Mexico Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

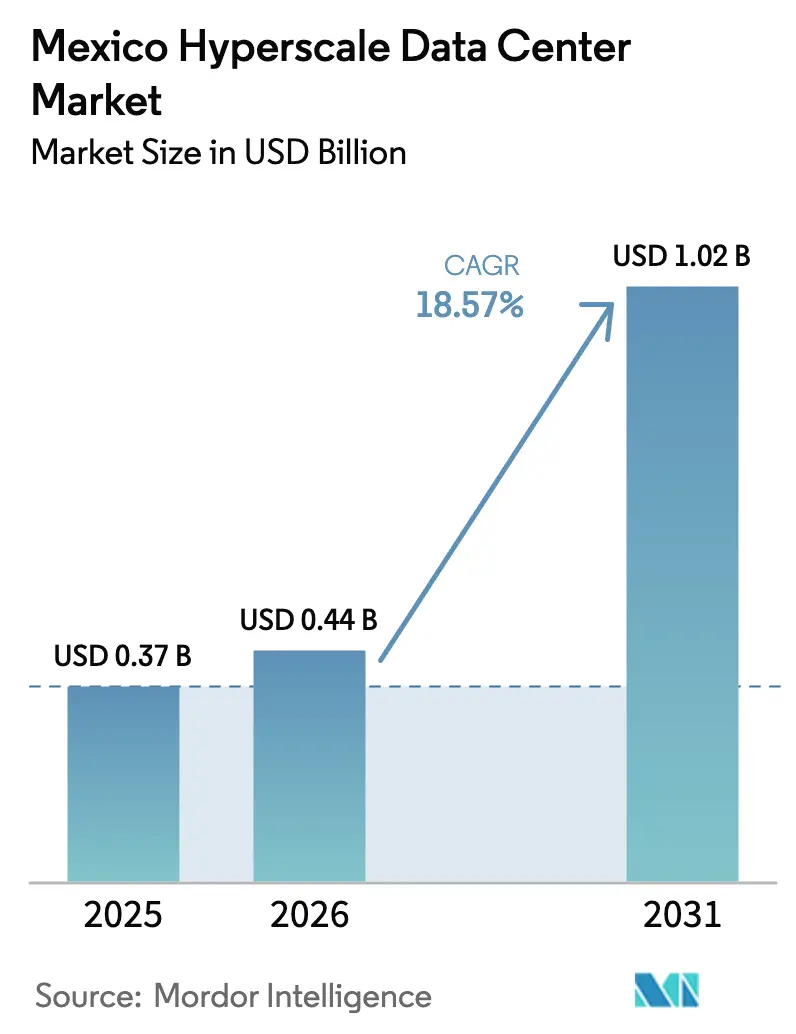

| Base Year Market Size (2025) | USD 0.37 Billion |

| Market Size (2026) | USD 0.44 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 18.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Hyperscale Data Center Market Analysis by Mordor Intelligence

The Mexico hyperscale data center market size was valued at USD 0.37 billion in 2025 and is estimated to grow from USD 0.44 billion in 2026 to reach USD 1.02 billion by 2031, at a CAGR of 18.57% during the forecast period (2026-2031). Mexico’s ascendance as a near-shoring venue for United States cloud growth, combined with shorter permitting cycles and lower real-estate costs, is accelerating hyperscale investment momentum. International cloud providers are pivoting to sovereign-cloud architectures that satisfy domestic data-residency mandates, while enterprises embrace hybrid infrastructure that blends on-premises workloads with low-latency colocation nodes. Rapid adoption of artificial-intelligence training clusters, mounting demand for Tier IV uptime to support real-time financial applications, and the emergence of multi-gigawatt campuses around Querétaro highlight the fundamental drivers guiding capital allocations. Competitive pressure from global real-estate investment trusts is compressing wholesale pricing and spurring service differentiation across connectivity, cooling, and renewable-energy procurement.

Key Report Takeaways

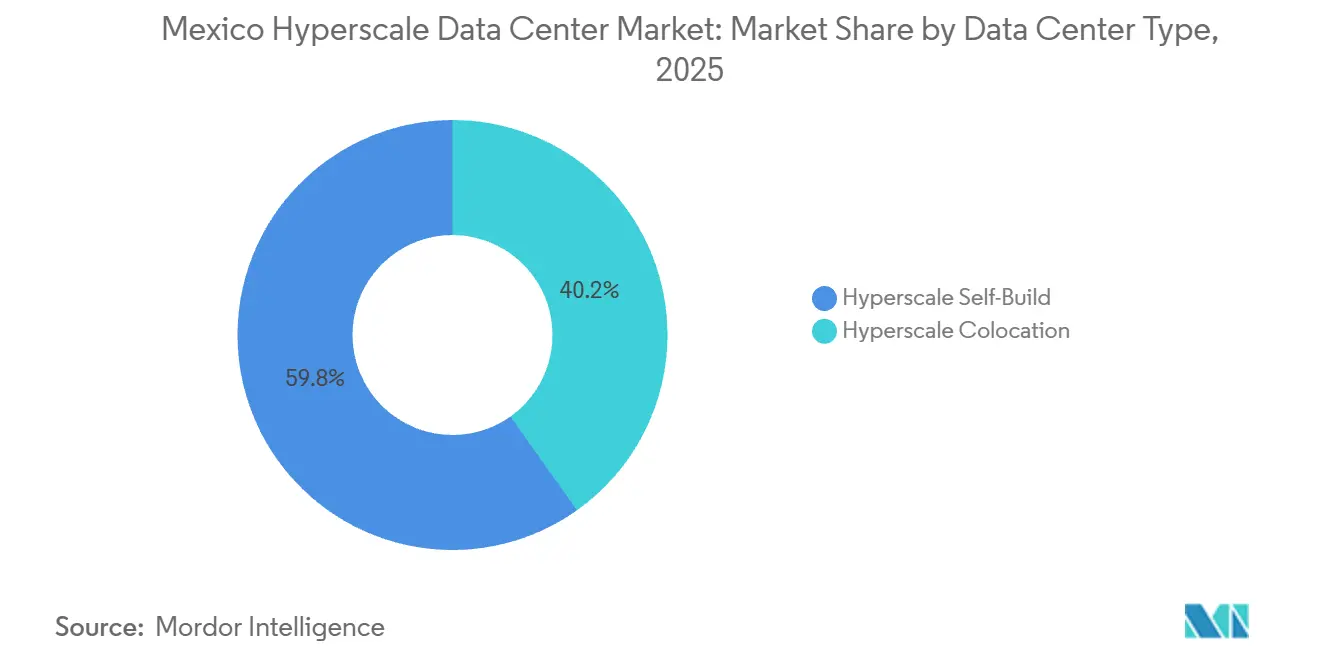

- By data center type, hyperscale self-build facilities led with 59.83% share in 2025, whereas hyperscale colocation is projected to expand at a 19.53% CAGR through 2031.

- By component, IT infrastructure accounted for 49.48% of share in 2025, while mechanical infrastructure is slated to grow at a 19.67% CAGR to 2031.

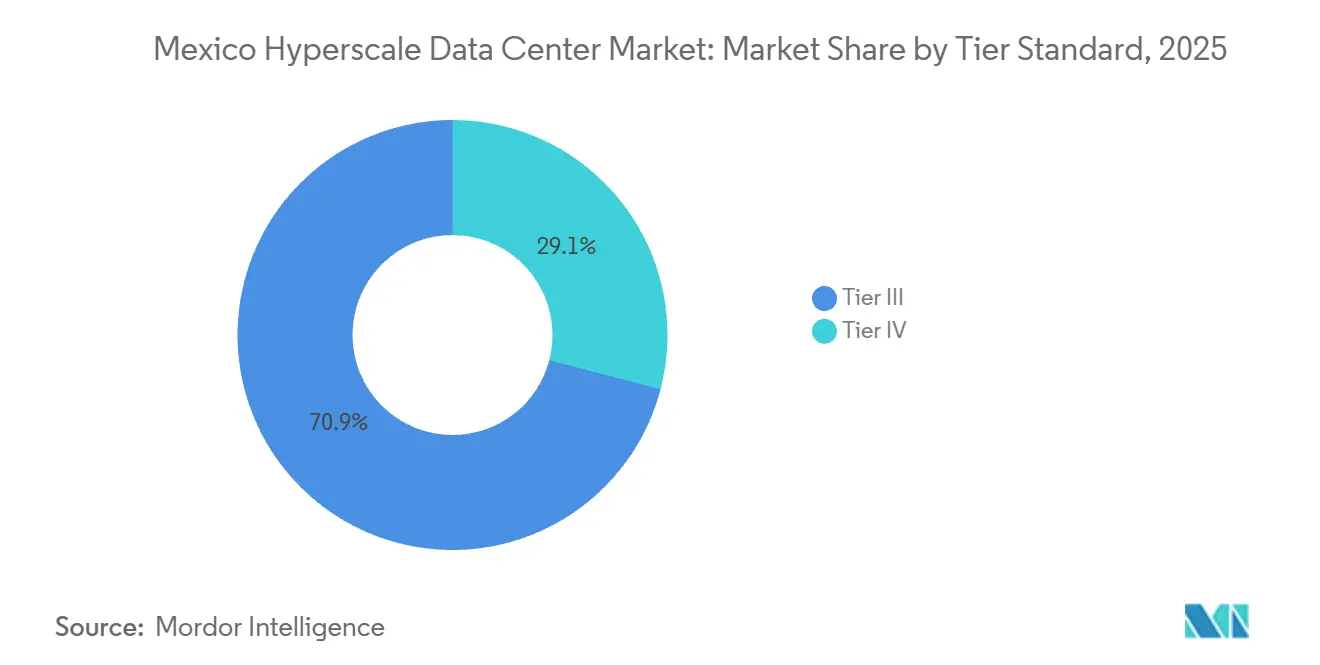

- By tier standard, tier III facilities held 70.94% share of the Mexico hyperscale data center market size in 2025, while tier IV builds are forecast to surge at a 19.75% CAGR through 2031.

- By data center size, massive facilities between 25 MW and 60 MW commanded 51.24% share in 2025, whereas mega campuses above 60 MW are on track for a 19.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Mexico includes both locally based firms and those operating across multiple regions. The market landscape in the global hyperscale data center industry research shows how these players are arranged internationally.

Mexico Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding GPU-Centric AI/ML Workloads (US Spill-Over) | +4.5% | Querétaro, Mexico City, Monterrey | Short term (≤ 2 years) |

| Sovereign-Cloud Roll-Outs by Hyperscalers | +3.8% | National, concentration in Querétaro | Medium term (2-4 years) |

| Real-Time Payment Mandates Driving Tier IV Builds | +3.2% | Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| 5G Edge-Core Consolidation Boosting Central Hubs | +2.5% | Central Mexico | Long term (≥ 4 years) |

| GenAI Inference Campuses Demanding Liquid-Cooling | +2.0% | Querétaro, Nuevo León | Short term (≤ 2 years) |

| Availability-Based Captive Renewable PPAs | +1.5% | National, early adoption in northern states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding GPU-Centric AI/ML Workloads (US Spill-Over)

United States hyperscalers are diverting 120 kW liquid-cooled racks into Mexican campuses to bypass land scarcity and lengthy environmental reviews north of the border, pushing operators in Querétaro to retrofit raised-floor halls with overhead coolant manifolds that exceed USD 2 million per megawatt. Foxconn’s local production of NVIDIA GB200 NVL72 systems shortens supply lead times from sixteen to six weeks, enabling faster revenue recognition for new halls. The Mexico hyperscale data center market therefore captures latency-sensitive AI training that requires proximity to U.S. model repositories yet benefits from lower real-estate costs. Higher rack densities triple power draw per square foot, compressing project payback periods even as construction budgets rise. The 4.5-percentage-point uplift on CAGR reflects this rapid densification wave.

Sovereign-Cloud Roll-Outs by Hyperscalers

Mexico’s National AI Strategy obliges public-sector data to remain inside the country, prompting AWS, Microsoft, and Oracle to open domestic regions that guarantee residence, encryption, and auditing compliance.[1]Secretaría de Economía, “National AI Strategy,” gob.mx AWS activated three availability zones in Querétaro during early 2025 and committed an additional USD 5 billion for expansion through 2028.[2]Amazon Web Services, “AWS Mexico Region Launch,” aws.amazon.com Microsoft is investing USD 1.3 billion across Azure Stack Edge nodes at Equinix and KIO sites to serve regulated workloads while allowing analytics to burst into U.S. clouds. Oracle’s Monterrey region underpins PEMEX seismic-data processing that cannot tolerate cross-border latency. These sovereign-cloud initiatives lock multiyear revenue streams, adding a 3.8-percentage-point CAGR contribution to the Mexico hyperscale data center market.

Real-Time Payment Mandates Driving Tier IV Builds

Banco de México’s CoDi platform processed 1.2 billion instant transactions in 2025, compelling financial institutions to pursue 99.995% infrastructure availability that only Tier IV designs can deliver. BBVA México and Citibanamex migrated core banking systems into Equinix MX2 and KIO MEX6 pods that feature dual utility feeds, rotary UPS, and 72-hour fuel reserves. Supply remains constrained, with just eight certified Tier IV buildings nationwide, pushing wholesale rates 40% above Tier III. Digital banking penetration is forecast to climb from 52% in 2024 to 68% in 2028, ensuring sustained demand for mission-critical colocation. This regulatory tailwind adds 3.2 percentage points to forecast CAGR for the Mexico hyperscale data center market.

5G Edge-Core Consolidation Boosting Central Hubs

América Móvil has collapsed two-hundred 50 kW micro-edge sites into twelve 5 MW regional hubs, citing 35% lower fiber backhaul costs and simplified operations. Querétaro’s intersection of the Bajío industrial corridor and Mexico City metro provides sub-20 millisecond round-trip times for autonomous-vehicle telemetry and AR streaming workloads. AT&T’s similar U.S. strategy validates the efficiency gains of consolidation. Carrier-neutral colocation with dense interconnection is therefore favored over scattered edge shelters, driving additional occupancy in Central Mexico. The trend supports a 2.5-percentage-point uplift in the Mexico hyperscale data center market CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-Usage Restrictions on Evaporative Cooling | -2.8% | Mexico City, Querétaro, Guadalajara | Short term (≤ 2 years) |

| GPU/Optic Supply-Chain Bottlenecks | -2.2% | National | Short term (≤ 2 years) |

| Rising Carbon Levies and Heat-Tax Proposals | -1.5% | National | Medium term (2-4 years) |

| Local-Grid Curtailment Caps > 30 MW | -1.8% | Querétaro, Mexico City | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water-Usage Restrictions on Evaporative Cooling

CONAGUA suspended new evaporative-tower permits in early 2025 because aquifer depletion exceeds natural recharge by 40%, pushing operators toward closed-loop liquid chillers that inflate capital costs by 30% and elevate PUE from 1.3 to 1.5. KIO paused the 8 MW MEX7 expansion pending clarity on recycled-water credits, illustrating near-term supply constraints. Smaller incumbents that cannot finance retrofits face margin erosion because legacy enterprise contracts restrict passthrough pricing. The -2.8 percentage-point drag reflects the operating-expense surge at facilities that previously relied on low-cost evaporative cooling.

GPU/Optic Supply-Chain Bottlenecks

October 2024 export controls extended NVIDIA H100 lead times to twelve months, delaying activation of pre-leased halls at ODATA’s campus and forcing phased commissioning through 2029. Simultaneously, 800 GbE switch backlogs at Broadcom and Marvell reach nine months because of constrained 3 nm wafer capacity, throttling AI fabric deployment. U.S. sites receive priority shipments, leaving Mexican projects dependent on secondary allocations that arrive six months later, erasing cost arbitrage. The constraint subtracts 2.2 percentage points from CAGR for the Mexico hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Captures Flexibility Premium

Colocation’s 19.53% CAGR through 2031 outpaces self-build growth because enterprises value rapid deployment, interconnection density, and modular power increments. Equinix’s platform, which aggregates more than 2,900 networks, reduces cross-connect latency to under one millisecond, a feature prized by high-frequency trading desks and advanced analytics workloads. In 2025 hyperscale self-builds still commanded 59.83% of market share in 2025, because AWS, Meta, and Microsoft seek proprietary cooling and power architectures for 120 kW racks. Yet the Mexico hyperscale data center market increasingly rewards asset-light leasing models that prevent capital lock-in while preserving performance. KIO’s build-to-suit pods at QRO2 replicate self-build economics, ensuring anchor tenants can scale down during demand troughs without carrying stranded assets.

Colocation providers amortize Tier IV redundancy across multi-tenant halls, spreading USD 15 million in dual-feed investments across dozens of clients and lowering the entry hurdle for regulated industries. Digital Realty’s 3 MW pre-lease with BBVA at its forthcoming Monterrey site exemplifies how financial institutions are shifting away from proprietary buildings toward managed hybrid-cloud environments that bundle orchestration, security controls, and renewable-energy procurement. Self-build operators, facing GPU scarcity and rising debt costs, are re-evaluating ownership strategies, particularly where the Mexico hyperscale data center market size could warrant redeploying capital into AI model research rather than concrete and steel.

By Component: Liquid-Cooling Retrofits Propel Mechanical Infrastructure

IT infrastructure dominated 49.48% of share in 2025, as servers, storage, and switching formed the compute fabric for AI workloads. Mechanical systems now represent the fastest-growing slice, advancing at 19.67% CAGR because operators must upgrade air-cooled halls to support direct-to-chip cold plates for GB200 NVL72 clusters. Vertiv’s modular coolant distribution units at ODATA reject 2 MW of heat each, enabling staggered retrofit schedules that keep existing tenants online.[3]Vertiv, “High-Density Liquid-Cooling Modules,” vertiv.com The Mexico hyperscale data center market therefore channels incremental dollars into pumps, manifolds, and rear-door exchangers rather than into bare-metal servers.

Electrical infrastructure follows close behind, growing 18.2% annually as Tier IV builds demand 2N UPS, rotary flywheels, and fault-tolerant switchgear. Eaton’s 93PM UPS series, rated 97% efficient in double-conversion mode, reduces power losses when coupled with dynamic-diesel generators that spin up within eight seconds. Construction software such as Schneider Electric EcoStruxure provides predictive analytics that shrink mean-time-to-repair by 40%, translating operational savings into lower tenant bills. Storage capex moderates because NVMe flash arrays compress physical footprints, allowing operators to reuse freed-up white space for GPU dense nodes. The Mexico hyperscale data center industry increasingly views cooling as core intellectual property, not ancillary plant, changing procurement priorities across the component stack.

By Tier Standard: Mission-Critical Loads Propel Tier IV Expansion

Tier III still captures 70.94% of share in 2025 because large-language-model pre-training and video rendering workloads can checkpoint progress and tolerate brief outages. Tier IV, however, accelerates at 19.75% CAGR as real-time payments, tele-health diagnostics, and securities clearing platforms demand concurrent maintainability. CoDi’s requirement for 99.995% uptime translates into no more than 26 minutes of annual downtime, a threshold unreachable for Tier III buildings, which average 1.6 hours. Wholesale pricing reflects scarcity, at USD 185 per kW per month against USD 130 for Tier III halls. The Mexico hyperscale data center market size will tilt further toward Tier IV by late-decade as healthcare and fintech regulators codify zero-downtime rules.

Cost differentials stem from dual substations, rotary UPS, and seismically rated envelopes that add roughly USD 8 million to every 10 MW block. Equinix and KIO differentiate by offering Tier IV suites inside otherwise Tier III campuses, giving tenants optionality on risk versus price. For AI training clusters, operators still prioritize lowest dollar per GPU hour, maintaining Tier III as the workhorse in Querétaro where land and power are inexpensive. Hence the Mexico hyperscale data center market share will split along workload criticality, with mission-critical loads gravitating to Tier IV city-center pods and batch AI workloads defaulting to sprawling Tier III campuses.

By Data Center Size: Mega-Campuses Centralize South America Workloads

Facilities between 25 MW and 60 MW led the market in 2025, accounting for 51.24% of the market share because they optimize capital efficiency while supporting modular expansion. Mega campuses exceeding 60 MW, typified by CloudHQ’s 900 MW blueprint at El Marqués, will grow at 19.46% CAGR as hyperscalers collapse former edge nodes into concentrated hubs along the Laredo-Mexico City fiber corridor. Construction economies of scale drop build costs to USD 8 million per MW, versus USD 12 million for sub-25 MW halls, allowing aggressive pricing strategies to lure anchor tenants. The Mexico hyperscale data center market is therefore pivoting to fewer, larger compounds that aggregate compute for generative-AI inference, telemetry ingestion, and content distribution.

Large facilities under 25 MW continue to satisfy regional and enterprise needs, particularly in Guadalajara and Puebla where land is 60% cheaper but connectivity still lags by two years. Prefabricated data halls at ODATA’s 300 MW campus can be commissioned in nine months, half the time of traditional builds, lending speed-to-market advantages that outweigh higher capital intensity. EdgeConneX and Neutral DC focus on sub-20 MW shells to avoid grid-curtailment caps, targeting customers that value proximity over economies of scale. These dynamics ensure the Mexico hyperscale data center market maintains a multi-tier landscape where mega campuses host AI megawatts while smaller halls address latency-sensitive industrial IoT and content-delivery workloads.

Geography Analysis

Querétaro, Mexico City, and Monterrey jointly represented about 78% of installed capacity in 2025, cementing Central Mexico as the epicenter of the Mexico hyperscale data center market. Querétaro alone amassed nearly USD 8 billion of cumulative investment because municipal fast-track permits shorten construction timelines to six months, while its moderate seismic profile reduces structural premiums. Dual CFE substations tap 400 kV lines that ensure stable delivery for multi-hundred-megawatt campuses, and north-south fiber trunks provide sub-30 millisecond latency into Texas cloud regions. Mexico City retains roughly 25% share due to in-city data-residency mandates for government and banking, although water-use restrictions and grid caps have slowed new permits, creating tight supply that forces tenants to pay premium rates.

Monterrey is emerging as the third pole for cross-border hybrid clouds, helped by proximity to U.S. manufacturing zones and the availability of industrial land parcels with pre-approved utility connections. Oracle’s planned region and Equinix’s MO2 facility demonstrate growing hyperscale appetite in Nuevo León, pushing the Mexico hyperscale data center market toward a tri-cluster model that balances regulatory compliance with disaster-recovery separation. Secondary cities such as Guadalajara and Puebla dangle land prices 60% below Querétaro and access to cheap renewable PPAs priced at USD 35 per MWh, but fiber backhaul deficits extend commissioning by six to nine months, dampening immediate hyperscale enthusiasm.

Southern states including Oaxaca and Chiapas command less than 2% capacity because unreliable grids, high seismic risk, and limited fiber conduits inflate build costs by 25%. The National Digital Inclusion Strategy commits USD 500 million to extend fiber into underserved regions, but completion stretches to 2029, deferring meaningful hyperscale expansion. Coastal cities such as Veracruz are attracting specialty disaster-recovery pods that leverage submarine cable landings for Caribbean connectivity. Geographic fragmentation thus persists, with hyperscalers favoring speed-to-market and infrastructure readiness over low land costs, ensuring that the Mexico hyperscale data center market remains anchored in Central and Northern corridors through the forecast horizon.

Mordor Intelligence tracks the hyperscale data center market across other major regions such as Asia, Europe, and North America, with additional country-level coverage spanning Argentina, Chile, Malaysia, Poland, Netherlands, and France, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Mexico hyperscale data center market exhibits moderate concentration, with AWS, Microsoft, Equinix, KIO Networks, and ODATA jointly controlling about 62% of installed megawatts during 2025. International colocation REITs Digital Realty, CyrusOne, and STACK Infrastructure are entering to capture overflow demand from U.S. hubs, compressing wholesale pricing in Querétaro by roughly 12% year over year. Equinix differentiates through unrivaled interconnection ecosystems, hosting nearly 2,900 networks inside its Mexican sites, and underpinning multicloud routing for financial services, media streaming, and gaming workloads. KIO’s land-and-expand strategy, which deploys modular suites that anchor hyperscalers then backfill enterprise tenants, lifted QRO2 to 85% utilization within six months of opening, evidencing strong demand elasticity.

White-space opportunities revolve around Tier IV colocation and liquid-cooling retrofits, where less than one-third of installed capacity currently meets AI thermal requirements. Vertiv, Schneider Electric, and Siemens compete to supply DCIM software that promises 15% energy-efficiency gains via predictive control loops. Layer 9 and Neutral DC target Guadalajara and Puebla, banking on lower land costs and generous state-level incentives, but commissioning risk remains elevated until fiber densifies. Uptime Institute’s M&O stamp is fast becoming a prerequisite for hyperscaler leasing, lengthening the certification runway for newcomers that lack operational maturity.

Strategic partnerships are flourishing: Microsoft aligns with Equinix for Azure ExpressRoute nodes, Oracle pairs with América Móvil for last-mile 5G backhaul, and AWS contracts with ODATA to secure dual-region redundancy. Defensive responses include price-indexed leases tied to power-usage effectiveness to maintain margins amid input-cost volatility. As GPU allocation, not land, becomes the scarcest asset, operators are evolving toward compute-as-a-service models that ship capacity wherever chips arrive first, thereby reshaping landlord-tenant dynamics within the Mexico hyperscale data center market.

Mexico Hyperscale Data Center Industry Leaders

Amazon Web Services, Inc. (AWS)

Microsoft Corporation

Google LLC

Digital Realty Trust Inc.

KIO Networks SAPI de CV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: CoreWeave secured USD 2 billion from NVIDIA to scale GPU-as-a-service infrastructure toward 5 GW global capacity.

- December 2025: KIO Networks inaugurated the 12 MW QRO2 facility in Querétaro, lifting regional footprint to 19 MW.

- November 2025: Equinix introduced managed-service bundles that integrate colocation, interconnection, and remote-hands support across Mexican sites.

- September 2025: KIO Networks earmarked USD 400 million for Latin American expansion, including Guatemala and potential Colombian sites.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Mexico's hyperscale data center market as all newly built or fully leased facilities that exceed 20 MW of IT load and are owned or long-term leased by major cloud and digital service providers; revenue reflects capital investment plus first-fill IT equipment and critical infrastructure services.

Scope exclusion: colocation halls serving multiple tenants, edge pods below 5 MW, and managed on-premise server rooms are outside this valuation.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-Build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Units

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commissioning Services

- Design Engineering

- Fire Detection, Suppression and Physical Security

- DCIM/BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By Data Center Size

- Large ( Less than or equal to 25 MW)

- Massive (Greater than 25 MW and Less than equal to 60 MW)

- Mega (Greater than 60 MW)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed facility engineers, regional utility planners, and cloud procurement leads across Queretaro, Mexico City, and Guadalajara. These discussions validated construction timelines, rack densities, and average selling prices, and they clarified local grid connection bottlenecks that rarely appear in documents.

Desk Research

We collated baseline signals from open sources such as Mexico's Secretaria de Energia power capacity releases, Instituto Federal de Telecomunicaciones spectrum filings, import-export shipment records from Volza, and data center land bank disclosures filed with CNBV. Trade associations like CANIETI and global cloud service environmental reports enriched our understanding. Select paywalled datasets, D&B Hoovers for hyperscale balance sheet clues, Dow Jones Factiva for project pipelines, and Marklines where automotive AI loads intersect, added depth. The sources cited illustrate our approach; many additional references informed model calibration.

Market-Sizing & Forecasting

We begin with a top-down reconstruction of hyperscale CAPEX using Secretaria de Hacienda building permit values, cross-checked against power connect approvals and average $/MW benchmarks. Supplier roll-ups of switch gear shipments and sampled GPU rack ASP × volume provide a bottom-up sense check before totals are adjusted. Key variables like grid interconnection queue, sovereign cloud mandates, AI GPU uptake, PPA renewable premiums, and exchange rate paths drive the model. Multivariate regression on these inputs, supplemented by ARIMA to smooth cyclical build waves, underpins forecasts through 2031.

Data Validation & Update Cycle

Outputs undergo variance scans versus satellite imaged construction footage and CBRE quarterly absorption data; anomalies trigger re-interviews before senior review. Models refresh annually, with interim updates when energy policy or hyperscaler CAPEX announcements materially shift the outlook.

Why Our Mexico Hyperscale Data Center Baseline Commands Reliability

Published estimates often diverge because firms mix hyperscale builds with colocation halls, apply different ASP ladders, or freeze exchange rates at publication.

Key gap drivers include wider scope (others add enterprise and edge sites), aggressive roll forward of global GPU cost curves without Mexico specific checks, or infrequent refresh cycles that miss 2024 power quota caps. Mordor's disciplined geographic scoping, dual path validation, and annual refresh cadence mitigate these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.37 B (2025) | Mordor Intelligence | - |

| USD 2.38 B (2023) | Global Consultancy A | Includes colocation and enterprise builds; limited Mexico field verification |

| USD 5.18 B (2023) | Regional Consultancy B | Rolls hardware, software and services together; top down LATAM allocation |

| USD 2.5 B (2023) | Trade Journal C | Conservative estimate from aggregated press releases; no IT load normalization |

In sum, Mordor Intelligence delivers a balanced, transparent baseline rooted in Mexico specific permits, power data, and stakeholder insights, giving decision makers a figure they can confidently trace and replicate.

Key Questions Answered in the Report

What is the forecast value of the Mexico hyperscale data center market by 2031?

The market is projected to reach USD 1.02 billion by 2031, growing at an 18.57% CAGR from 2026 to 2031.

Which Mexican city currently hosts the largest cluster of hyperscale campuses?

Querétaro leads, accounting for the majority of announced multi-hundred-megawatt projects and attracting USD 8 billion of cumulative investment by 2025.

Why are Tier IV facilities gaining momentum in Mexico?

Real-time payment regulations and other mission-critical workloads require 99.995% availability, achievable only with Tier IV concurrent-maintainability designs.

How are water restrictions affecting data center design in Mexico?

CONAGUA's halt on new evaporative towers forces operators to adopt closed-loop liquid chillers, raising capital and operating costs and impacting project timelines.

What component category is growing the fastest within Mexican hyperscale builds?

Mechanical infrastructure, especially liquid-cooling systems and distribution manifolds, is expanding at 19.67% CAGR as operators retrofit for 120 kW AI racks.

Which providers dominate interconnection services in Mexico?

Equinix remains the leader, hosting over 2,900 networks and offering AWS Direct Connect and Azure ExpressRoute across its national footprint.

Page last updated on: