Mexico Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

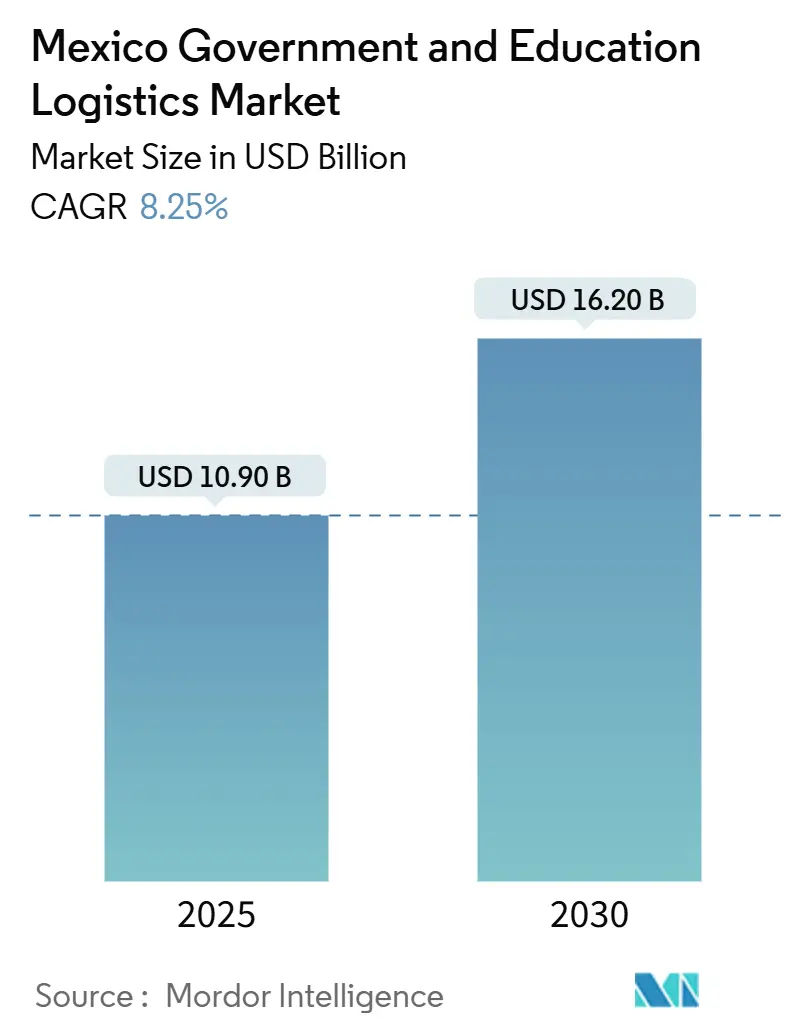

| Market Size (2025) | USD 10.90 Billion |

| Market Size (2030) | USD 16.20 Billion |

| Growth Rate (2025 - 2030) | 8.25% CAGR |

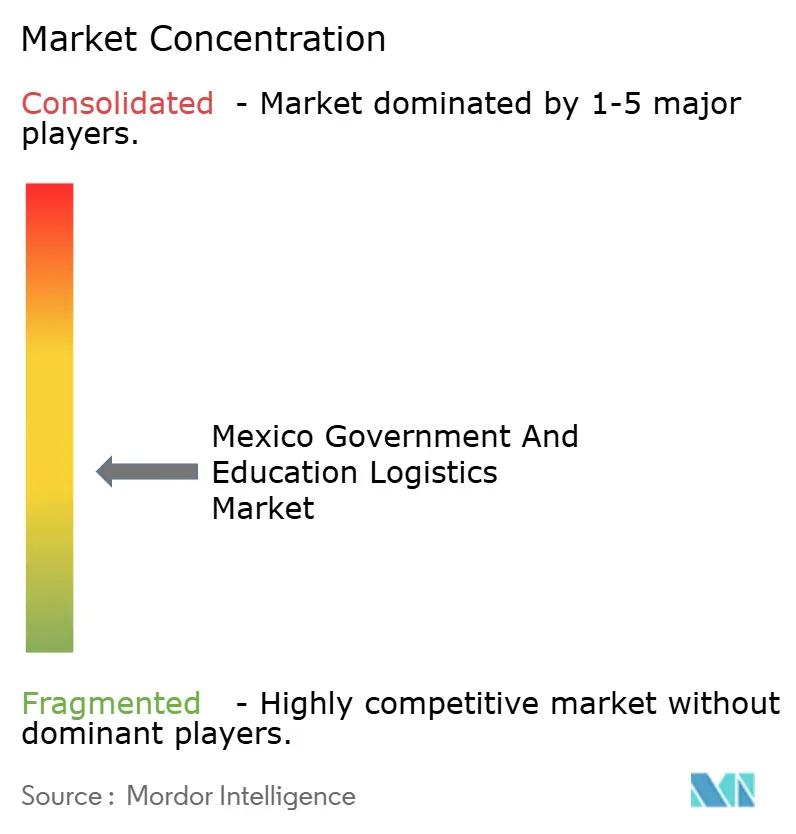

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Government And Education Logistics Market Analysis by Mordor Intelligence

The Mexico Government And Education Logistics Market size is estimated at USD 10.90 billion in 2025, and is expected to reach USD 16.20 billion by 2030, at a CAGR of 8.25% during the forecast period (2025-2030).

Momentum stems from the overlap of USMCA-driven nearshoring, federal corridor upgrades under the National Infrastructure Program, and accelerated digitization of public purchasing. Together, these forces shorten delivery lead times, raise service-quality thresholds, and expand contract volumes that favor providers with multimodal reach. Investments of MXN 157 billion (USD 8.7 billion) in logistics corridors in 2025 lowered average transit times by 18% on key federal routes, directly bolstering Mexico Government and Education Logistics market growth. Transparent e-tendering on the ComprasMX platform widened the bidder pool by 28% within six months of its launch, spurring price competition and compelling carriers to adopt real-time tracking, cold-chain validation, and ISO-compliant security protocols. Meanwhile, the defense ministry’s nationwide immunization campaigns opened a USD 180 million annual niche for temperature-controlled services, while the Universidad en Línea program’s reach to 2.3 million students lifted last-mile volumes in remote communities.

Key Report Takeaways

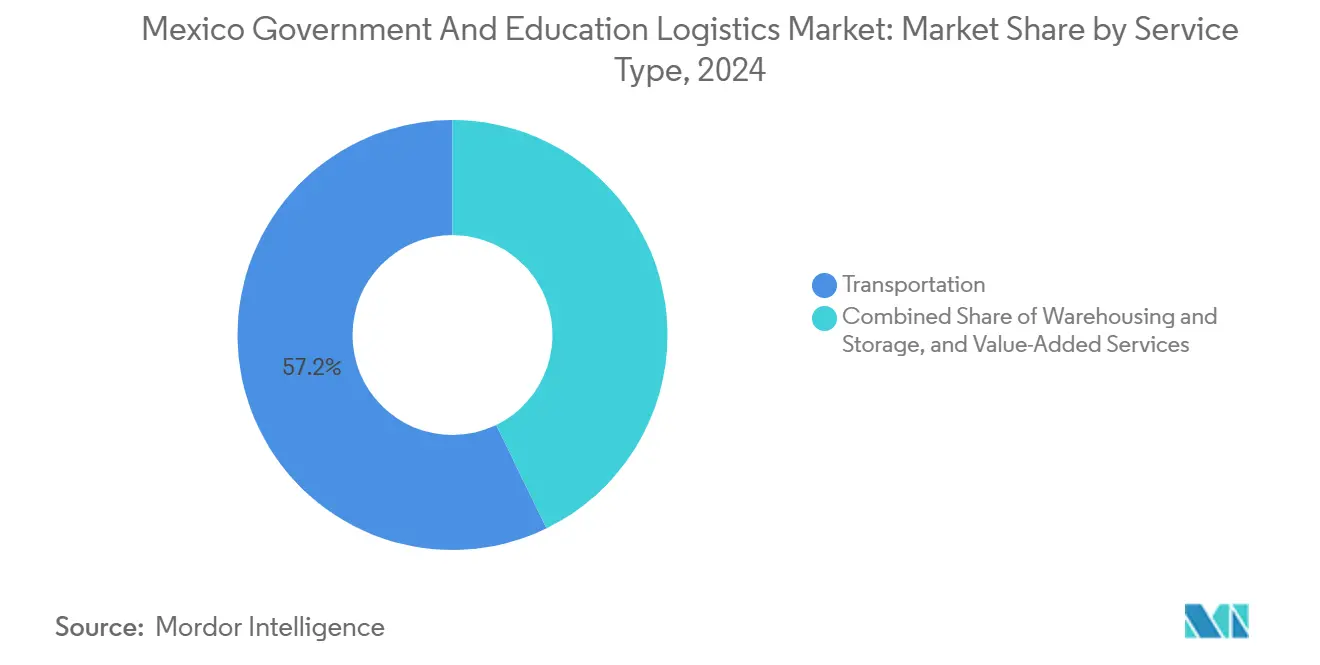

- By service type, transportation services captured a 57.20% Mexico Government and Education Logistics market share in 2024, whereas value-added services are set to expand at a 10.20% CAGR through 2030.

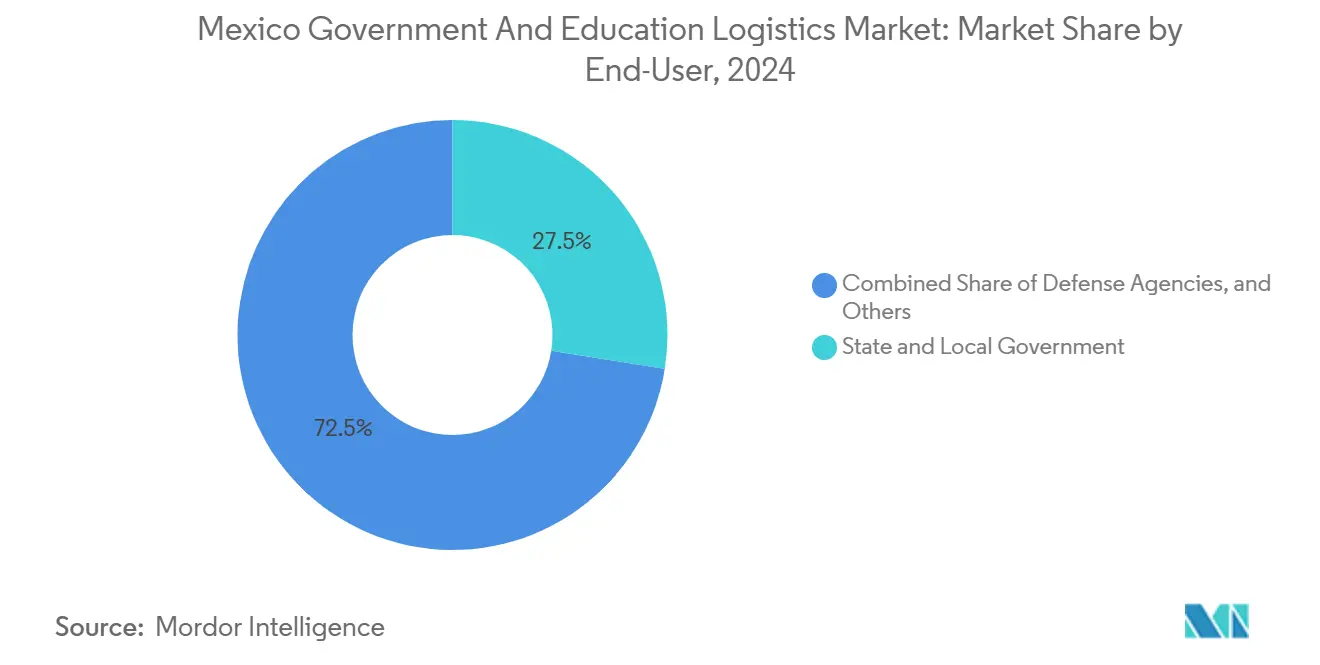

- By end user, state and local governments held 27.50% of the Mexico Government and Education Logistics market size in 2024, while higher-education institutions are projected to grow at a 9.80% CAGR to 2030.

Mexico participates in a competitive field that extends beyond its own borders. The market landscape in the global government and education logistics industry outlined by Mordor Intelligence covers that wider structure.

Mexico Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Infrastructure Program 2020-2024 upgrades logistics corridors | +1.8% | National, with concentration in central and northern corridors | Medium term (2-4 years) |

| Rapid digitization of federal procurement platforms raises 3PL demand | +1.5% | National, with early adoption in Mexico City, Guadalajara, Monterrey | Short term (≤ 2 years) |

| E-learning expansion drives distribution of IT and learning devices | +1.2% | National, with priority in rural and underserved communities | Medium term (2-4 years) |

| USMCA-linked near-shoring boosts government-funded industrial parks flows | +1.4% | Northern border states, with spillover to central Mexico | Long term (≥ 4 years) |

| Universidad en Línea micro-fulfillment to remote communities | +0.9% | Rural areas, particularly in southern and southeastern states | Medium term (2-4 years) |

| Defense ministry adoption of cold-chain for immunization campaigns | +0.7% | National, with emphasis on remote and indigenous communities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

National Infrastructure Program Drives Logistics Corridor Modernization

Federal highway and port investments totaling MXN 173 billion (USD 9.6 billion) through 2030 have trimmed Mexico City–border transit times by 18%, giving agencies faster replenishment cycles for textbooks, vaccines, and construction inputs. The 303-kilometer Interoceanic Corridor between Veracruz and Salina Cruz slashed east-west crossing times by up to 40% compared with Panama Canal routes, allowing imported learning devices and medical supplies to reach southern depots sooner. Reduced dwell times have cut logistics costs from 12-15% to 9-11% of procurement budgets, freeing fiscal space for additional service procurement. Providers with multimodal fleets now bundle road, rail, and short-sea legs to secure premium contracts tied to corridor milestones. As corridor capacity rises, the Mexico Government and Education Logistics market gains competitive headroom for specialized carriers, spurring growth in technology-enabled scheduling and predictive maintenance services[1]Secretaría de Infraestructura, Comunicaciones y Transportes, “Programa Nacional de Infraestructura 2025-2030,” Government of Mexico, gob.mx .

Federal Procurement Digitization Accelerates Third-Party Logistics Adoption

The April 2025 launch of ComprasMX requires real-time tracking and delivery confirmation on all contracts above MXN 500,000 (USD 27,800), prompting a 34% surge in 3PL registrations within half a year. Integration with the Llave MX digital ID system facilitates 2.1 million authenticated monthly transactions, tightening cybersecurity expectations through ISO 27001 mandates. Customs clearance for educational imports now completes in 24-48 hours, down from a week, improving fulfillment cycles for federal textbook programs. Agencies report 23% logistics savings thanks to standardized service-level agreements, while carriers invest in API-based visibility platforms to maintain compliance. The Mexico Government and Education Logistics market benefits from enlarged vendor pools, but only providers demonstrating data-security resilience and API fluency can capture elevated contract volumes[2]Secretaría de la Función Pública, “ComprasMX Platform Results 2025,” Government of Mexico, gob.mx .

E-Learning Infrastructure Expansion Creates Specialized Distribution Networks

Government shipment of 1.8 million tablets and laptops in 2024 marked a 67% rise from pre-pandemic levels and demanded last-mile reach to 32,000 rural schools. Logistics costs for Telesecundarias average USD 45-60 per device owing to unpaved roads and multi-modal legs. Providers now configure devices, add local-language content, and supply return-packing kits for warranty handling, elevating value-added service revenues. Regional hubs near Oaxaca and Chiapas benefit from shared storage and device-imaging lines that slash lead times by 20%. As hybrid learning persists, the Mexico Government and Education Logistics market will integrate IoT-enabled condition monitoring to prevent damage and temperature swings during mountainous transits, reinforcing the defensibility of specialized providers.

USMCA Nearshoring Amplifies Government-Funded Industrial Park Logistics

Government-backed industrial parks approved since 2024 rose 156%, unlocking USD 890 million in logistics contracts for site preparation and ongoing supply-chain services. Dedicated freight rail spurs, bonded warehouses, and just-in-time shuttle lanes now link automotive, electronics, and medical-device clusters to border crossings, compressing cross-border cycle times by up to 40%. Carriers that certify clean-room transport and temperature-controlled storage win multi-year contracts, especially where government agencies co-locate testing labs and customs offices inside park perimeters. Regional development-bank loans worth USD 2.3 billion finance supporting road and rail, ensuring sustained freight flow for at least a decade. Consequently, the Mexico Government and Education Logistics market deepens its portfolio of specialized services, from hazardous-materials handling to synchronized labor-shuttle operations.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-sector budget caps intensify price compression | -1.3% | National, with greater impact on state and municipal levels | Short term (≤ 2 years) |

| Limited rail connectivity in southern states | -0.8% | Southern Mexico, particularly Chiapas, Oaxaca, and Guerrero | Long term (≥ 4 years) |

| Complex customs rules for donated scholastic goods | -0.6% | National, with concentration at major ports and border crossings | Medium term (2-4 years) |

| Freight-security risks on rural school routes | -0.9% | Rural areas, particularly in states with higher crime rates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Public-Sector Budget Constraints Drive Logistics Cost Optimization

Despite rising service expectations, 2025 federal logistics allocations held flat in nominal terms while inflation touched 4.8%, forcing agencies to demand 15% cost reductions in new bids. Eighteen states trimmed logistics budgets by 8-12%, yet expanded delivery mandates, straining provider margins. To cope, INDAABIN mandated consolidated delivery routes, compelling carriers to adopt dynamic route optimization and shared-fleet models. Smaller regional providers face working-capital stress, accelerating M&A or subcontracting deals with larger networks. The Mexico Government and Education Logistics market thus polarizes between tech-enabled scale players and niche specialists that prove agile enough to meet stringent cost-to-serve targets[3]Secretaría de Salud, “Cadena Frio Vacunación 2024,” Government of Mexico, gob.mx .

Southern Mexico Rail Infrastructure Gaps Limit Logistics Efficiency

Southern states possess only 847 kilometers of active freight rail, 60% below national density, forcing 78% of government freight onto higher-cost trucking. Logistics costs to public schools and clinics run 25-35% higher than in the north. The Tren Maya will not add meaningful freight slots until after 2027, prolonging reliance on single-mode road transport and exposure to fuel-price volatility. Providers mitigate risk through security escorts and transload nodes but incur extra insurance premiums. These constraints temper otherwise robust prospects in the Mexico Government and Education Logistics market, underscoring the need for multimodal commitment in future infrastructure bills[4]“Educación 2024,” Instituto Nacional de Estadística y Geografía, inegi.org.mx.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Amid Value-Added Growth

Transportation services held 57.20% of the Mexico Government and Education Logistics market share in 2024, underpinned by a 176,000-kilometer federal highway grid that carries 85% of government freight. Rail’s improved Veracruz corridor trimmed city-port transit times by 22% and is projected to raise rail’s contribution to the Mexico Government and Education Logistics market size at a 6.8% CAGR through 2030. Airfreight supports medical emergencies and time-critical examination materials, while coastal shipping handles bulk commodities for public-works projects. Fierce competition drives carriers to add RFID-based cargo monitoring and encrypted electronic proof-of-delivery to meet federal transparency norms.

Value-added services, forecast to grow at 10.20% annually, emerge from government demands for inventory visibility, temperature integrity, and device configuration. Cold-chain operations for immunization programs alone generate USD 180 million each year. Providers bundle kitting, quality-assurance sampling, and reverse logistics into unified contracts, boosting revenue per shipment. Automated replenishment dashboards integrated with ComprasMX allow agencies to track stock levels in real time, enhancing contract renewals for providers demonstrating 99% fill-rate adherence. As public institutions co-locate warehousing near priority corridors, the Mexico Government and Education Logistics market attracts investments in robotics, pick-to-voice systems, and solar-powered refrigeration that align with federal sustainability metrics.

By End-User: State Governments Lead While Higher Education Accelerates

State and local governments accounted for 27.50% of the Mexico Government and Education Logistics market size in 2024, supporting 25.4 million K-12 students and 180,000 public schools. Their dispersed network of classrooms, clinics, and civic centers translates into more than 12 million annual delivery points, creating consistent throughput for regional carriers. Agencies prioritize balanced scorecard metrics that weight cost, punctuality, and security equally, encouraging providers to invest in telematics and driver-behavior analytics.

Higher-education institutions, projected to pace at a 9.80% CAGR, enlist specialized logistics for research equipment, laboratory chemicals, and cross-border academic exchanges. The segment recorded a 43% spending rise since 2024 as universities adopt hybrid learning models requiring cloud-configured devices and campus micro-fulfillment centers. Compliance with customs and bio-safety norms favors carriers with dedicated brokerage teams and GDP-certified facilities. As federal funding attaches performance-based payment triggers, logistics partners that can capture IoT-derived utilization data strengthen contract longevity, enhancing the resilience of the Mexico Government and Education Logistics market.

Geography Analysis

Central Mexico anchors the highest logistics density, with Mexico City and Estado de Mexico concentrating 21% of the national population and 35% of airfreight volume via Benito Juárez International Airport ASA. Federal agency headquarters and major universities cluster within a 200-kilometer radius, generating steady high-value shipments, especially for temperature-controlled vaccines and IT hardware. Superior road and rail connectivity allows carriers to stage inventory for nationwide dispatch, ensuring 24-hour delivery windows to 70% of municipalities. Two smart-logistics parks inaugurated in 2024 added 85,000 square meters of bonded storage with automated customs interfaces, reducing city congestion and enhancing same-day fulfillment metrics.

Northern border states—Nuevo Leon, Chihuahua, and Tamaulipas—capture escalating volumes tied to USMCA industrial parks, processing 40% of international trade through 47 land ports INM. Customs-bonded lanes, C-TPAT-compliant yards, and 24/7 inspection regimes require logistics providers to maintain strict security protocols and real-time data interchange with U.S. counterparts. Private investments of USD 3.2 billion in 2024 delivered modern cross-dock and cold-chain capacity, improving temperature-compliance scores for vaccine consignments to 99.8%. Carriers leverage bi-national driver pools and drop-and-hook trailers to turn border crossings in under two hours, uplifting service reliability for federally funded medical facilities along the frontier.

Southern states—Chiapas, Oaxaca, and Guerrero—face terrain, security, and infrastructure deficits that add 25-35% to logistics costs CONEVAL. Remote indigenous communities rely on mixed-mode trips combining trucks, riverboats, and pack animals for final delivery. Security escorts for school-meal supplies elevate insurance costs, while limited cold-storage nodes raise spoilage risk. Government programs like the Interoceanic Corridor and Tren Maya pledge improved connectivity by 2028; until then, specialized local providers with community ties dominate last-mile reaches. Federally funded pilot drone deliveries for urgent lab samples in Oaxaca began test flights in late 2025, hinting at future cost-effective alternatives and potential uplift for the Mexico Government and Education Logistics market.

Mordor Intelligence provides coverage of the government and education logistics market across other key regional markets, including Asia, North America, and Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Canada, South Korea, United Kingdom, Germany, Spain, and India incorporating local coverage and market participation, as required.

Competitive Landscape

The Mexico Government and Education Logistics market features roughly 15-20 sizeable competitors vying for USD 2.8 billion in annual contracts, yielding moderate fragmentation. UPS’s USD 1.1 billion purchase of Estafeta in 2024 consolidated the largest integrated fleet with 100% national coverage, advanced API interfaces to ComprasMX, and 12 percent share of federal shipments UPS. DHL Group leverages its Querétaro cold-chain hub, opened in December 2024, to pursue Ministry of Health tenders, adding 800 jobs and 40% extra temperature-controlled capacity DHL. Grupo Traxion secures provincial contracts by coupling regional trucking with ISO 14001-certified sustainability credentials, meeting rising environmental scoring criteria.

Technology-first disruptors such as Nowports and SkydropX deliver AI-driven routing and IoT-based asset tracking but face entry barriers because government bids demand multi-year audited financials and ISO-aligned data-security certifications. Nevertheless, partnerships with established carriers grant these startups access to corridor upgrade funds while enhancing visibility layers that federal buyers prize. Service differentiation trends center on predictive analytics for inventory planning, blockchain-backed chain-of-custody records for sensitive materials, and solar-powered refrigeration for rural immunization drives.

Price competition intensifies as budget-capped agencies demand 15% lower costs yet higher on-time performance. Providers respond with shared-asset models that merge textbook, vaccine, and construction-material loads along optimized corridors, improving vehicle utilization to 83%. Carriers with telematics-based safety programs also cut accident rates, an increasingly weighted KPI in ministry scorecards. Long-term, market leaders that embed ESG metrics into bids and showcase carbon-tracking dashboards stand to widen their moat in the Mexico Government and Education Logistics market.

Mexico Government And Education Logistics Industry Leaders

DHL Group

Estafeta

Grupo Traxion

FedEx

United Parcel Service, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: DHL Group confirmed a MXN 1.1 billion (USD 61 million) expansion for a 50,000 m² cold-chain facility in Querétaro, adding 800 jobs.

- September 2024: FedEx Express Mexico opened temperature-controlled sites in Guadalajara and Monterrey to grow healthcare and university research contracts.

- July 2024: UPS finalized its USD 1.1 billion Estafeta acquisition, creating the country’s broadest network for government tenders.

- February 2024: DHL launched its automated T-Mex Park campus in Nextlalpan with 35,000 m² of green design aimed at public-sector procurement DHL.

Mexico Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing and Storage | |

| Value-Added Services |

| Central/Federal Government |

| State and Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing and Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State and Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

What is the forecast value of the Mexico Government and Education Logistics market in 2030?

The market is projected to reach USD 16.2 billion by 2030, reflecting an 8.25% CAGR during 2025-2030.

Which service segment is expanding fastest?

Value-added services, propelled by cold-chain and device-configuration needs, are forecast to grow at 10.20% annually through 2030.

How did ComprasMX change contract dynamics?

The 2025 launch mandated real-time tracking and standardized SLAs, expanding 3PL registrations by 34% within six months and lowering average procurement logistics costs by 23%.

Why are higher-education institutions important to logistics providers?

Hybrid learning models and research globalization lifted university logistics spending by 43% since 2024, generating demand for specialized customs brokerage and secure lab-equipment handling.

Which regions show the highest logistics cost differentials?

Southern states incur 25-35% higher costs due to limited rail infrastructure and challenging terrain, while northern border states benefit from advanced multimodal connectivity.

Page last updated on: