Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

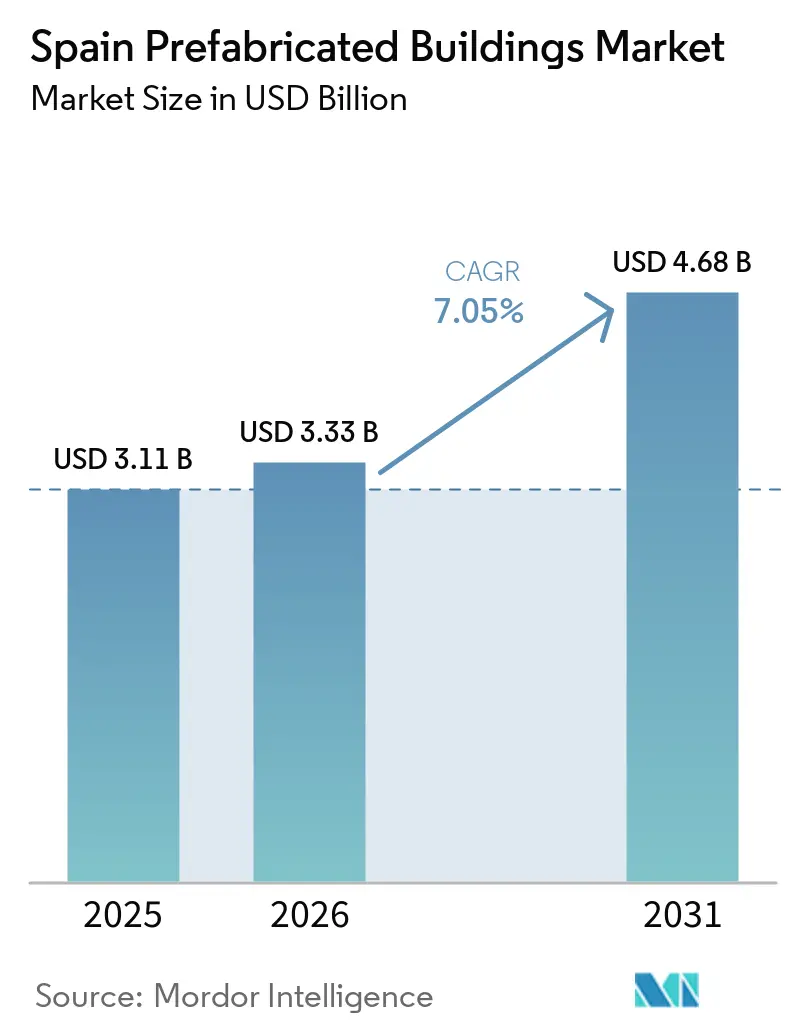

| Base Year Market Size (2025) | USD 3.11 Billion |

| Market Size (2026) | USD 3.33 Billion |

| Market Size (2031) | USD 4.68 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Prefabricated Buildings Market Analysis by Mordor Intelligence

The Spain prefabricated buildings market size in 2026 is estimated at USD 3.33 billion, growing from 2025 value of USD 3.11 billion with 2031 projections showing USD 4.68 billion, growing at 7.05% CAGR over 2026-2031. The combination of EU-funded industrialization grants, tightening energy rules, and a chronic housing shortage is propelling this expansion. Demand is strongest in urban and tourism-driven regions where speed, cost certainty, and energy efficiency are prized. Factory-built capacity is rising as the PERTE program injects USD 1.42 billion in long-term capital, while digital twin and BIM-LEAN workflows reduce on-site labor needs. As a result, the Spain prefabricated buildings market is rapidly evolving from small-batch panelization to high-throughput volumetric production[1]Government of Spain, “PERTE Industrialización de la Vivienda,” lamoncloa.gob.es.

Key Report Takeaways

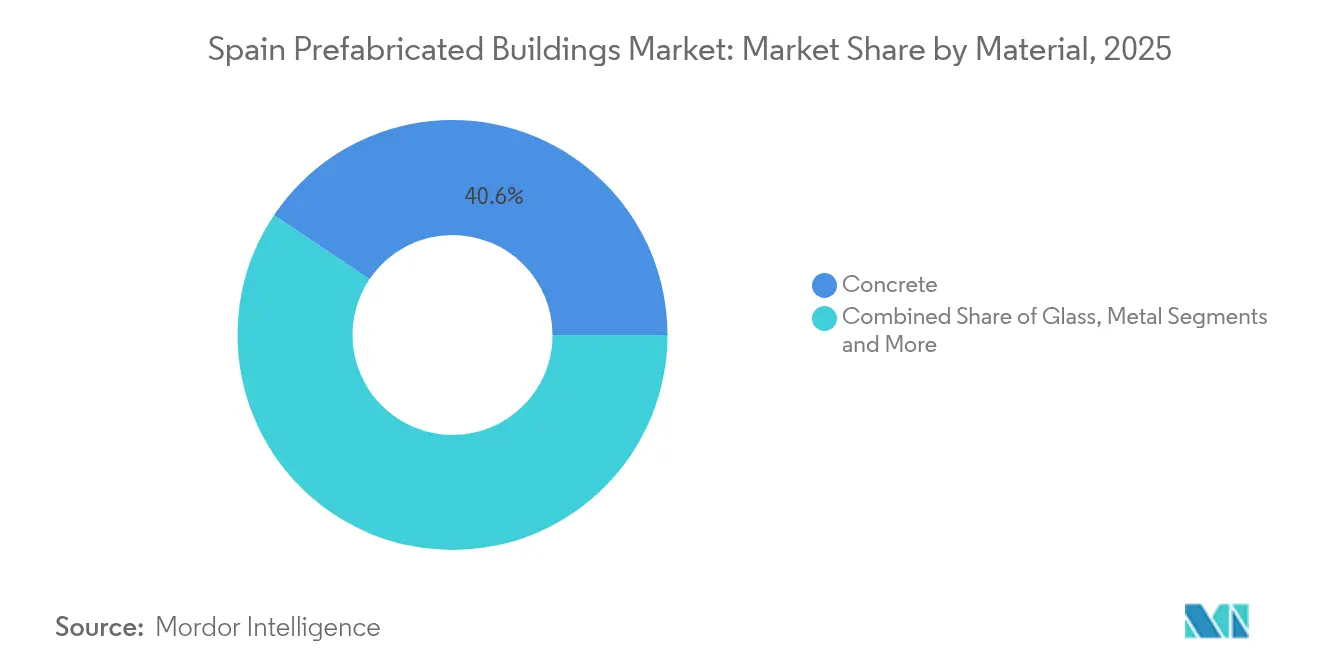

- By material, concrete led with 40.60% of Spain's prefabricated buildings market share in 2025, whereas timber is forecast to grow at an 7.86% CAGR through 2031.

- By application, residential captured 52.60% of Spain prefabricated buildings market size in 2025; commercial is advancing at a 7.58% CAGR to 2031.

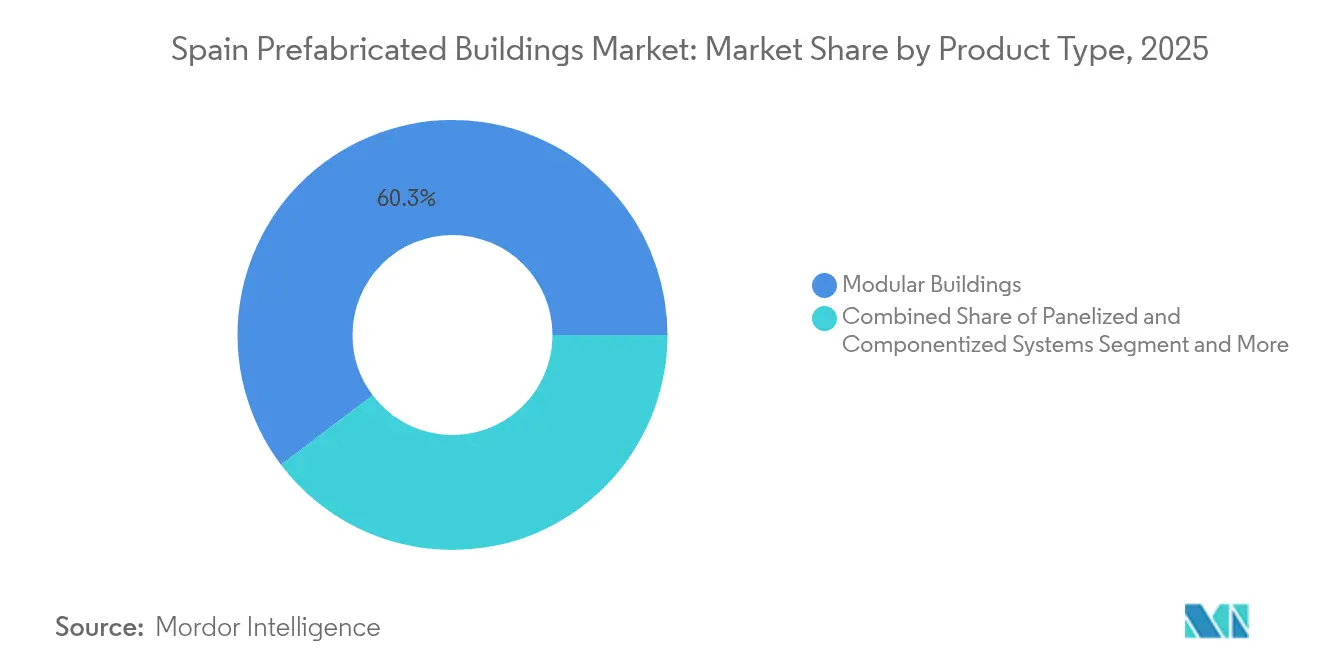

- By product type, modular solutions held 60.30% share of the Spanish prefabricated buildings market size in 2025, while panelized systems posted the fastest 7.74% CAGR through 2031.

- By key cities, Madrid commanded 20.80% of Spain's prefabricated buildings market share in 2025; Catalonia, excluding Barcelona, is expanding at an 8.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Prefabricated Buildings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU NextGen funds accelerating industrialised-housing uptake | +2.0% | National, with early gains in Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Mandatory EPC-B retrofit targets favouring modular over-cladding | +1.4% | National, urban and peri-urban zones | Medium term (2-4 years) |

| Labour-scarcity pushing off-site productivity gains | +1.1% | National, acute in urban centres | Short term (≤ 2 years) |

| Tourism-driven rental shortage boosting rapid-build demand | +1.0% | Barcelona, Madrid, coastal regions | Short term (≤ 2 years) |

| Wild-fire-resilient CLT modules for rural rebuilds | +0.4% | Rural Spain, wildfire-prone regions | Long term (≥ 4 years) |

| On-site crane permit exemptions for flat-pack volumetrics | +0.2% | Select municipalities, pilot cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU NextGen funds accelerate industrialized housing

The Spain prefabricated buildings market benefits directly from NextGenerationEU grants that channel USD 1.42 billion into factory upgrades, digital twins, and workforce training. Madrid and Valencia lead early pilots that target 20,000 industrialized homes a year by 2035. Manufacturers winning these funds enjoy reduced capital costs, faster type approvals, and priority access to public land. Public-private consortia are standardizing modules that hit EPC-B ratings at scale, lowering risk for lenders and insurers. The result positions Spain as an EU benchmark for industrialized residential delivery[2]Government of Spain, “NextGenEU Housing Investment,” lamoncloa.gob.es.

Mandatory EPC-B retrofits favor modular over-cladding

Royal Decree 390/2021 and the updated Technical Energy Code require EPC-B for both new builds and major retrofits. Modular over-cladding delivers airtight façades without displacing tenants, reducing on-site disruption by 50% compared with traditional scaffolding. Social landlords are bundling retrofit contracts into 10-year energy-performance agreements that reward suppliers able to guarantee kWh savings. These mandates generate predictable, long-run revenue streams and fuel the Spain prefabricated buildings market.

Labor scarcity pushes off-site productivity

With one in three skilled construction workers aged over 55, contractors face mounting delays and cost overruns. Off-site factories mitigate labor gaps through automation, robotic welding, and digital quality control. Pilot lines in Madrid now use 3D scanners and AI-driven scheduling that cut re-work rates by 40%. Investors view these efficiency gains as crucial to preserving margins amid wage inflation. Consequently, the Spain prefabricated buildings market is migrating from labor-intensive panelization to highly automated volumetric lines.

Tourism-driven rental shortage boosts rapid builds

Tourism’s strong rebound has tightened rental supply in Barcelona, Madrid, and coastal resorts, pushing municipalities to fast-track volumetric apartments that can be stacked and fitted out within weeks. Social rental homes comprise under 2% of total stock, well below the EU average, prompting USD 436 million in European Investment Bank funding earmarked for modular projects. Container-based schemes in Barcelona cut on-site time by 60% and integrate renewables to meet EPC-B thresholds. This surge in demand strengthens the order books of local volumetric specialists and international turnkey suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented municipal codes delaying type-approval roll-out | -1.4% | National, acute in smaller cities | Medium term (2-4 years) |

| Premium land prices squeezing plant-logistics radii | -0.9% | Madrid, Barcelona, coastal zones | Short term (≤ 2 years) |

| Shortage of domestic CLT capacity vs booming export demand | -0.8% | National, rural and export hubs | Long term (≥ 4 years) |

| Perception of prefab as low-quality in high-end coastal zones | -0.6% | Mediterranean coast, Balearics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented municipal codes delay type approval

Spain’s 8,000-plus municipalities enjoy wide autonomy over planning and fire codes, forcing suppliers to navigate a maze of local rules. While Madrid and Valencia offer digital one-stop portals, smaller towns still rely on manual checks that can push modular approvals beyond 120 days. SMEs lack the legal resources to track varying requirements, curbing cross-regional scale and slowing the Spain prefabricated buildings market.

Premium land prices squeeze plant-logistics radii

Industrial land near Madrid and Barcelona rose 18% year-on-year in 2025, inflating factory lease costs and trucking distances. Large volumetric units incur higher freight fees once the delivery radius exceeds 250 miles, eroding cost advantages. Producers respond with hub-and-spoke micro-factories or shift to lighter flat-pack modules to ease transport. Yet rising land costs continue to cap margins, restraining growth in the Spain prefabricated buildings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Concrete Dominance Meets Timber Momentum

Concrete accounted for 40.60% of Spain's prefabricated buildings market share in 2025, underpinned by an established supply chain and broad contractor familiarity. Volumetric concrete pods dominate student housing and hotel bathrooms, where fire and acoustic regulations are stringent. Producers such as Eiffage have integrated high-recycled aggregate mixes that cut embodied carbon by 35% compared with 2023 baselines. Timber, led by CLT and glue-lam, records the fastest 7.86% CAGR, driven by carbon reporting mandates and wildfire-resilient rural programs. Public tenders in Catalonia now assign up to 10 quality points for biogenic materials, tipping awards toward timber modules. Metal and glass hybrids serve iconic retail façades, while high-performance insulation panels extend concrete’s reach into near-zero-energy buildings.

Timber’s growth reshapes factory workflows: automated CNC lines cut panels to millimeter precision, and robotic spray booths apply fire-retardants within minutes. Modular makers pair CLT walls with steel chassis to meet seismic requirements in Granada and Murcia. Insurers offer premium discounts for properly treated timber, a shift from earlier skepticism. Concrete producers respond with ultra-thin UHPC walls that shave 20% off transport weight, defending market share. Such material innovation keeps the Spain prefabricated buildings market agile and responsive to evolving standards.

By Application: Residential Still Rules, Commercial Gains Pace

Residential applications held 52.60% of Spain's prefabricated buildings market size in 2025, cemented by social housing schemes and build-to-rent portfolios. Madrid’s latest tender bundles 2,000 modular apartments with 15-year concession contracts, guaranteeing occupancy and maintenance income. Developers value volumetric units that arrive 90% complete, shortening finance drawdown periods. The commercial segment grows at a 7.58% CAGR as hotels and flexible offices crave rapid refurbishments ahead of the 2030 EU energy deadline. Chain operators repurpose obsolete malls into prefab co-working hubs, embedding smart sensors for energy billing. Healthcare and education add a steady baseline demand through standardized ward and classroom modules.

Government subsidies covering 50% of envelope retrofits spur residential cooperatives to adopt over-cladding kits that lift EPC ratings from G to B in four weeks. Meanwhile, hospitality groups like Meliá pilot timber micro-suites that can be relocated between resorts, reducing stranded assets. Logistics firms install prefab mezzanine offices inside warehouses to comply with labor agreements for climate-controlled break areas. This diversity in use cases broadens the Spain prefabricated buildings market and attracts specialized suppliers.

By Product Type: Modular Supremacy with Panelized Agility

Modular products commanded 60.30% of the Spanish prefabricated buildings market in 2025, favored for turnkey delivery and predictable quality. Multi-story volumetric blocks reach 12-coupled levels using post-tensioned connectors, a leap from the six-story limit common in 2023. Factory integration of HVAC and solar pre-wiring slashes commissioning times by 40%. Panelized systems, while holding a smaller share, post the fastest 7.74% CAGR because they ship flat and flexibly navigate narrow urban streets. Retrofit specialists exploit lightweight SIP panels to upgrade façades without heavy cranes.

Digital twins anchor both product types: cloud models synchronize factory output with site progress, reducing idled inventory. Regulations permitting on-site snap-fit connectors speed panel assembly to one floor per day on social-housing pilots. Modular majors differentiate through embedded IoT that monitors indoor air quality, a feature aligned with post-pandemic tenant expectations. Panel makers counter with customizable façades that meet strict heritage-zone aesthetics in Toledo and Seville. Together, these dynamics reinforce competition and innovation within the Spain prefabricated buildings market.

Geography Analysis

Madrid leads the Spain prefabricated buildings market with a 20.80% share in 2025 on the back of large public-housing concessions and the region’s streamlined digital permitting portal. EU funds funnel through the regional housing agency to co-finance volumetric blocks that must hit EPC-B ratings. Investors gain confidence from a standardized type-approval catalogue that cuts legal fees by 30%. Municipal land auctions now reserve parcels for factory-built schemes, attracting joint ventures between local SMEs and foreign OEMs.

Catalonia, excluding Barcelona, is the fastest-growing geography at an 8.07% CAGR through 2031. Regional authorities promote CLT modules for fire-prone rural villages and subsidize micro-factory start-ups in Lleida and Tarragona. Public-education contracts bundle classroom pods with rooftop PV, guaranteeing builders long-term service revenue. Barcelona’s container-based program demonstrates how volumetric units can occupy vacant lots for up to 10 years, easing rental pressures without committing to permanent zoning changes. Such policy agility cements Catalonia’s role as an innovation sandbox for the Spain prefabricated buildings market.

Smaller cities and rural provinces adopt prefab to tackle energy poverty and depopulation. The updated Technical Energy Code mandates renewable integration, pushing municipal councils to procure over-clad kits financed by future energy savings. Regional banks offer low-interest loans backed by carbon credits earned from modular retrofits. CLT’s low embodied carbon triggers extra grant points under national wildfire resilience schemes. This distributed uptake widens the Spain prefabricated buildings market’s footprint beyond traditional urban strongholds.

Competitive Landscape

A fragmented field of regional champions, digital start-ups, and pan-European contractors competes for contracts across Spain. Local pioneer ROOM2030 operates a plug-and-play production cell in Asturias that outputs sensor-equipped micro-apartments completed in 72 hours. Eiffage aligns with Spanish architects to introduce ultra-low-carbon concrete pods, leveraging its continental procurement muscle. International entrants such as Skanska scout joint ventures to fast-track type approvals, recognizing the Spain prefabricated buildings market as a launchpad for southern Europe.

Strategic moves emphasize vertical integration and IP protection. ROOM2030 co-filed patents on telescopic CLT cores that enable modular high-rise extensions, while Eiffage invested in a Madrid BIM hub to drive common data environments across subcontractors. Start-ups target niche gaps: Galician firm Enxertia builds relocatable timber refuges for wildfire areas, while Valencia’s DecoMod focuses on façade-mounted energy-storage modules. Such specialization heightens competitive intensity yet broadens customer choice.

Capital flows keep pace. The PERTE program subsidizes 20% of capex for factories investing in robotics and digital twins, attracting private equity co-financing. Manufacturers hedge logistics costs by opening micro-factories within 150 miles of demand clusters. Corporate buyers negotiate framework agreements that lock material prices for five years, sheltering margins against commodity volatility. Collectively, these tactics shape a dynamic prefabricated buildings market moving toward industrial maturity.

Spain Prefabricated Buildings Industry Leaders

Algeco España

Grupo Avintia (Ávita Industrial)

Compact Habit

Grupo ALCO Modular

Wallex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Spanish government’s PERTE program injects USD 1.42 billion into factory upgrades, robotics, and workforce training, directly expanding domestic modular capacity and creating a pipeline of 20,000 industrialized homes per year.

- March 2025: Eiffage’s expansion adds low-carbon concrete pods and solar-ready façades to its Spanish portfolio, broadening the range of prefabricated components available to residential and commercial developers.

- February 2025: ROOM2030’s launch of the ROOM2030 Plus line and the completion of a six-story prefab building in Gijón showcase the technical viability of mid-rise volumetric construction and elevate consumer perceptions of modular living.

- December 2024: Arcosa’s USD 1.2 billion acquisition of Stavola strengthens domestic supply chains for aggregates and structural components, helping prefab manufacturers secure more predictable input costs.

Spain Prefabricated Buildings Market Report Scope

Prefabrication is the construction method where a building structure's components are assembled either in a manufacturing or production site, transporting complete assemblies or partial assemblies to the site where the structure is to be located. This work is carried out in two stages: manufacturing components in a place other than the final location and their erection onsite.

A complete background analysis of the Spain prefabricated buildings market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The Spain prefabricated buildings market is segmented by material type and by application. By material the market is segmented by concrete, glass, metal, timber, and other material types and by application the market is segmented by residential, commercial, and other applications (infrastructure and industrial)). The report offers the market size and forecasts in values (USD) for all the above segments.

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Key Cities

| Madrid |

| Barcelona |

| Catalonia (ex-Barcelona) |

| Rest of Spain |

| By Material | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Key Cities | Madrid |

| Barcelona | |

| Catalonia (ex-Barcelona) | |

| Rest of Spain |

Key Questions Answered in the Report

How large is the Spain prefabricated buildings market in 2026?

It is valued at USD 3.33 billion in 2026 and is projected to reach USD 4.68 billion by 2031, reflecting a 7.05% CAGR over 2026-2031.

What share do modular products hold in Spain’s prefab segment?

Modular Buildings represented 60.30% of total 2025 sales, making them the dominant product category.

Which Spanish region is growing fastest in prefabrication?

Catalonia excluding Barcelona posts the quickest 8.07% CAGR (2026 - 2031) thanks to supportive rural-resilience and retrofit incentives.

Why is timber gaining ground versus concrete?

Timber’s 7.86% CAGR (2026 - 2031) stems from lower embodied carbon, wildfire-resilient designs, and public tenders that prioritize biogenic materials.

How do EU energy rules affect prefab adoption?

Royal Decree 390/2021 sets EPC-B as the minimum rating, pushing demand for modular over-cladding and volumetric units that meet these standards with less on-site work.

What financing options exist for modular social housing?

EU NextGen funds, EIB low-interest loans, and municipal concession contracts combine to lower capital costs and derisk large volumetric projects.

Page last updated on: