Spain Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

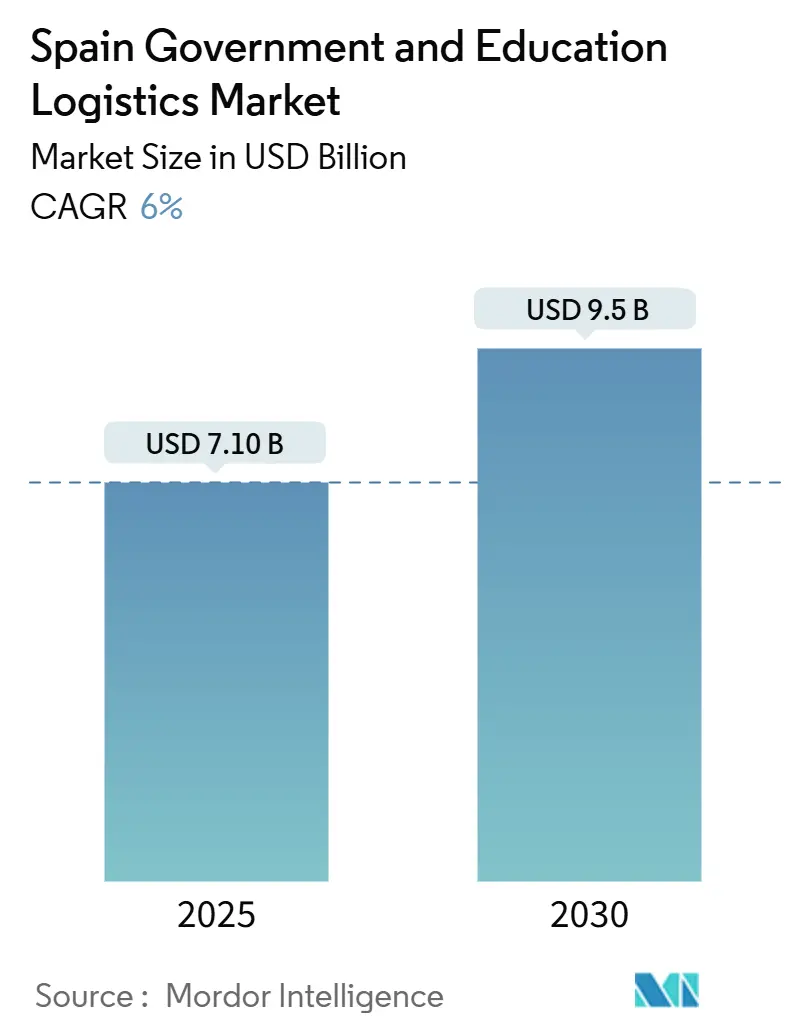

| Market Size (2025) | USD 7.10 Billion |

| Market Size (2030) | USD 9.5 Billion |

| Growth Rate (2025 - 2030) | 6.00% CAGR |

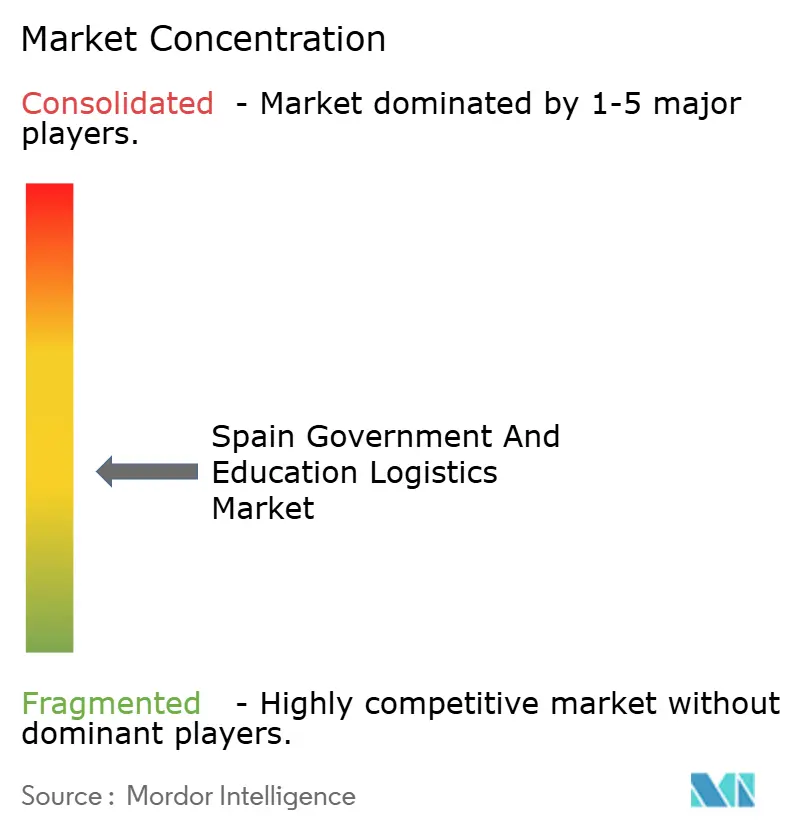

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Government And Education Logistics Market Analysis by Mordor Intelligence

The Spain Government And Education Logistics Market size is estimated at USD 7.10 billion in 2025, and is expected to reach USD 9.5 billion by 2030, at a CAGR of 6% during the forecast period (2025-2030).

Spain’s SIMPLE platform, mandatory eFTI documentation, and zero-emission delivery zones collectively accelerate contract cycles, favor value-added services, and reward providers able to integrate data-driven route optimization. Investments tied to the Recovery and Resilience Facility funnel capital toward multimodal hubs and campus micro-fulfillment centers, while smart-locker networks across universities shave last-mile inefficiencies. Providers differentiate through compliance readiness, secure document handling, and cold-chain reach, widening the gap between technology-intensive operators and traditional carriers. International entrants inject fresh capacity, yet regional specialists retain an edge where dense public-sector lanes intersect with localized regulatory know-how, especially for rural school-meal routes.

Key Report Takeaways

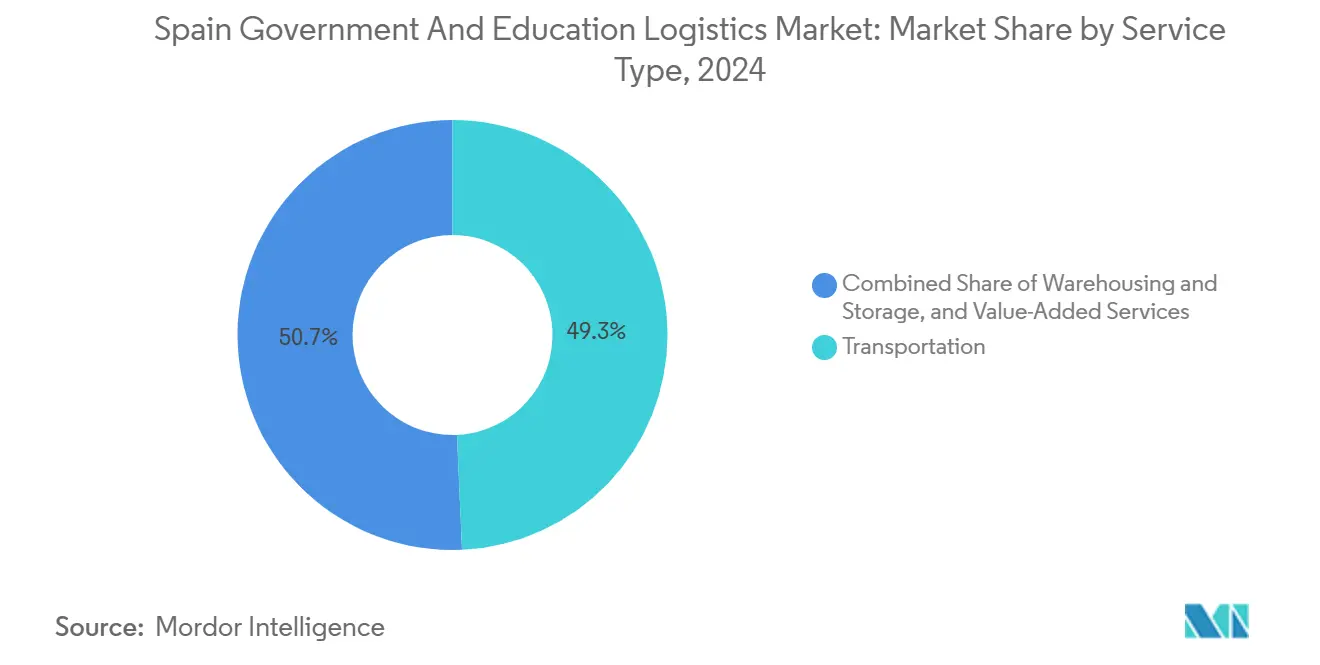

- By service type, transportation held 49.3% of Spain government and education logistics market share in 2024 and underpins public-sector distribution flows.

- Value-added services are projected to register an 8% CAGR through 2030, outpacing all other offerings as universities shift toward bundled outsourcing contracts.

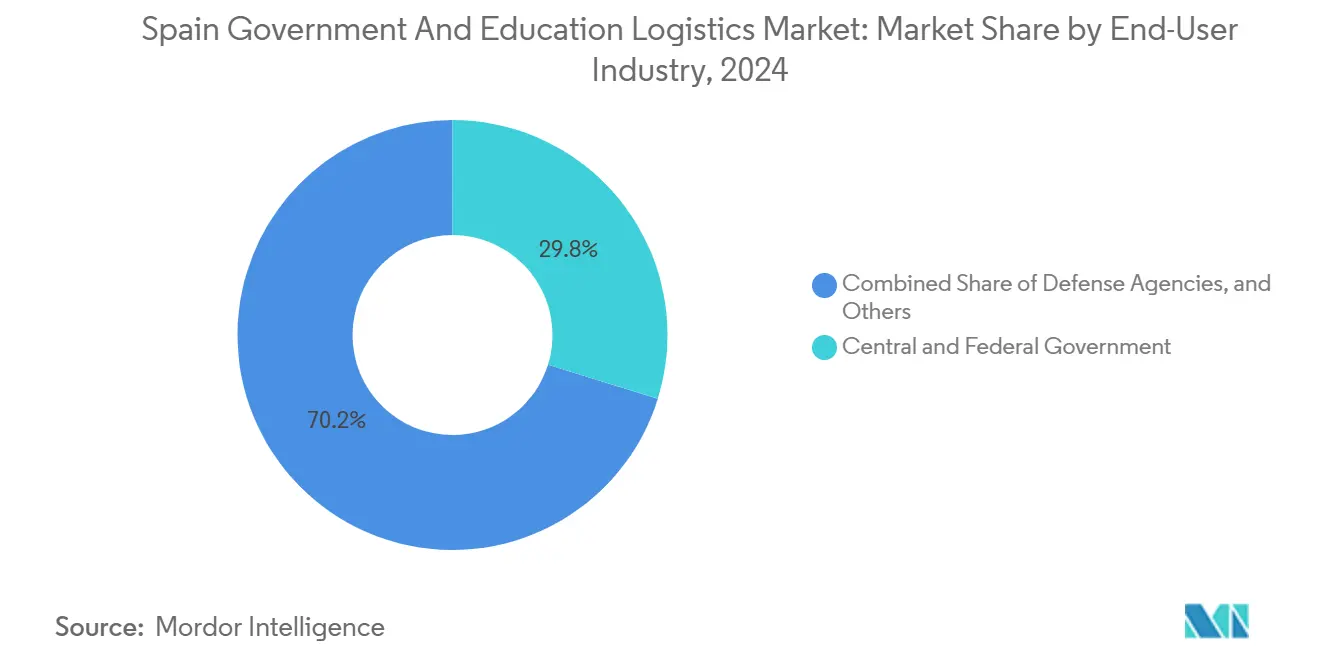

- Central and federal government agencies led with 29.8% share in 2024, whereas higher education institutions are forecast to grow at a 6.9% CAGR through 2030.

Future direction is shaped by developments occurring across multiple countries and regions, with Spain contributing to the overall trajectory. The outlook on worldwide government and education logistics market reflects how these are expected to evolve collectively.

Spain Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitization of public-sector procurement | +1.8% | Madrid, Barcelona, Valencia | Short term (≤ 2 years) |

| EU Recovery Plan funding | +1.5% | National; industrial corridors | Medium term (2-4 years) |

| Green last-mile mandates | +1.2% | Madrid and Barcelona urban zones | Medium term (2-4 years) |

| Smart-locker roll-out on campuses | +0.8% | University cities | Short term (≤ 2 years) |

| University outsourcing to 3PLs | +0.9% | Major academic regions | Long term (≥ 4 years) |

| Micro-hubs in government buildings | +0.6% | Administrative centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digitization of Public-Sector Procurement and Logistics Platforms

SIMPLE processed USD 49 billion worth of contracts in 2024, up 35% year on year, showing government buyers’ pivot toward fully online tendering. Bid preparation time dropped 40% once ESPD integration went live, letting smaller regional providers compete for Spain government and education logistics market contracts that once favored incumbents. Contract award cycles now close 25% faster, translating to prompt deployment of fleet resources during semester peaks. Providers must therefore showcase cybersecurity credentials, API connectivity, and eFTI-ready data flows or risk exclusion from high-value public tenders[1]“SIMPLE – Sistema de Información de Contratación Pública,” Ministry of Finance, administracion.gob.es .

EU Recovery Plan Funding for Logistics Infrastructure

Spain secured USD 21.3 billion for logistics corridors, of which 37% targets climate objectives, obliging contractors to electrify fleets and install renewable-powered depots. Eighteen new hubs broke ground in 2024, positioning multimodal nodes within a day’s reach of Andalusia’s and Catalonia’s university clusters. Early impact assessments indicate 15-20% last-mile cost reduction once consolidation centers open, bolstering provider margins within the Spain government and education logistics market[2]“Spain’s Recovery and Resilience Plan,” European Commission, ec.europa.eu.

Green Last-Mile Mandates for Urban Deliveries

Madrid’s expanded zero-emission zone and Barcelona’s parallel restrictions oblige carriers serving 68 government buildings and 23 campuses to deploy electrified vehicles starting 2025. SEUR allocated USD 27 million for electric vans dedicated to public-sector accounts, partially offsetting an 8-12% pickup in compliance costs through lower fuel spend and favorable tender scoring. Packaging must be recyclable, nudging providers to integrate circular-economy loops.

Smart-Locker Roll-out on University Campuses

Over 200 smart lockers installed in 2024 cut failed deliveries by 60% at universities such as Barcelona and Complutense, shrinking package-handling costs 40% and freeing facility staff for higher-value tasks. Lockers interface with campus ERP systems, delivering time-stamped chain-of-custody data critical to exam-paper security within the Spain government and education logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy multi-tier procurement cycles | -1.4% | National; stronger in smaller municipalities | Long term (≥ 4 years) |

| Regional budget austerity | -1.1% | Rural autonomous communities | Medium term (2-4 years) |

| Rural cold-chain gaps | -0.7% | Castilla-La Mancha, Extremadura | Medium term (2-4 years) |

| Driver shortages in ageing regions | -0.6% | Low-density areas nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Multi-Tier Procurement Approval Cycles

Contracts averaging USD 543,000 still take 18 months from tender to service start because of three-layer approvals and, for universities, senate validation when the value exceeds USD 109,000. Seasonal peaks textbook rush or fiscal year end are vulnerable to such lags, inflating project costs 12-15% through idle resources[3]“Circular Economy Strategy 2030,” Ministry of Ecological Transition Spain, miteco.gob.es.

Regional Budget-Austerity Limits on Logistics Spend

Twelve of Spain’s 17 regions cut discretionary spend 8% in 2024, trimming delivery frequency to remote public offices and shrinking route density. Smaller 3PLs feel margin compression, nudging consolidation as they exit unprofitable rural lanes[4]“Higher Education Statistics 2024,” Spanish University System Report, educacion.gob.es .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Drives Market Foundation

Transportation controlled 49.3% of the Spain government and education logistics market share in 2024 thanks to Spain’s 17,000-kilometer highway spider web linking 8,131 municipalities. Road freight handles 85% of public-sector consignments while high-speed rail corridors shuttle overnight priority documents between Madrid, Barcelona, and Valencia. Airfreight bridges mainland ministries with the Balearic and Canary Islands within 24 hours, yet volume remains niche and cost sensitive. Sea lanes serve bulk textbook imports through Valencia and Algeciras ports then feed inland warehouses.

Value-added services, the fastest-growing slice at an 8% CAGR, bundle inventory management, specialized packaging, and reverse logistics mandated by Spain’s Circular Economy Strategy 2030. Contract clauses now embed KPIs for electronic waste take-back and data-secure asset disposal, areas where technology-oriented 3PLs monetize expertise. Warehousing and storage maintain steady growth, absorbing procurement’s seasonal lumpiness and increasing campus micro-hub stockpiling.

By End-User: Government Agencies Lead Market Demand

Central and federal entities accounted for 29.8% of 2024 revenue, coordinating distribution to 52 provincial delegations from Madrid hubs. State and local governments trail closely, especially for health-service supplies and infrastructure parts. Defense agencies exercise premium pricing power on secure routes requiring vetted personnel and tamper-evident containers.

Higher-education institutions are the fastest-rising customer group, expanding at a 6.9% CAGR to 2030 on the back of double-digit international enrolment growth and rising research equipment inflows. K-12 public education depends on the national meal scheme that moves daily rations to 28,000 schools, sustaining predictable cold-chain demand cycles. A residual “Others” category—judicial courts and cultural archives—pursues high-security document logistics, supporting niche specialists.

Geography Analysis

Madrid anchors 35% of 2024 spend because national ministries cluster downtown and three flagship universities serve 300,000 students. Logistics corridors radiate from the A-2 and A-5 highways, offering same-day coverage to 50% of Spain’s population. Catalonia holds 22% share, with Barcelona’s port and the AP-7 corridor funneling supplies to 12 universities and cross-border Erasmus exchanges. The Barcelona-Girona belt gains extra demand from diplomatic freight bound for France.

Andalusia is forecast to post a 7.2% CAGR, buoyed by a USD 3 billion modernization push adding smart classrooms and lab complexes, each requiring sensitive equipment deliveries. Seville and Malaga work as spokes feeding secondary campuses through regional consolidation depots.

Valencia, the Basque Country, and Galicia deliver steady mid-single-digit expansion thanks to port connectivity, industrial density, and research grants. Rural provinces see logistics spend diluted by sparse populations and winding roads; per-package costs run 40% above urban baselines. Cohesion-fund allocations of USD 4.6 billion through 2027 assign 15% to rural connectivity fixes, promising to narrow the urban-rural service gap.

Analysis of the government and education logistics market by Mordor Intelligence spans multiple other regional evaluations across Europe, North America, and Middle East, supported by country-level insights for France, Russia, Canada, United Kingdom, Mexico, and China, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The Spain government and education logistics market is moderately fragmented; the top five operators held roughly 45% revenue in 2024, leaving scope for middle-tier and local specialists. Correos leverages its universal-service mandate and blockchain-backed Digital Government Services platform to win secure correspondence streams. SEUR exploits its local depot mesh and newly electrified fleet to align with zero-emission mandates. DHL’s USD 163 million capacity expansion pushes automated sorting efficiencies that cut turnaround on classified documents by 60%.

Domestic challenger Logista bundles textbook distribution with e-commerce returns, while GLS leads on metropolitan electrification. Kuehne + Nagel, GEODIS, and XPO Logistics seek beachheads via value-added campus solutions such as AI route planning. Entry barriers center on eFTI compliance, ISO 27001 security credentials, and cold-chain certification, tilting the playing field toward capital-rich incumbents yet still leaving niches—rural school-meal runs, judicial sealed-bag delivery—for agile regionals.

White-space potential exists in micro-fulfillment lockers inside administrative buildings, closed-loop haul-back of refurbished IT gear, and 24/7 campus parcel terminals. Competitive dynamics favor hybrid strategies that combine scale efficiencies with vertical specialization.

Spain Government And Education Logistics Industry Leaders

Correos

SEUR (DPDgroup)

DHL Group

Grupo Logista

GLS Spain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: DHL completed a USD 163 million network expansion, adding secure sorters in Madrid, Barcelona, and Seville to lift public-sector capacity 60%.

- February 2025: Correos rolled out a blockchain-enabled Digital Government Services platform, cutting document processing time 45% for 2 million items monthly.

- January 2025: SEUR bought three Andalusian regionals for USD 92 million, bolstering rural reach with 150 additional vehicles and cold-chain depots.

- December 2024: Grupo Logista signed a USD 130 million textbook logistics contract covering 28,000 schools, embedding digital inventory tracking.

Spain Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing and Storage | |

| Value-Added Services |

| Central/Federal Government |

| State and Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing and Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State and Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

What is the current value of Spain government and education logistics?

The Spain government and education logistics market is valued at USD 7.1 billion in 2025 and is projected to reach USD 9.5 billion by 2030.

How fast is demand from universities growing?

Logistics spending by higher education institutions is forecast to rise at a 6.9% CAGR through 2030, the fastest among all end-user groups.

Which service type shows the highest growth potential?

Value-added services—covering inventory, packaging, and analytics—are expected to grow 8% annually, outpacing transportation and warehousing.

What impact do zero-emission zones have on providers?

Urban low-emission mandates push providers to electrify fleets, increasing upfront costs but improving tender scoring and lowering long-term fuel expenses.

Which region is set to expand the quickest?

Andalusia should post a 7.2% CAGR to 2030, boosted by a USD 3 billion modernization program in its public university network.

Page last updated on: