Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

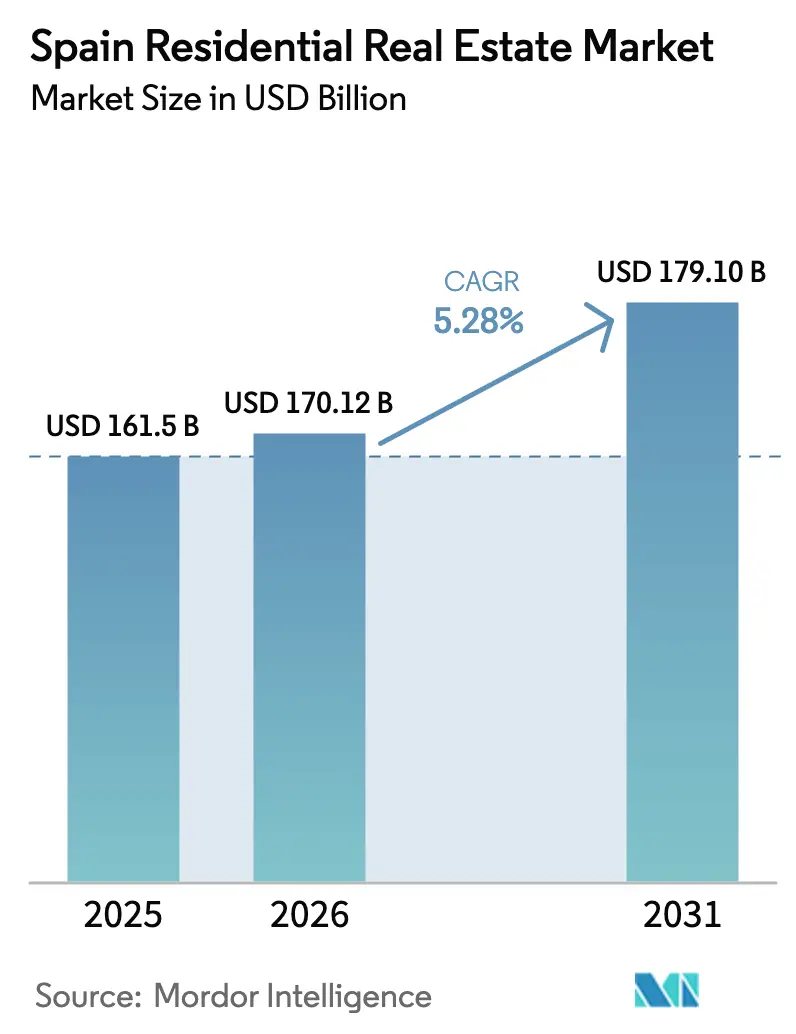

| Base Year Market Size (2025) | USD 161.5 Billion |

| Market Size (2026) | USD 170.12 Billion |

| Market Size (2031) | USD 179.10 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

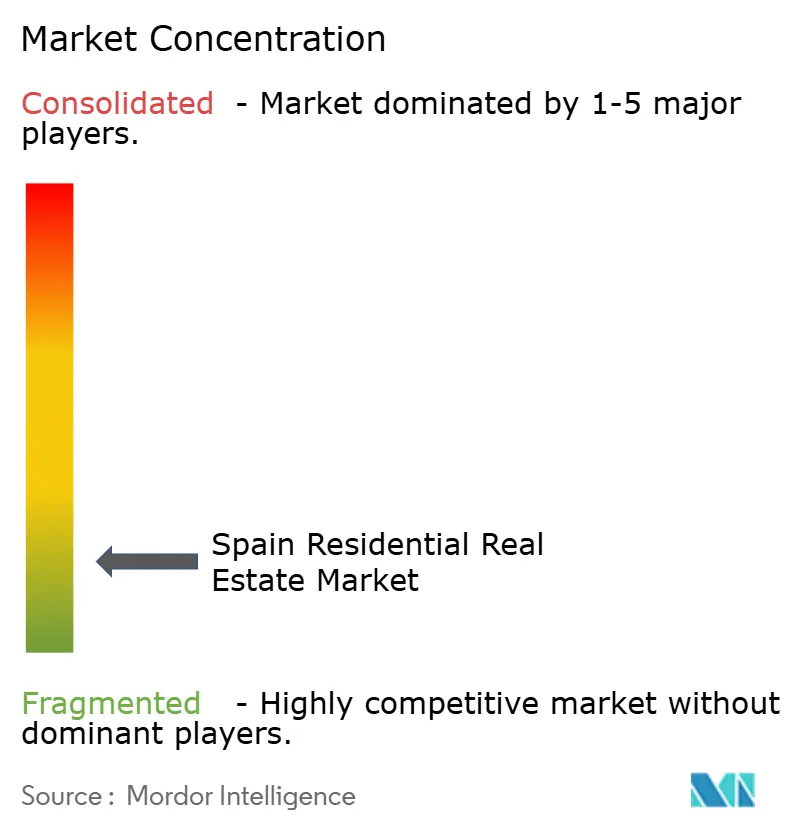

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Residential Real Estate Market Analysis by Mordor Intelligence

The Spain residential real estate market is valued at USD 170.12 billion in 2026 and is forecast to reach USD 179.10 billion by 2031, advancing at a 5.28% CAGR. Intensifying supply shortages, stronger foreign-buyer activity, and a wave of institutional Build-to-Rent capital continue to underpin pricing despite volatile financing costs. Madrid alone accounts for almost half of the Spain residential real estate market, yet Andalusia-Málaga & Costa del Sol posts the fastest growth as remote-working Europeans move south. Buyer demand is shifting toward energy-efficient “Clase A” dwellings after the 2021 Código Técnico update, while digital mortgage platforms lower onboarding frictions for non-resident purchasers. Tight labor markets and rising land prices impose cost pressure, but large developers consolidate land banks and pivot toward industrialized construction to accelerate delivery.[1]https://european-union.europa.eu/index_en

Key Report Takeaways

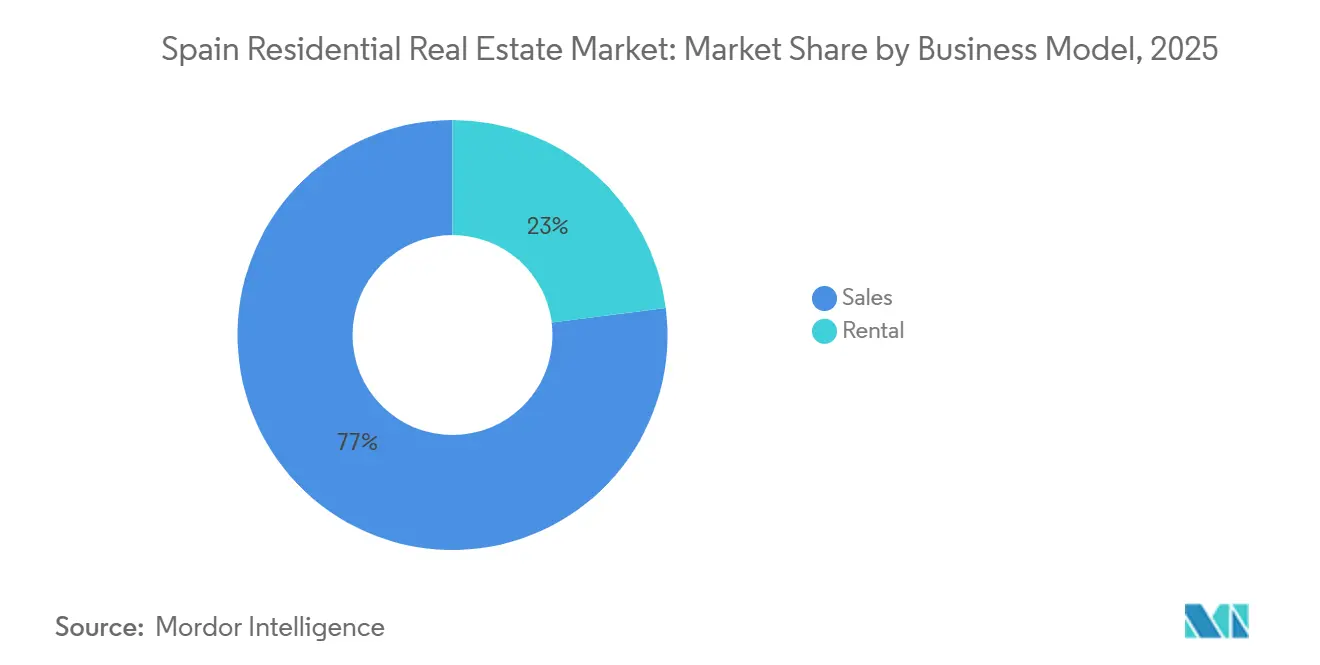

- By business model, sales retained 77% of the Spain residential real estate market share in 2025, while rental is advancing at a 5.81% CAGR through 2031.

- By property type, apartments dominated with 69% of the Spain residential real estate market size in 2025; villas are growing fastest at a 5.62% CAGR between 2026-2031.

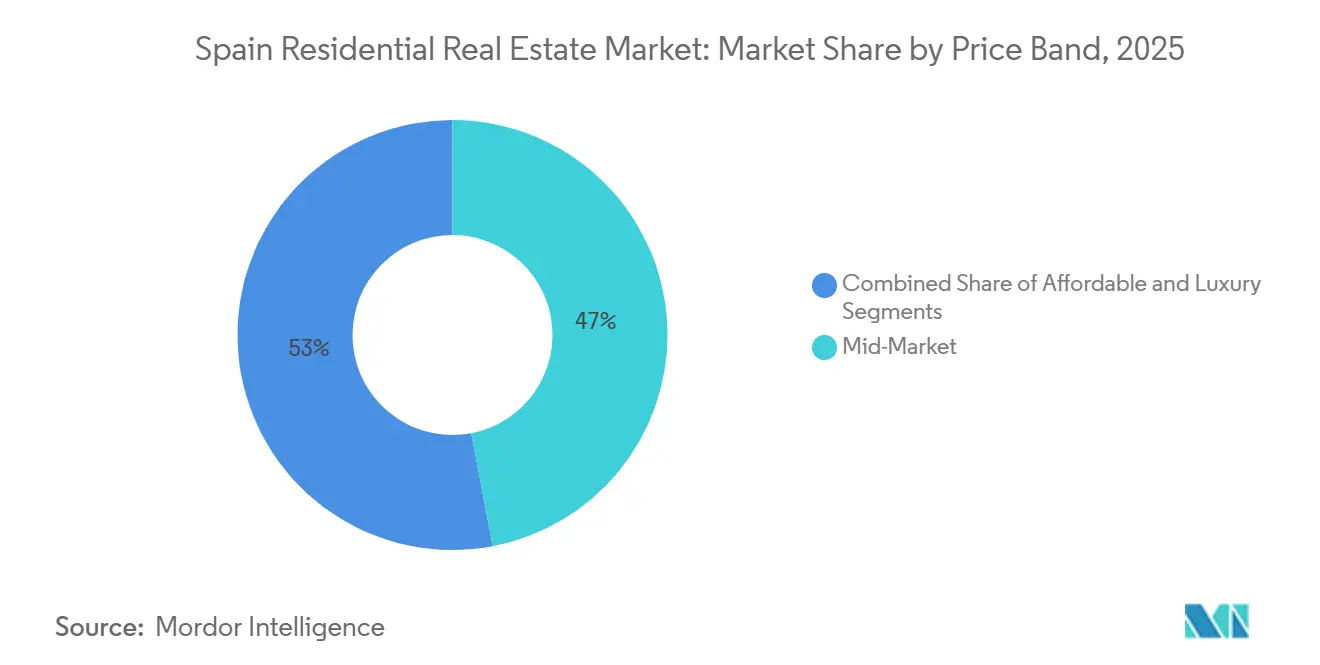

- By price band, mid-market units held 47% of transaction value in 2025; luxury is projected to expand at a 6.12% CAGR to 2031.

- By mode of sale, secondary resales accounted for 58% of the Spain residential real estate market size in 2025, and new-builds are poised to grow at a 6.44% CAGR through 2031.

- Madrid controlled 49% of the transaction value in 2025, and Andalusia–Málaga is the fastest-growing geography at a 6.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ECB-rate-linked mortgage repricing boosts pent-up demand | +1.2% | Global, strongest in Madrid, Barcelona, Valencia | Short term (≤ 2 years) |

| Institutional build-to-rent pipelines scale rapidly | +0.9% | Madrid, Barcelona, Valencia Community, Málaga | Medium term (2-4 years) |

| Tele-commute shift channels buyers to Valencia & Málaga | +0.8% | Valencia Community, Andalusia, Catalonia ex-Barcelona | Long term (≥ 4 years) |

| EU-funded energy-efficiency renovation subsidies | +0.7% | National; early gains in Catalonia, Madrid, and Andalusia | Medium term (2-4 years) |

| Digital-nomad and Golden-Visa inflows lift foreign purchases | +0.5% | Andalusia, Barcelona, Valencia coast | Short term (≤ 2 years) |

| Smart-home retrofit premiums unlock upsell revenue | +0.4% | Madrid, Barcelona, and high-end coastal developments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ECB-Rate-Linked Mortgage Repricing Boosts Pent-Up Demand

The European Central Bank’s 200-basis-point deposit-rate cuts between September 2023 and June 2025 lowered average variable mortgage costs from 4.8% to 3.1%, trimming monthly payments on a typical EUR 200,000 (USD 220,000) loan by roughly EUR 180 (USD 198) and reviving affordability for sidelined households because 65% of Spanish mortgages track 12-month Euribor, the drop in that benchmark from 4.23% to 2.50% restored buying power and pushed new originations 14% higher year-on-year in Q1 2025. Reservation-to-contract conversion climbed to 68% in early 2025, indicating renewed confidence among first-time buyers. The effect is strongest in Madrid and Barcelona, where lower rates expanded the qualifying household pool by 22%. With the ECB signaling a policy-rate floor near 2.00% through 2026, borrowers are locking in financing sooner, compressing the option value of delaying purchases.[2]https://www.bde.es/wbe/es/

Institutional Build-to-Rent Pipelines Scale Rapidly

Institutional capital commitments since January 2024 exceed EUR 765 million (USD 842 million), shifting strategy from single-asset buys to programmatic portfolio construction. Aviva Investors and Layetana’s EUR 300 million (USD 330 million) venture will deliver 928 rental units, while Barings-Salas and LandCo-Patron platforms add more than 1,900 homes across Valencia, Málaga, Madrid, and Barcelona. These vehicles professionalize management, offer CPI-linked escalations, and promise yields that diversify pension portfolios away from volatile retail or office exposure. Spain’s rental stock is 85% individually owned, so institutional operators fill a service gap with digital leasing, parcel lockers, and ISO 9001–certified maintenance, enhancing tenant retention and stabilizing cash flows. Compliance with regional energy-certificate mandates is embedded at the design stage, aligning assets with ESG capital mandates and supporting premium valuations at exit.

Tele-Commute Shift Channels Buyers to Valencia & Malaga Coast

Hybrid work allows Madrid-based professionals to relocate without sacrificing career prospects. High-speed rail now links Madrid to Málaga in 2.5 hours, and to Valencia in 1.8 hours, widening commuter belts. Detached-home transactions in Valencia climbed 10.5% in 2024, while Málaga villa sales jumped 18%, each outpacing national averages. Employers reporting sustained 2-day-per-week office attendance expect telecommute flexibility to remain a perk, reinforcing demand for coastal living with larger plots and outdoor space. These relocations reduce pressure on urban cores and distribute price growth into secondary cities, diversifying the Spain residential real estate market.

EU-Funded Energy-Efficiency Renovation Subsidies (NextGenEU)

Spain has allocated EUR 3.42 billion (USD 3.76 billion) from the EU recovery fund to retrofit 510,000 homes by 2026, reimbursing up to 40% of insulation, window, or heat-pump costs. Catalonia secured EUR 115 million (USD 127 million) and has already upgraded 18,000 units, improving average EPC ratings from E to C. Certified A or B homes command 7-12% price premiums in Madrid and Barcelona because buyers monetize expected utility savings. The subsidy requires owners to pre-finance works, favoring equity-rich households and institutional landlords over small investors. Developers leverage the grant by embedding energy features—photovoltaics, smart thermostats—into off-plan pricing, capturing the premium at sale and speeding permitting under near-zero-energy building codes.[3]https://european-union.europa.eu/index_en

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sharply rising Euribor raises debt-service ratios | -0.8% | National; acute in Madrid and Barcelona high-price zones | Short term (≤ 2 years) |

| Aging population slows net household formation | -0.6% | National; strongest in Castile-León, Galicia, rural Andalusia | Long term (≥ 4 years) |

| Tight coastal & heritage zoning caps new-build supply | -0.5% | Andalusia coast, Barcelona heritage districts, Balearic Islands, Valencia coast | Long term (≥ 4 years) |

| City-level caps on short-let licences curb yields | -0.4% | Barcelona, Madrid central districts, Valencia, Seville | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sharply Rising Euribor Raises Debt-Service Ratios

Although 12-month Euribor eased to 2.50% by mid-2024, the swing from –0.50% in 2021 still lifted median debt-service ratios from 28% to 37% of disposable income for variable-rate borrowers. Roughly 180,000 households breached the 40% prudential ceiling, forcing renegotiations that slowed 2023 originations by 22%. Lenders cut loan-to-income multiples to 3.8×, squeezing first-time buyers in cities where median prices exceed EUR 350,000 (USD 385,000). Fixed-rate uptake soared to 48% of new loans in 2024, but fixed rates remain 60–80 bps above floating, eroding purchasing power. Spain’s Mortgage Law lets borrowers switch to fixed without prepayment penalties, protecting consumers yet trimming bank net-interest margins.

Age-ing Population Slows Net New Household Formation

Spain’s median age reached 45.5 years in 2024, and over-65s will constitute 26% of residents by 2035. Annual household creation slowed from 185,000 (2015-2020 average) to 110,000 in 2024 as birth rates fell to 1.16 children per woman. Rural provinces suffer depopulation, leaving supply underutilized and price growth stagnant. Immigration partly offsets the decline in Madrid and Barcelona, yet work-permit processing caps net inflows at 60,000, half the level needed to stabilize the workforce. Developers respond by shifting to smaller one- and two-bedroom units and prioritizing infill sites near healthcare nodes, but overall demand momentum moderates, dampening the Spain residential real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Sales Dominates, Rental Leads Growth

Sales maintained a 77% share of the Spain residential real estate market in 2025 as households continued to prioritize ownership and benefit from grandfathered mortgage-interest deductions of up to EUR 9,040 (USD 9,944) annually. Transaction velocity in Madrid averages 42 days, underscoring liquidity in the resale channel. Yet rental is the fastest-growing segment at a 5.81% CAGR through 2031 as institutional platforms add inventory and municipal caps on short-lets steer capital toward long leases. Barcelona’s removal of tourist licences has already shifted 8,500 units into the rental pool, expanding supply and stabilizing rents. Institutional operators leverage digital signing to cut vacancy downtime, and tenants pay 12–18% premiums for professional management and bundled amenities. Forward-fund structures allow developers to pre-sell entire buildings to rental funds, de-risking projects and aligning delivery with market absorption.

Rental demand concentrates among the 25-35 age cohort, which faces higher down-payment hurdles amid tighter loan-to-income ratios and rising living costs in Madrid and Barcelona. Institutional funds such as Aviva-Layetana and LandCo-Patron, together committing over EUR 1.1 billion (USD 1.21 billion), are constructing mid-market units with CPI-indexed escalators to hedge inflation. Compliance with Spain’s 2019 Urban Leases Act extends corporate leases to seven years, ensuring cash-flow visibility for investors. The Spain residential real estate market size attached to institutional rental is small today but slated for compound expansion as pension funds target housing allocations in their domestic infrastructure buckets. Sustained capital inflow and policy support underpin the segment’s above-market growth outlook.

By Property Type: Apartments Rule, Villas Accelerate

Apartments captured 69% of the Spain residential real estate market share in 2025, reflecting urban density, vertical zoning, and cost efficiencies that keep unit prices within mortgage-eligibility thresholds. Average apartment size fell from 92 m² in 2010 to 78 m² in 2024 as developers optimized layouts to maintain affordability. New-build apartments routinely achieve near-zero-energy targets, adding EUR 8,000–12,000 (USD 8,800–13,200) per unit but qualifying for 20–30% property-tax abatements. Mortgage lenders favor the segment, offering 80% loan-to-value ratios versus 70% for detached homes due to better resale liquidity. Urban regeneration corridors—Madrid’s Valdebebas, Barcelona’s 22@—provide shovel-ready sites, shortening time-to-market and feeding a steady supply.

Villas and detached houses are the fastest-growing property type with a 5.62% CAGR anticipated to 2031 as telecommute flexibility lets professionals migrate to coastal provinces. In Valencia, detached-home sales jumped 10.5% year-on-year in 2024, while Málaga registered an 18% surge, and average villa prices reached EUR 485,000 (USD 533,500). Gated communities integrate communal pools and coworking pods, replicating condominium amenities but preserving privacy. Supply, however, is capped by Coastal-Law setbacks and heritage height limits, which preserve vistas but constrain new lot creation, ensuring price stickiness. Construction costs run 30% above multi-family projects, yet buyers accept premiums for yard space and customization. As high-speed rail reduces travel times, the Spain residential real estate market will see further diffusion of demand into peri-urban and second-home corridors.

By Price Band: Mid-Market Dominates, Luxury Outperforms

Units priced EUR 150,000–400,000 (USD 165,000–440,000) represented 47% of the 2025 transaction value as dual-income households prioritize affordability and mortgage accessibility. The mid-market benefits from NextGenEU renovation grants, which add energy features and capture 7–12% resale premiums, nudging some stock toward higher price strata. Developers focus on two-bedroom apartments under 80 m² to keep gross prices within the mid-tier, ensuring steady liquidity. Mortgage lenders offer preferential rates for EPC-A upgrades, boosting borrower capacity and supporting mid-segment turnover within the Spain residential real estate market.

Luxury, defined as deals above EUR 500,000 (USD 550,000), is the fastest-expanding band at a 6.12% CAGR to 2031, buoyed by EU buyers hedging currency and tax exposure. Marbella’s Golden Mile logged 142 sales above EUR 1 million (USD 1.1 million) in 2024, up 19% year-on-year, and Ibiza villa prices range from EUR 8,000–12,000 (USD 8,800–13,200) per m². Spain’s flat 24% non-resident rental tax for EU buyers and 19% on capital gains compares favorably with France’s 45% marginal rate, encouraging capital rotation into coastal Spanish assets. AML scrutiny extends closing timelines but promotes buyer confidence and pricing transparency. Developers schedule phased launches to pace absorption and preserve scarcity, sustaining luxury premiums in the Spain residential real estate market.

By Mode of Sale: Resale Leads, New-Builds Lead Growth

Secondary-market resales accounted for 58% of the Spain residential real estate market size in 2025, leveraging a mature housing stock where 68% of units predate 2000. Resale buyers value established neighborhoods and cheaper transfer taxes; notary and registration fees average 1.2% of price compared with 1.8% for new-builds. Mortgage banks lend up to 70% LTV on resales, reflecting perceived condition risks, yet still enabling liquidity. Coastal areas with 2000s-era oversupply—Alicante, Murcia—continue to see churn as investors reposition portfolios.

Primary new-builds are expanding fastest at 6.44% CAGR through 2031, propelled by developers unlocking land acquired in the 2020 downturn and benefiting from municipal fast-track permits that cut approval time to 11 months in Madrid. Neinor Homes delivered 1,850 units in 2024 with a 72% pre-sale ratio, while AEDAS launched 2,400 units across 18 projects, signaling supply acceleration. New-build premiums of 15–25% over comparable resales are accepted because buyers value EPC-A ratings, smart-home wiring, and 10-year structural warranties mandated by Spain’s building code. Banks grant 80% LTV on EPC-A new-builds, offsetting higher sticker prices. Consequently, the Spain residential real estate market is witnessing a pivot toward modern stock as consumers prioritize efficiency and amenity value.

Geography Analysis

Madrid retained 49% of national transaction value in 2025, anchored by head-office density, 68% mortgage penetration, and average selling times of 42 days. New-build permits rose 16% year-on-year in H1 2025 after the city extended its fast-track program to projects exceeding 50 units and 15% affordable allocation, reinforcing pipeline visibility. Andalusia, led by Málaga and the Costa del Sol, posted the fastest growth at a 6.28% CAGR outlook to 2031. Year-round temperate climate, high-speed rail connectivity to Madrid in 2.5 hours, and institutional acquisitions such as Stoneweg Living’s USD 93.5 million portfolio underpin demand. Average prices in prime Marbella rose 12.8% in 2024, outstripping national 7.8% growth and cementing the region’s lead within the Spain residential real estate market.

Barcelona commands 18% of value in 2025, but its CAGR cooled to 4.10% after the city voted in June 2024 to phase out tourist lettings by 2028, redirecting investor capital to long-term rentals and nearby municipalities. Sitges, Tarragona, and Girona represent 12% of market value in 2025 with 5.40% growth as buyers seek lower prices yet proximity to Barcelona’s job base. Valencia Community, buoyed by telecommute relocations, logged 10.5% price appreciation in 2024 and attracts about 18,000 net domestic migrants annually. Property-tax abatements for EPC-A builds foster green-development clusters along the Turia River and Marina Real, intensifying supply.

The rest of Spain accounts for 15% of value in 2025 and expands at just 3.80% as depopulation dents demand in Castile-León, Galicia, and interior Andalusia. Nevertheless, Bilbao and San Sebastián sustain 4.50% growth on industrial diversification and high-end tourism. Zoning nuances shape regional pipelines: Madrid’s minimum 15% affordable inclusion fast-tracks approvals, while Barcelona’s heritage reviews extend timelines to 24 months in Eixample. Valencia’s 25% property-tax rebate for EPC-A sites accelerates planning, whereas coastal setbacks in Andalusia cap beachfront new-builds, reinforcing price resilience along prime shorelines of the Spain residential real estate market.

Competitive Landscape

The Spain residential real estate market exhibits moderate concentration as the top five developers plus two large international funds control roughly two-thirds of current new-build pipelines. Traditional homebuilders—Neinor Homes, AEDAS Homes, and Metrovacesa—compete on land-bank optionality, prefabricated construction capability, and geographic spread. Neinor’s ongoing joint bid with Apollo for AEDAS at around EUR 1.1 billion could create the country’s largest residential champion. Such consolidation promises cost synergies in procurement and marketing but raises antitrust commentary around land hoarding.

SOCIMIs like Merlin and Colonial react by pivoting into data-center, life-science, and flexible-living verticals, committing nearly EUR 4 billion through 2025 pipelines. Meanwhile, global funds—Blackstone, Greystar, and Stoneshield—expand Build-to-Rent portfolios, importing North American asset-management techniques and technology. Their scale advantages cover tenant-experience apps, dynamic pricing engines, and centralized maintenance platforms that lift net operating income.

PropTech adoption remains fragmented. Only 37.5% of construction professionals report familiarity with Lean-planning tools, opening competitive white space for modular builders and integrated platform operators. Smaller regional developers differentiate through boutique ESG-certified projects and customer-centric digital sales journeys. Overall, the Spain residential real estate industry is in a transition phase where capital-rich institutions collaborate with tech-savvy upstarts to unlock production bottlenecks and mitigate sustainability challenges.

Spain Residential Real Estate Industry Leaders

Neinor Homes

AEDAS homes

MetroVacesa

Vía Célere Desarrollos Inmobiliarios

Kronos Homes

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AEDAS Homes proposed a EUR 3.15 dividend per share (EUR 138 million total) after posting a record EUR 150 million net profit on EUR 1.156 billion revenue and 3,151 unit deliveries.

- March 2025: AEDAS Homes and Barings launched a USD 198 million build-to-rent portfolio of 650 units across Madrid and Valencia, targeting stabilized yields of 5.2%

- March 2025: LIFT Asset Management raised EUR 50 million for its third reverse-mortgage vehicle, targeting EUR 100 million to acquire 200+ senior-leasing homes across six cities.

- February 2025: Tectum Investment Managers launched a EUR 450 million fund to build up to 2,500 affordable rentals, leveraging 50-75% debt with European institutional support.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Spanish residential real estate market as the yearly dollar value of completed, transferrable dwellings, both new-build and existing, that are bought, sold, or leased for primary or secondary living across mainland Spain and its islands.

Scope exclusion: Agricultural land, social-housing stock retained by public bodies, timeshare resorts, and properties zoned strictly for commercial or industrial use.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Price Band

- Affordable

- Mid-Market

- Luxury

- By Mode of Sale

- Primary (New-Build)

- Secondary (Existing-Home Resale)

- By Key Cities

- Madrid

- Barcelona

- Catalonia (ex-Barcelona)

- Valencia Community

- Andalusia

- Rest of Spain

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed developers, valuers, notaries, prop-tech managers, and build-to-rent fund executives in Madrid, Barcelona, Andalusia, and Valencia. Their insights refine foreign-buyer weightings, expected completion lags, and typical discount rates, closing gaps left by desk research.

Desk Research

We begin with national data sets such as INE house-price indices, MIVAU permits, land-registry closings, Eurostat demographics, and Bank of Spain mortgage releases, which anchor price and volume baselines. News and filings gathered through D&B Hoovers and Dow Jones Factiva flesh out developer pipelines, rental yields, and transaction multiples. These publicly available and subscription feeds supply the backbone of our model; many additional sources are also consulted for cross-checks.

Market-Sizing & Forecasting

The model starts top down; national residential transactions are multiplied by average notarized selling prices and then filtered through residential-only shares, foreign-buyer penetration, and rental turnover. Targeted bottom-up roll-ups of listed developer revenues and channel checks validate totals before adjustments. Key variables include new housing starts, permit-to-completion lags, household formation, disposable-income growth, and average mortgage cost. Multivariate regression married to scenario analysis projects values to 2030. Where provincial data are sparse, ratios from matched provinces are imputed and flagged for analyst review.

Data Validation & Update Cycle

Outputs pass variance tests against INE indices and banking-flow trends, are peer-reviewed, and then signed off by a senior analyst team. We refresh every twelve months and issue interim updates for policy shifts such as rent caps or tax incentives.

Why Mordor's Spain Residential Real Estate Baseline Commands Reliability

Published market values vary because firms choose different segment mixes, currency years, and model refresh cadences.

Our disciplined scope, price-volume pairing, and annual updates reduce those pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 169.22 B (2025) | Mordor Intelligence | - |

| USD 179.30 B (2024) | Regional Consultancy A | Includes off-plan units and capital-gain mark-ups |

| USD 165.79 B (2024) | Trade Journal B | Relies solely on registry data; excludes rental turnover |

These comparisons show that by tracking only realized transactions and maintaining a documented review cadence, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can depend upon.

Key Questions Answered in the Report

How large is the Spain residential real estate market in 2026?

The Spain residential real estate market size reached USD 170.12 billion in 2026.

What is the expected growth rate for Spanish residential property through 2031?

Market value is forecast to rise to USD 179.10 billion by 2031, delivering a 5.28% CAGR.

Which Spanish region is projected to grow fastest in housing transactions?

Andalusia-Málaga leads with a 6.28% CAGR forecast through 2031 due to climate appeal and transport links.

Why is institutional build-to-rent expanding in Spain?

Pension and insurance funds favor CPI-linked rental yields, professional management, and supportive municipal policy that redirects tourist rentals to long-term stock.

How does the end of Spain’s Golden Visa affect foreign demand?

While the Golden Visa ended in 2025, digital-nomad visas and stronger EU buyer interest continue to support luxury coastal purchases, sustaining growth in the high-end segment.

Page last updated on: