outputs pass through variance checks against national power statistics and colocation booking reports. Senior analysts review flagged anomalies before sign-off. According to Mordor Intelligence, every dataset is refreshed annually, with interim updates triggered by material events like hyperscaler site announcements or regulatory tariff shifts.

Why Our Italy Hyperscale Data Center Baseline Deserves Confidence

Published market values often vary because every firm chooses its own service bundles, geographic cut-offs, and forecast refresh cadence.

Key gap drivers include whether enterprise and edge facilities are folded in, whether investment or revenue is reported, exchange-rate timing, and if Milan alone or the full country is measured. Mordor's disciplined focus on >=4 MW facilities nationwide, yearly data sweeps, and price-weighted capacity modeling limits such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.45 B (2025) | Mordor Intelligence | - |

| USD 7.21 B (2024) | Global Consultancy A | Covers entire data center value chain, not only >=4 MW hyperscale sites |

| EUR 0.46 B (2024) | Industry Intelligence B | Measures Milan colocation revenue only, omits self-build and other regions |

In short, while other publishers swing wider or narrower, our Italy hyperscale baseline is anchored to clearly stated thresholds, validated cost metrics, and an update rhythm that keeps decision makers on firm ground.

Key Questions Answered in the Report

What is the projected Italy hyperscale data center market size by 2031?

The market size is forecast to reach USD 9.08 billion by 2031, up from USD 1.96 billion in 2026.

How large will hyperscale capacity in Italy get by 2031?

Installed capacity is expected to climb to more than 9 GW of critical load by 2031, in line with the USD 9.08 billion market value forecast.

Which Italian regions attract the most hyperscale investment?

Lombardy and Lazio together host about 70% of current megawatts thanks to dense fiber rings and proximity to enterprise clusters, while Sicily is emerging as a low-latency gateway to North Africa.

What cooling technologies are operators adopting for AI workloads?

Direct-to-chip liquid and immersion systems are replacing CRAC units, pushing power usage effectiveness below 1.15 and supporting rack densities above 60 kW.

Why is Tier IV demand rising in Italy?

Fintech firms must meet Bank of Italy instant-payment rules that cap downtime at 1.6 minutes per year, a level achievable only with Tier IV redundancy.

How are data-center builders securing electricity supply?

Developers reserve grid capacity up to two years in advance and increasingly lock ten-year solar or wind PPAs priced below EUR 50 (USD 56) per MWh.

Will GPU shortages continue to delay Italian AI clusters?

H100 and H200 inventories are still prioritized for Frankfurt, London, Amsterdam, Paris and Dublin, so Italian deployments could face another 6-9 months of lead-time friction before supplies normalize.

Page last updated on: